Now it has become much easier to transfer your EPF accounts while changing jobs. You no longer have to file separate EPF transfer claims using Form-13 after changing jobs. It will now be done automatically. EPFO has introduced a new composite form called Form 11 that will replace Form 13 in all cases of auto transfer.

In this article I will tell you the process of transferring your EPF account in case you are changing your job.

EPFO i.e. Employee’s Provident Fund Organization has introduced the online portal to transfer your EPF account from one employer to another employer.

How to transfer EPF online automatically in case you change your job?

Old Process –

Earlier, transferring EPF account from one employer to another employer was quite a hassle for an employee for which employees needed to wait for a prolonged time period. As per the old process, one had to complete the process only through offline mode which resulted in various problems like misplacing your documents, taking a long time to get the claim approved and a communication gap which had proved as a major problem.

New EPF composite form 11 –

Form 11 is a composite declaration form, which includes all the basic details of the employee such as Name, registered mobile number, bank account number, PAN number, date of birth, date of joining, etc.

From now on, employees have to fill only form 11 to his employer at the time of changing his job, and his EPF account will be transferred to his new employer automatically. But for this process employee’s UAN must be linked with his Aadhaar number, so that the employer can verify employee’s details and e-KYC.

The introduction of this new online portal has saved lots of effort from every employee and made this process a lot easier.

Let’s see the process of how to transfer EPF online.

Online mode of transferring EPF Account:

Here in this process, I have classified all the steps into 3 categories according to the work done by employee, employer, and EPFO. Now let’s see the steps –

What employee has to do –

Fill form 11 – providing all your details.

Provide all the details regarding your previous job.

Sign and submit this form to a new employer.

What employer has to do then –

Get the form filled by the employee and check the details entered.

First, enter all the details of the employee and then upload form 11.

Further process –

The employee will get an SMS on his registered mobile number to inform him that his auto-transfer request is in process.

Once the process of transferring the account is completed, the employee will be informed via SMS or e-mail ID register with UAN.

The process will be completed unless –

Employee stops it in between

The new employer deposits his 1st contribution

Watch this video to know how to merge EPF account from one company to another company:

Let us know if you understood the process? Have you tried doing this?

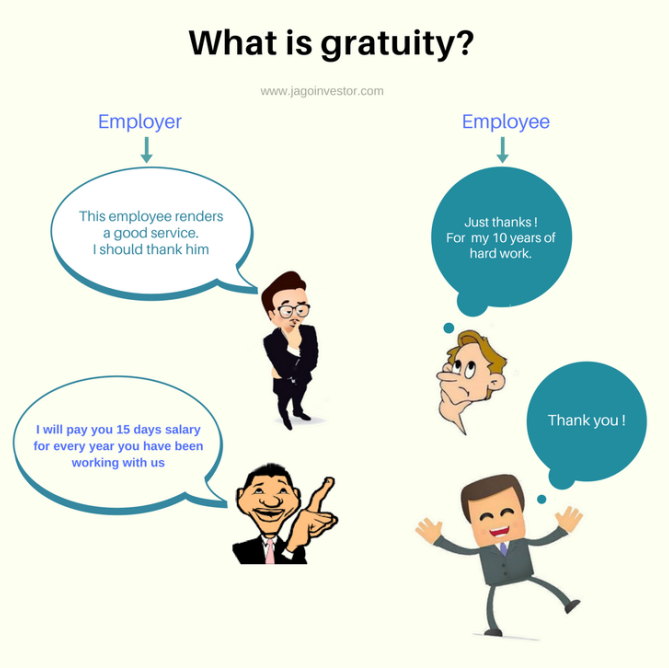

Do you know anything about gratuity? It is one of the components of your salaried income which you will get at the time of your retirement. A lot of people are not even aware of the term gratuity and tax exemption on this amount.

In this article, I’m going to tell you what is a gratuity, how it is calculated and how much tax exemption you can get on this amount.

Recently limit of gratuity payment has been increased from Rs.10 lac to Rs.20 lac. This hike is a kind of good news for employees who are working in the non-government sector for more than 5 years in the same company.

First of all, let me tell you what is a gratuity.

Meaning of Gratuity

Gratuity is the reward given in the form of money by an employer to his employee for being loyal to the company and completing 5 or more than 5 years of service in the same company.

Various countries have different gratuity limit. In India, this limit was Rs.10 Lac earlier but after implementation of the 7th pay increment of salary this limit has been increased from Rs.10 lac to Rs.20 lac.

Mode of Gratuity payment:

Just like your provident fund gratuity is also paid totally by the employer only. It depends on the employer’s decision that either he will pay you this amount or he may take a group gratuity plan with an insurance company. The employee can also contribute to his gratuity if it is paid through insurance company whereas it is not mandatory.

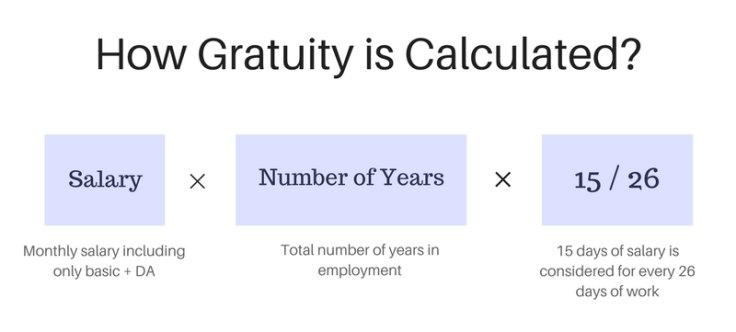

How gratuity is calculated?

