Are you looking to buy a home which is already funded by a home loan and someone else is paying the EMI?

Does it make sense to rely only on the bank for verification process or should you take the second legal opinion? Most customers have this query when they are buying a property and availing a home loan.

They are well aware that the FIs (financial institutions) have a panel of lawyers that do this day in and day out but still want to satisfy themselves by getting an opinion from that one ‘recommended’ lawyer that their uncle knows.While it is a harsh truth that no property can be legally proofed to a 100%, there are a couple of things which need to be considered while deciding to take a second legal opinion.

Let us consider two kinds of properties – one where there is a large apartment complex and second where it is an individual plot or a small apartment complex.

Case #1 : Large Apartment complex

When a corporate real estate developer intends to purchase a large parcel of land and develop it, they know they are going to invest a huge amount of time and money.

They already have the experience to pick up the right projects. They also have a tried and tested lawyer or legal department to check details and guide them through all the steps till they reach the point of selling apartment units.

It’s at this ‘late stage’ that the bank receives the set of papers and the em-paneled lawyer comes in and usually it is a matter of checking off the title, EC’s (encumbrance certificate) and other revenue records.

Such developers also have the financial might to settle any disputes that can be a legal hassle.In the unlikely event that there is a problem in the title / parent documents, then the owners can join together to fight against the developer or any other party.

Division of costs and burden

The financial costs can also be distributed, reducing the burden. However, this is likely to be an unwieldy and argumentative coalition so this is not a major advantage. To sum it up, these kinds of properties developed by a reputed builder are ‘less risky’.

In any case, it is a good idea for all buyers to keep a copy of documents pertaining to legal such as the legal opinion, copies of all documents including sanction plan and other statutory documents as far as the land on which the project has come up is concerned.

Case #2 : Individual House on a plot

Coming to the other classification of property – individual house / plot or small apartment complexes, it is worth taking a second opinion. The first and basic reason is that it is good to have a legal opinion in place.

The FI treats its legal opinion as confidential and does not share it with the customer. So, if the customer wishes to understand the intricacies of the property and also have a document to refer to at a later date, this is necessary. Even if the property is to be sold, the potential buyer would have more confidence considering that the legal clearance had been taken earlier.

However, one has to consider the cost of the opinion. It could be prohibitive considering there are payments to be made including the FIs processing fees, insurance premium and stamp duty of 0.25% to the government for availing the loan.

Hire a lawyer to do title search

The next best option is to commission a lawyer to conduct a title search on the property and give a clear report. This is different from what the FI em-paneled lawyer does (which is a title clearance report, checking the EC (encumbrance certificate) and an additional check of the approved building plans).

A title search report essentially consists of going to the sub registrar’s office and verifying the revenue records, ensuring there aren’t any open encumbrances or claims by any party. Usually, this is done for a period of 30 years. This will be an additional and strong check for a clear title to the property.

You will find a lot of articles out there detailing the list of documents one needs to check before purchasing a property. Many of the common issues are also listed. These are definitely worth perusing and acting upon. It is important to remember that purchasing a property is not the only important aspect, having peaceful possession of it is equally important.

This is a guestarticle by Pravin Mathew from Bangalore, who is a reader of this website. Incase you have any questions, we will be happy to answer it in comments section.

Government has decided to make it compulsory for every individual to link their Aadhaar Card with PAN card by 31st July, 2017. This is part of the digital India campaign and an attempt to digitalize everything.

Why it is mandatory to link Aadhaar with PAN?

There is a great chance that there are a lot of fake PAN cards in India, because it can be easily applied online with fake identities and anyone with a little luck can get a duplicate PAN card. Hence in order to identify those fake PAN cards, govt wants to link Aadhaar card with PAN.

Because each person will have only one Aadhaar card, they will only be able to link it with a single PAN. Rest other PAN cards will be of no use after this process. This is an important move and is necessary for an orderly society and also to keep pace with the technology.

Importance of linking Aadhaar with PAN

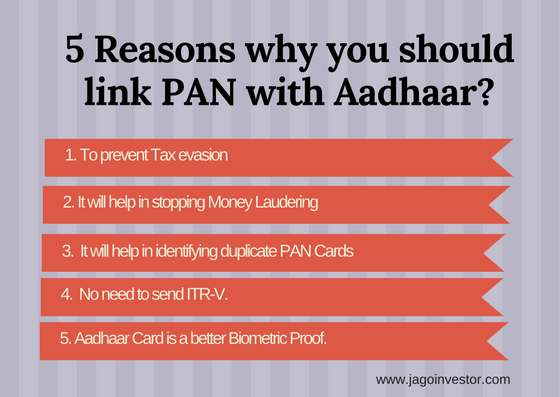

PAN card and aadhaar card are the unique identification cards which can be used for verifying a person’s income and address respectively. Let’s have a quick view why this linking is important.

Some reasons behind linking aadhaar with PAN in details are as below:

Fraud PAN cards– Because of this linking a person can use only one PAN card wherever it is necessary which is linked with his aadhaar card. Though he has any fraud/duplicate PAN card, it will be of no use.

Tax Evasion – with the help of this, government will be able to track on the taxable transactions of an individual or an entity.

Tracing money launders- Aadhaar card is a full-proof identification of an individual and it cannot be duplicated easily so that linking of aadhaar with PAN can also be useful for tracing money launders.

There are fewer chances to have a duplicate aadhaar card as it is a more secured source of identification. Because Aadhaar card is the only identity proof which has all the possible information including Bio-metric. So it is little bit difficult to have a fake aadhaar card as compared to PAN Card and voter ID.

Curb corruption: This is also useful to curb corruption to a significant level as the record of each transaction will be verified by the government.

Also, the government wants to get every individual identified by their Name, Address and also their income. A lot of PAN cards were very old, and many people have changed their address, contact details etc which were given to govt at the time of applying for the PAN card decades earlier. With this linking, all the data will also get updated.

What is the process to link aadhaar card with PAN?

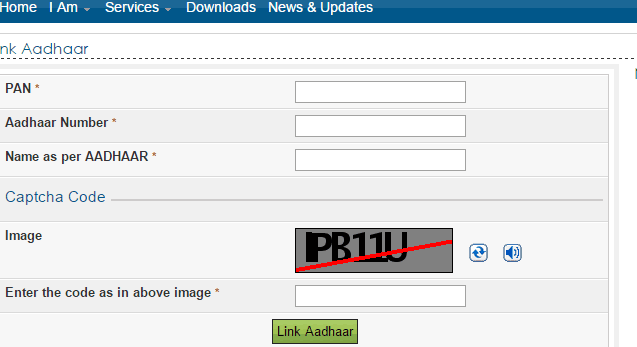

If you are unable to link your aadhaar card with PAN, no need to worry. Here are the steps to link your aadhaar card with PAN.

Visit the page of Income tax e-filling portal & register if you are not registered with it. If you have your registration already then just login.

Login with the details i.e. registration ID, Password or date of birth.

Your PAN no. will be your registration ID

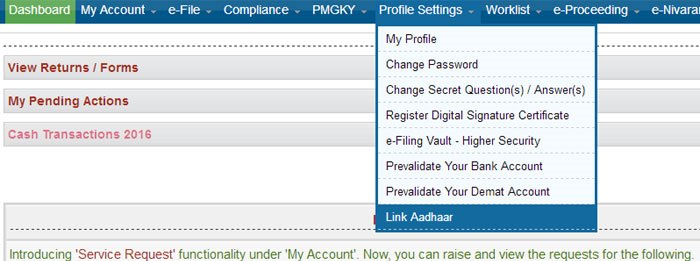

once you login you will immediately get a pop-up to link your aadhaar with PAN

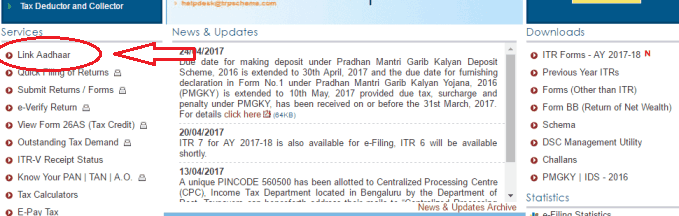

If you don’t get a pop message then check the blue bar above and click on “Profile setting” and then on “Link aadhaar” in the list.

Or you can also see the option “Link Aadhaar” on the left side of the site when you open it without logging in. Simply click on it.

The details like your name, gender and date of birth will be given there already as per the registration. Just check that the details available there are same as on your aadhaar Card.

If the details match with aadhaar card then fill your aadhaar card number and captcha code and click on “Link Aadhaar”.

Once you submit you will get a pop-up that your aadhaar has been linked with your PAN successfully.

What happens in case of name mismatch between Aadhaar and PAN?

UPDATE:Now you can link your aadhaar card with PAN without changing your name as the option “Name on Aadhaar” has given there.

Now it’s suggested that you first decide what is the exact name you want to keep for future, in case you have different names on various documents.

If your aadhaar card has the name which you want to keep, then you should change your name in PAN. However if your PAN has the desired name, then change it in Aadhaar card.

Now, for those who want to change their name in aadhaar card, they can follow this process or watch the video below.

We really feel that one should have the proper name in Aadhaar card, because it’s going to be the universal documents in future.

UPDATE: New Feature by IT department

Besides this, there is also a new option on the e-filling site from where you can link you Aadhaar card with you PAN card without changing your name.

