When it comes to investment, everyone is conscious and curios to know about the best investment products. In this article I’m going to tell you about few of such products that I know and I thing they will be helpful for you.

1. Term Insurance

Term plan is an affordable insurance which provides a full protection cover for your family at a very low premium cost. One of the best products in Term insurance markets I know is SBI life Insurance Shield Plan.

Before taking any Insurance into consideration, we should give importance to

Premium amount you pay : Premiums are among the cheapest in market

Claim settlement Rate : Next only to LIC

There Shield plan is designed very nicely, have a look at it and you will love it.

2. UTI Gold ETF’s

It is simply an investment in gold which tracks it’s price on day to day basis. It has its own expense ratio which is very high is compared with US market, but it is the price that we pay to invest in gold electronically. You should have a demat account to invest in Gold ETF’s and you can trade these ETF’s through stock market.

If you want to invest in GOLD, try this ETF, search GOLDSHARE or UTGOLD (if you are on ICICIDIRECT).

3. Mutual Funds

Mutual funds are categorized on the basis of its objectives, style and strategy. Investing in Mutual Funds only is not enough to get good returns. You should know about the types of mutual funds and then invest in different funds by deciding your goal.

See here some of the good options of mutual funds to invest in :

We are going to discuss today, a huge wealth creation by investing with discipline over long period of time. We often think that investing a small sum of money will not be able to generate huge Wealth and we need to invest huge amount of money.

Creating Wealth

Its obviously true that more money will create more wealth, but we are going to see today that we underestimate small savings and how small investments over a long period of time can generate fortunes.

How much wealth you can create, if you earn around $1000 /month (Rs.40,000 per month) and can invest 10% of that amount every month for next 30-35 yrs. I am assuming you are a 25 yrs old and retiring at the age of 60 (though i want to retire at 40). Total dependents are 3-4.

And monthly expenditure is Rs.25,000 ($600/month).

What kind of wealth can this person create?

Can he invest Rs 5000 ($125) in a diversified Equity Mutual fund per month till his retirement. I hope the answer can be YES

As we said that he is investing in Equities, What kind of return should we expect? 5% , 20% or 50%, but Wait … Equities are risky, it can be negative also !!! that’s very true … but People may not know that Equities are extremely risky in short term, but its almost not at all risky in long term, and if the long term = 35 yrs, then forget it, you can get some great returns.

Risk in Equities are inversely proportional to the investment tenure. Well that’s a different topic to talk about (And i will post an article on that soon , keeping an eye !!!) Just for the data, Indian Stock markets have given return of 17%+ CAGR return in 28 years, from 1979 (inception) to 2007. We are talking about Sensex.

So, to be safe we can easily consider 15% CAGR return in Long term (remember LONG TERM).

Coming to the point, It may happen that during initial years, our investor may face difficulty investing this much money considering, he may have other important things to take of and later he may have more responsibilities. But during is career life, his salary will also rise and then 5000 will be a small percentage of his salary.

So assuming he can do the investment we are proposing, what kind of retirement corpus he can build? Guesses?

I am sure most of the people will be thinking the following way:

He invested 5000 * 12 in a year, which is 60,000, and then he does it for 35 yrs , so he invests total of 60,000 * 35 = Rs 21,00,00 0 (21 lacs). And he will get some return of 15% every year. if we take 15% of this 21 lacs, it will be around 3,00,00, so total corpus = 24,000 and also as this is compounded , his interest will also keep growing at 15%, so it will be more than 24,00,000 , so lets take it 50,00,000. Fine …

Ok , let take 70,00,000 (70 lacs) to be safe. This is a calculation done not exactly by the proper annuity formula, but a workaround, which a general person can think of.

How much does he generate with this strategy

You can also look at my another article on Early investing and power of Compounding to get an idea about early investing and how compounding is a great tool. But keep going ahead if you are enjoying this article.

So the question is What will be his corpus , can it be anywhere near to 70,00,000 . The answer is that his actual Wealth will be way beyond this amount. After doing the actual calculation i can see that it will come around 7.43 Crores (Rs 74 million) .

But how is it possible , such a big amount !!! .

That’s because of compounding power . The interest earns interest and that again earns interest and this keeps on going. Initially the interest earned is very small , but as the time passes , the amount keeps growing and the interest also grows at an unbelievable amount.