Once you complete 5 years of your service, gratuity will be calculated for 15 days per year of your employment. The total working days considered are 26. It will calculated the number of years of your employment.

While considering years of service if the time period is more than 6 months then it will be considered as 1 year. For example, if your service period is 5 years and 7 months then for gratuity calculation it will be taken as 6 years.

Below are the terms taken into consideration while calculating gratuity:

Last drawn salary including basic pay and dearness allowance.

No. of years of your employment.

Paid for 15 days per year of employment considering working days as 26.

The formula for calculating gratuity is given below.

Let’s take an example of gratuity calculation.

Suppose you are working with a company from the last 5 years and 7 months and your salary is Rs.50,000 including DA. Then your Gratuity will be –

= 50000*6*15/26

= Rs.1,73,076.9

At what time gratuity is given?

Gratuity is a kind of superannuation. When a person completes 5 or more years of his service in the same company then he is eligible to get gratuity.

The criteria for gratuity payment is given below.

Retirement of employee

When an employee resigns the job after completing 5 years.

In case of death or permanent disability because of an accident.

The criteria of completing 5 years of employment will be relaxed in case of death or permanent disability caused due to an accident. In this case, the employer will pay gratuity for 15/26 days of every completed year of service.

Companies are supposed to pay Gratuity?

The gratuity act was originally passed in 1972. This act covers all the workers or employee’s in various companies, factories, mines, etc. As per this act, all the companies who have at least 10 employee’s have to pay gratuity.

If a company has 10 employee’s though for a single day in a period of 12 months then the company is eligible for paying gratuity.

Who is eligible to get Gratuity?

There are 3 criteria’s for an employee to become eligible for Gratuity which is as:

The employee should retire after completing 5 years of service in the same company.

Employee must resign after 5 years of service in the same company.

In case the Employee passed away or suffers from any kind of deficiency while he was still working.

Whereas as per the rule under section 4(2), 5 years doesn’t mean 365 days/ year. As per this rule, an employee who satisfies the criteria given below is eligible for Gratuity, the criteria are as –

The employee should work 240 days a year – if the company has 6 working days.

The employee should work 190 days a year – if the company has 5 working days

This rule is will not be applicable if the employee dies or becomes disable while he is still working. In that case, the company will provide Gratuity to such employee or the nominee.

Is gratuity Amount Taxable?

In the current situation all the government employee has a tax benefit on their gratuity. There will be no tax on the amount received as gratuity for government employees for state government, central government or a local authority.

For non-government i.e. private sector or public sector employee’s tax exemption is depending upon either the employer company is covered under gratuity act or not.

1. Employer covered under payment of gratuity act:

When a person is working in a private sector and his employer company is covered under gratuity act then he can get tax exemption on his half months salary i.e 15 days salary of every year of his employment.

2. Employer not covered under the payment of gratuity act:

When your employer company is not covered under the gratuity act then you can get tax exemption on any one of the three options given below. Whichever is less will be considered for exemption –

Rs.20,00,000

Actual gratuity received by an employee.

15 days salary of every year of employment.

[CP_CALCULATED_FIELDS id=”6″]

Change in taxable income because of hike in gratuity limit:

Hike in gratuity limit is more beneficiary for employee’s working in private or public sectors. In any case, government employees are getting tax exemption on the entire amount of gratuity payment.Let’s see the difference in tax exemption after this hike in the gratuity limit.

I hope you got an idea of calculating gratuity and tax exemption on it. If you have any query let us know by leaving your reply in the comment section.

Aadhaar card is becoming the most important documents for any individual in India. Isn’t it very critical to secure crucial details from hackers who might try to steal your data? Some months back, even MS Dhoni’s Aadhaar data was leaked.

So today we will talk on how you can secure your Aadhaar card bio-metric details and prevent others to access your data, and also how to unlock it back later.

Why unlock your Aadhaar card details?

At the time of applying for Aadhaar card, you gave your photo, fingerprints and iris details (eye scan) which is called biometric details.

Nowadays, every organization like phone companies, financial organizations have come up with the concept of e-KYC, where they will just enter your 12 digit Aadhaar number into their Aadhaar-based authentication system instead of asking for all your details when you want to open an account, and it will access all your information like name, date of birth, address etc. from the Aadhaar database.

Details of information captured in Aadhaar:

Photo

Signature

Full name

Address

Mobile number

Date of birth

Education

Bio-metric

Bank details etc.

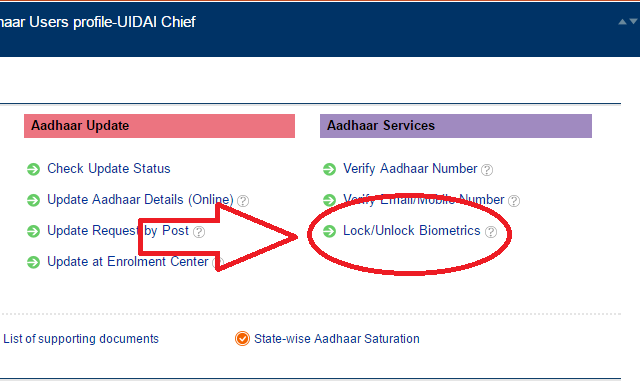

If you lock your bio-metric details then no one will have the authority to use it without your permission. Not even any government institution. If you want to perform e-KYC then you can unlock it for 10 minutes, after that it will lock again automatically.

This locking and unlocking can be done only through online and your mobile number or mail ID must be registered in your Aadhaar.

Enter your Aadhaar number and security code and click on Send OTP

Enter the OTP received.

Now if you want to unlock your details for temporary then click on “Unlock It”.