Only date of birth, Name and Gender on both the documents should match, however we feel that as a long term solutions it’s a good idea to have the same name on both the documents.

What to do if I don’t have one of the documents (Either PAN or Aadhaar)

Now a days, almost all the people at least in urban areas have both aadhaar and PAN, very rarely it happens that someone does not have both the documents. However incase one of the documents is missing, here is what you should do ..

For those who do not have PAN

If you don’t have PAN card, then this rule is not applicable to you right now. You don’t need to take any action at the moment.

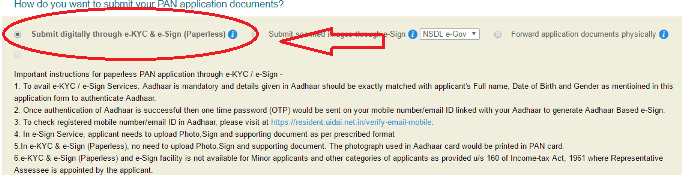

When you apply for PAN in future, at that time you can give your Aadhaar details as the address proof while applying for PAN offline or you can choose an option called digital e-kyc and e-sign, where you will be asked for aadhaar number and it will be automatically linked to your PAN. Below is a snapshot of the e-KYC looks like.

What do you if you don’t have Aadhaar?

If you don’t have Aadhaar card then you should apply for it soon, because anyways it’s going to be the universal mandatory documents very soon and every PAN has to be anyways linked with aadhaar. You can apply for aadhaar card by online or by visiting its office and providing you essential documents.

How to Check whether your PAN card is linked with Aadhaar card or not?

For some people their PAN might be already linked with Aadhaar card. To check this you just have to visit the official page of e-filling and click on the login button on the right corner of the site. Fill your PAN number and captcha code and click on OK.

If your card is already linked then it will show “Your Aadhaar is already linked with PAN” and if your card is not linked then it will show “User ID does not exist”.

Below is the demo of this process

Is it safe to link your PAN details with Aadhaar?

Recently there was a news that M. S. Dhoni’s Aadhaar details were leaked somehow, which shows that aadhaar details are not 100% secured. If this can happen to a big celebrity, this can happen to anyone.

Many people are wondering if it’s safe to link their Aadhaar with their PAN?

Will their bank details be exposed ?

Will there be any fraud involved?

Will others get access to their income tax data ?

Will others get access to my personal data like Mobile number, Email and Bio-metric details?

But, you don’t need to worry!

The solution to problem is here. There is no need to worry about the security of your PAN after linking with Aadhaar. UIDAI has introduced safety features of aadhaar Card.

Now there is a facility of “Lock” and “Unlock” of aadhaar details.

If you “Lock” your aadhaar details, all your data will be freezed and the access to any third party will be blocked. All you will need to do is, verify the OTP which is sent to you when you apply for this “Lock” feature online. If you want to get details about all the safety features, you can download this PDF.

What will happen if your Aadhaar card is not linked with PAN card?

As per this amendment if a person do not link his aadhaar with PAN card then there is possibility that he could lose his access to the PAN card after December 31,2017 as per Hindustan Times.

You will be unable to file IT returns and pay the dues or claim the IT returns.

It’s been also said that the use of PAN cards may stop in upcoming days as Aadhaar card will be the unique Identity proof. So if you don’t link it now you have to link it with your PAN in future in any ways.

Because your PAN card will be blocked, and for higher value transactions PAN is mandatory, you will not be able to do many high value transactions online as the bank will keep asking for PAN

UPDATE:What if I have both the documents but don’t have any Income Tax Returns?

If you don’t file any Income Tax Return then this rule is not for you. It will not affect either you link your Aadhaar card with PAN or not.

But if you have both the documents, we suggest to link the documents.

UPDATE: What if I’m an NRI and have only PAN card?

NRI’s can also apply for the Aadhaar card. The procedure and documents required for NRI and Foreigners are same as Indian residential’s. Only thing is they have to be physically present at any of the Aadhaar card center in India.

But it is not mandatory for NRI’s till date because as per Indian Government Aadhaar is an unique identity for the person who is living on Indian soil. Read this PDF by UIDAI.

How can I apply for Aadhaar if I’m out of India?

If you are not in India currently and wanted to apply for Aadhar crad then the procedure is almost same. But you should have an introducer who can introduce you by providing his/her own Aadhaar card.

The verification of your identity will then become the responsibility of the introducer.

So, what are you waiting for ?

You should quickly complete this whole process as it’s just a 5-10 min work. Not completing this can impact you in negative way, so do not wait for the last minute.

Also you should spread this news among your friends and help others to complete this important step in their financial life.

In case you have any questions, I will be happy to answer them in comments section

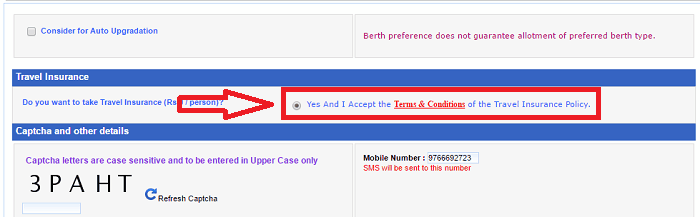

In next 7 min, you will read how you can secure your family with just Rs 1. I am going to teach you that. IRCTC has made it compulsory for every train traveler to take a Personal Accident Insurance Policy which has been applied from September 2016.

Railway minister Mr. Suresh Prabhakar Prabhu had announced in his speech that from the month of September 2016, railways will provide an optional travel insurance of Rs.10 Lakh to the passengers while booking tickets from its website, which can be opted by paying an extra 92 paisa.

UPDATE:Now while booking for train ticket you will see the prize “Rs.0 per person” in the option of insurance. So there is a possibility that the insurance amount have been added with the ticket fare.

Travel insurance policy by IRCTC is now mandatory

Earlier this accidental insurance policy was optional but now IRCTC i.e. Indian Railway and Catering Tourism Corporation Ltd. has decided to make it mandatory for the safety purpose of the passengers. Now if you book your tickets, you will not get an option to choose if you want the insurance or not. It has recently become mandatory as it was hinted some time back as per this article.

You can see the snapshot below

This policy is just like a travel insurance policy where a train traveler or passenger who books a train ticket from IRCTC’s website will get the insurance up to Rs.10 Lakh by paying an amount of less than Rs.1 extra while confirming the ticket. This amount will be provided to the family/nominee/heir of the person if he/she gets injured or dies in train accident.

3 companies which provide IRCTC policy

IRCTC has a tie up with 3 insurance companies which are providing this policy. These insurers are Shriram General, Royal Sundaram and ICICI Lombard. We recently tested it to see which company is providing the insurance and we got a message with Royal Sundaram. It might be different in your case.

Initially this scheme was introduced on a trial basis, but now it’s compulsory. The passengers having confirmed tickets, RAC (Reserved Against Cancellation) or are on waiting list can have benefit if this insurance.

This facility is not available for the sub-urban trains. Only Indians can get this policy. Children and Foreigners are not eligible for this policy. The insurance will be valid in cases like train accident, riots, terrorist attacks, shoot-out or arson in train, on platform or on the route to its destination.

What is covered under IRCTC Travel Insurance policy

Unlike common belief, the travel insurance with IRCTC goes beyond cover on death and provides various other benefits like disability insurance in various conditions.

Below are the details

10 lacs for death

10 lacs for permanent disability

7.5 lacs for partial disability

Upto 2 lacs for hospital expenses

Upto 1 lacs for transportation of mortal events

Who can claim compensation of accidental insurance policy by IRCTC?

If the deceased is married then his wife, son or daughter can claim for the compensation. The daughter or son should not be minor if they are claiming. If the deceased is not married then his or her parents can apply for compensation. In other case, if the deceased has nominated someone else like other relative or any friend then he/she can also claim for the compensation.

In short we can say that the person whose name and details have been filled in the application by the deceased while booking the ticket can claim the compensation. The only thing is that he/she should have ID proof.

As per rules, within 4 months the insurance claim has to be filed from the date of insured event. All the terms & conditions, benefits and exceptions of this policy are mentioned in this pdf, download it and read it in detail.

Please watch the video below to learn about this topic ..

How to apply for the compensation of IRCTC accident insurance policy?

The nominee or the claimant can apply for the compensation to the nearby office of the insurer company which the deceased had selected at the time of booking ticket. You has to visit the insurance office and fill the compensation form and attach all the documents essential for the claim.

Why this Policy is Important?

In last 6 years around 800 train accident cases were registered in India in which near about 600-620 people died and 1850 were injured. More than 15000 people are killed in railway accidents per year as per some reports

Just imagine, you could have been one of those. What financial impact it can have on your family?

But many people just ignore the travel insurance thinking that it can never happen to them, as if they are GOD. Anyways the irctc insurance charge is just Rs. 92 paisa, which is nothing compared to the benefits it provides.

Disability in case of train accidents

For an ordinary person, if such accidental case happens then it will be too much difficult to arrange money for hospitalization. And the cost of this policy i.e. 92 paisa is negligible as compared to the total train fair and the compensation.

The big reason to worry is many times these accidental victims die just because they couldn’t get proper medical treatment or even immediate help also.

Are you one of those investors who are still away from mutual funds investments because you do not have enough understanding about it or have a lot so myths about them?

Every day we get constant inquiries from several of our readers who want to invest in mutual funds and often they have myths, which make us wonder about those myths.

