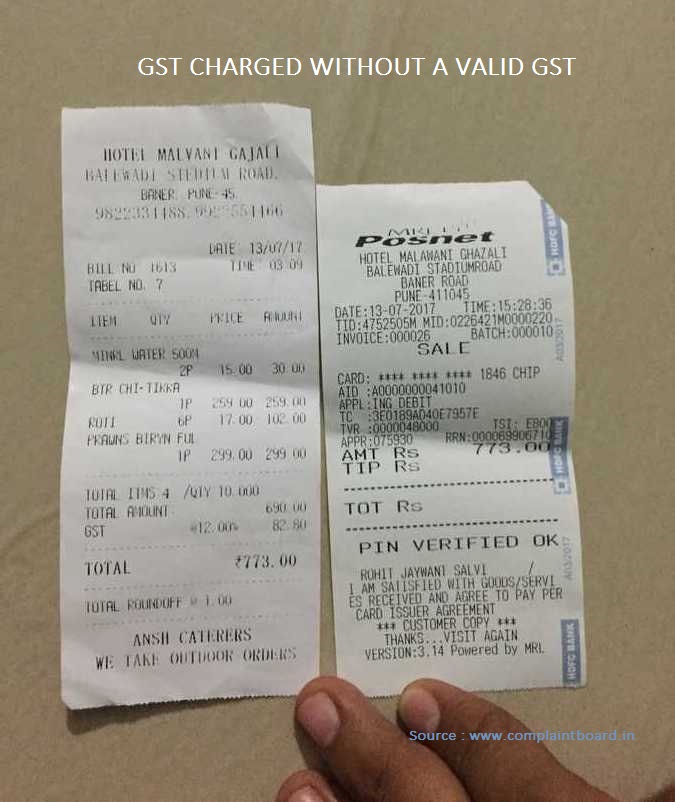

Now a days various restaurants and businesses are putting fake GST number on the bills and charging extra from the customers without registering with the GST department. In this article, we will teach you how you can check the validity of the GST number and its really valid of not in just 30 seconds. It’s a simple process that can be done with 2 clicks.

GST is now a reality and almost everywhere GST is charged. You can see that suddenly those restaurants who never mentioned any taxes in their bills have also started adding 18% more on the bill on the name of CGST and SGST (more on that later)

How fake GST number on bills is creating a hole in your pocket?

GST is a big reform in the country and while govt claims that it’s a simple tax, there are lots of inherent complications to this taxation system. A common man thinks that now everything has got costly by an extra 12% or 18% (especially in smaller cities)

One of my friend in Varanasi told me that a small shop near his place is charging extra Rs 2 on a packet of biscuits now telling the poor customers that its GST tax which is now to be paid.

While that’s an example of a mid-level city, many restaurants have also started putting fake GST number on the bill and have started charging extra taxes which they will never deposit to anyone.

How to verify the GST number?

Verifying the GST number online is a very simple procedure. First of all check the GST number on the receipt. It’s 100% mandatory to mention the GST number on the invoice or bill.

If someone is charging GST, without mentioning the GST number, then it’s illegal. Earlier it was service tax, now it’s GST number which is mandatory to put on the invoice.

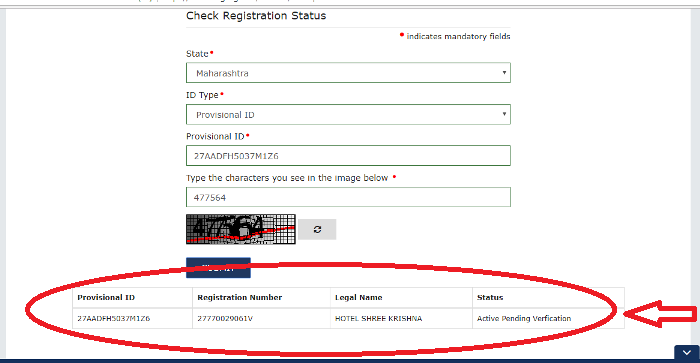

Here is how to check if GST number is real or fake?

You will see the business name registered, match it with the name of the business on invoice

What if I don’t have a GST number?

Some businesses still don’t have the registration number confirmed, but they have the provisional GST number with them, so you can also check the provisional GST number online and verify them. Even you can verify the business based on their PAN.

Here the steps to verify GST number in this case

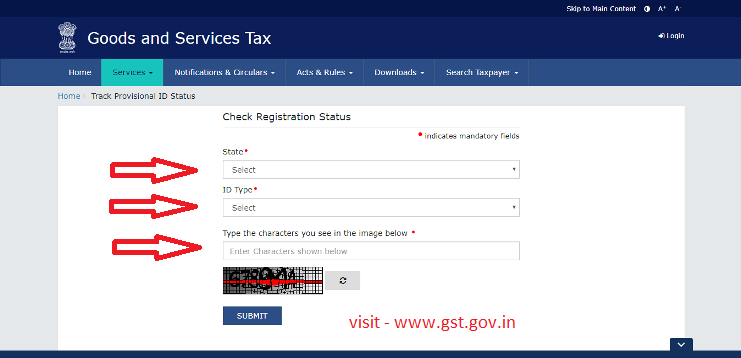

Go to this link and you will be asked various details which you need to enter.

Here you need to fill the data required correctly i.e. state, ID type (PAN number, GST number or Provisional ID), ID number and verification code. At last click on submit and then scroll down to see the details of the registered business.

This is how you can verify if GST number is valid or not with the help of a provisional ID or PAN number. As of now, there is no way of finding or verifying the GST number just by entering the name of the business entity.

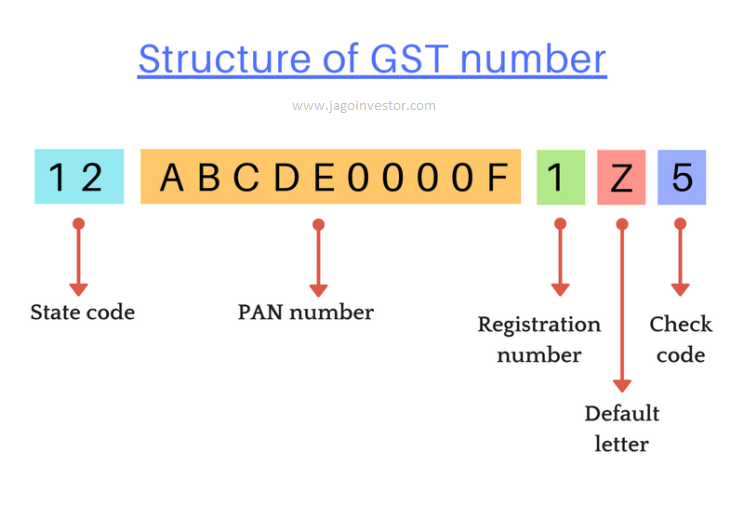

GST is a 15 character code

It’s an important point to know that GST number is 15 characters which are a combination of numbers and characters. These 15 digits are broken into 5 parts as follows

First 2 digits are state code where the business is registered

Next 10 digits are PAN number of the business

13th digit is registration number of that store or business with same PAN number

14th digit is Z by default for right now

And the last i.e. 15th digit is a check code

What is someone says “I have applied for GST number”?

Some shopkeepers and business owners are playing the trick of “I have already applied for GST number, It’s not yet approved?”. This is to give a feeling to customers that they are rightfully charging GST. But this is again a fraud.

Because when they apply for GST number, they get a provisional GST number anyways and they need to either put a GST number or provisional GST number on the invoice/bill

Don’t fall for this trap and demand to see the GST number.

Where to complain about fake GST number?

GST department has dedicated the helplines for you to complain or ask any queries regarding GST. Here are the emails and phone numbers

Earlier RTI filing was too much pain, because it was very much time-consuming as it was an offline process.

A form was to be filled and then a Rs 10 stamp was to be attached and the entire form had to be sent by post to the required department of the government. The form took approximately 3 to 4 days to reach the concerned department.

So many people who wanted to file RTI refrained from doing it.

However now filling RTI is just a click away because we can file it online. I will tell you 4 SIMPLE and EASY steps to file RTI ONLINE without any hassle. But before that, let me explain to you in brief what is an RTI act.

What is the RTI?

The Right to Information Act 2005 commonly known as RTI is a law using which an Indian citizen can request for information from state or central government departments and offices. And such a request should be processed in a timely way as mandated by the RTI Act.

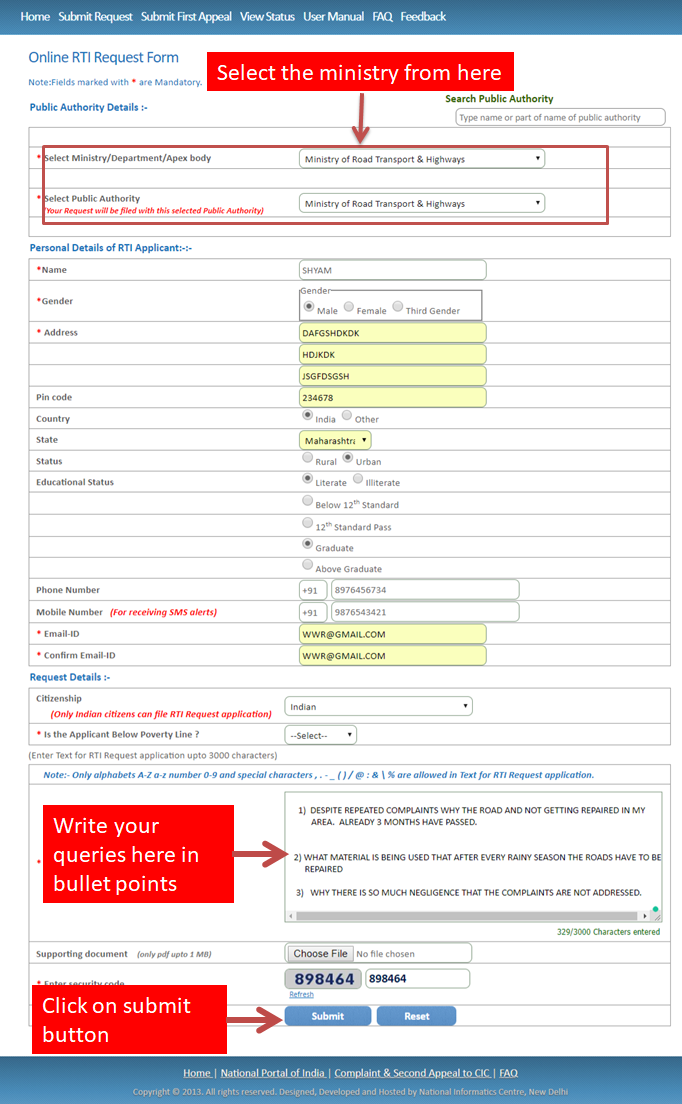

Let me now share what steps you should take to file RTI form online.