Can you believe that this investor will earn more than 1.04 Crores only in interest in his 35th year (last year) , more than 4 times the money he actually invested whole his life. That’s all possible because of systematic and consistent investing with out fail and because of Power of compounding.

That’s the reason why one of the greatest ScientistAlbert Einstein said “Compound interest is the 8th wonder of the World”.

So it that all we are going to talk about today , NO !!! We have more to talk on this topic.

Why does this investor takes pain of investing that 5,000/month all this life. What if he invests just 10 yrs and leaves that money to grow for another 25 yrs. What if this is his plan till retirement.

The sudden thing which will come to your mind is that he invests for 35 yrs and created wealth of 7.43 crores , What if he just invests for 10 yrs .. it should be 10/35 * 7.43 crores = 2.12 Crores . Is that true ?

Will it actually be 2.12 Crores only. The answer is NO !!! . Then the question is how significantly different will his Wealth be in this case. The Answer is 5.88 Crores. Yes it will not be significantly less but just 21% less .

So Just by not investing for 71% tenure he actually gets 21% less money , that’s not a bad deal !!!

But wait , What if he wants that same 7.43 crores at the end , and still wants to invest for 10 yrs. the obvious way out is to invest more than his regular 5,000 per month . The question now is HOW MUCH MORE !!!

The answer is Rs 1420 more . Instead of 5,000 , he should invest Rs 6,420 per month for 10 yrs and then leave the money to grow for rest of 25 yrs. And he can generate wealth of Rs 7.43 Crores.

Watch this video to know how one can use Equity to create wealth over long term:

What we can learn from this

So there is a learning here and a very important thing to note , that more pain we take in the start , the better it is . In the initial years of career , its possible for people to invest more , as they have less responsibilities to handle and less dependents.

So it may be feasible for them to invest heavily in the initial phase of there career, which will benefit them for long term . Now see this person . Instead of investing 5,000 for whole of 35 yrs , If he chooses to take a little more pain in the initial 10 yrs and manages to invest Rs 1,420 more per month, then he can save investing for 25 yrs of his life and still can generate same Money.

One great question now !!!

What if our investor is ready to invest his 50% salary (20,000) per month for starting 2 yrs and then let it grow for rest 33 yrs. He is ready to heavily invest first 2 yrs of his career and do some sacrifices like not spending too much , no vacation , no fancy spending and all.

Can he still beat the target !!

Will he be able to generate the same Wealth for himself like in earlier examples !!

So here you go !!! , He will not only achieve the target , but exceed it.

His Wealth will be 9.24 Crores (Rs. 92.4 million) at the end of 35 yrs. I know that’s an Eye-opener . So now you know that the best time to invest was 5, 10 or 20 yrs ago , but if you missed it , don’t worry 🙂 . there is another golden chance and that’s NOW !!! .

please let me know what you feel about this article , that helps me to refine and write better articles.

Do you want to invest your money more safely? Here is one of the best options for you. ETF i.e. Exchange trade funds are one of the safe way of investing your money in equity market.

It is an investment fund traded on stock exchange, much like stock. These are attractive investments because of their low cost and stock like features. It offers both tax efficiency and lower transaction cost.

What are ETFs?

Exchange Traded Funds are a basket of securities that are listed and traded on a recognized stock exchange. Simply, they are mutual funds, whose units can be bought and sold on the stock exchange.

Given that an ETF is traded on the stock exchange, its price may not necessarily be the same as the NAV of the underlying portfolio. In other words, an ETF could have an NAV distinct from its market price. The reason being that the market price is usually driven by the demand and supply of units.

Hence there is a distinct possibility of an Exchange Traded Funds units trading at a premium or discount to its NAV.

For Example Nifty BeES , whose underlying is NSE , may not have same price as its underlying , For example if Nifty is 4500 , it may be possible that The ETF’s value is 4600 or 4400 , depending on the sentiments and expectations.

Watch the video given below to know the current status of ETF in India:

How does ETF work?

Exchange Traded Funds are just like stock exchange. For that you need to open a Demat account by any medium like through bank, online brokers or through any consultancy. Check for the prize value of the share so that you will know which of them are in your budget and then you can buy or sell your shares at any time you want to.

It is so easy like suppose you buy some shares at 10:30 in the morning and sell it at 12 pm. then again you can buy another shares after lunch.

Benefits of ETF

ETF’s are the low cost simple solution for the generating good returns from stock market investment. The benefits of ETF are as Given below.

