This is a guest post by one of our readers and our financial planning client Mr. Rahul Udare from Mumbai.

He is CA by profession, and he has created a 45 min excellent video for beginners on the topic of Income Tax. This video below will help anyone understand various things related to income tax and returns and how everything works.

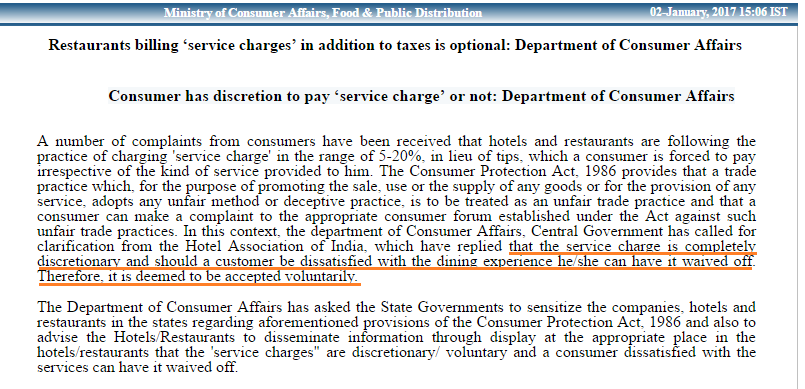

Govt has clarified that the “service charge” is optional and customers can refuse to pay that if they feel like.

For some years, most of the restaurants and hotels have started charging “Service Charge” along with the other taxes in their bills and us customers due to lack of understanding feel obligated to pay it.

However, the govt has issued a notification today which clearly mentions that if the customer is not satisfied with the experience at the hotel or restaurant, they can choose to not pay it. Below is the video clip of this news

Govt Notification

“A number of complaints from consumers have been received that hotels and restaurants are following the practice of charging ‘service charge’ in the range of 5-20%, in lieu of tips, which a consumer is forced to pay irrespective of the kind of service provided to him,” the ministry said in the notification below

Note that the Hotel Association of India has themselves clarified this point.

Why do restaurants charge “Service Charge”?

For those who don’t know this, the service charge was mainly introduced to replace the tips given to the workers (waiters etc), so instead of your giving the tips, the restaurants charge a fixed charge (5% – 20%) and its distribution among the employees.

However, there is no strong proof that most of the restaurant owners actually distribute it among employees. Also irrespective of the service and experience, the customers pay this service charge.

But now after this clarification has come, you can freely tell the restaurant that you will not pay this charge if you didn’t have a good experience at the hotel or restaurant.

I got a fraud call recently and I was able to record it.

The person at the other end was posing as RBI officer and said that because I have not linked my Adhaar card with my bank account, they are getting closed and if I want to save them from not getting blocked, I will to do some verification on the phone call.

Watch the video below which as my recording!

Never reveal your critical information on a phone call

Never share the following things ever on a phone call with anyone

If you listen to the audio, you will realize that the person on the other side many times told me that the CVV number and account number is my personal information should not be shared with anyone. They do this to give a feeling that we can trust them and they are really some official people.

However, these people do not realize that their way of speaking and the language is such that it’s hard to believe that they are really some authorized person.