So in this post, I have listed down 33 various myths related to mutual funds and SIP in general. So if you are totally new to mutual funds, reading this article start to end will make you fully knowledgeable about mutual funds.

So let’s start…

Myth #1 – SIP is the name of an investment product

A lot of people think that “SIP” is the name of some investment products other than mutual funds. So they say – “I want to invest in SIP”. However, SIP means a systematic investment plan, which just means a way to regularly invest only in mutual funds. In this, a pre-fixed amount is automatically deducted from your account and gets invest in mutual funds on a pre-defined date.

For example, if you are doing an SIP of Rs 5,000 in ICICI Pru Discovery mutual fund on the 10th of every month, then on the 10th of each month, Rs 5,000 will get deducted from your bank account and will get invested automatically.

Myth #2 – I can’t stop SIP in between once I start it

Another myth that stops investors from entering mutual funds is that they think starting SIP for X yrs, is a commitment they can’t break in between and they will face some penalty if they stop their investments.

A lot of people do not want to give any PROMISE of regular payment. However, the truth is that once you start the SIP, you can anytime stop the SIP in between. So don’t worry while starting the SIP for the next 5, 10 or 30 yrs. The day you want to stop it, it can be stopped with just one notification!

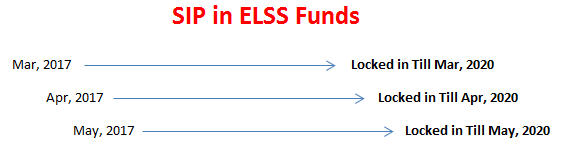

Myth #3 – All the money from ELSS can be withdrawn after 3 yrs if one is doing SIP

One of the biggest myths of investors is that if they are doing SIP in ELSS (tax saving mutual funds), then after 3 yrs, they can withdraw all their money. However, that is not true. Each investment in ELSS is locked for 36 months from the date of investments. This means that the first SIP which goes in March 2017, will be free of lock-in only in April 2020.

The same is the case with the installment which goes in Apr 2017 (will be free in May 2020)

Myth #4 – Lower NAV is cheaper than higher NAV

Most of the mutual fund’s investors think that a smaller NAV mutual fund is a better deal compared to a higher NAV mutual fund. While this may be sometimes true in case of stocks because a Rs 10 stock has the potential to grow faster than a stock with Rs 10000 stock value.

But in case of mutual funds, NAV has no significance. It’s ZERO!

Because your mutual fund’s appreciation has everything to do with the appreciation in NAV value in percentage terms and not an absolute value. I mean if you invest Rs 10 lacs in a fund with NAV of Rs 10, and if the mutual fund performs great and in the next 5 yrs it doubles in value, then the NAV will rise to Rs 20 and your fund value will rise to Rs 20 lacs.

However, if the NAV was Rs 10,000 per unit, still the effect would be the same for you. The NAV would have increased to Rs 20,000 and your value would have increased to Rs 20 lacs. No difference as such.

So stop thinking that a fund is better (especially NFO’s) just because its NAV is lower.

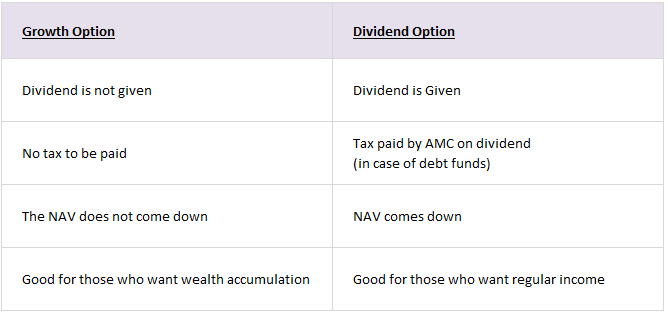

Myth #5 – Dividend in mutual funds is better than Growth option

Dividends are not extra!, The NAV comes down by that margin after the dividend is paid, on top of it, if the fund is not an equity fund, a dividend distribution tax is first paid by AMC, which lowers the return of the investor. However, in the case of growth option, the money remains in the fund itself.

For example, imagine a fund XYZ with NAV of Rs 100 and a dividend declaration of Rs 10

Now in case of dividend option, Rs 10 will be paid to investors and NAV will come down to Rs 90.

However in the case of the Growth option, nothing is paid to the investor, but the NAV is Rs 100.

Myth #6 – Mutual funds means Stock Market

One of the most common myths is that mutual funds are highly risky because they invest in stocks. However, this is half true. Only equity mutual funds invest in stocks and are risky (in fact volatile is the right word, not risky)

There are other categories of mutual funds called debt mutual funds, which do not invest in equities. They invest in bonds, govt securities, and other secured investments. While debt funds have their own risks and even their returns are not 100% stable, still, debt funds are highly stable when it comes to returns and often provide better tax-adjusted returns then most of the bank fixed deposits.

Myth #7 – You have to invest big amounts in mutual funds

Many small investors stay away from mutual funds and stick to recurring deposits and other products because they think that mutual funds are for big investors and one has to invest big money in it. However, you can start a monthly investment of even Rs 1,000 per month in most of the funds. If you want to invest on the onetime basis, the limit is Rs 5,000.

So someone who is just earning Rs 10,000 per month and wanted to invest 10% of his income, can also start mutual funds SIP.

Myth #8 – Mutual funds are always for long term

Mutual funds are marketing as long term investments most of the time. However, it’s not always the case. There are mutual funds called liquid mutual funds and even short term debt funds which can be used for short term investment horizon like 6 months or 2 yrs.

This article from Economic times talks about some of these funds

Only in case of equity mutual funds, it’s suggested that one should invest from a long term perspective to reap the maximum benefits.

Myth #9 – Mutual funds offer guaranteed returns

No, Not always.

Actually never!

Mutual funds never offer a guaranteed return like a fixed deposit. This is one reason why many investors who are totally in love with “assurity” shy away from investing in mutual funds.

Various categories of mutual funds offer various return range. An equity mutual funds can offer return anywhere from -50% to 100% return in a year (just a high level estimate). Whereas a debt fund can also deliver a return ranging from 5% to 15%. And a liquid fund will mostly give a return in range of 6-8%

So the returns are not guaranteed, but highly probably within a range depending on its category.

Also note that as the investment horizon shifts from 1 yr to 10-20 yrs, the probability of getting a stable return within a range increases.

Myth #10 – I will lose my money if the mutual fund’s company goes bankrupt

This is common thinking, but not true

Mutual funds are highly secured in terms of structure. The way it’s designed and regulated by SEBI, it’s almost impossible for investors to lose money due to a scam or AMC going bankrupt. Your mutual fund’s units does not lie with AMC (it just takes the decision of buying and selling). Units and all the money lies with the custodian and highly secure.

Myth #11 – Past returns in mutual funds indicate future returns

Not correct.

While past returns can surely tell you that the fund did very well in the past and there is some probability due to legacy that it will perform well. But it’s not written on stone.

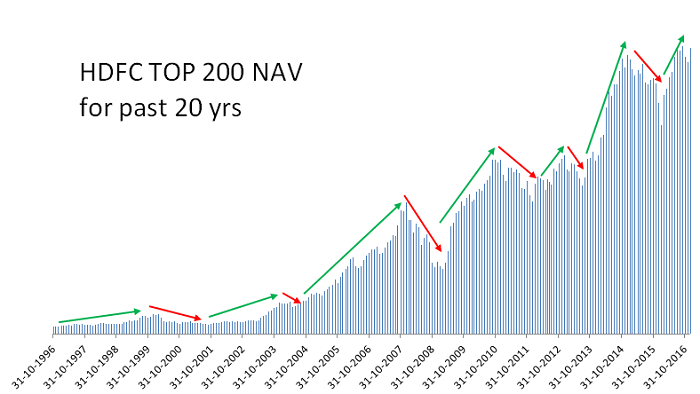

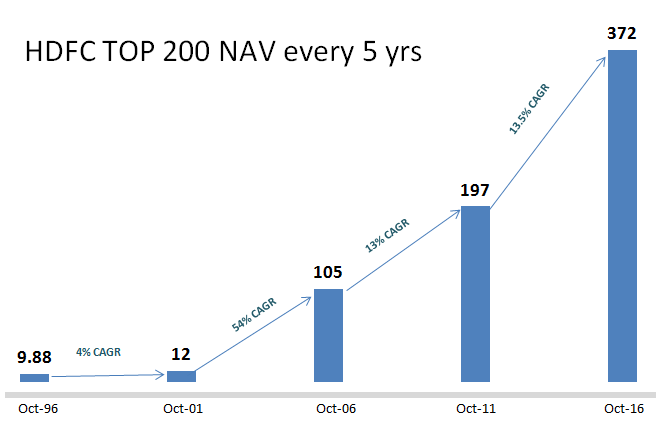

How the fund will perform in future is totally a function of what decisions fund manager takes in future. HDFC Top 200 is a classic example, where the fund who ruled the mutual fund world is now not one of the top 10 funds.

Another example is the SBI Maxgain tax saver which was one of the best ELSS funds some years back but is now replaced by many others.

Here is a study by Yahoo Finance on this topic with respect to funds in the US, which tells that around 92% of top performers do not remain top performers after two years.

Myth #12 – More mutual funds means Diversification

Diversification is an abused word, at least in mutual funds.

Just because you invest in more mutual funds does not always mean that you have achieved diversification. The reason is simple. A mutual fund invests in close to 50-100 stocks. So when you invest in an equity mutual fund, your money is already well diversified across sectors, types of companies, etc.