1. Easy to access:

ETF’s can be purchased with just a single transaction. In EYF’s you are buying mini portfolio’s so it is way more easier than buying a basket of Indexes.

2. Cost effective:

Commissions are generally low on ETF as compared to the other tools. Besides this it there is no load fee’s and managing fee is also very low.

3. Transparent:

The most important thing of your investment is transparency. You should know where have you invested your money and how’s it performing. In Exchange Traded Funds, your portfolio details and underlying are publisher daily.

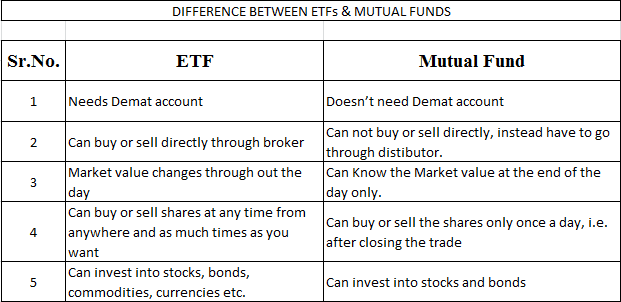

Difference between ETF and Mutual Fund:

Many beginners get confused between Exchange Traded Funds and Mutual Funds. Though ETFs are part of mutual funds, they are different in many aspects than Mutual funds. Lets see some of the differences between Mutual fund and ETFs:

ETF’s in India

Nifty BeES : Tracking NSE

Quantum Index Fund : Tracking NSE

ICICI SPIcE Fund : Tracking BSE

Bank BeES : Tracking CNX Bank Index

GOLD ETF’s or G-ETF’s

Gold ETF’s are the simple investments products that combines flexibility of stock investment and simplicity of Gold investment. Gold ETF’s are different from Gold savings.

IT tracks Gold prizes. Gold ETF’s are one of the best form of Gold Investments. Earlier investors used to invest in gold in metal form. Then comes paper bond and now you can invest in gold through electronic form.

BENEFITS OF GOLD ETF’S:

No risk of impurities.

Flexibility in buying Gold. Like one can buy in smaller lot.

Held in electronic form.

No storage cost.

No security concern like in physical form.

Transparent pricing and potentially cheaper.

Can track your investment values in real time.

No wealth tax like in Metal form.

Advantages of ETFs

1. ETFs tend to be more cost-effective vis-a-vis comparable mutual funds. The expense ratio of a passively managed ETF (tracking a benchmark index) would normally be in the range of 0.50%-1.00%; for an index fund, it can be as high as 1.50%. And for mutual funds the entry load is 2.25% .

2. ETF’s can be bought and sold anytime during the market hours , unlike the Mutual funds NAV at the end of the Day.

3. Given ETFs are traded on the stock exchange, and can be bought/sold on a real time basis; they tend to have low tracking error (deviation of ETF’s performance from that of the underlying index) as compared to index funds.

Disadvantages of ETF

1. Investors need to have a demat and a trading account, with a SEBI registered stockbroker, for investing in ETFs

2. Costly to operate – You need demat account to buy ETF and the charges for demat account might compensate the low expense ratio of ETF. One of our blog readers comments on that

While promoting ETFs it is argued that their 1% edge of expense ratio over mutual funds will be significant if it is compounded over a long period of time, say 20 years. So this advantage of less expense ratio is not there if the calculations in the previous comment are true. What I am trying to say is that the only advantage that ETFs have is that they are like mutual funds that will guarantee market related returns. Nothing less and nothing more.

If you have any query related to this topic you can leave your reply in the comment section.

There is no doubt that 40% is more better return. But is it a right way to judge the return just by seeing the number. we ignore another important factor called as “RISK” involved. In most of the cases, people really don’t consider evaluating the return in relation to RISK taken to earn that kind of return.

Which is better?

1. 30% with High risk

2. 20% with moderate risk

In this case , 2nd is better than 1st , as the Return per unit of risk is better than the 1st case. (considering High risk is 3 units , and moderate is 2 and Low is 1 .

So the actual measure of return should be, Return per unit of risk

REAL RETURN = ABSOLUTE RETURN / RISK TAKEN

There are many balanced mutual funds which have given little less return than diversified equity funds , and hence can be called as much better investment tolls because there was much lower risk involved with them , in case there was any fall in markets , these mutual funds would have fallen less than equity funds. Many mutual funds advertise there products only on the basis of returns and don’t care to tell investors that there is high risk involved with the products.