And if you want to Unlock your details permanently then uncheck the checkbox of “Lock” and click on “Disable Locking”

Why do we need to safeguard our Aadhaar details?

It is of utmost importance to secure yourAadhaar card details. Let us know why we need to secure our Aadhaar details.

As we all know that Aadhaar card is becoming the Unique identification and in future every legal procedure will be Aadhaar verified. This means that if someone has your Aadhaar details then he/she can take advantage of your details and misuse your Aadhaar card.

Various companies have taken contracts of issuing Aadhaar cards. So they had taken the biometric details of every person who enrolled for Aadhaar card through these companies. Now as these companies have your details there is a possibility that they may misuse these details for their own purpose.

The experts have said that the details provided in the Aadhaar card should be secured so that no one can take advantage of any other person’s personal details.

This newly introduced safety feature can help you to secure your details and only you have the authority to unlock the details whenever you wanted. No other person, company or bank has permission to use these details without your permission.

For this, your registered mobile number must be in use because the OTP required will be sent on the registered number.

You can click on this video given below to see the feature.

What if I happen if my mobile number or E-mail ID is not registered?

As per our conversation with the Aadhaar customer care executive on their contact No. 1947, if you don’t have your registered mobile number or E-mail ID in use, you cannot go further for the online procedure to update or Lock/Unlock your details.

In that case, you have to visit the Aadhaar center with the Xerox copy of your Aadhaar, fill the required details and submit it.

To search the nearby Aadhaar center you can visit this link. Or you can download & fill the form by yourself, attach the copy of your Aadhaar and send it by post on the address given on the form.

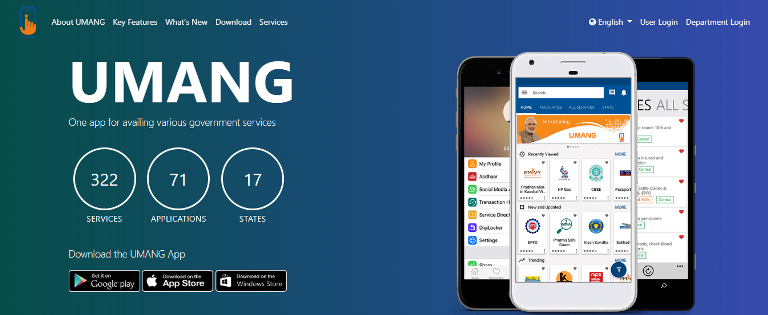

After the launch of the BHIM and TEZ app, the government of India has now launched a new multi-channel platform which is known as Umang App. This move has been taken by the GOI to unite all the government services and schemes in one place and make it more convenient for all the citizens to take the benefit of these services.

What is UMANG APP?

Umang (Unified Mobile Application for New-age Governance) is an all-in-one mobile app that has 1200 services including state and central government. It is a multi-channel platform that is absolutely free for everyone. This app will reduce your efforts of going to the regional government offices. It will also save you precious time and energy.

How to register for the Umang app?

Downloading and registering for the Umang app is as easy as downloading other apps from the Google Play Store and the iPhone app store. It can be completed with a few simple steps. Let me tell you how?

Download the Umang app from your mobiles Play store

Select preferred language and click on terms and conditions

Click on register (if you don’t have login id and password) and proceed by entering your mobile number (make sure that you have this number in front of you because you will receive an OTP)

Enter that OTP and proceed to set MPIN.

Now enter all the other details like your name and all and click on submit.

Once you save all the data then you get confirmation at your registered mobile number .It also says if you have not updated your details then you can give missed call at this number- “1800-11-5246.”

That’s it. With these simple steps, you will be registered with the Umang app. If you enter your Aadhaar number, it may use your Aadhaar number for E-KYC purpose and your data linked with your Aadhaar will be automatically linked with the Umang profile. You don’t need to provide any other details for the registration process.

Watch this video to know about all the features of Umang app :

Many of our investors, when we ask them about their accumulated balance in their Provident fund account or pension fund, they don’t have any idea about the same. So for all those investors, Umang app is very useful to get to know the balance of all their investments in EPF/PPF, or other government schemes, on just a few clicks. So, in this article, we have focused on how to check EPF balance. By following the same process you can get to know about other government schemes balance.

What is EPFO?

EPFO (Employee Provident Fund Organization) assists the Central Board in administering a compulsory contributory Provident Fund Scheme, a Pension Scheme and an Insurance Scheme for the workforce engaged in the organized sector in India.

How to check EPF balance and view passbook on the Umang app?

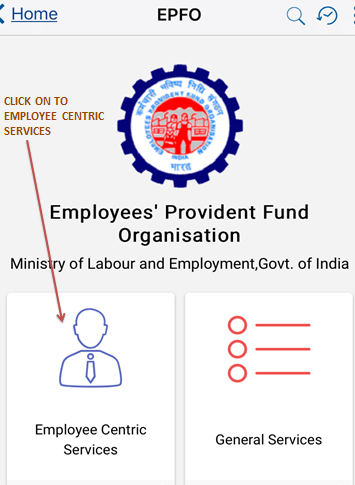

Step#1– Open the Umang app and click on to EPFO :

Once you click on the Umang app and click EFPO. After you click EFPO the below window opens. Then click on to employee-centric services to know your EPF balance.