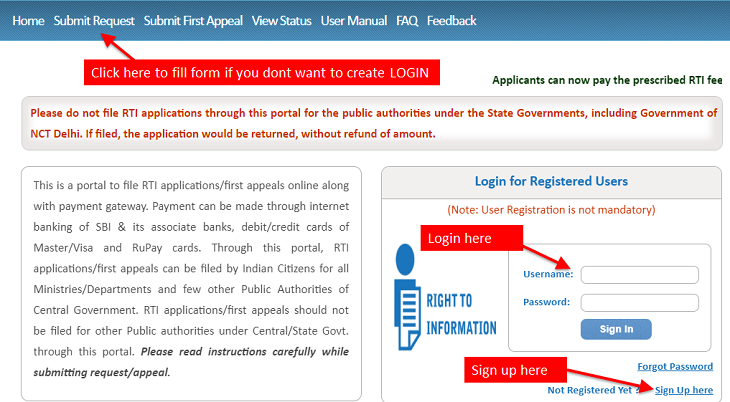

Step #1 – Create your free login or file RTI as a guest

If you do not want to create login then continue as a guest (by directly clicking to submit request button). To make it simpler I have attached the screenshot of the login page.

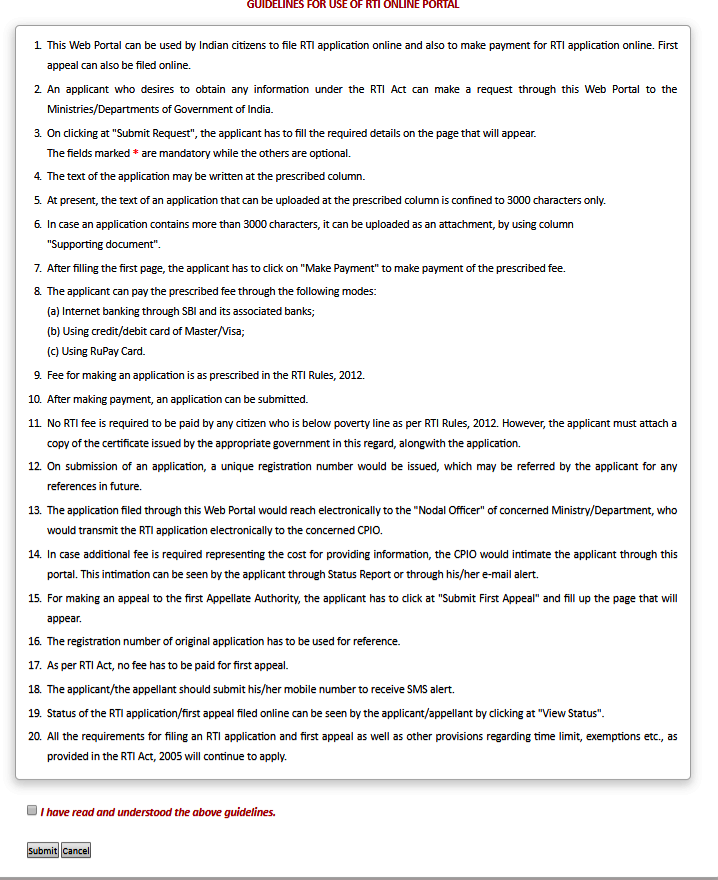

When we log in or even directly click on “submit request”, then the below image will appear and you just have to tick on “I have read and understood the guideline and click on submit button”. Below is a snapshot!

Step #2 – Fill the RTI form

The next step is to fill the main RTI form, you can access it directly by clicking here.

Filling an RTI form is a bit tricky. There are lots of things you should take care. There are dozens of govt departments and ministries which handle a different kind of work. So it’s important to know which department or ministry handles your RTI form.

Whatever is your complaint, it is important to write to the point and not hit around the bushes and also to write in bullet points because it will be very easy and eye-catching for the RTI OFFICER to understand your query and reply you even faster.

Let me make it easier for you by giving an example.

CASE STUDY – Mr. Shyam wants to file RTI for reasons for delay in roads repairs.

After the rainy season was over, Shyam noticed that the road was not at all in good shape. He also noticed that there were frequent accidents on that road and many people were losing their precious lives. He complained to the authorities, but no actions were taken and 3 months had already passed.

Shyam finally decided to file an RTI to know what is the reason behind so much delay.

If you are not sure which ministry you should choose while filing the RTI, then just Google search about it, and most probably you will find that information.

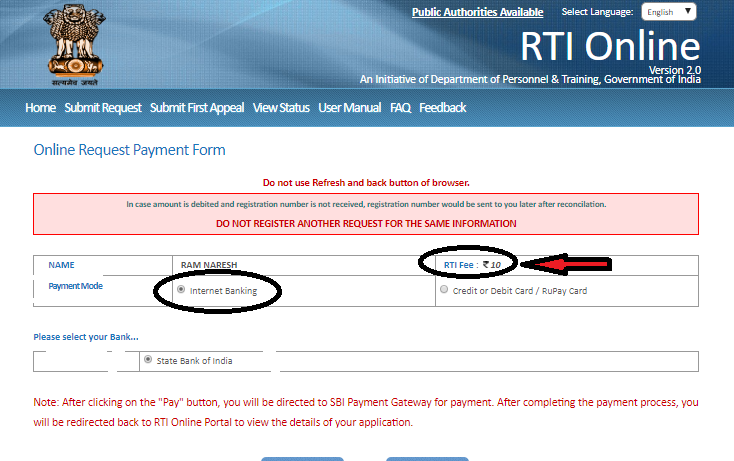

Step #3 – Make the fees payment

Once you click on submit, then the final step is to make the fees payment. The Fees for filing RTI is Rs 10 only. Two modes of payment are mentioned as

Internet Banking (only SBI bank option in there)

Credit or Debit Card / Rupay Card

Step #4 – Submit your application

The last and final step

Once you have made the payment click on to the submit your application. A unique registration number is generated. (please save it for future reference).

Now, wait and watch for a maximum of 30 days and you will mostly get a reply for your query.

If you have not received the reply or you are not satisfied with the answer from RTI department, then you can file the first appeal, which is free of cost for the first time. Learn more about first appeal here

You can’t File RTI to State Govt departments online

Note that the facility of filing online RTI is available only for central govt departments and ministries. You can’t file RTI for State govt departments through this online portal. For that, you should follow the offline process of RTI only.

I hope this article has taught you about filing RTI online and answered most of your basic queries. Please feel free to ask any questions in the comments section below.

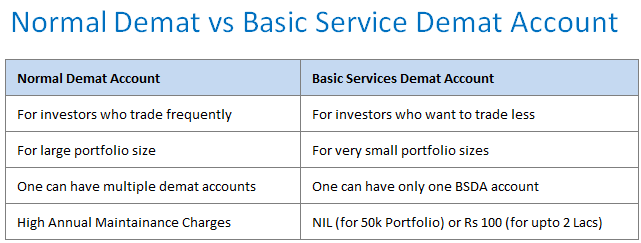

Do you hold a Demat account or planning to get one? Then you should know what is a Basic Service Demat Account because it can be helpful for you if you are planning to trade very less and want to save on yearly maintenance charges.

Basic Services Demat account as its name suggests is a basic version of a full-fledged Demat account that provides basic level services. It’s ideal for those whose portfolio size is quite small. We will look at the details in this article. But before that, do you know what is Demat account at the first place?

What is the Basic Services Demat Account?

Demat or Dematerialized Account means an electronic account that holds various financial securities (especially shares) in an electronic format securely. Demat account is a compulsory account for those who want to buy company stocks from the stock market.

Demat accounts are under the control of SEBI i.e. Security and Exchange Board of India. Now, from 27 August 2012, SEBI has brought a guideline that every Demat provider will have to provide “Basic Demat accounts” available to every beginner in the share market so that it can encourage the people to invest in trading. This will be helpful for achieving wide financial inclusion.

So all those investors, who want to trade less and have a portfolio size of small amounts can open a basic Services Demat Account (BSDA) and save on the annual maintenance charges.

Where to open a Demat account or BSDA account?

You can open your Demat account or BSDA at any bank like SBI, ICICI, HDFC, Kotak Mahindra and many other banks, or with a stock broking companies Angel broking, 5Paisa, Sherkhan, etc. directly. Opening both Demat Account and Basic Service Demat Account is free at both banks and broking companies, but again the AMC varies.

These banks and broking companies provide free services for the first year and from 2nd year onwards they may start to apply charges on the basis of transactions. So before applying for a BSDA or Demat account check for all the details on the website of that particular bank.

How are Basic Services Demat account different?

Basic services Demat Account is a Demat account which can be opened with any Demat Service provider of your choice when your holdings are expected to be below Rs.2,00,000/-.

If we are maintaining holdings of value less then Rs 50,000/- then no annual maintenance will be charged from our account. In case our holdings are between 50,000 to 2,00,000/- then the annual maintenance of Rs. 100 /- will be charged.