If you are given 2000 for climbing a tree and 5000 for jumping from one building terrace to another , the first choice is much better. In that case you don’t go for the second option just looking at 5000.

If today all banks start giving 12-15% assured return on Bank deposits, Equities investments will fall to great extent , because bank deposits will have much better returns considering the risk involved. I would be happy to read your comments or disagreement on any topic. Please leave a comment.

There are many things we hear and believe , but they are little different in reality, which helps if we know.

– Do you know that When you take an SIP for 6 months or 1 years or for any period , the first installment (which you make by cheque) is not counted for inside the tenure of your SIP. So if you take a SIP for 6 months , you make 6 payments other than your initial payment with cheque , so total is 7 payments.

– The short term capital gain period is 1 yr , means 365 days , but it does not work exactly that way , its 12th month other than your buying month. Means if you buy shares or MF on 12th May , 2008 and sell on 13th May , 209 it is still short term capital gain , to call it long term capital gain , it must see it after 12 months after May , 2008 (your month of buy) . which means you shall sell it on or after 1st June 2009.

– Suicide is also covered in Life Insurance after 1 yr of policy (atleast its there in my policy with SBI Life Insurance).

– ULIPS : The deductions availed under sec 80C is taken back if you surrender your ULIP before 5 yrs. If you surrender your policy in 4th or 5th year , then all hte premium paid till date will be added to your salary for that current year and you will have to pay tax on that too. ULIPS just put restriction on paying of premium fr the first 3 yrs, but offer tax benefit under 80C if you hold it for minimum 5 yrs.

– If you repay your housing loan by taking another loan , you can continue to claim tax benefit on the interest amount paid for new loan under sec 24.

– Tax deduction is available for the prepayment charges paid for the home loan .

– Dividend distribution tax is levied on the Dividend which you recieve , and it also affects the fall in NAV . So NAV falls not just to the extent of the dividend declared , but also by the tax which mutual fund company pays to govt (12.5% on dividend + 2.5% surcharge also , under sec 115-O )

I would be happy to read your comments or disagreement on any topic. Please leave a comment.

Finally many people like me have chance to take take plunge in the rising and booming Real estate sector , Any one who does not have Crores and Lacs to invest in flats , plots etc , to earn the capital appreciation will to be able to invest even small amounts like 5,000 or 10,000.

What are Real Estate Mutual Funds ?

They are simple close ended mutual funds which will invest in Real-estate , as simple as that … The lock in period will be 3 yrs. These REMF will invest in properties and they will be owners of those properties , they will also rent out these properties and pass on the rents to the investors as dividend. And when the mutual fund matures , it sells its holdings and pay us the returns.

REMF’s will be listed on Stock Exchanges and they will be traded just like shares.

How do they work exactly ?

Lets take simple example :

You invest Rs 20,000 in some ABC REMF and one unit costs Rs 10 at the start , so you get 2000 units. many people like you will also invest and Suppose the total money they get from investors in 10 crores. Now they invest this money as per the laws defined for them. Suppose they receive 50 lacs as rental income from their investments in a year and the total investments has grown to 12 crores (because of rise in value of properties and other factors).

From this 50 lacs they will distribute dividend and you will recieve your share for 2000 units and the unit value will be around Rs 12.

Rules and Restrictions for REMF’s

– They will have to invest atleast 35% in completed projects , ready flats , shops , houses etc.

– At least 75% should be invested in real estate and related Securities.

– They can partner with real estate developers and invest maximum of 15% in the project (not in company).

– The NAV will be published on daily basis.

– Most probably they will be in category of debt funds. Tax treatment not clear at the moment.

– Further caps will be imposed on the fund on investments in a single city, project or securities issued by associate companies and sponsors. Funds are not allowed to invest in assets owned by the sponsor or the asset management company or any of its associates during the last five years the aforesaid entities hold tenancy or lease rights.

– The cities for investment by real estate mutual funds would include 35 cities in million-plus urban agglomerates and 27 under the million-plus category as per the Census 2001

They are still to be launched , keep a watch !!!

I would be happy to read your comments or disagreement on any topic. Please leave a comment.

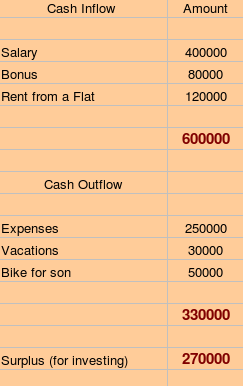

What is Financial Planning? Its a little stupid definition, but its just planning you finances. You plan your Investments in such a way which meets your financial goals over time.