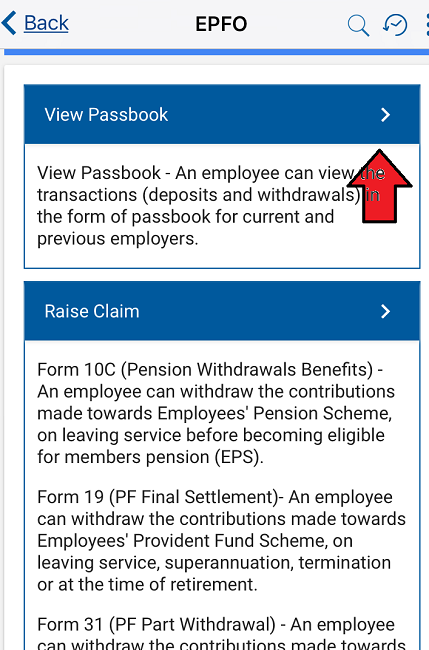

Step#2 – Click on to view passbook :

After clicking on to employee-centric services, below window appears. Now click on to view passbook and wait.

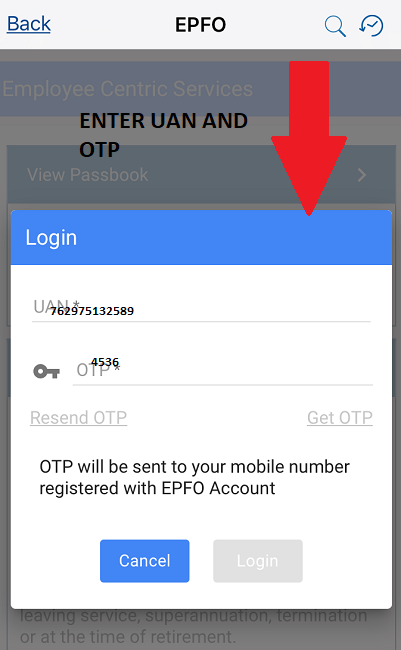

Step#3 – Login :

After you click on to view passbook now you will have to log in. For login, you need UAN (Universal Account Number) allotted by the EPFO to every employee that contributes to PF. You can ask your employer for your UAN number. Once you enter UAN number, you will have to click on get OTP. You will receive OTP on your registered mobile number. Put the OTP and log in.

Please note – If you leave your current job and move to another job then your UAN number will not change. This UAN number will be with you forever.

Step#4 – Again click on to view passbook :

After you log in the below window appears. You will have to click on view passbook and

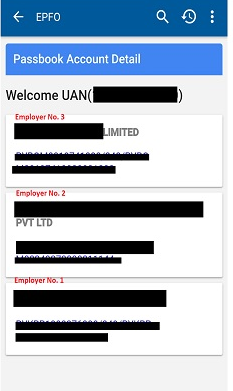

Step#5 – Details of your EPF balance :

After you click on to view passbook the below window will appear which will show you the entire EPF balance created during your employment with various employers. You can open each of the links that are mentioned employee wise to see complete details of the deposit made towards PF.

List of other services available on UMANG APP:

Central Services :

AICTE ( All India Council for Technical Education)

Aadhaar Card

Bharat Bill Pay

Bharat Gas (BPCL)

Buyer Seller – mKisan (Sell product to Better Price)

CBSE (Central Board of Secondary Education)

CHILDLINE 1098 (Night and Day)

CISF (Ministry of Home Affairs, Govt.of India)

CPGRAMS (Centralized Public Grievance Redress and Monitoring System (My Grievance)

Crop Insurance (Department of Agriculture, Cooperation and Farmers Welfare)

CRPF (Central Reserve Police Force)

DAY – NULM (Deendayal Upadhyay Antyodaya Yojana National Urban livelihood Mission)

Digi Sevak (Digital India Volunteer Management System)

Directorate of Marketing & Inspection (Department of Agriculture, Cooperation and Farmers welfare)

e-RaktKosh (A Centralised Blood Bank Management System)

eMigrate (Ministry of External Welfare)

ePashuhaat (GPMS Transportal)

ePathshala (National Council of Educational Research and Training)

EPFO (Employees’ Provident Fund Organisation)

eRahi Sukhad Yatra (National Highways Authority of India)

ESIC – Chinta Se Mukti (Employees’ State Insurance Corporation)

Extensions Reforms Monitoring System (Ministry of Agriculture and Farmer Welfare)

Farm Mechanisation (Ministry of Agriculture and farmer Welfare)

Goods & Service Tax Network ( Ministry of Finance)

HP GAS

INDANE GAS (Indian Oil Corporation Limited)

Kendriya Vidyalaya Sangathan

Khoya Paya (Citizen’s Corner of Track Child)

Kisan Suvidha (Ministry of Agriculture and Farmer Welfare)

MADAD (Ministry of External Affairs, Government of India)

Ministry of Petroleum & Natural Gas

My Pan (Income Tax Department )

National Consumer Helpline (Department of Consumer Affairs)

National Scholarship Portal (Ministry of Electronics and Information Technology, Government of India)

NDL India (National Digital Library of India)

NPS (Retired Life ka Sahara, NPS hamara)

ORS (Online Registration System – Patient’s Portal for e-Hospital)

Parivahan Sewa – Sarathi (Ministry of Road Transport & Highways)

Parivahan Sewa – Vahan

Passport Seva

Pay Income Tax

Pensioner’s Portal (Department of Pension and Pensioner’s Welfare)

SARAL (Transforming Citizen service delivery in Haryana)

SSRD KYRC (Special Secretary Revenue Department – Government of Gujarat)

The welfare of Plain Tribes & Backward Classes Department (ASSAM)

As you now know that, with just a few clicks you can know your EPF balance. I have checked mine, what are you waiting for go and check yours. If u still have any doubt or query please ask in the comment section.