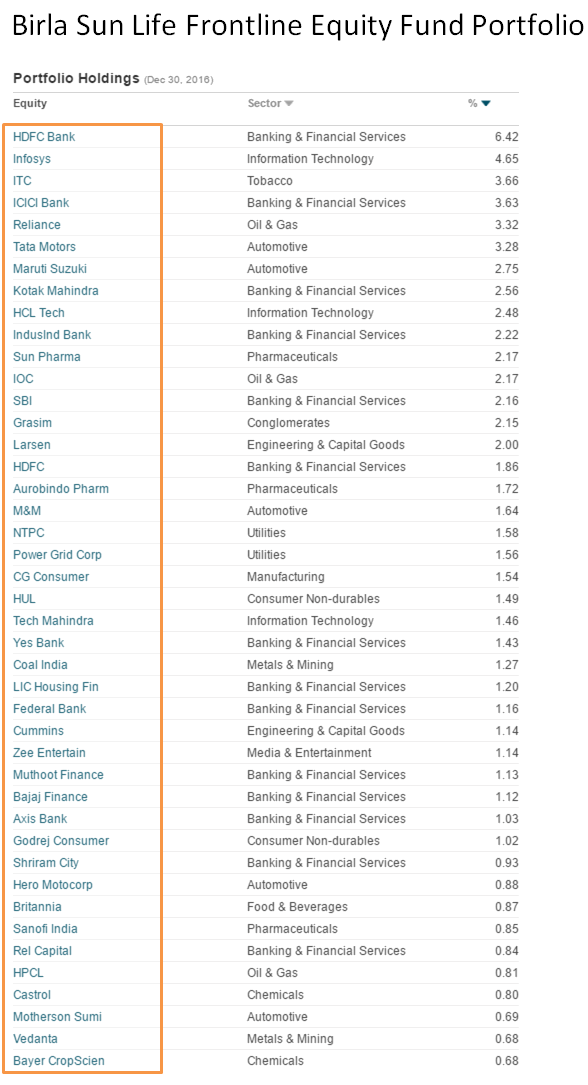

When you add another mutual fund, most of the stocks might be the same and also in the same proportion, giving you very little extra diversification. When you add 3rd fund and 4th fund, almost no diversification happens. Below is the portfolio of one mutual fund and you can see how much they have diversified already.

This is one reason why it’s of no use to invest in 10-20 mutual funds of the same category. 2-4 funds of a similar category are the maximum one should invest into. You should add more SIP amount or lump sum in the same fund once you have chosen 2-4 funds.

Myth #13 – I need Demat account to invest in mutual funds

No, it was never the case.

A lot of people think that unless they have a Demat Account, they can’t invest in mutual funds. You can invest in mutual funds from your Demat provider also, but it’s not mandatory.

So when you invest from ICICIDirect or HDFC Securities, you are actually investing via a Demat account and the units you get sit in your Demat account.

So if you want to invest in mutual funds, you can invest directly from the fund house or through an advisor.

Myth #14 – I can start SIP and forget it for long term

A lot of investors think that once they have started a SIP investment or even lump sum investment they can just sit back and relax for next 10-20 yrs. This is not suggested.

Mutual funds need constant review every year. So you should at least keep an eye on your fund performance. Do not overdo it and start looking at weekly and monthly returns, but do that in 1-2 yrs.

Invest in Mutual funds with Jagoinvestor for FREE

[su_button background=”#FF2F3B” size=”6″ url=”https://www.jagoinvestor.com/mutual-funds#sign-up” target=”blank”] Schedule a FREE Call [/su_button]

Myth #15 – You can’t save tax under 80C in mutual funds

Many people who regularly save income tax through PPF or life insurance policies, do not know that even mutual funds have 80C benefits. ELSS or Equity linked saving scheme is the category of mutual funds which gives you 80C benefits up to Rs 1.5 lacs.

Myth #16 – SIP can be done only on a monthly basis

No, An SIP can be done even on a weekly or quarterly basis. While monthly SIP is the most suitable for all (we all get monthly income), but at times if you want to invest on a quarterly basis or weekly basis, even that can be done.

However, note that it depends on a mutual fund if it gives you the facility of weekly/quarterly SIP or not. Most of them do, but at times, some mutual funds might choose to not have that option.

Myth #17 – Mutual funds investments are complicated

While investing in mutual funds is definitely as simple as creating a fixed deposit. But it’s not too complicated. You need to do one-time documentation to start with and once it’s done, After that you can buy/redeem mutual funds online.

One place where you might feel complication is while choosing the funds out of the big pool, but with your own research or with guidance from someone else (like Jagoinvestor), you can get a set of mutual funds to invest in.

Here is a good mutual funds tutorial for beginners by Deepak Shenoy

Myth #18 – I can’t add more lump sum amount in my fund where I do SIP

A lot of investors feel that if they have started a SIP in a fund XYZ, then they can’t add additional money in the same fund under the same folio. It is not true.

When you invest in a fund (either SIP or one time), you get a folio number. This is like an account number. You can anytime add any amount of fund to the same folio. So if you are doing a SIP of Rs 10,000 in Birla Balanced Advantage fund, and now if you want to add another Rs 1,00,000 suddenly, you can do that.

Myth #19 – You need documentation every time you want to invest in mutual funds

Again a big myth.

Once you are done with the first time documentation, after that every time you want to invest and redeem or switch, you can do it online. The documentation comes into picture only when you want to do changes like your email id, phone or address etc.

Myth #20 – Mutual Funds are not for retired investors

This is entirely false.

There are various kind of mutual funds which are suitable for retirement needs. You can invest your hard-earned money in debt funds and keep them secure while it’s growing at a decent return. One can choose an option for a monthly dividend and get an income.

One can also SWP from a fund, and withdraw a fixed amount each month. One can invest in debt-oriented mutual funds, which can have some equity component for some return kick!.

We have helped many clients to plan for their parent’s retirement money deployment.

Myth #21 – I can’t invest in mutual funds because I need high liquidity

Again a myth.

Mutual funds are highly liquid and you can get your money ranging from instant redemption to 3-4 days depending on the fund type. If you want very high liquidity, then you can invest money in liquid funds, from where you can redeem in 24 hours.

Myth #22 – Mutual funds are not that famous among investors

This may be news to many, but the Mutual Fund’s industry will overtake Deposits in Banks very soon (maybe a decade). Right now at the time of writing this article, the money in India mutual funds was around 18 lacs crore, It has doubled in the last 4 yrs, and set to grow very fast in the next decade.

In the US, mutual funds are already several times bigger than Fixed deposits and it’s going to happen in India too over the long term. So if you still think that mutual funds are some alien concept, then you are wrong. It’s very popular now in India and one of the standard investments products.

Myth #23 – Mutual fund redemption needs the permission of a broker or advisor

Your broker or advisor has no control over your mutual funds. You can do redemption on your own by either installing the app of the fund house or through the portal where you have access to.

In the worst case, you can anytime go to the fund house office or CAMS/KARVY office and apply for redemption. This does not need any approval from anyone.

Myth #24 – I can’t skip an SIP payment once started

A lot of people are worried about what will happen if they skip the SIP in a particular month when they are low on funds?

If your bank account does not have sufficient money for a month, then on the SIP date the SIP will not get processed, but from next month it will go fine again. Mutual funds company does not charge any fine or penalty for this, but your bank can levy a small charge for this like Rs 200/300.

I think it’s good, because that way you will be disciplined enough to make sure that your SIP’s go on time, but also does not hurt you too badly in case of emergency

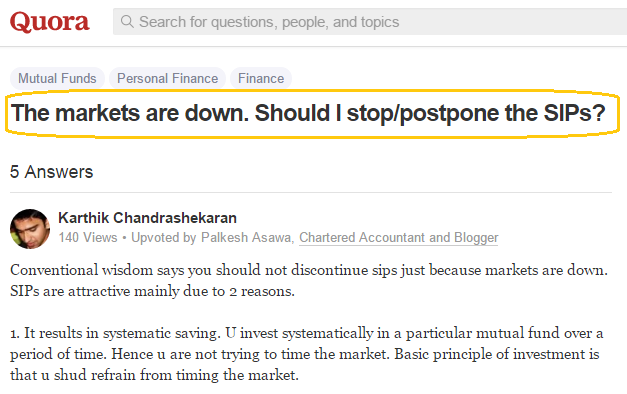

Myth #25 – I should stop my SIP when markets are down

Unless you are an expert in understanding markets and how they will behave (which I think no one knows), it does not make a lot of sense to time your SIP’s. Just let them run in all kinds of markets and focus on your long term goals.

Most of the investors make this mistake that they stop their SIP’s when markets tank. In fact, this is the best time when you should accumulate more Mutual funds units in your portfolio so that when markets are up, you will reap the benefits.

Myth #26 – TDS is applicable when mutual funds are sold and redeemed

Mutual funds are not like Fixed Deposits or Recurring Deposits.

When you sell your mutual funds, there is no TDS which is deducted. You get the full amount in your bank account and then you need to figure out the tax amount and pay it later.

However there is no exception to this. In the case of NRIs, if they redeem their debt funds, then TDS is applicable.

Myth #27 – My money will be locked in mutual funds like other products

Many investors think that in mutual funds their money is locked for a specific period. in case of mutual funds, most of the funds are open-ended funds, which means that you can invest any time and redeem anytime.