You must be very disciplined when you do this, you must know from where you the money is going to come to you and how are you going to save or invest it, and in future how are you going to achieve your goals.

Steps in Financial Planning

1. List down your Goals

Prepare a list of financial goals. It can be any requirement like Buying Home, Car, Child Education, Child Marriage, Vacation, Retirement etc. Along with this there must be a very clear timeline associated with the Goal. Something like “I want to buy a Car after 3 years, which will cost 10 Lacs at that time”.

2. List down Your Cash Flows

Prepare the list of your cash flows, cash flow means, how money is coming and going? Any money coming in is Cash inflow and Any Expenses is Cash outflow.

It it help you understand how money is coming to you and how is is utilized and how much is remaining for investing purpose.

Example (yearly) :

By Doing this , you can get very clear of how you are going to get money and how you are going to spend it, and how much you are left with to spend.

3. Understand and figure out your Risk-appetite

This is a very important part of financial Planning, Risk appetite is the amount of risk a person can take while investing. How much money you can afford to loose in order to earn high returns defines your risk taking ability.

For Example:

If you are ready to loose 60% of your money , your risk appetite is high

When you are ready to loose 25% of your money , your risk appetite is moderate

If not at all ready to loose your money even 1% , you are not at all a risk taker.

It depends on you which category you belong in. it depends on individuals Psychology, Family Conditions, Attitude etc.

Generally people in there early age have more risk appetite as they have less responsibilities and more freedom to invest. Later when they get married and have responsibilities, they cant risk money to loose.

4. List down your Financial Goals

At this point, you must be clear with your goals. Financial goals are the list of things for which you need money and you must have a predefined target time.

Example:

Ajay earns Rs 3,00,000 per year with Rs 1,00,000 left for investment, he has moderate risk appetite.

Goals:

1. Buy a Car within 2 years worth 5 lacs.

2. Vacations in New Zealand worth 8 Lacs within 4 yrs.

3. Buy home worth 40 lacs in 10 years.

Here, Goals are not compatible with amount invested per year and with that kind of risk-appetite.

Therefore, Goals must be realistic and achievable, it must not look totally irrelevant.

Watch this video to know the financial planning services by Jagoinvestor :

5. Make sure your Goals are realistic

At this point you must make sure that your goals do not look unrealistic and unachievable. If they do, then you must either lower your goals or increase risk appetite or increase the investible amount per year. This gist of the matter is, Be Realistic !!!

6. Make the Plan

Once you are done with all these steps, Its the time for the planning.

But for a short term goal like vacation in 1-2 yrs, don’t invest in equities, rather go for a debt fund or a fixed deposit.

In this way, you have to be clear how you are going to invest for achieving your goals.

7. Review and Take advice

Revise your steps and make sure everything is correct. If you are unclear about anything meet some one who is more knowledgeable than you, See a financial planner or a knowledgeable friend.

8. Take Action and keep Reviewing

The last step is to take Action and start executing the plan with discipline and make sure you change you goals, risk appetite as time passes and these things change over time.

I would be happy to read your comments or disagreement on any topic. Please leave a comment.

Do you remember the price of a movie ticket or any or your favorite thing few years back? It is the same today also? I don’t think so. It has increased by some numbers. This increase in the price is known as inflation. In this article I’m going to tell you what is inflation and how it can affect your investment.

Inflation :

Inflation is the increase in the rate of prices caused because of devaluation of the currency. Is is also known as the decrease in purchasing power of the currency.

Its a tool to measure the increase in prices. If inflation is 6%, it means on an average the prices have increased by 6%, means anything which had cost of Rs.100 last year will cost 106 this year. (Its a average price and not exclusively for some item)

For example:

Considering inflation at 6%, the value of Rs.100 will go down to Rs.53.86 in 10 yrs and to 29.01 in 20 yrs. In order to keep value of you money same, the absolute return earned must be greater then inflation.

Inflation vs returns on different financial products

Fixed Deposit :

Investing in Fixed Deposits just retains its value, but people feel that they get good returns upto 8.5 or 9.0%.