In case our holdings exceed 200000/- then our BSDA account will be converted into Regular Demat account. This initiative is to promote retail investment and to promote retail investors to hold securities in Demat form.

How is the value of holding determined?

The DP i.e. Depository Participants will keep calculating the daily closing prices of securities (stocks, mutual fundsetc.) to determine the portfolio size.

This will be calculated after every trading day and then it will be compared with the limits set for your BSDA account. The moment your portfolio value exceeds the limits, you will be charged the fees for the normal Demat account or the slab you fall into on a pro data basis.

Check the video below for more.

Services provided for Basic Service Demat account

Now you must be clear about normal Demat Account and BSDA. Generally, the Basic Service Demat Account provides all the major facilities covered in normal Demat Account. But other that those services, there are few services in BSDA which are a little bit different than normal Demat Account. These services are as given below:

1) Transaction statement:

When your BSDA account is active and balance is maintained then you will get the transaction statement of your account quarterly. But if you don’t have any transactions in a quarter and your no security balance then you will not get the transaction reports or statement.

The statements are available in two forms i.e. electronic and physical document or hard copy. Electronic statements are free of cost; you don’t need to pay any charges for that. But if you want the statement in hard copy then your first two statements will be provided for free of cost and for additional statements you will have to pay the charge which will not exceed Rs.25.

2) Annual holding statement:

One annual holding statement ho holding of the account is sent to the registered address of the account holder. These documents will be sent in physical or electronic form i.e. via e-mail as per the account holder’s choice.

3) SMS Alert:

The account holder should register his mobile number to get the facility of SMS alert. Here you will get SMS for every transaction in your account.

4) Delivery Instruction Slip (DIS):

Two delivery Instruction Slips will be provided to you for free at the time of opening the Basic Services Demat Account.

These are the services which are slightly different in the case of Basic Service Demat Account then normal Demat Account. If you want to read more details about the services and charges of BSDA then you can download the circular by SEBI.

Can I convert my current Demat account into BSDA?

Yes, if you feel you are not making much use of your Demat account or if your portfolio is of less size, you can contact your DP to get your Demat converted to basic services Demat account.

This Basic Services Demat Account is a kind of free account because you don’t need to pay any maintenance charge if your transactions are below Rs.50,000. And Rs.100 only if your transactions are between Rs.50,000 to rs.2,00,000.

I hope you get all the basic details about BSDA. Do let us know if you need more details about the Basic Service Demat Account…..

Do you get HRA as part your salary? If yes, then it’s critical for you to understand how the HRA exemption amount is calculated?

In this article, we will talk about things like what is HRA? How to calculate HRA? And various other things related to house rent allowance. You can check out the video below to quickly understand everything about HRA

What is HRA?

HRA i.e. House Rent Allowance is the amount paid as a part of salary by the employer to the employee. Employee can get tax benefit on this HRA amount if he is living in rented house and paying rent. This simply means that if your salary skip has HRA component, then you don’t have to pay income tax on this amount. However you can’t save income tax on the full amount.

There is a rule on how much HRA you can claim and save tax on it. In this article, we will look at the rules and calculations. But before we move ahead, here is one good news.

If an employee does get HRA as part his salary, but paying rent, even then he/she can claim some part of HRA for saving tax and there is separate calculation for that. We will also look at that today.

How to Calculate HRA amount?

Lets now see how the HRA is calculated, but the calculation depends whether you are getting salary component from your employer or not (it should be mentioned in your salary slip).

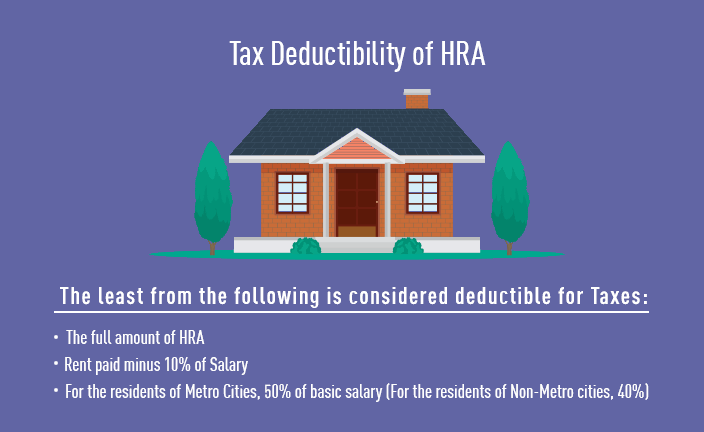

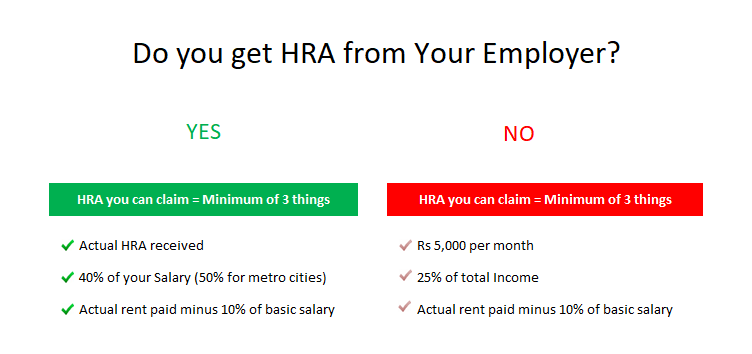

Case #1 – When you get HRA from employer

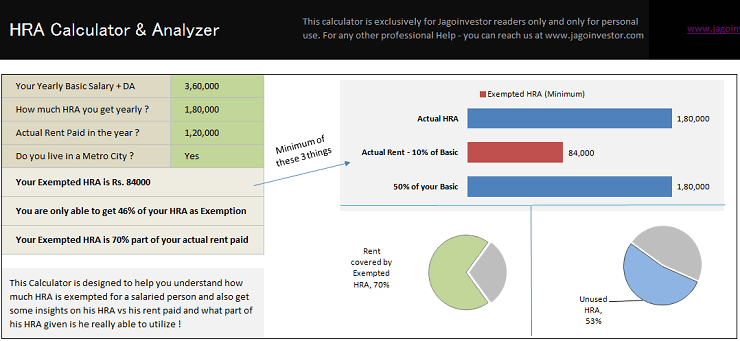

Actual HRA offered will be the lowest of the following 3 things:

Actual HRA received.

40% (in non-metro city) or 50% (in metro city) of your salary.

Actual paid rend is reduced from 10% of basic salary.

Let’s take an example of how HRA is calculated.

Example: An employee who lives in a metro city, has basic salary Rs.30,000 per month and the HRA part is Rs.15,000. The actual rent he pays is Rs.10000 per month. Then the exemption he will get is –

Actual HRA received = (15,000 x 12) = 1,80,000

Actual rent paid – 10% of basic salary = (10,000 x 12) – [(10/100) x (30,000 x 12)] = 84,000

50% of basic salary = (30,000 x 12) x 50/100 = 1,80,000

Now the lowest amount in above calculation is 84,000. So the employee will get exemption of Rs.84,000.

Case #2 – When you don’t get HRA from employer

If you are living in a rental house or paying for your accommodation and do not get HRA from your employer then also you are applicable for the tax deduction in income tax return. These people can also claim for HRA exemption under section 80(GG) of IT act.

Actual HRA offered will be the lowest of the following 3 provisions:

Rs.5000 per month

25% of your total income

Actual paid rend is reduced from 10% of basic salary.

Though there are some conditions which should be fulfilled if you want tax deduction in this case. The criteria are as bellow:

You should be salaried or self-employed and paying rent for accommodation.

You haven’t received any HRA in the financial year in which you are claiming for HRA exemption.

As per HUF our spouse or minor child should not own house registered on their name.

If you do not meet any of the above criteria then you can’t claim for HRA. Here is chart which explains the same thing which we talked above.Important points regarding HRA?

HRA is applicable only to the salaried person and not to those who are self-employed. If a person is living in his/her own house then also he/she can’t claim for HRA benefits.

If the employee living in a rented house is paying more than Rs.1 lac on rent in one financial year then he has to submit PAN details of landlord along with HRA claim.

If a person is living in his parents’ house and paying rent to them, he is applicable for HRA claim. However he cannot claim if he states that he is paying rent to his spouse or child.

Documents required for claiming HRA

The first thing you need to know is that you don’t need to submit anything to Income tax department to claim HRA. You only need to submit the documents to your employer and your employer will verify documents and give you the exemption and then issue form 16 and include these details in that form.

So basically at the start of the year, you need to update your employer on the rent you are paying each month and based on that data the employer will deduct the TDS from your salary. Finally at the end of the year, you will have to submit following documents

PAN card of landlord if the amount is above Rs.,1,00,000.

Some employers may ask for lease and license agreement

Also, In last few years, many tax payers were found submitting fake documents for HRA claim in many cases. This is the reason that IT department is asking for more and document while claiming for HRA exemption. If there is any scrutiny by income tax department, you might have to submit some more documents like

Electricity bills

Water supply bill

Agreement or a letter from housing society

Some cases when charges of IT department can make enquiry are

If a person has a house loan and also applying for HRA.

If a person living with parents without paying any rent but still apply for HRA and says that he pay rent.

Adding higher amount in receipt than he actually pays.

Download HRA Calculator

We have created a nice HRA calculator and analysis tool, which will help you to calculate your HRA and also help you know how much HRA are you not able to utilize and how much is it covering your rent paid.