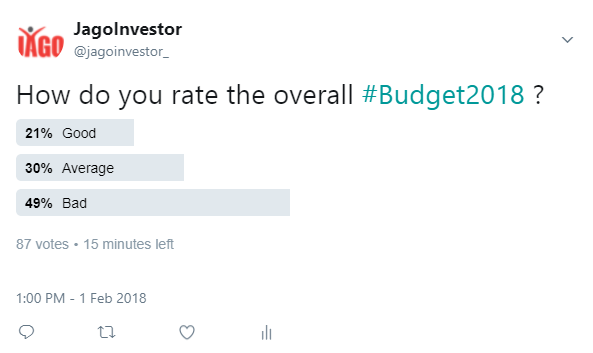

This was the last budget of BJP govt before the next elections and it was expected that they would announce some very good changes in budget which will be for middle class. From last many years, the tax slab rates have not seen any major changes (except few small changes) . The 80C limit and housing loan interest deducted limits were revised few years back, but still the common man expected some really good news.

While the budget was very good for farmers and rural sectors in general and also for senior citizens, it was extremely disappointing for middle class who are mainly into jobs.

On twitter, I asked about people opinion on the budget and as expected, most of the people were not happy about it.

12 Things related to the middle class in 2018 BUDGET :

[su_table responsive=”yes” alternate=”no”]

1. No change in Tax Slabs

2. Standard Deduction of Rs 40,000

3. Long Term Capital gain Tax on Equity Gains at 10%

4. Dividend Distribution tax of 10% on Equity

5. Increase in Health and Education Cess to 3% to 4%

6. No tax on interest from Deposits up to Rs 50,000 for senior citizens

7. No TDS for deposits for Senior Citizens up Rs 50,000

8. Health Insurance deduction increased from 30,000 to 50,000 for senior citizens

9. Increase in limits for critical illness treatments

10. Corporate tax @25% for companies with turnover of less than 250 crores

11. EPF contribution of new women workers capped at 8%

12. Health Insurance Scheme for 5 lacs sum assured for majority

[/su_table]

1. No change in Tax Slabs

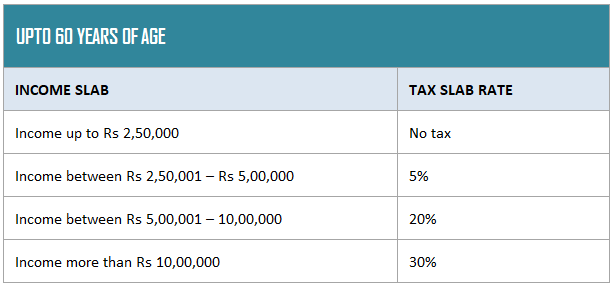

One of the biggest disappointments for everyone in this budget was that the tax slabs were not changed at all. In media we keep hearing on how the minimum limit for taxation should be raised from 2.5 lacs to 5 lacs, but it was not even raised to 3 lacs.

Below are the slabs.

So you will still pay the taxes as per old slab rates only.

2. Standard Deduction of Rs 40,000

There is a standard deduction of Rs 40,000 allowed in this budget, which means that you can now reduce your taxable salary by Rs 40,000 directly along with other deductions and benefits. But this only looks great on paper, because the transport allowance of Rs 19,200 and medical reimbursement of Rs 15,000 are now removed as benefits.

So earlier anyways one was able to claim around Rs 34,200 ,so the added advantage is only for Rs 5,800 more.

You will only save a little headache of providing the medical bills which you used to do for claiming Rs 15,000 (a lot of people used to provide fake bills). So now the process will be simple

3. Long Term Capital gain Tax on Equity Gains at 10%

The biggest news in this budget was the reintroduction of 10% tax on long term capital gains on equity without Indexation benefits. Let me touch base on this a bit as this is very important to understand, however I will make another details article soon on this.

Till now, if you held equity stocks or equity mutual funds for more than 1 yr, then all the profits you made were tax free when you sold them. However now you will have to pay 10% tax on the profits on profits above Rs 1 lac.

However this will only apply on the profits made after 31st Jan 2018 and if you sell your holdings after 31st Mar 2018. All the gains you have made till 31st Jan 2018, are protected and now they will be considered as your cost price.

So if you had bought a stock or equity mutual funds for Rs 1 lacs in May 2017, and its value on 31st Jan 2018 was 1.2 lacs, then you do not pay any tax on this profit of Rs 20,000 . Now your cost price will become 1.2 lacs .

Now if you sell it in let’s say Dec 2018 for Rs 1.5 lacs , then your capital gains will be 1.5 lacs – 1.2 lacs = Rs 30,000 (not 50k).

[su_table url=”” responsive=”no” class=””]

Particulars

Before Budget

After Budget

Buy Date : 1st June 2016

Rs 5,00,000

Rs 5,00,000

Sell Date : 1st July 2019

Rs 10,00,000

Rs 10,00,000

Price on 31st Jan 2018

Rs 7,00,000

Rs 7,00,000

Purchase Price Considered

Rs 5,00,000

Rs 7,00,000

Capital Gains

Rs 5,00,000

Rs 3,00,000

Capital Gains Exempted

Rs 5,00,000 (100%)

Rs 1,00,000 (as per new rule)

Capital Gains which will be taxes

Rs 0

Rs 2,00,000

Tax Rate

NIL

10%

Tax Payable

NIL

Rs 20,000

[/su_table]

Note that the capital tax gains will come into picture only when you sell your holdings and the tax will be applicable only on the profits above Rs 1 lac.

Capital gains on equity was already there before 2004, At that time it was 20% on profits with indexation or 10% without indexation. Now they are reintroduced.

Note that if you sell your holdings before 31st March 2018, the old rules still apply. This new rules are only going to be in picture if you sell after 1st April, 2018.

What should you do?

Nothing!