There is no lock-in except in ELSS funds (which comes under 80C) and close-ended funds (which specifically tell you the duration for lock-in)

Myth #28 – SIP should not be started when stock markets are very high

Yes, this is actually not a myth, but truth.

But only if you know that stock markets are high. If you are very sure you can figure that out then Yes, it’s better to wait for markets to tank down, and then start SIP. But 95% of the people don’t have time and energy and even expertise to read these signals.

So that’s the reason, why you should not think much when you are starting the SIP. Start your SIP’s irrespective of market conditions. And when markets do down, it’s time to increase your SIP amount

Myth #29 – SIP is always better than Lump sum investments

None of them are better than the other.

SIP’s will outperform the onetime investments in certain conditions and vice versa. SIP’s, however, are more suitable for a common man as it’s a monthly commitment and averages the risk of market volatility.

Here is a good discussion on SIP vs Lumpsum Investments by Monika Halan and Vivek Law in a show called Smart Money

Myth #30 – I can’t switch from one mutual fund to another fund

Many people do not know that it’s possible to move from one fund to another fund across the same fund house. You don’t need to sell the fund, get the money in your account and then again invest in another fund of the same fund house.

So if you have a mutual fund from Birla AMC, you can switch it to another Birla fund without redemption.

Myth #31 – Mutual funds of bigger and trusted brands are always better

Do you know that LIC also has mutual funds business?

However, LIC mutual funds are one of the worst-performing funds across the whole MF industry. LIC mutual funds is not same as LIC insurance.

In the same way, SBI mutual funds should not be confused with SBI bank. A lot of first-time investors in mutual funds investors want to go with trusted brands like LIC, SBI, or HDFC.

Not that mutual funds is a different business, and you need asset management expertise. A small fund house like Motilal Oswal or even Quantum or PPFAS has high-quality funds and should be explored.

Myth #32 – I can’t partially withdraw from mutual funds

Yes, you can. Mutual funds can be redeemed in parts. You just have to choose the number of units you want to redeem or the amount you want to redeem (it will calculate the units required). So that way, it’s a great product. Because in case of deposits it’s either the full amount or none (which is one positive thing also)

Myth #33 – Only humans can invest in mutual funds

Even companies and partnerships can invest in mutual funds. It’s not limited to just humans. So if you are a business owner, you can also go for your business KYC, and then start invest in mutual funds. If you have money lying in current accounts, you can park your excess money in liquid or debt funds and redeem them anytime you want with a single click.

Let us know if you have any more myths or queries related to mutual funds or SIP.

Are you ready to invest in mutual funds?

Are you still waiting to start your mutual fund’s journey? If Yes, then our team at Jagoinvestor can help you start your mutual fund’s journey.

Invest in Mutual funds with Jagoinvestor for FREE

[su_button background=”#FF2F3B” size=”6″ url=”https://www.jagoinvestor.com/mutual-funds#sign-up” target=”blank”] Schedule a FREE Call [/su_button]

We help our clients to set their financial goals, do all the documentation, and give a free portfolio tracker along with mobile apps to check your portfolio.

Yesterday I went to watch a movie late night at Amanora town center in Pune. I and my wife had our dinner at a small Italian restaurant and the food there was quite good.

When it was time to pay the bill, I went to the counter and paid the bill. When I got the bill in my hand, I realized that there is a problem. They had charged me a “service tax”. However, the main issue was that there was no service tax number mentioned on the bill.

Charging Service Tax without Service tax number is Illegal

Yes, you heard it right.

The Bill copy did not have any service tax number mentioned on it, but the restaurant had put a service tax charge on the bill. This is Illegal and can’t be done. Hence I told the staff that I can’t pay that service tax unless they give me the service tax number.

The staff, as usual, was ignorant about this and told me that I should talk to “owner” and tried to give me his number. However I told them, it’s not what I will deal with and I will not leave unless they give me service tax number because they are illegally charging service tax.

Finally, after 5 minutes, the staff told me that the Owner is not reachable and they will give me a service tax number later. But I refused to budge and demanded them to pay me service tax amount back and not repeat this, as its illegal.

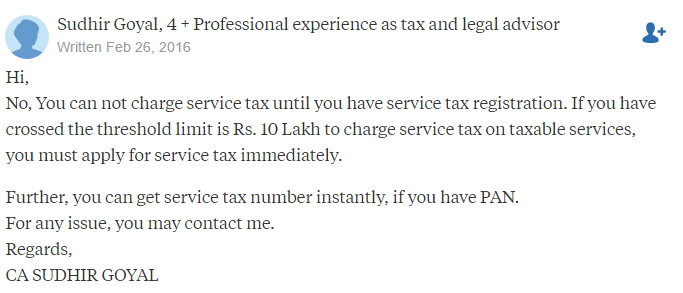

Finally, they had to refund me back and I took the money. Here is what another CA has to say about this on Quora

I realized that not more than 1 out of 1000 people know this rule, and this needs to be spread among people. Many restaurants are misusing the fact that now people know that service tax is an unavoidable tax and has to be paid, however many do not know the rules and conditions under which any business can charge it. Even Service charge is now an optional thing and you decline to pay it.

Note that many restaurants will tell you that they have applied for the service tax number and are awaiting it, but this is mostly a trick to fool you and to save themselves out of the situation and embarrassment. However even in that case, it’s not right, and you should demand to see the proof for that.

The service tax number is mandatory to charge Service Tax

As per service tax rules, service tax can be charged only if you applied and got your service tax number. This service tax number has to be written on the invoice copy. Without that, you cannot charge service tax from your customers.

In the case of restaurants, the service tax has to be charged only on 40% of the FOOD bill and beverages. So if you eat for Rs 1,000 (food + beverages), then only 6% on the total bill is to be charged, which will be Rs 1060.

Here is a sample of a correct bill that mentions the service tax number on the bill itself.

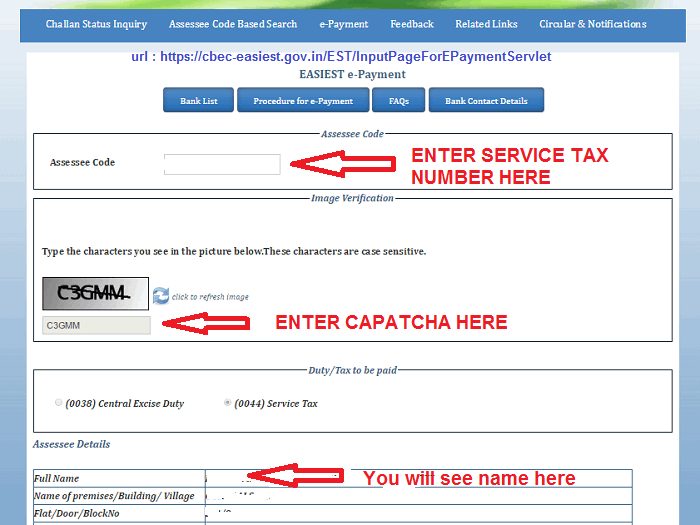

How to verify whether the service tax number is valid or fake?

Few people ask me, how to verify that the service tax number mentioned on the bill is not fake? Because the hotel guy can just randomly put some number, which looks like the service tax number.

The simple solution is to check the name of the person/company under whose name the service tax number is registered. It just take 1 min to verify that.

Step 2: Enter the 15 digit Service tax code (also called Assessee code)

Step 3: Enter the captcha

Once you do this, the page will show you the

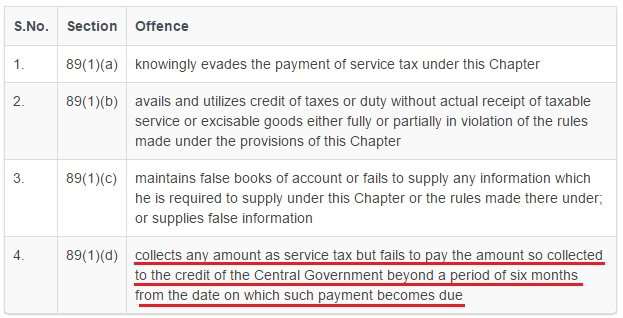

Non Bailable Offence under sec 89 of service tax

If service tax is charged without a service tax number, then how will it be paid to the government? Because you need the service tax number to pay the tax to govt. Sec 89 of finance Act tells that incase an offense is done like this, then the person can be jailed for up to 1 yrs (and up to 2-3 yrs in case the amount involved is above Rs 50 lacs).

Below is a snapshot is taken from Taxguru website which writes about tax-related topics.

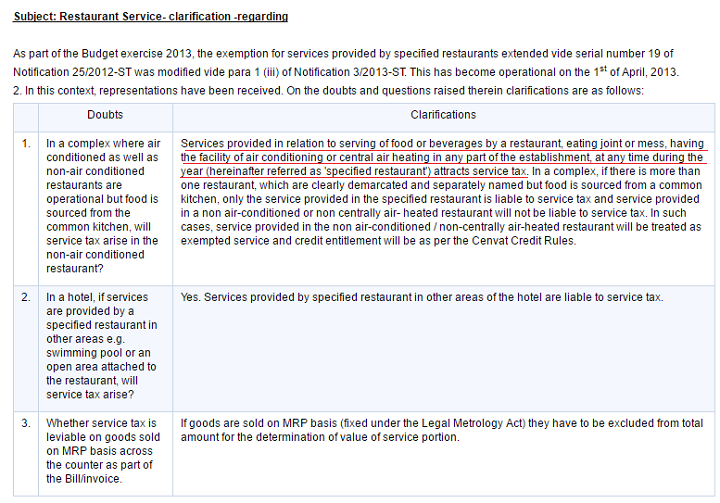

Do you need to pay a service tax if you don’t sit in AC?