If you look at the same example which is mentioned above in this article (salary = Rs 30,000 per month, HRA = Rs 15,000 per month, and Rent paid = Rs 10,000 per month, and living in metro) and if you do the HRA analysis , you will find out two things

He is only able to claim 46% of his HRA provided to him (84k our of 1,80,000)

He is able to cover 70% part of his rent paid through HRA (84k out of 1,20,000)

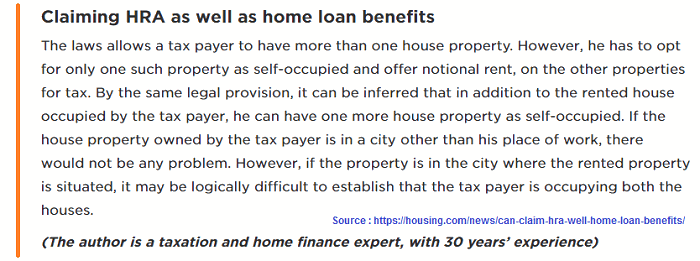

Can you claim both HRA & deduction on home loan interest?

If you have bought a house in a different city and you are doing job in different city, then in that case, you can claim HRA benefits as well as home loan interest too. However if you have the house in the same city of your job, you cannot claim the HRA benefits.

Housing.com has explained it in a nice way.

Are you claiming HRA tax benefits? Do you follow any other process which is not part of this article? Can you share some more HRA related tricks which you have learned over part few years?

Most of the people who want to do tax saving in 80C are confused if they should invest in PPF or ELSS (tax saving mutual funds). Both PPF and ELSS offer taxation benefits of up to Rs 1.5 lacs under sec 80C.

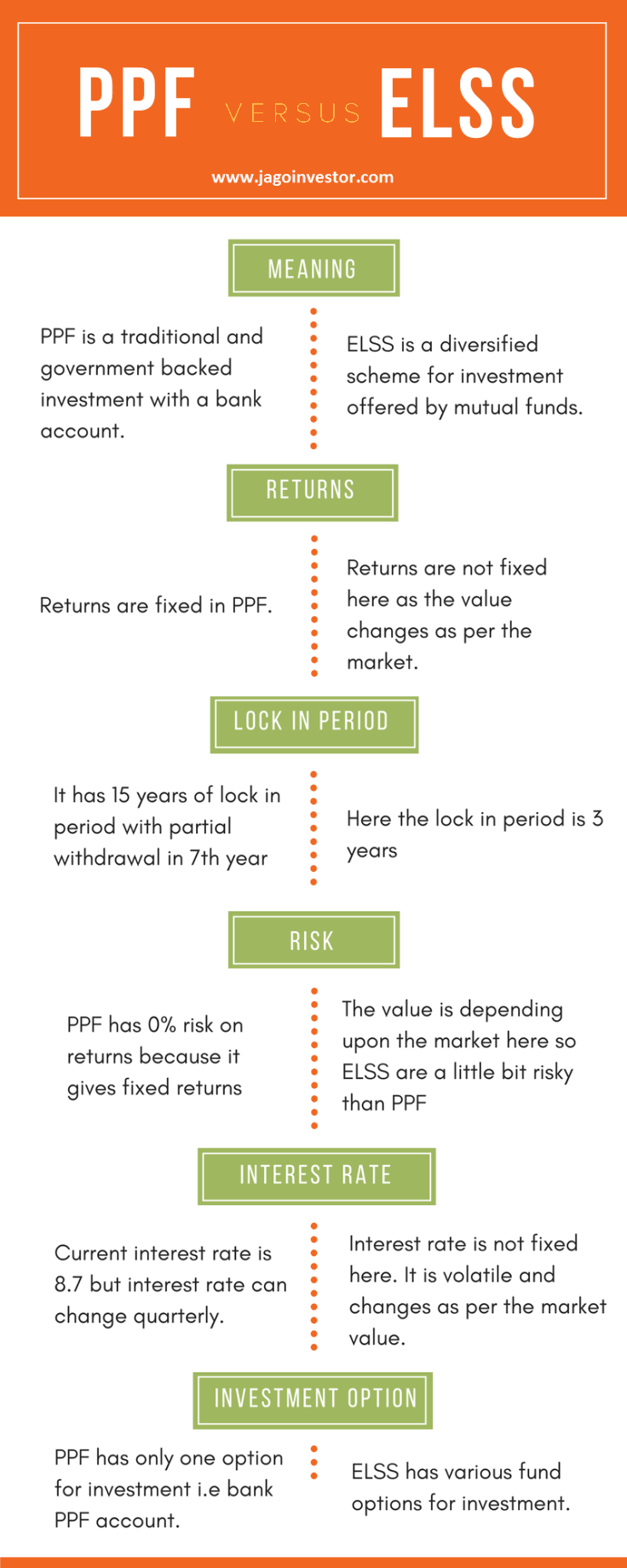

ELSS vs PPF – Meaning

Let’s start with their meaning and what exactly they are.

PPF means public provident fund. Its a govt scheme which is run by the post office and its a very safe financial product. There is no risk to it because it’s guaranteed by the govt of India. Its quite famous among investors for its safety and assured returns.

On the other hand ELSS (Equity linked saving scheme) is fairly new financial product in India (from last 15 yrs). It’s mainly an equity mutual fund that gives you an income tax benefit. Equity mutual funds mainly invest in stocks of companies, which makes sure that they deliver high returns, but at the same time they are risky (actually volatile) and their returns keep going up and down.

Now, let’s compare PPF and ELSS on various parameters.

#1 – Returns

The returns in PPF change every year and it’s around 7.5-8 %. Right now its 7.8% and it keeps on changing from time to time which is notified by govt. Earlier many years back, PPF returns were in a range of 12% and then it came down to 9%. But from the last few years, it’s hovering around 8%.

In the case of ELSS, it’s linked to the market and the returns are not fixed in the short term. Some years it can be 20 %, some times it can be 50% and in some years it can be -25% also. So you can see that the returns are totally dependent on stock markets and how well they perform. However, in the long term, you can be assured that you will get a return in the range of 12-18%. The returns are not at all guaranteed by anyone.

#2 – Lock-in Period

Your PPF investments are locked in for 15 yrs, but some partial money can be withdrawn after 7 yrs. So basically its a very long term product, and if you are investing in PPF, you should be ready to lock you money for a very long time. After 15 yrs, you can again extend your PPF for another 5 yrs (any number of times) and your money will again be locked for that 5 yrs.

On the other hand, ELSS has a lock-in for just 3 yrs. You can take out your money after 3 yrs. The important point to note here is that each investment is locked in for 3 yrs, so if you have a SIP running in an ELSS fund, then each installment is locked for 36 months.

So if you want money in 4-5 yrs, ELSS is a better choice compared to PPF from a liquidity point of view.

#3 – RISK

PPF is not at all risky because its value does not go down. PPF is also guaranteed by govt, so there are no changes in fraud. If you plot the graph of your PPF value, you will see a straight line going up. However, note that PPF has a totally different kind of risk, which is that it does not give inflation-adjusted positive returns. This means that its returns match the inflation and in the end, you do not have any net returns.

On the other hand, ELSS is volatile, which is often referred to as “RISK” . The value of ELSSS keeps going up and down depending on the stock market movements. In the short term, you might experience a downturn and loss in value, but over the longer-term, you will see good results.

As most of the investors are risk-averse and do not like to see a dip in the value of their investments, most of the investors stay away from ELSS or stocks in general and lose the chance to experience great returns at the same time.

#4 – Taxation

PPF is tax-free. There is no tax on PPF returns. Whatever returns you get in PPF is 100% tax-exempt.

Earlier ELSS was also tax-exempt after 1 yr, but with budget 2017-2018, now any gains in equity mutual funds or stocks are taxable @10% when you sell them, but you get an exemption of Rs 1 lac per yr. This means that if your profit after selling ELSS is 4 lacs, then you have to pay a 10% tax on 3 lacs. However, even after this taxation, the post-tax returns of ELSS are much better than any other investment option.

Here is an infographic that shows you a quick comparison between PPF and ELSS.

How to invest in PPF or ELSS?

If you want to invest in the PPF account, you can open a PPF account in a post office or any bank (generally SBI is very famous for PPF). Note that it does not matter where you are opening your PPF account, if you open with the post office, SBI, or ICICI .. at all the places you are going to get the same interest because ultimately it’s controlled by POST OFFICE only.

The banks are just a medium to invest and nothing else.

If you want to invest in ELSS, then you can choose any fund house (there are many AMC like ICICI, HDFC, SBI, Motilal Oswal etc). You can either go to their website directly or contact an advisor (You can also invest in ELSS through Jagoinvestor help)