There is a tax of 3.5% on your FD returns and then if you adjust inflation of 6% after that, you will realize that though your Rs.100 has become 109 in a year, you have to pay 3 or 3.5 tax on that, and then if you have Rs.106 after that, you can purchase the same thing which you could have purchased in Rs.100 a year ago.

Hence, FD don’t give returns in real sense, they just keep your buying power. (considering inflation + tax = return from FD)

Gold investment :

Investing in GOLD is considered the traditional way of investment and also it is consider as the best way to beat inflation. Historically Gold has always outperformed inflation. It has generated 13.66% annualized return since 15 years, which is almost double of the inflation rate.

See the graph given below, in this graph the returns of gold investment since 20 years is given. You can see that how gold prices have moved or increased in last 2o years.

Image source: www.Bemoneyaware.com

Cash in bank :

The worst thing one can do is to keep Cash in Bank account, instead of investing it in any product. The returns generated from this saving can not beat the inflation rate.

For example: Suppose you have some cash in your savings account on which the interest rate applicable is around 4-4.5%, whereas the inflation is around 6%. Here the returns can not even meet inflation rate.

Cash must only be kept to a limit which may fulfill your emergency needs (preferably 3 times of you salary). Any extra amount must be invested.

Mutual fund :

Mutual fund is an investment in stocks so the returns are volatile here but if you consider it as a long term investment product then you will realize that it has given returns way higher and beat the inflation rate by almost double.

So this is the difference between the inflation rate and the returns of different financial or investment products. Now you can compare the returns and choose which product is suitable for you to invest in.

We can help you to improve your portfolio by making a perfect financial planning for you. If you have any doubt or query you can ask us by simply leaving your concern in our comment section.

There are 3 Mutual Funds Options (Growth , dividend , dividend Re-investment) and we will discuss those today. There are lot of misconceptions and myths which add to confusion in the world of mutual funds and agents use it against investors and make them fool …

Different Options in Mutual funds

1. Growth Option

Under this option you get the units at the time of buying and you have same number of units till the end. The NAV keeps changing according to performance.

2. Dividend Option

This is the most misunderstood option in mutual fund.

Dividend option in mutual funds means that you will be repaid some amount of your investments every year and it will be called as “dividends”, this helps those people who want some regular returns every year from their investments in mutual funds.

People think that dividend is something extra which they receive other then their investments which is not true 🙂

Dividend is declared per unit basis, if you have 100 units and MF declares dividend Rs.4 per unit, you receive Rs.400, and you think that your earlier investments have the same worth, where as it decreases by the amount you receive as dividend, because its paid out of your investments only.

The NAV of the unit goes down after paying dividend proportionately.

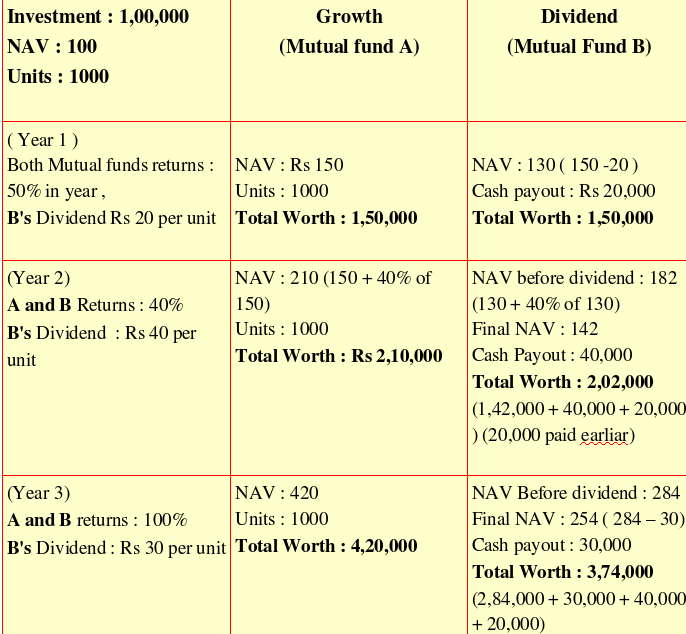

Example : Let assume you have Rs 1 lac of units in a mutual fund with NAV of Rs 100, you will have 1000 units. dividend declared : Rs 20 per unit

How it works :

You will get Rs 20,000 and then your remaining worth will be Rs 80,000 and as you have 1000 units, the NAV will go down to 80. So your actual worth is same as Rs 1 lac. The only advantage to you is that you are getting liquidity with your investments and getting regular cash every year, unlike growth option.