Dont get too emotional about the tax part. I know people hate paying tax in any form, and especially when it comes as a surprise. But the truth is that the capital gains tax was there before 2004. Its not reintroduced. You should feel happy that for 13 yrs, there was no taxes on equity gains and those of you who have made great returns in past decade enjoyed it tax free.

Also, the capital gains tax on equity is one of the lowest in India at 10% . Most of the other countries tax it at anywhere from 15-35% . So we are not in bad shape.

Equities are still one of the best asset classes, and now lets focus on your wealth creation over long term. The fundamentals are still strong and the equity is set to give great returns over long term. Even with this 10% tax, equities are the best thing to invest in (for long term)

4. Dividend Distribution tax of 10% on Equity

Before of the LTCG on equity , now the dividends from equity mutual funds and stocks will also be taxed at 10%. However this will at source. Which means that it will get deducted by the company itself and you will get the dividend post deduction of 10% . You will not be paying any tax at your end, so there is no headache of all that calculation and CA work

For example, if the company announces Rs 10 dividend per share/unit and you are suppose to get Rs 10,000 dividend , then you will get Rs 9,000 and Rs 1,000 will be paid to govt directly by the company.

This applies to both dividend and dividend reinvestment option in mutual funds.

The dividend distribution tax and treatment for debt mutual funds is still the same. No changes in that.

5. Increase in Health and Education Cess to 3% to 4%

The cess was increased from 3% to 4% in this budget.

Cess is something which you pay extra on the income tax. So if you are in 20% income tax bracket, then you will pay 4% more on 20% , which will make your income tax rate as 20.8% .

If your income tax amount comes to Rs 20,000 per year, then your cess will be 4% of Rs 20,000 = Rs 800.

With 1% increase in cess, you will pay Rs 200 more now (if your income tax is 20,000). This will increase your tax burden by a very marginal amount.

6. No tax on interest from Deposits up to Rs 50,000 for senior citizens

This budget has given a lot of benefits for senior citizens.

One big benefit is that now there won’t be any tax on interest on all the deposits and bank interest up to Rs 50,000 for senior citizens. This will include interest of saving bank account, fixed deposits and recurring deposits.

7. No TDS for deposits for Senior Citizens up Rs 50,000

Now there won’t be any TDS deductions for interest from deposits (fixed deposits and recurring deposits) upto Rs 50,000. Till now the TDS was deducted as per provisions of section 194A , if the interest was above Rs 10,000 , but now it will be Rs 50,000 limit.

8. Health Insurance deduction increased from 30,000 to 50,000 for senior citizens

Under section 80D, there was an exemption of up to 30,000 per year for health insurance premiums for senior citizens, but now it has been increased up to Rs 50,000 . It’s a major relief because for senior citizens the health insurance premiums are very high and in most cases, it’s more than 40-50k anyways.

9. Increase in limits for critical illness treatments

There is an increase in the deduction limit for medical expenditure for certain illness up to Rs 1 lac for all senior citizens under section 80DDB . So in a particular year, if a senior citizen spends money on treatment of these illness, they can claim deduction on up to Rs 1 lac.

Here is the list of all illness covered under Sec 80DDB

Dementia

Dystonia Musculorum Deformans

Motor Neuron Disease

Ataxia

Chorea

Hemiballismus

Aphasia

Parkinsons Disease

Malignant Cancers

Full Blown Acquired Immuno-Deficiency Syndrome (AIDS)

Chronic Renal failure

Hematological disorders

Hemophilia

Thalassaemia

Increase in deduction limit for medical expenditure for certain critical illness from Rs. 60,000 (in case of senior citizens) and from Rs. 80,000 (in case of very senior citizens) to Rs. 1 lakh for all senior citizens, under section 80DDB.

10. Corporate tax @25% for companies with turnover of less than 250 crores

Those of you who are running any companies, the good news is that the tax rate will be 25% now instead of 30%, provided your turnover is less than Rs 250 crores yearly.

11. EPF contribution of new women workers capped at 8%

Now all the new women how will join the workforce for the first time, their EPF will be deducted @8% only instead of 12% for the first 3 yrs, also the govt will now provide 12% from their side also. It’s still not clear if the employer contribution will also be extra other than govt contribution.

12. Health Insurance Scheme for 5 lacs sum assured for majority

Another big news was that now govt is bringing a health insurance scheme for masses, where each family will be entitled for Rs 5 lac sum assured each year. But this will be mostly for weaker section of society and I don’t think any of our readers will be eligible for this.

There are no details about this scheme right now in budget and no allocations is made for this. I would rather wait for more details before commenting on this more. However if successfully implemented it would be wonderful for our country.

Let us know what do you think about the budget? What is one major disappointment and one great thing about the budget for you?

Digilocker is a Digital Locker service provided by the Indian Government for the citizens to reduce the efforts of carrying hard copies of their documents everywhere. It is a part of the digital India campaign.

Many times it is difficult to carry the hard copies of your documents everywhere. And there is also the possibility of misplacing or losing your documents. So to reduce your efforts and keep your documents safer, the government has introduced this new feature where you can save all documents and use them whenever you want.

Now, let’s see how digilocker works.