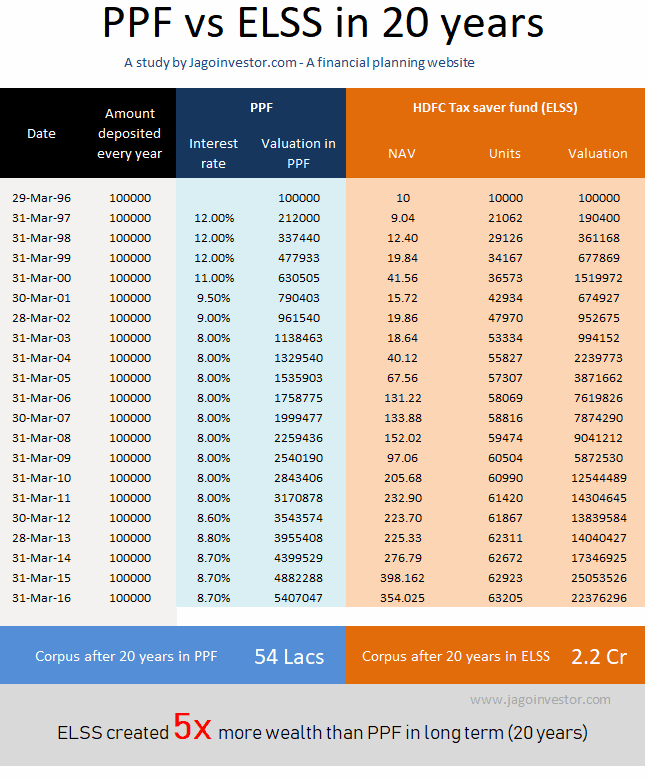

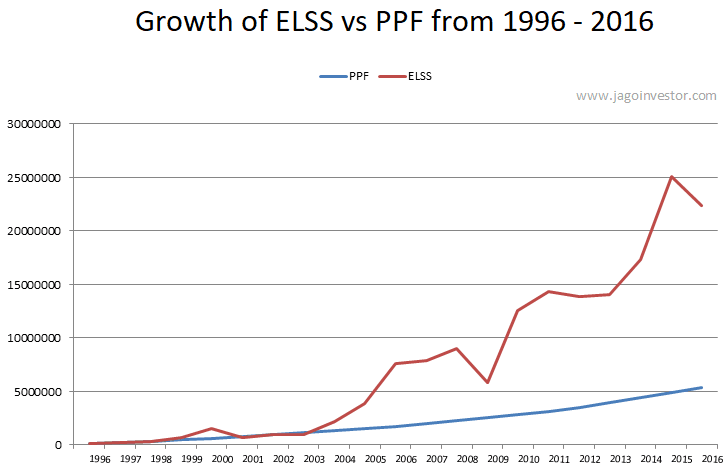

Returns of ELSS and PPF from the last 20 years

It’s important to check how PPF and ELSS have performed in the last 20 yrs (1996 – 2016) so that you get a fair idea on their performance and which one is better from a long term point of view. So we took one of the famous ELSS (HDFC Tax Saver) as an example along with PPF and calculated how the value in both will increase over time if someone invests Rs 1 lac in both the financial product.

In the above table, you can see that Rs 1 lac of yearly investment for 20 yrs have accumulated to Rs 54 lacs in PPF, whereas it becomes 2.2 crores in the ELSS, which means that ELSS gave 5 times more returns than PPF.

However, this difference is more visible only after 10 yrs passed and compounding starts kicking in.

In the initial years, there was no big difference in their values. See the graph given below. You will get a clear idea of how ELSS has performed incredibly towards the end of tenure.

Important Note :

The example of HDFC Tax Saver is taken only for the illustration purpose. This is not a recommendation, and right now HDFC Tax saver is not the best option for tax saving. There are many other ELSS funds which can be chosen other than HDFC Tax saver. Kindly contact your Financial Advisor for any recommendations.

So after studying the table data and graph, I hope it becomes easier for you to know the difference between the returns from PPF and ELSS investments. If you still have any confusion or any doubt in your mind, feel free to ask us by leaving your query in our comment section.

There are many investors who have very low or zero tax liability and therefore they skip filing their income tax return. Then, there are investors who do not file their returns for years and only when something urgent comes up which requires their last few years of ITR, they go to a CA and file their old tax returns.

Today, I will share with you why you should file your income tax return, even if you have income below the taxable limit.

Before that, let me share with you what exactly is ITR, for those who are not aware of it.

What is Income Tax Return (ITR) and who should file it?

An Income Tax Return is a form, where a taxpayer discloses details of his/her income, claims applicable deductions and exemptions and taxes that are payable on the taxable income.

As a responsible citizen of India, everyone who has an income should file an ITR, because in this way we are actually declaring all sources of income whether taxable or non-taxable.

The Income Tax Department mandates everyone to file an income tax return if one’s gross total income (before allowing deductions under section 80C to 80U) exceeds Rs. 250,000 in a financial year.

One can also file it even their income is below the taxable limit or its zero (in which case it’s called NIL return). Filing Nil return will act as proof of accumulated funds in your bank accounts or other investments.

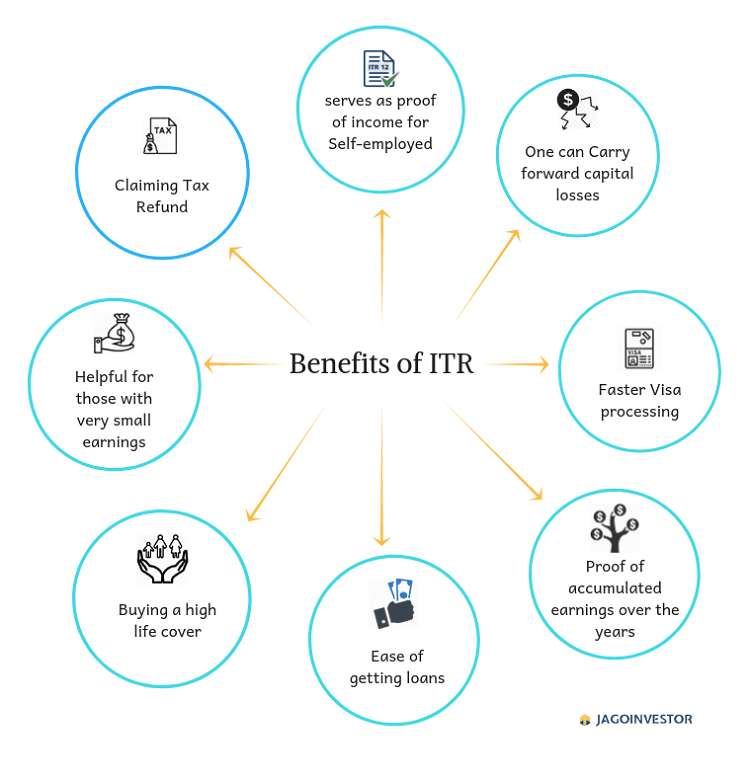

There are various benefits if one files ITR irrespective of their income. Below I have listed a few benefits of filing ITR.

Benefit #1 – Proof of accumulated earnings over the years

It might happen that a person is earning some small income over the years which is below the taxable limit and over the years they accumulate good corpus. Now it may happen that they might get tax scrutiny for some reason after a few years.

If someone has not filed the ITR over the years, it will be a lengthy and tiresome process to explain the sources of earnings over the years. However, with ITR, it will be legal proof of income earned in each year.

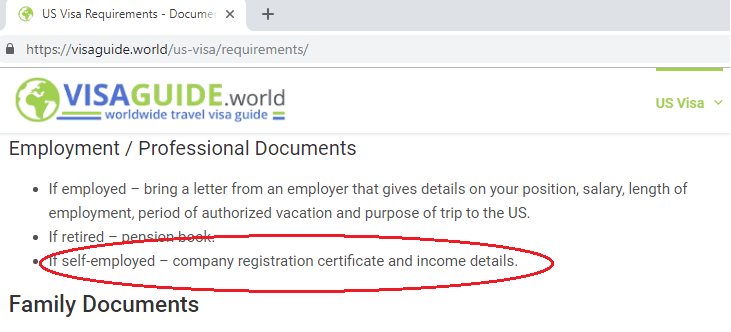

Benefit #2 – VISA processing

If you are traveling overseas or planning to travel in the near future, proof of earning is required. If you are salaried than the employer certificate will work but if you are self-employed than income details are needed to be submitted. So, ITR return will work as income-earning proof.

Benefit #3 – ITR serves as proof of income for Self-employed

Being self-employed does not provide earning proofs such as salary certificate from the employer and form 16. So, having ITR ready with you as proof of income is the most convenient proof.

Benefit #4 – One can Carry forward capital losses

If you have incurred capital losses, the Income Tax Act allows you to carry forward losses for eight consecutive years, and balance it against future gains and income.

To keep a track of your losses, the Income Tax Department has laid out that, Losses for a year cannot be carried forward unless that year’s return has been filed before the due date. So, even if it’s a loss return, you do not have any income to show – do file your return before the due date to declare the capital loss incurred.

Benefit #5 – Helpful for those with very small earnings

There are many people who get some small incomes such as

Tax-free incomes like Agricultural Income, tax-free bonds, etc.

These people total income might be below the taxable limit and they might feel that they are not supposed to file any tax returns, as they don’t have to pay any tax (because TDS is already deducted). But by filing ITR they will get legal proof of income (in case they need it).

Benefit #6 – Claiming Tax Refund

If you have paid excess tax on your income, then you can file for a refund from the income tax department. In order to get this refund, it is mandatory that you file ITR.

Getting a refund of your taxes feels like getting a paycheck credited. Many salaried people don’t file their ITR as they feel that the tax on their income has already been deducted and they have form 16. But, it might happen that, the employer has paid more tax on your behalf, not taking into consideration your actual house rent, tax-saving investments or insurances. So, in that case, filing of ITR will lead you to ask for a refund from the IT department.

Benefit #7 – Ease of getting loans

If you apply for any loans such as a home loan, car loan, etc., then ITR for the last 2-3 yrs is asked as the mandatory documents. ITR will help your lender to assess your repayment capacity and is an important document. A lot of people who have not filed ITR on time rush at the last minute for these documents, so why not better file it on time?

Benefit #8 – Buying a high life cover

When you buy higher life insurance cover the Insurance company asks for proof of income to assess the cover amount to be provided to you. For this salary slip, bank statements or ITR of the last 3 consecutive assessment years are required.

It might happen that you don’t get a salary receipt or your monthly income is being paid from different groups so bank statements will also not work as strong proof. So, better to have an ITR return filed.

Do you know someone who should file ITR in your circle/family?

I hope the above points will make you understand why it is always preferable to file ITR, even if it might be NIL return. In a lot of families, there are people whose name there are small incomes like dividend income, income from tuition fees, small business income and this article applies.

So make sure you start filing an ITR for them and save yourselves from the future hassles involved.

Do share your views, experiences and ask queries through comments.

Category 1– Those who invest their money manually at the end of each month

Category 2 – Those who auto-invest at the start of each month.

Today we will discuss which option is better than others and what are the benefits of choosing the auto investment mode at the start of the month

While investing at the end of the month manually is very intuitive and sounds comfortable to most of the investors, we think that investing in the auto mode at the start of the month is much better and beneficial for an average investor.