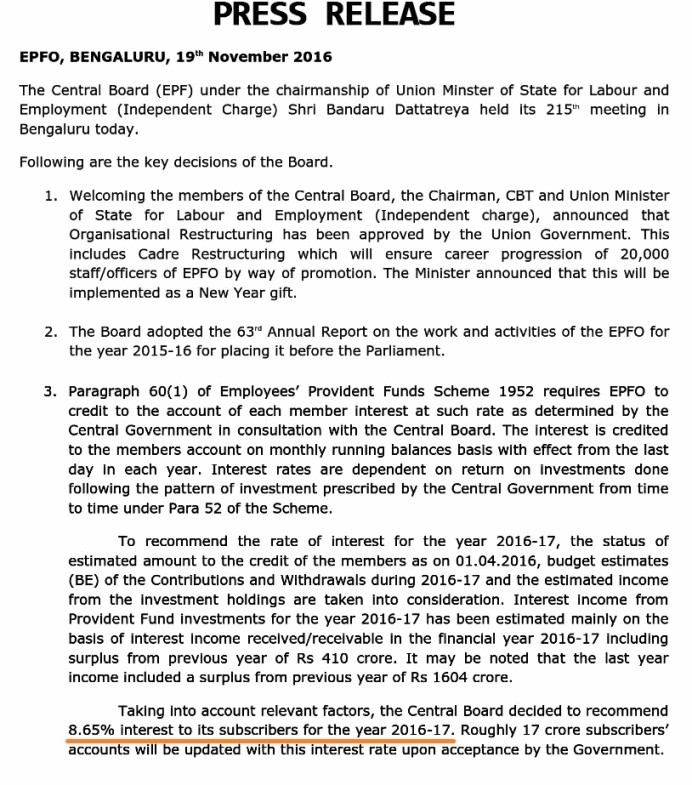

The EPFO department (Employees Provident Fund Organisation) reduced the EPF interest rate to 8.65% today. The old interest rate was 8.8%.

This interest will be applicable for the deposits made for financial year 2016-2017. Which means that all the deposits which were made after 1st Apr, 2016 by the employers will be earning the interest of 8.65% only, and not 8.8%.

While an interest rate of 8.62 per cent would allow the EPFO to keep a surplus of around Rs 22 crore, fixing the interest rate at the present rate of 8.8 per cent would have left it with a deficit of Rs 700 crore, EPFO’s income projections showed.

According to sources in EPFO, the lower interest rate is on account of poor rate of return on investments made by the EPFO on all fronts.

You will notice that the bank deposits interest rates were also reduced recently and this move might be in tune to that decision, as it’s tough to provide high interest as the money availability is high.

Can you name a billionaire who didn’t start a company?

Or a $ millionaire for that case?

In this article, we are going to talk about various ways people become RICH. No, it’s not a tutorial on how to become rich, but just a conversation on are various ways using which people have become rich. Maybe you will get some idea of which path you want to take or try for yourself.

#1 – Starting a successful business

One of the ways, most people become rich is owning a successful business. Yes, think of any rich person and chances are that they own a business. It can be a tech company, a big store or some kind of traditional business, but it’s BUSINESS.

A job gives you linear income and growth. The business gives you exponential growth and income over time, along with the huge risk of losing the money. That’s the primary reason why most of the people are into jobs and not business.

My point is simple. If your goal is to be in the middle class or higher middle class, you can continue doing your job. However if your dream is to own that exotic villa, or to drive the most amazing cars and never worry about money all your life, you need to own a business, otherwise, it’s going to be really tough to get rich (apart from other 9 points)

#2 – Let someone else run business and get a share

A lot of people have become extremely wealthy by investing money in other business and just holding the shares for long. No, this is not stock investing.

I am talking about funding others’ businesses and keeping a share of ownership to cash on in the future. This is definitely not very common or an easy thing to do. The failure rate is very high, but many people have become very rich through this method.

Paytm Founder sold 40% equity for 8 lacs many years back

For example, you have heard about PAYTM. Right?

You know it’s now a multibillion company and its owner is already a billionaire. But did you know that years ago, there was a guy who helped paytm founder with Rs 8 lacs and in exchange took 40% of the company and exited the company with a couple of 100 crores?

Watch the interview with Paytm founder Vijay Shekar Sharma, where he shares about his journey and this incident (Just click the video and watch the next 1 min)

It’s not always the case that you have to start the business, the main point is to be part of a business and contribute in the journey of the business since the start when it was not successful.

Most of the people who joined large companies as employees got equity in the company (ESOP’s and stocks) and years later when the company becomes big, they all became rich.

Take Infosys for example, It was a business owned by a few people, but those who stayed with Infosys and contributed for its growth over years were rewarded and now they are quite RICH.