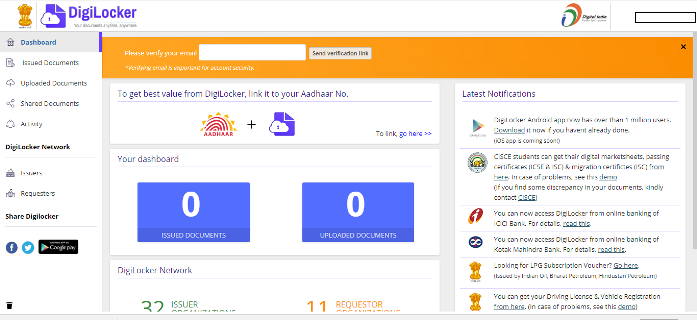

Key Components of Digilocker

When you log in to Digilocker account, on the first page you can see some key components which are useful for the user. These key points are as:

Dashboard

Activities

Shared documents

Issued documents

Uploaded documents

Issuer

Requester

Features of Digilocker:

Digilocker is available in both website and Digi locker app form. Various features of Digilocker make it more attractive and convenient for the users. Some of the main features are listed below:

1 GB space.

Part of digital India.

Can store both uploaded and issued documents.

You can then also share this URI link of the documents to others when you need to submit your document anywhere.

Both Aadhaar holder and non Aadhaar holders can open this account.

Easy and more secure to use.

What are issued and uploaded documents?

Issued documents:

Issued documents are the documents which are shared by the issuer to the Digi locker of the user through push or pull way of sharing documents.

Push way means sharing the documents to the Digi-account of the user by using his Aadhaar number to search his Digilocker account if he has already linked it with his Digi-account.

Pull way is the way of sharing documents through URI link if the user doesn’t have his Aadhaar number linked with his Digi-account.

Uploaded documents:

Uploaded documents are the scanned copies of the documents which are saved by the user to his Digi-account.

How to use DigiLocker?

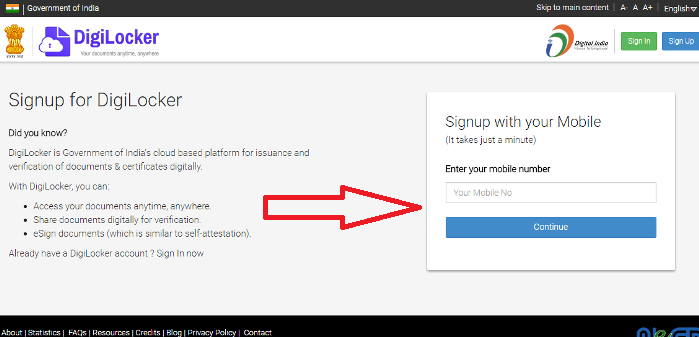

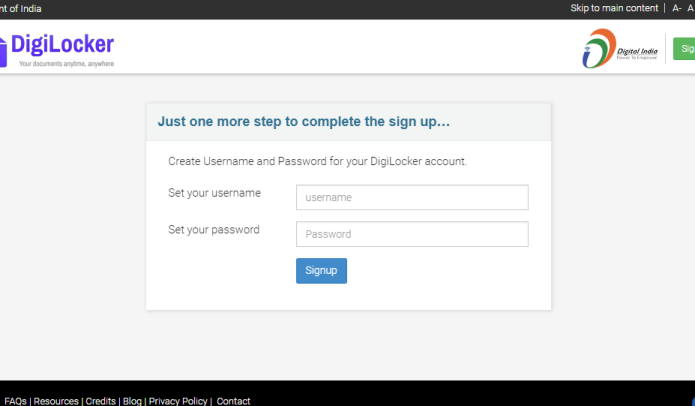

To take the benefit of Digilocker account you have to sign up first which is very simple. To start a Digi-account first sign up for Digi locker and create a Digi-locker account. Go through the steps given below to sign up for a new Digilocker registration.

Step 1: Download Digilocker app or visit the government authorized Digi locker link https://digilocker.gov.in and click on the sign-up button on your right.

Step 2: Enter your mobile number and click on continue. You will get an OTP on your registered mobile number. Once you enter the OTP and click on continue you will be directed to the next page.

Step 3: Now enter your username and password and click on sign up.

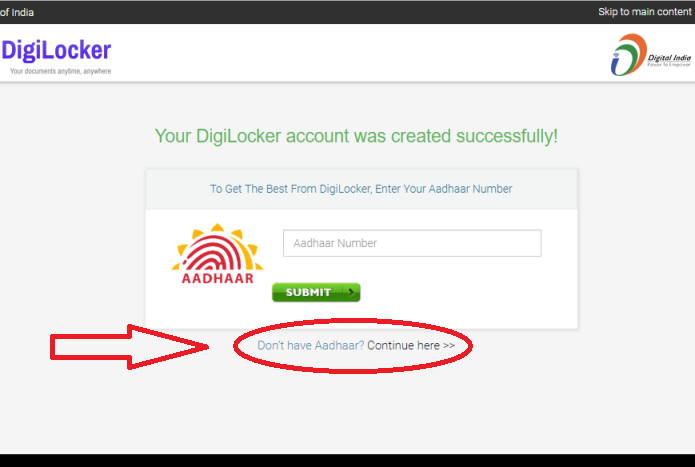

Step 4: Here you will be asked to enter your Aadhaar number. To link your Aadhaar with your Digi-account, your mobile number must be registered with Aadhaar so that you can get OTP. If your mobile number is not registered with Aadhaar, you can skip this step by clicking on the “continue here” button given below.

That’s it. Your Digilocker account is ready to use now.

You can read the user manual for Digilocker here.