Most people adopt the “Save whatever money is left at the end of the month” approach in their financial life, but there is enough research and proof that it does not work for the larger masses. The best option is to put your investments in auto mode and let it happen automatically each month.

Now let’s looks at the benefits of investing in auto mode at the starting of each month

Benefit #1 – You can manage your lack of discipline

Can you trust yourself in investing each month manually for the next 5-10 yrs?

If you decide to invest Rs 10,000 on the 25th of every month for the next 10 yrs, will you be able to do it consistently for the next 120 months (10 yrs X 12 months)?

Trust me, it’s a lot of work and very hard to act in a robotic fashion.

Sometimes, you will postpone it

Sometimes, you will feel – “Let’s do it next week”

Sometimes, you will skip it for the sake of other expenses

Sometimes, you will just be involved in some other tasks

Sometimes, you will actually follow it

And most of the times, you will just forget it

Compare this will an auto mode, where you have set up your SIP (automatic monthly deduction in mutual funds) or a recurring deposit (for those who don’t think mutual funds are their cup of tea), and the money automatically gets deducted from your bank account (considering you have the balance) and then gets invested without your intervention.

Which one of these options do you feel will be in your interest?

Most people think that each month of a certain date they will invest some X amount on a regular basis, but they are not able to do it on a consistent basis. They either lack in discipline or they are so consumed in other areas of life, that they are not able to follow what they promised themselves.

Due to this, their financial life suffers. The money does not get transferred from the bank to the investments and eventually gets spent.

Trust me, even if you are the KING of indiscipline, the auto investing will create wealth for you!

Benefit #2 – You avoid unwanted expenses

“Supply creates its own demand” – a classic principle of economics. If you have money lying available in your bank account, you will find enough reasons for spending that money.

Hence, if you think – “Let me first spend, if anything is left, I can always save/invest it at the end of the month” , it’s almost guaranteed that you will not find any money at the end (unless your income is very high compared to your expenses)

This is the reason why you should create a structure that takes away some part of your salary from your savings bank account to somewhere else which is not easily visible to you (like PPF, RD, or mutual funds).

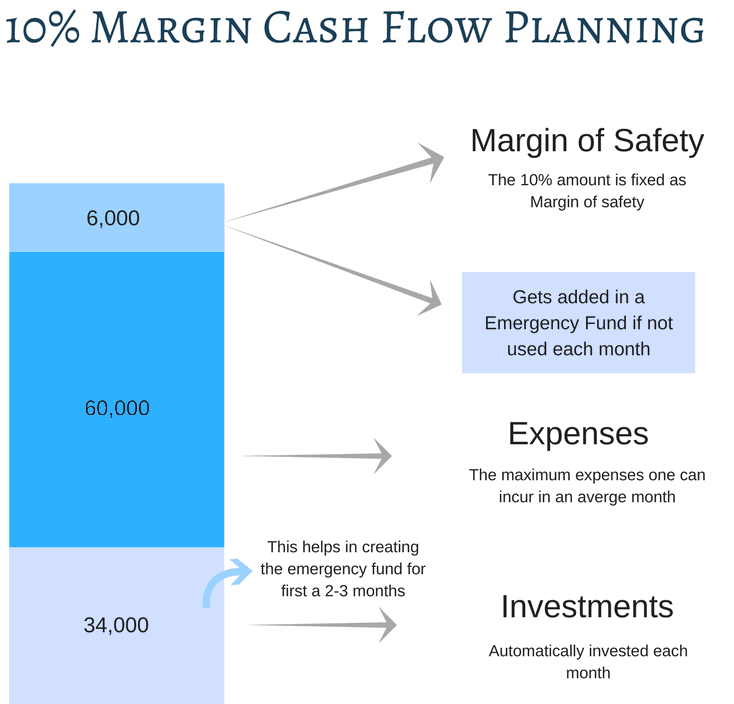

I have devised something called a “10% margin system”, which can truly transform the way you manage your cash flow. It’s one trick that will help you save more money each month.

Under this system, you only keep your monthly expenses + 10% more in your bank account and invest everything else at the start of each month. Click here to read more on this 10% margin system.

So if you invest at the start of this month, you will shop only limited to your needs, you will not overeat outside, and to a great extent, you save on the unwanted expenses.

The whole idea is to “cut” the excess supply of money to yourself by investing it at the start of the month itself.

[su_button size=”6″ radius=”square” background=”#306bf1″ url=”https://www.jagoinvestor.com/mutual-funds#account”]Start your FREE Mutual Funds Account with Jagoinvestor[/su_button]

Benefit #3 – It develops the Habit of Saving

One of the biggest challenges for new investors is to develop the “habit of saving” in them.

The world these days is such that it’s very easy to SPEND money on things you don’t really need. You spend on mobiles, gadgets, parties, traveling and consuming various things (nothing wrong in these things). However, beyond a point, you start crossing the limits and you start “wasting” money at the cost of the future.

Most of the investors find themselves not saving any money and living paycheck to paycheck for the simple reason that they never develop the saving habit and eventually end up in the never-ending cycle of earn -> spend -> earn -> spend

You should check this excellent simple video by Brain Tracy on why you should save at least 10% of your salary if you are a beginner investor.

Some time back, I had written an article for beginner investors and how they should manage their financial life. Please go through it.

If a person sets up the auto investing at the start of the month, then at some level the habit of saving starts. If one is able to continue that for a few months, the overall expenses will get adjusted with the leftover money in the bank account. If you are a new investor, the primary reason to start your SIP or RD is not to save money, but to develop the habit of saving.

Benefit #4 – You reduce the risk of investments

If you do not spread your investments across months, then there are good chances that if the markets fall suddenly, its impact will be high on your wealth. In the same way, the upside potential is also high. But let’s focus on the risk part here.

If your investments are happening each month on a regular basis, then your investments are spread over all kind of markets like bull and bear market (assuming your investments are happening in mutual funds SIP)

So if you want to control the risk part, it’s a good idea to let your investments happen on a monthly basis and not a one-time basis. A good example of this is SIP in ELSS vs. One time investment in ELSS for 80C.

For example, consider two friends Ramesh and Dinesh

Case 1: Ramesh invests Rs 1.5 lacs in one go for tax saving during the month of Feb, but the markets in next one year go up and down and eventually go down by 10% . In this case, the investment done will be having high risk, because all money was invested in one go (which also means that potential returns can also be high if markets do well) and all the ups and downs impact will be on the total money.

Case 2 :However, Dinesh does a SIP of Rs 12,500 per month in ELSS, and in 12 months he invests total of Rs 1.5 lacs. In this approach, the investments are spread over 12 different months and risk (and returns) will be more controlled. If markets go down in the first few months, then it’s only for the amount invested before that event.

Benefit #5 – Guilt-free Spending

This is one benefit that is often not appreciated enough.

When you save your money at the start of the month, then the rest of the money is available for your expenses. Now you can spend it freely, without any guilt.

Most of the people who do not save enough or save at the end of the month, keep worrying and thinking while spending their money. They keep feeling “Bahut Kharcha ho Gaya is Baar” while going for outings or movies etc. This is because they have not allocated money for the future.

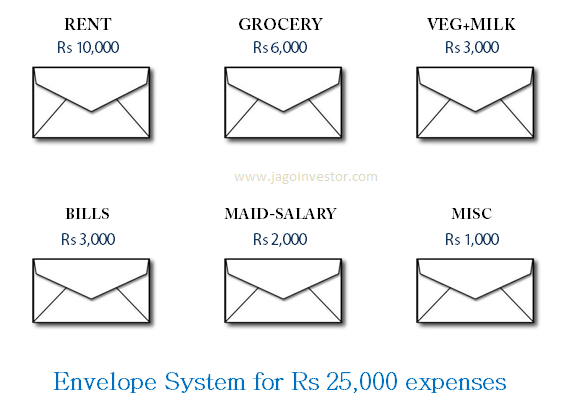

So you should start your auto investing (SIP is one of the best way of doing that) and once you have done that, I suggest you adopt the envelope style of expenses where you create few envelopes for each expenses category and put the cash in the envelope and use only that till the end of the month.

However once you setup your automatic investments at the start of the month, you then just have one agenda – “Spend rest of the money” guilt-free.

Are you starting your investments in Auto mode Now?

So what are you waiting for?

If you have not yet started your investments in auto debit mode, you should immediately start your investments. You can either start your SIP with our team or reach out to your trusted advisor who can guide you on this.

[su_button size=”6″ radius=”square” background=”#D8180A” url=”https://www.jagoinvestor.com/mutual-funds#account”]Start your FREE Mutual Funds Account with Jagoinvestor[/su_button]

For Long, the real estate sector was unregulated and in favor of builders and developers. From getting delayed possession to bearing a huge loss of project cancellation, all has to be borne by home buyers.

Even in worse case after living in a society for a long period of 10-15 years, homeowners need to vacant the society due to builder’s mistake of not getting approval from government for the said project.

And after all these, for any of these malpractices, if a home buyer files a complaint, it use to take years to get a verdict. However, now to bring transparency and accountability to this sector, Real Estate Regulatory Act, 2016 has come to force.

This aims to create a more equitable and fair transaction between sellers and buyers of properties. The Real Estate (Regulation and Development) Act is expected to ensure consumers will not be cheated or taken for a ride by the developers.

So, we will see in 14 points that how RERA will benefit us. But, before that let’s see all loopholes and malpractices builders and agents use to do in the real estate sector.

Delay in project completion

Use to cheat buyers with false information

Divert funds to another project or for other purpose

Get-away with sub-quality construction

Offer special pre-booking rates

Keeping Date of possession clause in agreement empty

Altering the project developments without consent

14 RERA rules investors should know

1. Registering project with RERA :

RERA makes it mandatory for all commercial and residential real estate projects where the land is over 500 square meters, or eight apartments, to register with the Real Estate Regulatory Authority (RERA) for launching a project, in order to provide greater transparency in project-marketing and execution.