At Infosys, drivers, electricians are millionaires

The Infosys management has over the years rewarded selected staff belonging to the C, D and E grades with shares for faithful service and excellence in work. By the time Infy began skyrocketing in value, 67 of these people including eight drivers, owned enough stock to make them very rich men indeed. Kannan’s portfolio of 2,000 shares when multiplied by the latest share value makes for a huge value statement

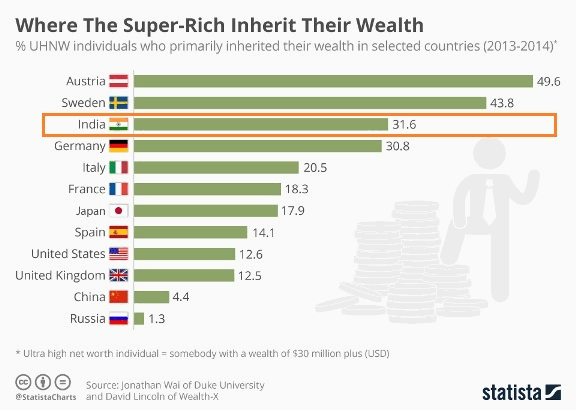

#3 – By Inheritance

Another way a lot of people become rich is when they inherit a lot of money from their parents or some relative. As per this report, around 31% of ultra-rich people in India have inherited their wealth, which is quite a good number. Every 1 out of 3 people in an ultra-rich category is rich through inheritance.

However, this option is not applicable to most people like us.

#4 – Become a highly paid top executive

If you are very clear that you do want to own a business and will keep continuing doing the job, then your salary is the most important factor which can make you rich. No, we are not talking about packaged of Rs 10 lacs or 20 lacs here.

We are talking about packages which some top executives earn at important positions in the company. They are people like

CEO

Managing Directors

Vice Presidents

Top Managerial Positions

Top-Level Professionals (Doctors, Lawyers)

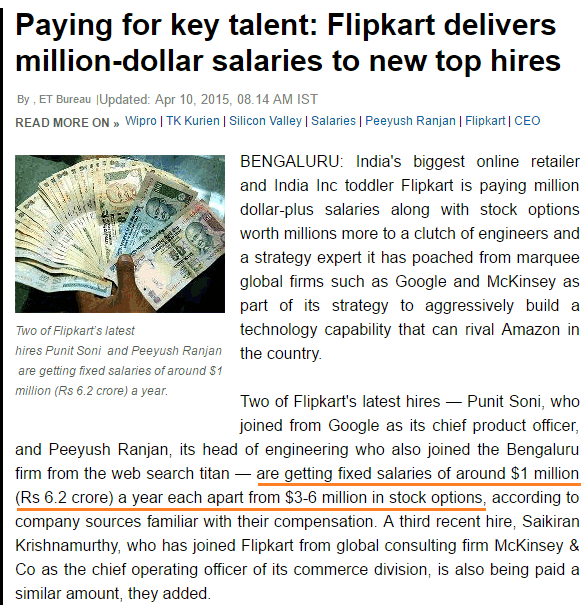

It comes only when you are really out of the class in what you do. If you have skills to manage the company or help a company excel at something, you can reach these top positions, but it takes quite an amount of hard work, smart moves and a bit of luck too. Many professionals earn very high salaries like examples below.

Here is another example of a high salary –

It’s not always the case that you own a business to earn high income. To run a company or business many skills are required and if you have that in you, you can help someone else to build and manage the company in exchange for your skills.

As per this report, around 42,800 have reported an income of Rs 1 crore per annum in India. You now have to set yourself to be in that club

#5 – Speculation or Gambling

This is not a recommendation, but a lot of people become rich by speculation or gambling. This has more to do with Luck and smart thinking at times, but not with hard work.

I do not want to label speculation as BAD, because speculation takes guts and courage and those who take that route also get lucky at times and make a lot of money. There are two kinds of speculation

Blind Speculation – A speculation where you are just shooting in the dark. Things like buying lottery, horse race etc is pure speculation and unless you get lucky, you will lose your time and money. A lot of people are into these speculative and gambling activities

Calculation Speculation – Then there are many situations where you have to take a very calculated risk, where the risk is still high, but then the return potential is huge and clear at times. These are high risk, high return situations where if you take a chance, you can get really lucky.

One can get lucky, only when you take a risk and speculate. Speculation is seen as a bad word, but one can’t deny that it also has a brighter side to it. If you want to innovate something, you need to speculate on the fact that it will become successful.