This is very interesting.

One of the biggest questions people raise is that if a restaurant has AC in one part, but not in other parts and if you are seating in a non-AC section and dined, still do you have to pay the service tax?

Or imagine is AC was not working at that time, even then will you be charged the service tax?

The answer to that is YES.

Sorry, but the service tax rules clearly state that. The service tax rules simply say that if the establishment (the hotel or restaurant) has the facility of air conditioning or central air-heating in any part of the establishment, then they have to charge the service tax in their bill.

It does not matter if you got the benefit of the AC at the time of eating. All that matters is that they have AC anywhere on the premises.

This itself is enough for a restaurant to charge the service tax. However, if an establishment is divided into two parts with the two different names and entities, then the non-ac part can’t charge the service tax (where the service was given), even if the food was prepared in the AC part. Here are the exact wordings from the service tax notification on this issue

3 things to remember when you visit a restaurant next time

When you visit the restaurant next time, make sure you keep in mind the following 3 points.

Check if service tax number is mentioned on the bill or not, if they are charging service tax on the bill

Make sure the service tax is charged @6% on the food + non-alcoholic bill and 15% on the alcoholic charges

Make sure there is AC in the restaurant if you are charged service tax.

Spread this Information

There are thousands of restaurants that might be charging service tax illegally without having a service tax number and millions of customers on a daily basis are paying that as they are not aware of the exact rule. This is practiced by many restaurants, small hotels, and many other businesses.

So spread and share this article as much as you can so that more and more people can know about this. Also, share your experience with this.

Do you know that every person is entitled to 1 free credit report and score each year from each of the credit bureaus in India? There is 4 credit bureau in India which are CIBIL, Experian, Equifax and Highmark.

As per RBI guidelines, now each of them have to provide one free report each year. For those of you who do not know, a credit report is a document that has all your past loan repayment history and a score that tells a lender if you should be given any loan or not.

So each lender checks these reports and scores as part of their loan approval process. It’s very important for investors to keep track of their credit scores from time to time.

Step by Step Process to Check FREE Score online

So today I am going to share the process of getting the free report and score online from each CIBIL Transunion, Experian, Equifax, and Highmark credit bureau. I have personally checked my own score + report from each credit bureau and I will teach you the step by step process of how you can do it too. The whole process is online and you do not have to fill any form by hand or send any documents anywhere.

Note that your credit report will be available only if you have taken some kind of loan or credit card. So if you do not have any kind of loan, you will most probably not have it, unless someone has misused your documents and applied for some loan.

So let’s start with CIBIL first.

How to check the FREE CIBIL report and Score?

In order to check your free CIBIL Transunion report and score, you need to follow below steps –

Enter your current details like Identity Details, Contact details etc and continue to step 2

Confirm your email on next page, and then go to your email to click on a link inside for email verification

On the page, enter your voucher number and move ahead

You will then be asked for some verification questions related to your debt.

Once you answer them correctly, you will be taken to your free report

How to Check FREE Equifax Credit Report and Score?

Here are the steps to check your free Equifax report and score

Download the Equifax India mobile app (android or iOS)

Register your email and get temporary PIN number

Enter a temporary PIN and reset a new PIN and then log in to the App

Enter your Name, Phone, Date of Birth and Adhaar Card

An OTP will come to your phone number which is linked to adhaar card

After OTP verification, your KYC check will be complete

On the app, click on the link “Credit Report”

On the page, click on the link “Request Free Credit Report”

Enter all your details and then click on Submit

Now your “Knowledge-based Assessment” will be in the pending stage.

After 24 hours, your knowledge-based assessment will get generated.

Click on the app, and click on the link which says “Knowledge-based assessment”

Give correct answers to the questions asked, after which your credit report will be in the “Initiated” stage

After 24-48 hours, you will get an email with the free credit report as an attachment

Download the attachment and have a look at your report and score.

You can also login to the app and check your report there

For those, who do not have mobile linked with adhaar, they can send their KYC documents along with a filled form to Equifax customer care, and on verification, they will get their free report in 48 hours

How to Check FREE Highmark Credit Report and Score?

Here are the steps to check your free Highmark credit report

Go to https://cir.crifhighmark.com

Register as a new user and set your new password

Activate your account by clicking on the link inside the email

Again login and choose an option to get a free report on the top of the page

Enter all your details and click submit

You will get a notification that inquiry was successful and now wait for the email

After a few hours, you will get an authentication email

Click on the link and verify some of the information asked on the page

On successful verification, you will get an email with PDF attachment after 48 hours

Open you free Highmark report and check it

I hope the above videos must have given a good clarity on what needs to be done to check your report online, totally free of cost.

Why you should check your report every year?

A credit report is fast becoming a very integral part of the credit system in India from the last few years (it’s already is). It’s highly recommended to have a clean record and a fairly good credit score if you don’t want to get rejected for your future loan applications.

Now with one free report from every credit bureau, everyone should check theirs from each company and make sure that all the credit remakes and details like name, age, score, and other details are correct. If you find any problems, immediately raise a dispute with the lender and the credit bureau and start fixing it.

PRO Tip – Subscribe to each report with the gap of 90 days

Don’t subscribe all 4 reports at the same time. Time them one per quarter so you can monitor your credit report for any frauds frequently instead of once every year.

So the point is that if you divide your free reports checks every 90 days, you will be able to find out if there were any frauds happening throughout the whole year. However, if you just apply for all the reports in a single month, then you will be able to apply them only next year.

Let me know if you face any issues while checking your free report

Think for a moment that you have 3 yrs worth of your salary in your bank account.

How does it feel?

So if you earn Rs 10 lacs a year, you have Rs 30 lacs lying in your savings (other than real estate). If you earn 20 lacs per annum, its 60 lacs!

But in real life, most people do not take enough effort to save more money. It’s on their wish list to “start saving from next month”, but the motivations soon fizzles out. Most of the people are so busy and stuck with various problems in life that with each day, saving money for the future remains a distant dream for many.

Are you one of them?

Life has various dynamics.

Many people are stuck in a bad job, while some people are in a bad marriage which is draining all their energy and time. Some people are running around to arrange for a house down payment, while some are wondering if they should have a second kid or not!

Life keeps throwing so many things at us, that we forget where we are headed towards and we are not able to see how our actions today will shape our future.

We keep dealing with the NOW, only to realize many years later that our FUTURE is almost there waving at us. And then suddenly we realize that we have so much to catch up in life. More health, More money and more happiness!

We start our jobs in our 20’s, then settle by the end of the ’30s, move to next level in our lives while we are in our 40’s and then in this journey we realize we are approaching our 50’s and if we have not done a good job of saving enough money then we PANIC !

And we tell ourselves – “Oops .. I could have handled my life in a better way, if only …”

As per an HSBC report, around 47% of the Indians have not yet started saving for their retirement or have stopped it after starting.

6 reasons why you should save money and create wealth

Today I want to do a deep conversation regarding saving money. I know you might feel, is there a lot of it to talk about that?

Today I want to make sure that this is the last article, to get serious regarding saving & investing more money in your life (I will refer to “saving and investing” as “saving” in this article henceforth).

Almost all people feel that “saving money” is only related to securing your future. The equation for them is

Save money = Lead a better life tomorrow

But there is more to it!

[su_table responsive=”yes” alternate=”no”]

Reason #1

To secure your future

Reason #2

To do what you love in life

Reason #3

To spend and live a better lifestyle

Reason #4

To be financially independent

Reason #5

Peace of mind

Reason #6

To pass your wealth to next generation

[/su_table]

There are various other angles you need to think about, and that’s what I want to discuss today. So read this article with all our eyes open!

Reason #1 – To secure your future

Let’s start with the most basic and core objective of saving money. You save money to accumulate the money and use it for your future requirements.

Let me give you a surprise – “One day, your salary will stop coming in your bank account”

There will come a time when you will be left with 40 more years of your life and there won’t be a regular salary coming into your account like it happens today. You need to create a big enough corpus, which helps you to lead a life you desire for the next few decades till you die.

You should not be worried about “death” in today’s world, It should be “living enough”.

Some people think they can avoid creating their wealth because their kids will take care of them. However, it’s up to you to decide if that’s the right approach towards life or not.

Savings and Investing definition by a 9 yrs old girl

Long back, Subra had asked a 9 yrs old kid to read a book on money and summarize what she learned about “saving and investing” and she gave a very crisp understanding about it. Please appreciate the simplicity of the girl’s thoughts.

Saving: Saving money is very important. We should save money because if one day suddenly we need money we will have it with us. If we just keep on spending all the money that we get and one day we need money we will not know what to do. I am also saving all my pocket money because I might need it in the future. I have kept it in a bank account and I get interested in that every year.

Investing: Investing makes our money grow. Just as a plant grows from a seed to a plant. When we keep our money in a savings bank we get interested but if we will invest our money in fixed deposits, shares, mutual funds, public provident funds, etc. our money will grow from a small amount to a big amount faster. Real money takes more time to grow whereas a plant grows within weeks.