The builders or developers have to publish all the details such as sanctioned plan, layouts, the location of the project with clear demarcation of land, carpet area, number and area of garage, etc. So, with RERA builder have to get all the clearance before they could advertise or sell any property, it will help in malpractices to be curbed.

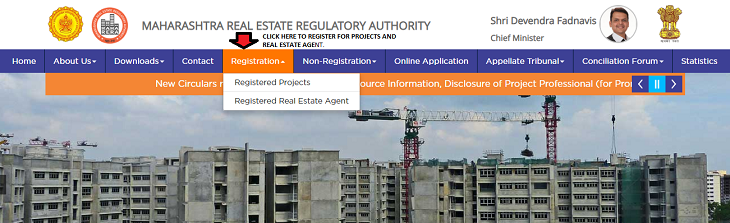

Hence, before entering into the contract, you can check online on the website of RERA about every detail of the project by visit the RERA site of the concerned state and go into the registration tab. I have attached a screenshot of RERA Maharashtra. To get an idea about how RERA MAHARASHTRA REGISTRATION site looks like.

If you are offered to buy a property of any unregistered project then you can notify the same to RERA to save others from any kind of fraud.

2. Quarterly updates on Construction progress :

Now builders/developers have to upload project details including number and types of units sold out, government approval taken or approval pending list & completion scheduled every three months. Along with that if there is any litigation going on related to that property then all the documents of proceedings have to be uploaded by builder/developer. Hence now you can check online the progress of the project they are putting their money in.

3. Escrow Account:

The developer will have to transfer 70 percent of the money received from customers to an escrow account. This will ensure the builder does not spend the money on other projects since they can withdraw money from this account after approvals from engineers and chartered accountants they appoint and your money will be used only for the project you invested.

4. Sale agreement standardization –

Earlier sale agreement use to be in such format that the home buyers were penalized on any default but similar defaults by promoters would not attract any penalty. But, now as per RERA norms, a standard model sale agreement has to be entered between promoters and homebuyers to ensure equality and protect buyers from various penalties and charges.

The agreement of sale shall specify particular details of the project including the construction of buildings and apartments, along with specifications, internal development works and external development works, the date on which the possession of the apartment, plot or building is to be handed over, etc.

5. Maximum 10% of cost of project as advance payment :

The promoter can not accept a sum of more than 10% of the cost of project, plot, etc.. as an advance payment or an application fee from you without first entering into a written agreement for sale with such person and register it.

6. Five years of defect liability period :

Under RERA, in case of any structural defect or poor quality, it will be the responsibility of the developer to rectify such defects for a period of five years. So, if any defect is found in the quality used in the construction of property then you can make the developer/builder liable for all sub-quality issues and ask for repairing or compensating the same.

You can also watch the video on RERA –

7. Carpet Area :

The area of a property is often calculated in three different ways – carpet area, built-up area, and super built-up area. Hence, when it comes to buying a property, this can leads to a lot of disconnect between what home buyer pays and what he actually gets.

But, now it is mandatory for the developers to disclose the size of their apartments, on the basis of carpet area (i.e., the area within four walls). This includes usable spaces, like the kitchen and toilets.

8. Title Representation :

Promoters are required to disclose clear title over the property and project. If any defect is found in title of property then you can ask for the compensation and there is no limit for the amount of this compensation.

9. False information to home buyers :

If you made an advance payment for a project on the basis of any false information given to you via prospectus or in advertisement then you have the right to ask for a refund of your money. And if you want to continue with the project then the builder has to pay penalty and that can go up to 5% of the cost of property.

10. Failure to complete possession on time :

If the promoter fails to complete or is unable to give possession on time then, the promoter is liable to pay the entire amount given by you if you wish to leave the agreement. But, if you wish to stay in the agreement then the promoter will have to pay interest for every month of the delay till you receive the possession.

11. Approval for alteration in sanctioned plans :

If a builder wants to make alteration in plans and specifications of your individual flat then he can do that only with the approval of you. And if a builder wants to make alteration in the entire project’s layout & common areas of society then he needs approval of the 2/3rd number of total buyers.

12. Obligations of the promoter in case of transfer of real estate project to a 3rd party :

The promoter will not be allowed to transfer the majority rights and liabilities in respect of a real estate project to a 3rd party without the prior written consent from two-third allottees (buyers), except the promoter, and without the prior written approval of the RERA authority.

13. Agent registration is mandatory :

Now, every real estate agent has to register himself under RERA before selling or advertising any property and he has to abide by all rules of regulation like, maintaining books & records, not be involved in unfair trade practices or make any false statement oral or written.

14. Grievance Redressal: :

If any buyer, promoter or agent has any complaints with respect to the project, they can file a complaint with RERA. State real state regulatory department will try to resolve the dispute within 60 days. If you aren’t satisfied with RERA’s decision, a complaint can also be filed with the Appellate Tribunal within the next 60 days. Even after that if he is not pleased the complaint can be filled to high court and supreme court.

Benefits of RERA act 2016 :

This act is not benefiting only buyers but also agents and builders. RERA infuses credibility by making the sector mature & transparent and helping to Channelize investment into the sector. It will increase the confidence of financial institutions & foreign investors in the real estate sector.

Offense-wise penalties for developers :

The following are the penalties and compensation that can be levied on promoters.

[su_table responsive=”yes”]

For non-registration of a project

Penalty of up to 10% of the estimated cost of the project.

For violation of other provisions of the Act

Penalty of up to 5% of the estimated cost of the project.

For non-compliance of the orders of the Authority

Penalty for every day of default, which may cumulatively extend up to 5% of the estimated cost of the project.

For non-compliance of the orders of the Appellate Tribunal

Penalty for every day of default, which may cumulatively extend up to 10% of the estimated cost of the project or with imprisonment for a term which may extend up to three years or both.

[/su_table]

Offense-wise penalties for Real Estate Agent :

The following are the penalties and compensation that can be levied on the real estate agent.

[su_table responsive=”yes”]

For non-registration under project, he is selling

Rs. 10,000 per day of defaults which may extend up to 5% of the cost of the property.

For contravention of the orders or direction of the RERA

Penalty on a daily basis which may cumulatively extend up to 5% of the estimated cost of the property whose sale or purchase was facilitated.

For contravention of the orders or direction of appellate tribunal

Imprisonment up to 1 year with or without fine which may extend up to 10% of the estimated cost of project or both.

[/su_table]

Offense-wise penalties for Allottees(Homebuyers) of RERA registered project:

The following are the penalties and compensation that can be levied on allottees.

[su_table responsive=”yes”]

Contravention of any order of the RERA

Penalty for the period during which defaults continues which may cumulatively extend up to 5% of the apartment or building cost.

Contravention of the orders or direction of appellate tribunal

Imprisonment up to 1 year with or without fine for every day during which such defaults continues, which may cumulatively extend up to 5% of the apartments or building cost or both.

[/su_table]

*Apartment means block, chamber, dwelling unit, flat, office, showroom, shop, warehouse, premises, etc.

How to file a complaint :

After the implementation of RERA, we are optimistic that the new law will protect our interest. However, the most important question is, how to file a complaint or a case, under the new RERA rules.

So, for this, every state has described specific forms and procedures which are to be followed. The application can also be filed online, as per the format available. For filing a complaint, the complainant has to provide following details-

Particulars of the applicant and the respondent

Registration number and address of the project

A concise statement of facts and grounds of claim

The form has to be filled and submitted with Real Estate Regulatory Authority or the adjudicating officer.

Conclusion:

RERA is a huge step forward against thief developers. Till now, there wasn’t any regulator and neither were the rules in place. Delay in delivery of projects, bad material used for construction, changing of sanctioned plans every now and then was the major reason why RERA ACT,2016 came into existence.

However, even after RERA, there are many loopholes in this sector. For eg. It might happen that you wrongly signed some document which gives consent to any changes in agreement or project. Because RERA is just a mechanism which is in place to serve justice to all the parties. So, it is always your responsibility to be alert and get into any contract after due diligence.

I hope this article has helped you in understating RERA act 2016. Feel free to ask any doubts in the comment section.

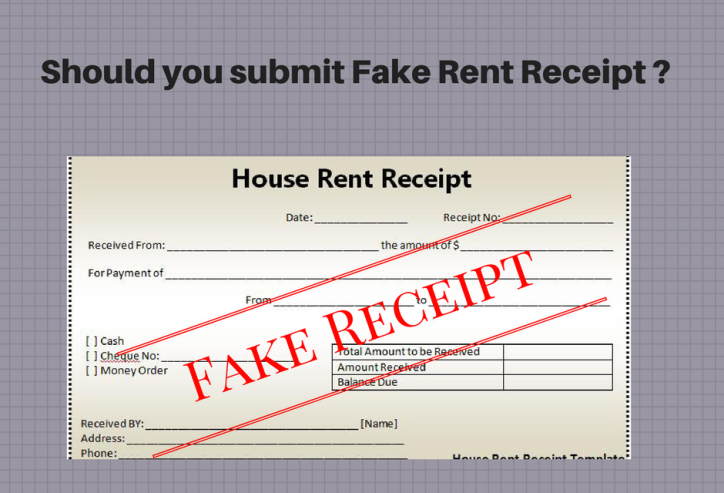

If you are living in a rented house and using any fake documents for HRA claim then be careful.

Because from now on there will be a big trouble for those who are using fake rent receipts to claim HRA, as Income tax department have started asking for more document.

Many times it is seen that people claim for HRA by submitting fake rent receipts. This also helps to get them tax benefit. But now as there is increase in the number of fraud HRA claims, IT department has started to ask for some other legal proofs.

Documents which IT department can ask in case of verification

Before you know about the documents needed for verification purpose, lets understand what is HRA (for those who are new to this)

HRA i.e. House Rent Allowance is an amount or we can say a part of salary of an employee which an employer pays if the employee lives in a rented house. It is beneficial for the employee as it lowers the tax which he/she pays on accommodation per year.