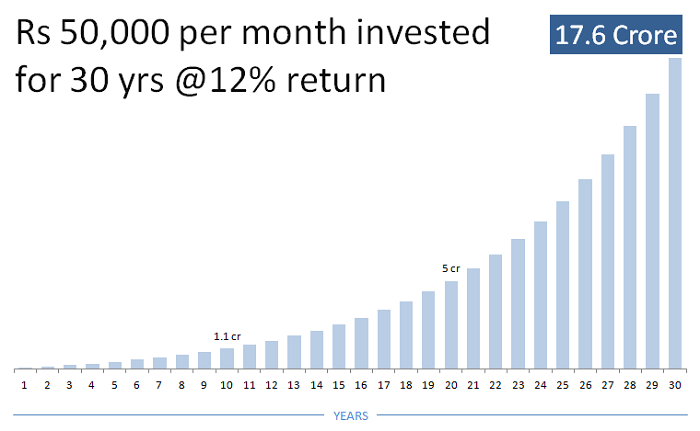

#6 – By Investing money regularly – the boring & long route

In the end, if you feel you are not made for the above 5 points, then the only way to get rich is to invest your surplus money on regular basis and that too in high return instruments like equity mutual funds or stocks and wait for a long time to become rich.

The big problem is that there is too much-delayed gratification here. If you start your investments today, you can’t expect to get rich in just a few years which is possible in other ways mentioned above.

You need to have time on your side and extreme discipline. On top of that, you need to invest a good amount of money. You can’t expect to become rich by doing just Rs 4,000 SIP in an equity fund. You need to invest a good amount like Rs 20,000 or Rs 50,000 per month (at times Rs 1 lacs per month too) to accumulate a good amount of wealth.

So, the only option left for most of people to become rich (that too in future) is only by investing their money and that will happen only if you earn a good income because only then you will be able to invest a good chunk left out of it.

Let us know what do you think about the points mentioned above?

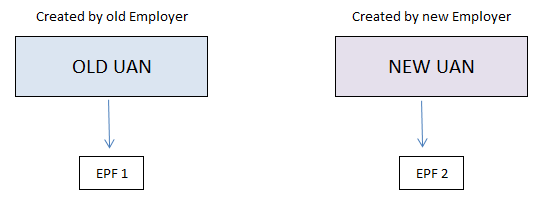

Today we will talk about the issue of duplicate UAN, which has confused a lot of employees. A lot of people have contacted us that 2 UAN were generated for them by their past employer and current employer and now they have no idea what is to be done in this case.

You can see following question which was posted by one of the reader of this blog.

Hello Manish,

I left my previous company on 1st April 2014 and joined new company on 7th April 2014. Now problem is I have been allotted UAN no. from both employer. I want to withdraw whole amount of EPF (Employees’ Provident Fund) of previous employer.

So kindly guide me what to do in this situation?

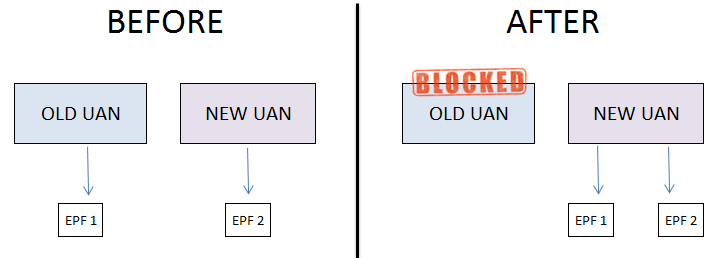

Why does multiple UAN get allotted?

UAN (Universal Account Number) as you all know, is a single unique number for each EPF member for all this EPF accounts under them. You can see the UAN as the folder (UAN) which has various files under it (EPF accounts)

Before we discuss how to solve the duplicate UAN problem, I want you to know how two UAN are generated and why does it happen?

Reason #1 – Not disclosing old UAN number

A lot of employees do not want to disclose about their past employment, hence they do not quote their old UAN number to new employer. In that case, the new employer will generate a fresh UAN for the employee. This is one of the reasons for having duplicate UAN number.