Agents generally lure investors to invest in NFO’s claiming that if company declared dividends, they will get more dividend compared to existing funds as they will have more units, Which is nothing but a idiotic myth 🙂

3. Dividend reinvestment

In this option ,the step is as follows

Re-adjust the NAV assuming that dividend is paid.

After that buy more units of same MF with that dividend money and allot it. So ultimately the number of units increases and the NAV goes down. In this case dividend money is not given to the investor but re-invested in the same scheme.

Example : Let assume you have Rs 1 lac of units in a mutual fund with NAV of Rs.100, you will have 1000 units. dividend declared : Rs.20 per unit

How it works :

Your dividend will be Rs.20,000 , and NAV will come down to Rs.80 like it happened above. Now this 20,000 will be re-invested in same mutual fund and you will get extra 250 units (20000/80).

Your Total units = 1250

NAV = Rs.80

Worth = 1250 * 80 = 1,00,000

Which one is better Dividend or Growth?

It depends. There is no thumb rule to decide which one is better then the other, it depends on the situation and your needs.

Watch the video to learn more about growth and dividend option:

When is Growth Option better?

If you are a person who earns well and does not need regular money back from your investment and if you are looking at long term investments then growth option is best for you because your investments gets compounded, which does not happen on the dividend part in dividend option as it goes back to investor and its never part of future growth.

When is Dividend Option better?

If you are a person who need regular money every year from investments for some purpose, It may happen that you have more responsibilities and more dependents and if any small money which you get extra every year is helpful to you , in that case you can go for dividend option.

Conclusion : Different options in mutual funds are for different types of investors, before investing just see what do you want from your investments and take appropriate option.

Returns in long term from Dividend and Growth :

Below is an example which shows the returns from similar funds with growth and dividend options and there performance over 3 years.

I would be happy to read your comments or disagreement on any topic. Please leave a comment.

SIP is a way of investing in Mutual Funds where you pay a fixed amount each month for a fixed tenure.

Like If you take an SIP of 5,000 for 1 year on Jan 1, 2008, you will be paying Rs 5,000 per month for next 12 months.

Please understand that its not a financial instrument, but a way of investing in mutual funds, some people confuse SIP with PPF, NSC, and mutual funds, they think they can invest in “SIP”, its just a mode of investment.

SIP CALCULATOR :

When to invest in mutual funds through SIP?

Investment through SIP must be done only when markets are uncertain or very volatile, when you don’t know which side they are headed to ..

SIP will be beneficial only if markets really are volatile or going down after you invested. If it happens that markets turns bullish and starts going up, in that case SIP will not be beneficial and will give less return compared to lumpsum investment in start.

SIP is a simple concept and hence very powerful, lets see some reasons why its worth investing through SIP

Reasons to invest through SIP in Mutual Funds?

More convenient for average person on wallet

Its more easy for a person to invest in small amount every month, rather than a lump sum amount. Investing through SIP is lighter on wallet. Its easy to pay Rs 5,000 per month for 1 years, rather than investing 60,000 at a same time.

It brings your average cost price for unit down (in volatile market)

The biggest advantage of SIP is this part, There is a concept of rupee-cost averaging, In SIP you buy less when market and NAV are UP and you get more units when they are low. When this happens, the average cost of per unit is lower.

Lets take an example of “Ajay” who invests 1,000 per month through SIP starting Jan 2, 2007.

How SIP helps in this case ? See the result below :

ADVANTAGES of SIP

Makes you a disciplined Investor

The other advantage of SIP is that it makes you a disciplined investor. Once you start SIP, each month you have to contribute certain money in mutual fund and that habit is cultivated.

DISADVANTAGES OF SIP :

It will not work in bullish markets or when market goes up over time

When market goes up and keeps growing over time, the units bought every time will be at high price then the previous one, which will ultimately bring the average cost up , compared to the lump sum investment at the start.

In case of tax saving fund, the lock in period gets extended for every investment.

Tax saver mutual funds lock your money for 3 yrs, When you invest through SIP, each of your investment is locked separately for 3 yrs from the date of investment. So if you pay your first installment on Jan 2007, it will locked till Jan 1 2010, then the installment paid on Feb 1, 2007 will be locked till Feb 1, 2010 and like this each installment will be locked with the gap of 1 month.

In which type of markets do you think SIP will not work?

If you have any query related to this topic you can leave your reply in the comment section.