Start saving some money for future

If you can’t manage to save enough money, at least start saving some money starting next month TODAY. Let me share with you some numbers on this. If a 30 yrs old person invests Rs 10,000 per month for the next 30 yrs consistently, then @12% average return over the long term, a total of approx Rs 4.4 crore can be accumulated.

I know a lot of people who can surely start with Rs 10,000 per month investment. Don’t worry if you can’t do that much?

What about Rs 5,000? Rs 2,000 ?

Anything is a good start! , upgrade later – but at least START.

Our team at Jagoinvestor helps our readers to start their SIP in mutual funds and track their goals on an ongoing basis. If you are interested to start your wealth creation journey with us, just leave your details here and a mentor from Jagoinvestor team will reach out to you in the next 24 hours

[su_button background=”#FFA52F” size=”6″ url=”https://www.jagoinvestor.com/mutual-funds” target=”blank”] Start your SIP in Mutual funds with Jagoinvestor Help [/su_button]

Reason #2 – To do what you love in life

Do you love what you do?

No, I am not talking about pursuing your passion for living or doing a full-time job in the area which you love. All I am saying is do you have enough time and money to do things you love for a few hours each week? Something which you truly want to do other than your regular job work?

Do you love traveling to new places, but you are stuck because the EMI needs to be paid first?

Do you love photography, but those costly lenses seem to be out of your budget?

Do you want to socialize more by throwing a party for your friends, but worried about how you will afford to do it?

Are you afraid to tell your boss that you want to go on a month-long road trip, with your best friend which was planned years back?

Want to go on a weekend trip with your friends, but oops. it’s out of the budget!

It’s going to be very tough to achieve all the points mentioned above if your bank balance is very low. Less money means less power with you!

While you cannot afford a lot of things, you can’t also arrange for a lot of time to do all these things, because you can’t make some tough decisions because you are so dependent on monthly paychecks.

You need two things!

You need money or time to pursue your hobbies and both of these will come only when you focus on creating wealth.

I understand that you will not be able to achieve all these things right now, but If you don’t start your wealth creation right now, you will NEVER be able to achieve the above. Enough wealth in your kitty gives you that power to do things you love.

If you are so much dependent on your monthly paychecks, it’s going to be very suffocating going forward. A lot of wonderful people are dying slowly inside because they have no wealth created.

Reason #3 – To spend and live a better lifestyle

A lot of things in life do not require money. A great nap, a conversation with a good friend, a simple meal with your loved ones.

But then there are things in life which require money.

Yes, I am talking about those materialistic things.

A better Car

A better house

Dining in a great restaurant

Partying with your friends

Buying that gadget

Going on that trip

Redesigning your house

That Ladakh road Trip

That DSLR Camera

Travelling to exotic places with your family

You will spend money on various experiences and possessions, only if you have the money in the first place (not always, but most of the times), and you be able to do it only if you have money saved at your end at the first place.

Your lifestyle will improve only if you have created enough money.

While you can always take a personal loan and upgrade your car or go on that vacation and earn all the facebook likes, I am not talking that!

I am talking about, the real upgrade in your lifestyle which does not increase your EMI or stress level and does not compromise your cash flows to a big extent.

It’s easy to upgrade your life from a bike to a car and a rented apartment to the first house, but then beyond that’s it’s not as simple as it was earlier. It takes a good amount of money and dedication because we get stuck with EMI’s and mid-level crisis in our 30’s

So see, what are your aspirations for yourself and your family? What kind of life are you looking forward to in the coming times? Is your wealth enough to lead you there? Are you doing enough for that?

Reason #4 – To be financially independent

Don’t confuse financial independence with retirement.

Retirement happens “when you don’t work anymore”

Financial Independence happens “when you don’t work for money anymore..”

While retirement is linked to age (which is generally around 60), financial independence is a function of wealth and not your age. Financial independence can happen even at the age of 35 (My best friend at age 32 is already financially independent)

Where do you stand in your financial independence?

Financial Independence is often referred to as financial freedom. Nandish likes to describe as “A situation where your passive income equals your desired lifestyle expenses”

For a normal investor, financial independence can happen only when you start your wealth creation journey well at the start of your life and are disciplined enough not to disturb it for a long time.

Do you always want to keep doing the same job you are doing? And wait desperately for that “salary credited” SMS at the end of the month? How dependent are you on that monthly inflow in your bank account? How will your life look like if that SMS that does not arrive (I mean the money) for the next 6 months?

Millions of people go to their jobs in the morning with different moods depending on the day. They are happiest on Friday and very sad on Sunday night. You need to seriously start investing for the goal of financial independence if this is the case with you.

You need to also reduce your dependence on your active income (salary) as you move from age 25/30 to age 45/50. You should have created enough wealth in the first 10-15 yrs of your life that some part of your expenses can be met by passive income your wealth can generate if things go wrong.

I am not saying that you should create wealth and then start the passive income right away, but you need to create that situation for yourself. It will bring peace of mind (which I am going to talk in detail next)

Reason #5 – Peace of mind

Not have enough money brings a lot of stress. If you need peace of mind, you need enough wealth on your side which can comfort you!

You will keep worrying about the future now and then and every small financial problem will give you goosebump and force you to think about your scary future.

Imagine a guy who is around 45 yrs of age, and has not to create any significant wealth to show. By this time, he should have ideally created a corpus of 1 crore, but he has just 2 lacs in an FD which might get broken if some financial emergency happens!

This is bound to cause a lot of stress.

Various thoughts will cross the mind …

How will I meet my financial goals?

What if I lose my job?

What if I suddenly need a lot of money?

What if I am not able to give my kids all the things they want?

A respectable amount of money saved at your end might not end your worries, but it will surely bring some peace of mind and lower the stress. You know you are not in that bad shape and have arrived somewhere in the middle at least.

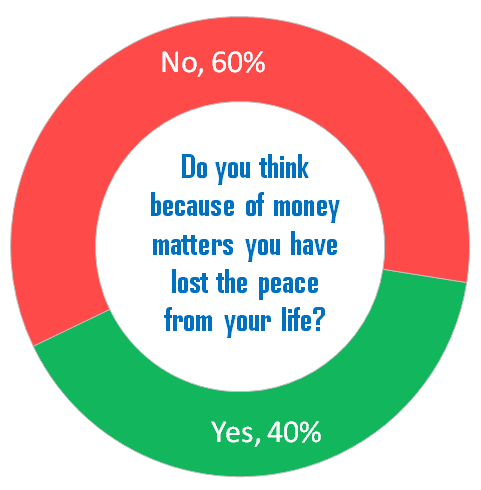

We surveyed with as many as 2,440 investors and we found out that 40% of the investors in our survey reported that the money matters have taken away their peace of mind.

As a general rule of thumb, If you have worked for X yrs in your life, you should at least have X/2 years worth of basic expenses saved at your end. This I think is the minimum one should aim for.

Our team at Jagoinvestor helps our readers to start their SIP in mutual funds and track their goals on an ongoing basis. If you are interested to start your wealth creation journey with us, just leave your details here and a mentor from Jagoinvestor team will reach out to you in the next 24 hours

[su_button background=”#FFA52F” size=”6″ url=”https://www.jagoinvestor.com/mutual-funds” target=”blank”] Start your SIP in Mutual funds with Jagoinvestor Help [/su_button]

Reason #6 – To pass your wealth to the next generation

A lot of families struggle for money generation after generations. The grandfather worked for money all their life, then father and then the son is also doing the same.

Many people who struggle financially set a goal in life that their kids should not face the same. They want to teach them money lessons and make them responsible, but also want to leave them a house and some wealth which makes their start a little easier in life.

Is that the right approach?

It’s a debatable topic if that’s the right thing do to or not. Many people believe that they should not handover anything to kids and let them create their own life out of what they have learned. Let them see the struggles and only then they will appreciate what they earn in life.

While that’s the correct approach for many people. I am sure we have many others who will not agree with that thought process in the same way.

Anyways, coming to the point, if you create wealth in your life, you can leave some part of it for your kids so that they can pursue things they truly wanted to do and not work just for money to bring food on the table.

A lot of wonderful people are never able to do things in life which they truly want to do. They are not able to live their own life fully because of the money matters. You need to check for yourself, if passing wealth to your next generation is part of your plan or not?

What will happen if you don’t save enough money for future?

So to summarize this article, there is a great possibility that one or more things mentioned below will happen to you if you do not get serious about saving money in your life going forward.

You will have hard time maintaining a good standard of living

You will depend too much on others (your kids maybe) for money

You will be spending a lot of time worrying about the future and how will your life end

You will be too dependent on your active income and will be forced to keep working even when you don’t like it

It will be hard for you to focus on things you love to do because you don’t have enough money or time

You will find it tough to lead a better life compared to current lifestyle

Final words

If you have still not crossed the age of 45, You still have a good chance to create a respectable corpus by the time you retire, even though you have lost a lot of time for compounding. Our team can help you in getting your financial planning done if you are interested to do leave your details for a small chat!

Just make sure you do not reach your pre-retirement age of 50+ without doing anything because that’s the zone where it’s going to be very tough creating any sizable corpus.

This is a guest post which is already published on Ravi Karandeekar’s blog, which is an excellent blog when it comes to real estate (more related to Pune). Ravi discusses various projects and his experience meeting with Builders and various stories of real estate frauds etc.

A few days back, I read a real-life story of a female IT engineer in Pune and she shared various aspects of her life in detail, which I thought should be read by more and more people and I took permission from Mr. Ravi, if I can republish his article on this blog, which he agreed to and I am thankful to him.