Reason #2 – Past employer did not furnish ‘the date of exit’ details in the ECR

ECR or Electronic Challan cum Return is an electronic return filed by employers to EPFO to submit your EPF payments and other things. In this, they mention “the date of exit” for those employees who have left the job. So incase due to some issue the employer does not mention this date of exit.

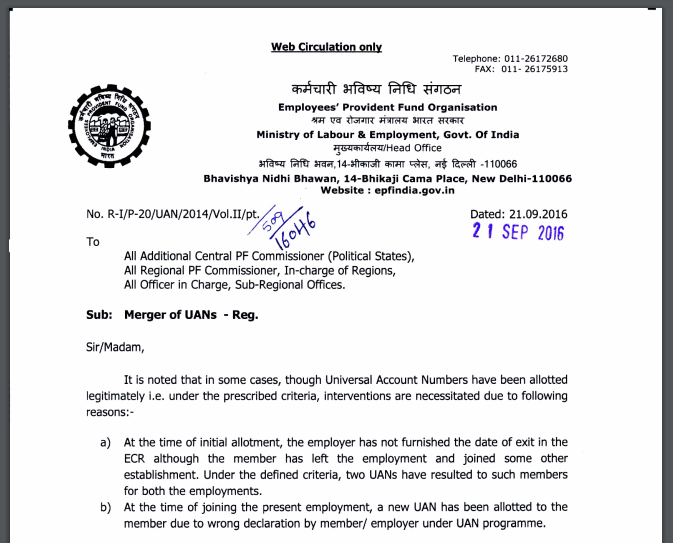

This is another reason why another UAN gets generated by new employer. I have no idea why that happens, but this is the reason which is mentioned by the EPFO in their recent circular which talks about the issue of multiple UAN allotment

How to solve the two UAN problem?

Note that each person should have only one UAN number (like PAN), hence if you have multiple UAN, it’s not allowed and creates problem in the EPF system, because is no proper track. Hence, as soon as you come to know that there are multiple UAN assigned to you, you should cancel one of the UAN (mostly the old UAN) or should try to deactivate one of them

Process to deactivate old UAN

Step #1 – The first step if that you should start the EPF transfer for all the EPF’s which are not under the latest UAN generated. This can be done using the OTCP portal of EPFO . I am not going in details here, but first you need to make sure all the old EPF’s are transferred and linked to the new UAN.

Step #2 – In the next step, the EPFO system will automatically identify those UAN for which the EPF transfers have happened and completed. Once they find the idle UAN, they will automatically deactivate that UAN. You don’t have to do anything here. This deactivation process will take place from time to time as per decision taken by EPFO. Once the deactivation happens, your old member id (your old EPF accounts) will be linked to new UAN.

If you are already sure that your past UAN does not have the EPF linked to them, then you can mail your old UAN number along with recent UAN to your employer and to [email protected] . They will verify your UAN’s status and deactivate the old UAN.

Let us know if you have more clarity on this subject or if you have already completed the process for the benefit of other readers.

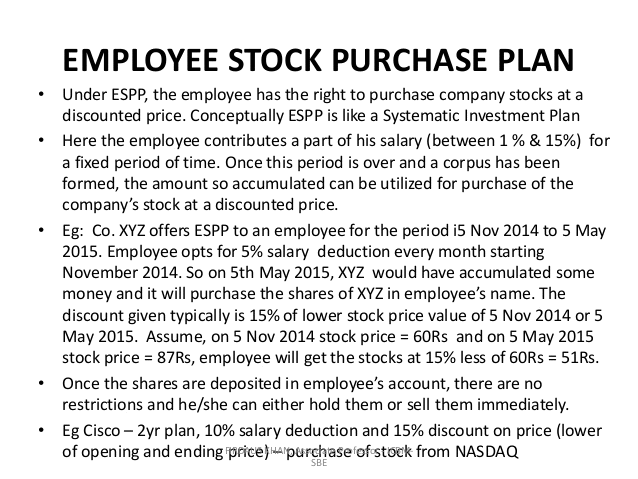

Today we will talk about various aspects of ESPP Plan? We will also see if it really makes sense to invest in your employers ESPP plan or not, and what are the pros and cons of that.