If you claim for HRA exemption then you need to submit some legal documents like a receipt or an agreement and ID proof of landlord. You can also claim for HRA exemption on your income tax by filling 12BB Form

If the IT department suspects that a person is providing fake receipts for HRA then they can ask for some other related documents. The list of documents which IT department can ask is as follows –

5 documents which IT department can ask in case of verification

Copy of leave and license agreement

Electricity bills

Water supply bill

Agreement or a letter from housing society

PAN card of landlord if the amount is above Rs.,1,00,000.

Is there any risk in submitting fake rent receipts to claim HRA?

People are asking various question related to fake rent receipt. You can see the snapshot given below…

The verification process is going to be more strict day by day so there is a risk in claiming for HRA exemption by providing any kind of fake documents. If a person wants to apply for HRA with fake receipt by knowing all the risks he has to prepare all the fake documents and as we know submitting each and every document fake is not that much easy.

In many cases employees asks their parents or relatives to sign the documents for HRA claim or sometimes employees shows the higher amount on their rent receipt than they actually pay so that they can get the exemption. In case IT department suspects your case as fraud, in that case you will have to go through verification

Some example where enquiry can happen

If a person has a house loan and also applying for HRA.

If a person living with parents without paying any rent but still apply for HRA and says that he pay rent.

Adding higher amount in receipt than he actually pays.

To know about this in detail you can watch this video..

IT department has stared cross checking the address on ITR ( Income Tax Return) form and the receipt submitted. They are also checking the records so that they can know who is the legal owner of the house to verify the Leave license agreement.

What are your thoughts on this issue? Do you know anyone who is submitting fake rent receipts?

This article is a guest post by one of our readers Vikram Agarwal, who wanted to share his experience on the concept of “Early Retirement”. Vikram was generous enough to share his story and some of the real-life things which will make you think hard about this concept. Like Vikram, if you feel you can write on jagoinvestor, please click here

Over to Vikram.

—

Most of my friends in my friend circle in late 30’s ask me one question – “How much money I should have now, so that I don’t have to work anymore while maintaining a decent standard throughout of my life, with all the future expenses taken in to account?”

They want to ‘Retire Early’

In fact, I also used to be an ardent follower of the concept of ‘Early Retirement’ but now have realized that the concept is more like a mirage, which does not exist in reality and once you reach there, it vanishes.

Moreover – in my view, it is quite dangerous for an individual to run after this concept. In my opinion, you achieve retirement either ‘NOW’ or ‘NEVER’ irrespective of your current level of income or financial state.

Early Retirement is a state of mind

It is a state of mind, rather than a stage achieved. The moment you achieve early retirement as per the physical criteria set by you five years ago taking inflation, life expectancy and all major and minor expenses in your monthly calculations, by the time you achieve retirement as per your old financial definition, all those things become sub-normal or default.

Your mind will have another definition that looks normal for you in today’s context for example for future kids’ education, your house quality, the type of car you own, facilities you desire and all other such expenses.

My personal example

For example, five years before, owing a 2 BHK house in the newly developed area with Marti Dzire hatchback car and with the kids going in a decent school used to be a life I wished for and I had done calculation for the amount required to maintain the same standard throughout rest of my life without working.

And that was ‘Early Retirement’ according to me and as per standard definition.

But, now it seems owing a 3BHK house (one extra room for parents or for guests) in a good location of a metro city, a nice Honda sedan and a ‘good’ school for kids throughout their education duration is ‘Normal’ for me. Now it’s the standard, I would like to maintain before retirement and after retirement.

My next target!

My new “target” might be owing to a villa or bungalow, and a nice SUV and kids in the ‘best’ school of the area. And once I achieve it, I think it will become a new normal with time.

The next level

And who knows, a car for wife will be a standard I will look for in the future, as I will not be able to manage all the household activities on my own and an extra car becomes a necessity. (I did all my retirement planning calculations with taking decent return on investment as 10% which is quite modest in the long term, so as not to fall in the trap of exuberant returns which might be temporary and actual return might spoil all your calculation.)

Even with a slight increase in any of the above ‘wish’ list (like the possibility of sending you kids abroad for his or her graduation) will push you back in time and you will not be able to achieve you ‘wished’ retirement any time and this carrot and stick game continues.

When your desires convert to your “needs”

You would not know when your ‘desires’ got converted into your ‘needs’. And now it looks like there is a meaning in the sayings of wise old man that “There is enough in this world for one’s needs and not for one’s desires”. I can sense the truthfulness in these lines with some financial literacy and practical experiences.

If at all early retirement could mean anything for a ‘disciplined’ guy is thru’ a windfall gain from lottery or legacy, otherwise if one tries to achieve early retirement from normal gradual process where mind and hard work is involved, his thinking mind will quickly adapt to current situation and will turn the old desired standards in to ‘Normal’ or ‘Below Standard’ life in today’s’ terms.

The word ‘discipline’ need stress here because there is an old saying that irrespective of the size of the pot, if kept isolated all the water will drain out eventually if not refilled on time and only a disciplined life can control this drainage process and can prolong it (Read, why we are overspending these days by Manish)

Or you can become a hermit in deep forest, secluded from this physical world and concepts of ‘Future Expenses’, ‘Inflation’ become meaningless for you, one can think of early retirement stage.

But, I guess this is practically impossible and this article is not intended for those who might be thinking of this stage as one of their future possibilities.

Story of my seniors – Real-life case

I personally know two of my seniors who after working at very senior positions in the company left their jobs as they thought they had enough money to sustain the rest of their lives and tried to follow new pastures in future life.

But, eventually, they had to join back in their respective jobs in order to meet their monthly bills and continue with their other passions in life.

It is human psychology to get adapted to the current situation and at present it looks like achievable calculations on paper and unreal confidence of being satisfied in case you achieve current target, but in reality it does not happen and by your own nature and human being’s reason of existence, you will always be pushed to work.

Basic foundation of human existence is WORKING

This wish of ‘ Not working’ one day will take you away from ‘Karma Yoga’ which is the basic foundation of human being’s existence. Even in GITA, it is mentioned that all of us have to work one way or other and this is the law of life.

I remember a recent discussion with a prominent businessman in my home town. He told me that he used to ‘struggle’ a lot to book rooms in his locality for any private family functions for his guests they had to ‘adjust’ sometimes as per hotel terms and conditions.

Now, he has built his own guest house and no need to be ‘dependent’ on the hotels any more for bookings, etc. and I was thinking that if this rich man thinks booking rooms in 5 star hotels as per their terms and conditions is a compromise in life, what independence could mean for him ?

Don’t buy anything less than a BMW

A few years ago I was having a discussion with one of my friends and in his views, having something below Mercedes or BMW is a compromise as all other brands do not give importance to safety standards and life is precious more than anything else.

At that time owing a Honda city and maintaining it was the kind of life I wanted to live for all early retirement calculations and now since I can afford Honda City easily, I have a choice, either to keep working to be able to buy Mercedes or BMW one day or put my life always at risk while driving mass-produced cars!

We can retire the day we are BORN

On second thought, I achieved financial freedom years back, the moment I had enough money to be able to afford public transport all through my life. In fact, to take it to one extreme side, we have the potential to retire the day we born and it is only afterward that we enter into the working force in this world, fall into the financial trap and again want to get rid of it.

This wish of ‘Not working one day’ can make you lazy, averse to work and afraid of accepting challenges as in your thought process you are always after something else and it is quite natural that you will not focus on the very basic aspect of life you want to get rid of one day.

Here is a great answer which deals with this issue on quora thread

These days a lot of people think of retirement at an early stage, some talk about retirement in the late ’30s or early ’40s and there are various articles circulating around to tell how to achieve it.

But, this kind of thinking pattern in today’s youth is preventing them from acquiring skills which can help them in their current job profile and make it interesting.

Story of my father

My father achieved his financial freedom just after his retirement and both of his sons are well settled and living a decent life and he does not have any liability in his life, yet he is always focused on ‘working life’ and whenever he gets any chance of making money with guest lectures etc., he always looks forward to it and that’s what he says is the secret of his healthy life.

Had he focused on early retirement, this ‘fire’ or ‘energy’ inside him would have subsided quite early and he could have attracted many lifestyles related diseases like blood pressure and diabetes etc, which is happening these days even to the young generation.

So, one should not focus on achieving early retirement any time but should think of living a simple, satisfied, and an exemplary life and realize that the ‘Work’ is the only thing that matters in life and for this you need continuous practice for sound physical and mental health to keep your body fit and energetic and let other things come on its own without worrying about it.

Watch this TED video which talks about an experiment of living a simple life in a tiny home.

It is a good idea and in fact a necessity to have the habit of saving and investing, but the idea should come from the need to meet future expenses and not to achieve early retirement.

So what should be your plan in life?

The financial goal in one’s life should be to have sufficient inflation-adjusted funds for all major expenses in the future like owing a house, Kids education funds, children’s marriage funds, emergency funds, and retirement funds in present terms and all funds invested properly.

At large, one can think of a ‘stage’ where he or she will not be worried about ‘Net savings’ from the income and can live a life one desires with his current income from job or business and even If he/she spends all of the earnings he should not be worried financially.

The more one earns, the more facilities one can desire and his current lifestyle will remain in accordance with his income levels and this is what I call real ‘Financial Freedom’.

That is an inherent assumption here that the rise in expenses (with inflation) will be taken care of by salary increments/ job changes or business expansionsand for there is no other alternative but to ‘Work’.

What do you think about Early Retirement?

So let us know what you feel about this concept and my points regarding it? Do you agree with them? Is there any point where you can add?

Would you like to share your own story in the comments section and how you have dealt with the concept of early retirement? We would like to thank Vikram for his contribution on this subject on this blog.

Also, if you feel you can write on jagoinvestor and contribute, please click here

Important points regarding HRA?

Important points regarding HRA?