Here is a great write up below.

—

Hi Ravi,

I regularly follow your blog and I like your sarcastic style of writing. I have read several of your articles where you have highlighted the importance of living a quality life versus living a life under pressure to own a house as soon as possible at any cost in huge debt.

I think in life we have to make certain choices where we cannot achieve what others can because our circumstances are different. Mine is another such case.

I am an IT engineer and a daughter and a wife.

I am the only child of my parents so their entire responsibility is on me.

My parents are simple middle-class people who worked hard, saved every penny so that they can give me a comfortable life and a good education.

They sacrificed nearly every personal need of theirs so that I can go to a convent school, become an engineer and have a happy childhood with all worldly comforts. Beautiful clothes, birthday gifts, toys, ice creams, picnics. Everything was for me and only me.

We lived in the heart of the city

Until I graduated we lived in the heart of Pune city in our very old ancestral rented home. They did not even buy a new flat within the city limits although they could have afforded it.

If they had bought that flat they would have had to cut out almost all the comforts from my life and quality education.

So they bought a cheap apartment on the outskirts in a pathetic locality (just as a backup) while we continued to live in our ancestral home.

That 1.5 lakh difference mattered to them. And they made a choice – Me

When I graduated eight years back we had to move out of our ancestral home.

Our backup apartment is on the 3rd floor with no lift and my mother has health issues because of which she cannot climb those 3 sets of stairs.

So eight years back, at the age of 22, I had to think about our future accommodation.

My starting salary at that time was 24K and the rent was 7.5k. My father retired around the same time with a government pension. There was not enough money to buy a new flat in the city.

I had 2 Options

So there were two options.

Option 1: Save that 7.5k of rent for my future life and let my parents stay on the 3rd floor in a sad locality.

If I save the rent money I may even be able to buy a home inside the city in 7-8 years.

Or in that money, I can have a lavish wedding.

Whatever!

My mother’s diabetes had impaired her health and climbing stairs would have been extremely difficult. She compromised saying “I won’t get out of the house much so I don’t have to climb the stairs”. From age 55 she would have been trapped in a house for months like a caged animal.

My father too was old. The neighbors were not nice. Water supply problems were there. Medical facilities, our relatives and all the other things that we were used to would have been unreachable for us.

Parents were ready (as always) to live that life as of course they don’t want their daughter to spend 7.5k every month. Our scrupulous traditional middle-class parents will never touch their daughter’s money!

Option 2: Spend the rent money, I will have fewer savings and let my parents live a decent life.

All their life they sacrificed and adjusted. Don’t they deserve a good life at least during their last years?

Importance of TIME in life! YOLO!! (You only live once)

My parents are not going to have these last (healthy) years again!! Soon they will cross mid-sixties after which they will be too old to even get out of the house.

This is the time window (55 to 65 years) when I can give them the lifestyle they deserve as the proud parents of a highly qualified daughter. So I take the decision and rent out an apartment (against my parent’s wishes).

Our backup apartment stays locked.

Eight years have passed and option 2 has worked out really really well!

How?

We live in a beautiful spot in Kothrud surrounded by greenery and beautiful bungalows.

My mother goes for walks every day since we live on the ground floor. She enjoys going to the market and being able to live a normal life.

My father is thrilled as there is a katta nearby where all the retired members like him meet in the evening.

All our relatives live nearby. We live in a 30-year-old 1 BHK and the floor tiles belong to the 70s era. But the people here are so friendly we live like one big family.

I can get a flat on rent in a high rise in a cosmopolitan atmosphere in Baner or Wakad (where I would be very happy btw ).

But here we are surrounded by Marathi families like ours. There is an excellent hospital nearby. The convenience, homeliness and the safety of the neighborhood are important to me. The society does not have amenities like swimming pool, club house but my home is filled with happiness.

My Priorities

Years passed, I got promotions and salary increased. I was easily getting a home loan. 1 BHK was a piece of cake and 2 BHK was also possible.

But turns out not buying a flat was very wise. There were many things that had to be handled first. We planned our monthly budget well, saved most of my salary, spent smartly and also had a little bit of fun.

Four years back my mother had a heart attack. Several hospitalizations and a bypass surgery set me back by around 8 lakhs.

But that was easily managed. I was never tense about money and my parents were relieved that we don’t have to borrow from anyone.

I had managed my finances so well that I gifted my mother a pair of gold earrings 2 months after the surgery for a speedy recovery!

I am happy too!. I was able to save for my own wedding. Since our wedding expenses were well within our reach we were able to enjoy it completely.

I have also been able to fulfill some of my dreams. I am passionate about travelling and I have been to my dream destinations Himachal Pradesh, Kerala, Dubai and New York.

In these eight years, I have lived a fulfilling life. Dining out in fine restaurants, going shopping in malls are some of the things we never thought we would do.

Parents/Family suffering because of loan

My folks are happy that I am able to have fun and don’t have to scrimp and save like a person in debt. I do not frown like a debt-ridden son when some unexpected expense turns up. I have seen the scenes from movies\tv serials where the son reproaches his parents when any expense comes up as he has a big loan and says “Baba atta Kasa Shakya ahe! Tumhala Kalat nahi ka loan ahe” (English meaning is – “Dad, How is it possible right now, dont you know there is a loan”). Way to go, son!

This is what you give your parents in return for their entire life spent on you!!. Unbelievably, I have seen this scene in real life also in many homes!!!. These guys have a 2 BHK and a Sedan worth 10 lakhs but they will frown upon if their parents\wife have to have something basic.

There was a time when my parents made a choice between me and their dream home. When I grew up I made a similar choice. It’s okay if I don’t have my own flat at the age of 26 like IT engineers do.

I will have it when I am 35 or 40 years old. But these 10 years of my life were important to me.

Spending on top-notch medical treatment, living comfortably, travelling around the world, saving for my wedding, supporting my husband was my top priorities.

All the while I am saving money aside for my dream house too. I am halfway there, slowly and steadily I will get there. You must work out a plan that suits your circumstances and lives happily because you only live once.

Regards,

—

2 Tough Question for all readers

Do girls take the decision of buying a house in a more sensible way compared to guys?

Do males face more life issues when it comes to “home ownership”?

Disclaimer: This is a personal story and views by 1 person depending on her life, her experience, and her circumstances. Let’s not judge male/females by this one article alone.

Please share your perspective about this article and what do you feel about the issue? How is a male life different then a female when it comes to buying a flat considering how our society has shaped up to date.

I would like to hear your views and stories in the comments section.

Today we will discuss why you need to stop investing in bank fixed deposits.

I know you are a bit shocked by this statement, but my only attempt is to give you some understanding of why banks fixed deposits are not the best financial products in these times for your long term wealth creation. There are other better alternatives today if your focus is assurity of returns, near inflation returns and convenience of investing

You can either read the article or just watch this 10 min video below where I have share why you should avoid investing in fixed deposits.

Why we create Fixed Deposits?

Since our childhood, I think most of us have only heard about Fixed deposits and PPF as investment products. We saw our parents talking about fixed deposits all the time. They broke “FD” when they needed sudden money.

And FD’s become were like the default financial product for most of us and when we started earning, we just created fixed deposits because that’s all we knew about.

On top of it, the fixed deposits come with assured returns of 7-8% (though the FD rates are going down and down these days). Also, almost all the banks offer the online fixed deposits creation (not breaking it) and that fact also adds to our love to creating fixed deposits whenever we need to park our money for some months/years

But, now there is a great alternative for fixed deposits called Debt Mutual Funds. This article will focus more on fixed deposits disadvantage and we will touch upon debt mutual funds to some level, but this is not a deep tutorial on debt funds

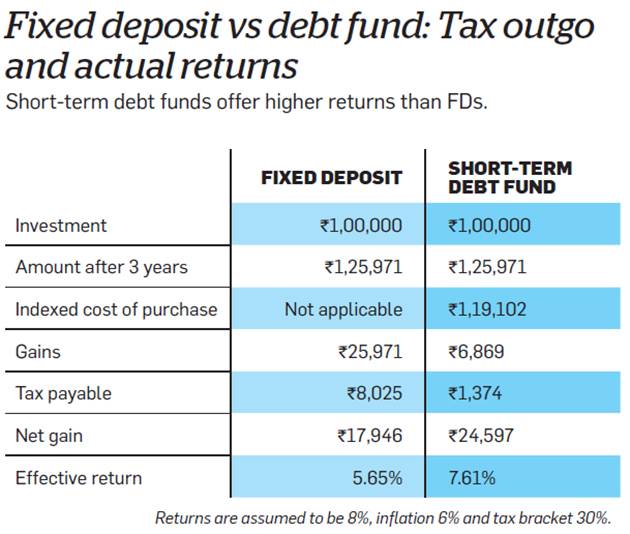

a) High Tax on FD – Fixed Deposits do not have any special taxation benefits. If you are into a 30% tax bracket, you will have to pay the tax on the interest you earn in a year as per your tax slab.

So if you create a Rs 10 lacs FD and you earn Rs 80,000 in interest (@8%) then you pay Rs 24,000 as the tax if you fall in the highest tax bracket. That’s not the case with Debt mutual funds. While debt mutual funds are not tax-free, their taxation is much better compared to a fixed deposit.

The video below explains how fixed deposits taxation is different compared to debt mutual funds.