For those who have no idea about ESPP, its full form is Employee Stock Purchase Plans and It’s mainly an offer from your employer to buy the stocks of the company at some discounted price.

How does ESPP Plan look like?

Let me give you a rough idea of how an ESPP plan looks like. Under this plan, your employer might offer the discount of 15% of the stock price, and you can contribute some part of your salary for purchase of ESPP.

This might run for 3 or 6 months and then at the end of the period, all the money which you have paid, will be used to purchase the stocks at a discounted price (It might be the current market value or the lowest of the period, it all depends on your companies offer plan)

So you get the stock at a discounted value

You invest the money for X number of months

The stocks are purchased at the end of 3/6 months period

You get the stocks on your name

Is ESPP Plan worth?

Now let’s come to the main point. Is investing in ESPP plan worth? Should you do it? Is there any catch?

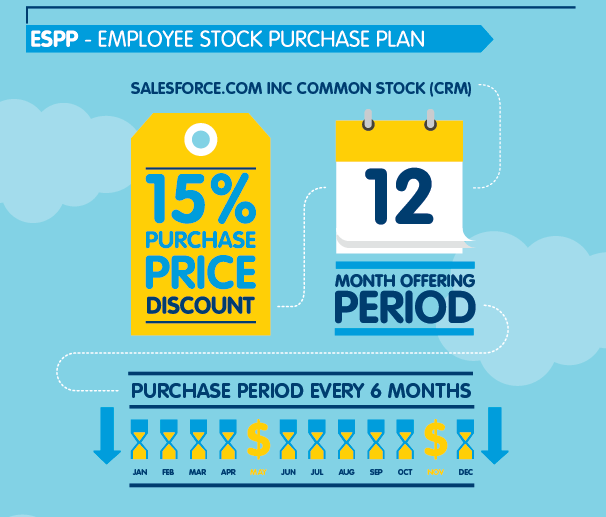

Below is an example of Salesforce ESPP plan, where they are offering 15% discount and the offering tenure is 12 months (employee will pay for 12 months), while the purchase will happen every 6 months.

Now the main question is – “IS IT WORTH?”

and the Answer is ALMOST ALL THE TIMES.

Yes, most of the times, it makes sense to invest in ESPP plan because you get the stocks at a good discount and if you sell it off after they are allotted to you, you will make a good enough profit (15-20%) in most of the cases, unless things go really bad.

In some cases, you might want to think hard before you invest in ESPP plan offered by your employer.

Point #1 – At the end of the day, you are buying a Stock

ESPP is nothing but a plan where you buy a STOCK. Hence the price of the stock will move up or down. So if the stock does not do well, you will not be able to make good profit and your hard earned money will not give you the desired returns.

Imagine a stock which is on decline or not doing well. Your ESPP plan will give you the stock at 15% discount of the lowest price (mostly the latest price) . Not every time, people sell it off immediately, and keep holding it. Now if the stock price does not come above your purchase price and you kept on holding it, you might suffer good amount of loss.

Look at Yahoo, as an example (I worked there for more than 3 yrs). Imagine people who bought ESPP of Yahoo and kept on holding it? Even if they got it for discount, does not mean that they will make profits.

So don’t get emotional and look at your company stock and see if as an outsider. Check out what are the future prospects, Is it promising? Does your company find its place in most of the mutual funds portfolio?

Point #2 – Your Income and Profits come from same company

You earn your income from your company, and now your portfolio is also linked to same company. If the company is doing very well, your income will rise and so will your portfolio value. But what happens if things go bad?

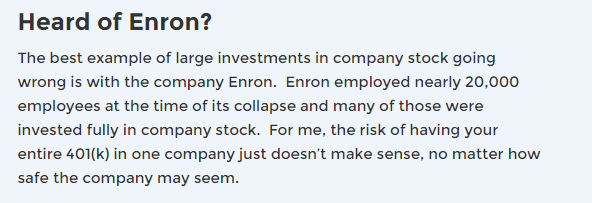

What happened to Satyam?

What happened to Enron?

What happened to Yahoo?

If someone worked in companies above, they lost their jobs. And at the same time, their stock prices were either worthless or reached the lowest value and they suffered huge losses. The snapshot below was taken from this website, which talks about Enron collapse.

The point is, when you invest in an ESPP plan, all your eggs are in same basket. If things work out and your company does well (Google, Facebook), you will enjoy the benefits of promotions, income rise and your stocks value rise, but in the other case, it will be the opposite and it’s not going to be the best situation.

Conclusion

At the end, you need to ask yourself about the prospects of your current company where you work? Do you think it’s going to be great in coming times? If Yes, then not just ESPP, you can even go for ESOP’s and other plans from your employer.

Last night, it was a historic moment when our Prime Minister informed the whole nation that Rs 500 and Rs 1000 notes will not be eligible currency notes from midnight at the end of 8th Nov, 2016. Here is the RBI notification

PM Modi had also explained all the points very well in his speech and shared how people should not worry about this if they have money with them and it can be exchanged with new notes in next 50 days, however seems like a lot of confusion is there around this topic and many myths are floating around.

5 important facts about the old notes bank

Below are some of the most important facts which you should know after this Rs 500 and Rs 1000 notes bank. There are lots of myths around and I wanted to clear them. These points which I have mentioned below are taken out of the RBI notification itself.

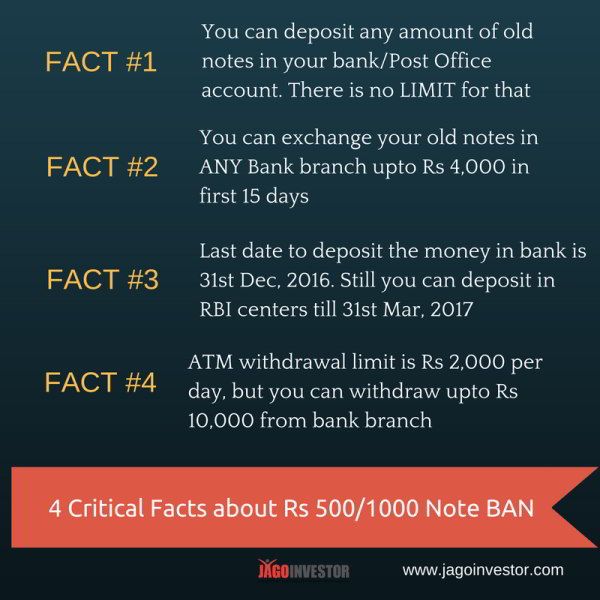

Fact #1 – You can deposit any amount of old notes in your bank/Post Office account

You can “deposit” your old currency in your bank account till 30st Dec, 2016. There is no limit on this amount and if you have Rs 50 lacs with you in Cash, you can just walk into your bank branch (expect a lot of rush) and just deposit the amount in your bank account. The limit which is there is on the “exchange” which is the next point. Please find below the exact wording from the RBI notification.

Also note that there is no limit of deposit for account whose KYC is complete. If KYC is not yet complete, the limit is Rs 50,000.

#2 – You can exchange up to Rs 4,000 notes in ANY bank branch in first 15 days

You can walk to ANY bank branch and exchange up to Rs 4,000 of old notes along with your identity proof (PAN, Aadhaar card, Passport etc). You don’t need a bank account in the same bank. After 15 days, this limit of Rs 4,000 will be reviewed and raised. I am sure this small limit is kept so that most of the middle class and poor people are handled before other privileged class 🙂 . Apart from the bank branches, you can also visit RBI centers for this exchange.

#3 – You can deposit the money in 3rd party account also

It is also possible to deposit the money to 3rd party account also if you follow the full procedure and produce a valid ID proof (your own)

#4 – Cash withdrawal Limit from ATM and Bank Branch

There is following withdrawal limit set by the govt.

ATM – Withdrawal from ATMs would be restricted to Rs.2,000 per day per card up

to November 18, 2016. The limit will be raised to Rs.4,000 per day per card

from November 19, 2016 onwards.

Bank Branch – Till 24th Nov, 2016, you can walk to your bank branch and withdraw up to Rs 10,000 in a go, but the overall limit is Rs 20,000 per week.

You can walk to ANY bank branch and exchange up to Rs 4,000 of old notes along with your identity proof (PAN, Aadhaar card, Passport etc). You don’t need a bank account in the same bank. After 15 days, this limit of Rs 4,000 will be reviewed and raised. I am sure this small limit is kept so that most of the middle class and poor people are handled before other privileged class 🙂 . Apart from the bank branches, you can also visit RBI centers for this exchange.

#5 – You can deposit the old notes till 31st Mar, 2017 in worst case

In worst case, if you are not able to deposit the cash in your bank account or exchange those till 30st Dec, 2016, Still you will get another change to deposit the amount at RBI designated branched till 31st Mar, 2017 with proper documentation. One of my close friend parents are coming back to India from US after Jan, and they were worried after this news. I told them about this 31st Mar, 2017 deadline which calmed them!

Below is the speech by our Prime minister in case you want to hear it.

The big confusion and the Panic

This whole news which came out last night has created a big confusion among people and I can see many of them in panic situation. A lot of people who know clearly that their money is still safe and can be deposited back in bank account are also acting like the world has come to the end.

On the lighter note, social media went crazy and there were some really hilarious tweets which started circulating across various platforms.

There was news of people rushing to buying gold, doing shopping last night (till midnight) and what not. Understand that if your money is legally earned and you are paying the taxes, you need not panic and just keep calm, you can deposit it with bank and your money is 100% safe.

Only those who have black money will be facing problem as now all the money they have is worthless.

Discomfort because of the BAN

While there is surely some level of discomfort, but that’s very obvious and it’s bound to happen when things change at this level. This bank of old bank notes is for good and our countries future. This will really help curb black money and corruption in a big way.

Will update more on this topic in coming days. New notes of Rs 500, and Rs 2,000 will get started from Nov 11th .

Let us know your views around this topic in comments section below

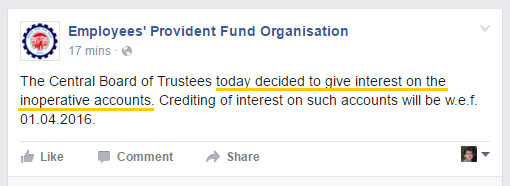

Good news, the inactive EPF accounts will now start getting interest. Also the interest will be paid since Mar month of this year. This will start once the govt issues the notification regarding this. Since 2011, the EPF accounts which were not active for 3 yrs before inoperative EPF accounts and they stopped getting the interest.

Now Inoperative EPF accounts will earn interest

However now the rules are changed and if someone wants to keep the money in EPF account, they can do so. The EPF account will keep earning the interest decided by EPFO from time to time. This year itself the news was out that the inoperative accounts will get interest. However the notification news has come just now yesterday.

As per the EPF officials, Around 42,000 crore has been lying in inoperative EPF accounts and they will get interest @8.8% now.

“The inoperative EPF accounts are not being paid interest since 2011. As per the instructions given by Prime Minister Narendra Modi and Finance Minister Arun Jaitley, we decided to start paying interest on those accounts to make them operative,” Mr. Dattatreya said on Monday.

You can now leave your EPF accounts active even after leaving the job

As per this latest development, now after you leave your job, and do not join somewhere else, you can leave the EPF account to keep earning the interest. Given that the EPF interest is upwards of 8%, it’s a good place to park the money.

I had written my first book “16 Personal Finance Principles Every Investor Should Know“ a few years back and it got very popular among investors. It has close to 130 reviews on Flipkart + Amazon. Now the same book is translated in Hindi Language and is available for sale.

In Hindi it’s called – Ache Niveshak Ke 16 Sutra

The Hindi version is targeted towards those who can read Hindi books and not only for those who cannot read English, because it used enough English words (in Hindi script) at various points.

There are enough number of people in our country who need financial literacy, but they are not able to read English and hence don’t read on internet as most of the content is in English

So if you know anyone who can benefit with my first book in Hindi format. Feel free to share about the book with them