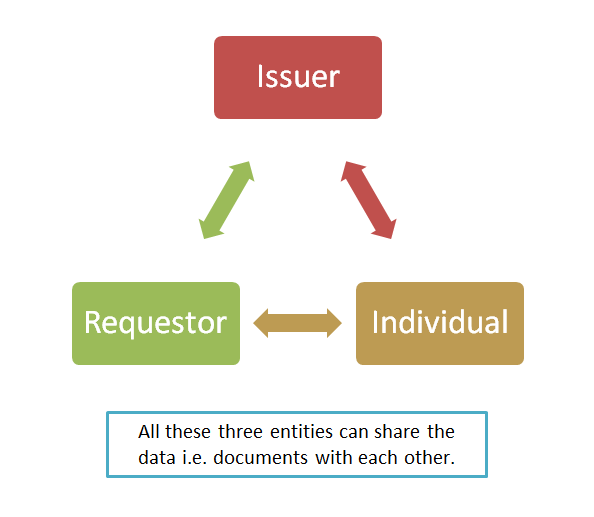

Three entities in Digilocker:

Any person having an Aadhaar card can open a Digilocker and save his documents safely in it. There are generally three categories of people considered as the users of Digilocker. These categories are made on the basis of users of this facility.

1) Citizens/Individual:

The first category includes the person holding the Digi locker account. The person here has all the authorities regarding his Digi locker. Only he can manage the account. And no one can use his Digilocker documents without his permission. On the other hand, this person can use his documents whenever and wherever he wants.

For example: if you go to any government office for some very urgent work and then you realize that you have forgotten to bring one of your document which is very important. what will you do in such a situation?

If you hold a Digilocker account and have saved a copy of that document in that account then you can take print of that document or can simply share the URI link.

2) Issuer:

The issuer can be any Governmental or private institute or company. This issuer provides the e-documents through URI by using persons Aadhaar number. It will help the issuer and the receiver both to provide the document on time and avoid delay.

Besides, there is no need to send the documents physically to each individual on their respective address and track those documents in case that person doesn’t receive it.

3) Requester:

Requesters is the institute or individual who uses your e-documents through Digilocker for the verification or any other legal procedure. When you provide your URI link to the requester then you don’t need to submit any hard copy of that document.

Requester can be universities or any government officials etc.

Benefits of Digilocker:

All the documents shared are paperless so it reduces the efforts of maintaining the paper documents for government officials.

When you save any document to your Digilocker account you can add you e-sign so that it becomes a more authenticated document with self-attestation.

The issuer can directly issue the documents to an individual which makes the document delivery procedure more safe.

User can use the documents saved in Digilocker anywhere, at any time which proves more convenient for the users.

When you use the URI link of the documents directly shared by the issuers, it reduces the possibilities of submitting fake documents.

#Digilocker helpline:

If you have any complain regarding digilocker then you can send your query at [email protected].

One of our readers, Anjan had shared his experience of leaving his salaried job last year to become self-employed. He wrote a detailed experience of his journey on one of the posts so I am reproducing his message in the form of the article here. (note that this was shared last year, but I am posting it now)

Over to Anjan experience sharing below…

I want to start off by saying that I was really inspired by that one article of yours (I am talking about Manish Article) where you wrote your experience about how you quit your job at Yahoo and finally decided to follow your dream against all odds and opposition.

I left my software job at 27

Ever since the day I read that, I knew I had to get started on my dream and drew up an action plan to free myself from this IT job which I considered as nothing more than slavery from Day 1.

So last month, I successfully quit my job at the age of 27.

How my frugal nature helped me

I was always very frugal by nature even from back in my college days when I used to do odd online jobs that didn’t pay much but I ensured I saved every penny I possibly could. I built up sizeable savings which netted me a few thousands of rupees as interest every month.

I guess that habit carried over to my professional life when I got a job. I started saving almost 95-98% of my monthly income and managed my expenses as much as possible from the interest income.

My salary was a meager 35k, so it wasn’t easy but where there is a will, there is a way.

I was fed up of boring work and Politics

So after working 5 years during which I cursed my company and boss every single day, I finally had enough of the BS and dropped the resignation notice on them out of the blue. I got the topmost rating in 4 out of 5 years of my stay there.

So they were surprised by my decision especially at a time when media is reporting massive job cuts in IT due to US Visa issues and automation.

Having to do 12 hours of boring donkey work everyday, having to work on weekends/holidays thanks to impossibly tight deadlines without any extra pay, having to beg for 5 days leave to go on a vacation once a year, having to tolerate their politics and favoritism which denied me opportunities I deserved was killing my soul from within and I was dying a little with every passing day.

Even on holidays/vacations, there was an expectation to be available on phone for support.

I started acquiring new skills and planned my exit

I just knew life couldn’t go like this forever. So I made plans to become self-employed late last year. I started acquiring new skillsets through sleepless nights and sheer hard work to switch over to freelancing with the aim to open a small business a few years later.

Once I felt ready and confident, I quit.

After being self-employed for just over a month, it feels amazing. It’s hard work without a doubt and there have been many sleepless nights to deliver projects on time but the sense of freedom is just indescribable.

There is truly something to be said for working for yourself. The best thing is my salary is not fixed anymore. The harder I work, the more I earn, so there is an incentive to work hard and increase income.

Why I planned it NOW and not in the future?

Age is an important factor. I have reached an age where I knew my parents would start badgering me for marriage within the next couple of years. So I knew it’s now or never. I had to act and I knew I had to stick to my plan no matter what may come or else it will be too late.

The fact that I love to travel was perhaps my biggest motivation to become self-employed as employers would never give you more than 5 days’ leave even if you beg. I am the kind of guy who loves to go on month-long tours.

My next plan?

Thanks to my frugal nature, I saved up enough money during my employment to last many years even if I stop working today. I plan to increase my savings to an amount that would last a lifetime by the time I reach 30.

So a few years of sheer hard work is ahead of me but for now, I am enjoying my new found freedom even though I am working super hard.

Conclusion

Congratulations to Anjan for this new journey in life and best of luck to him. I hope reading his experience would be helpful for those who need some motivation to leave their jobs to break the monotony and explore their full potential.

Let us know if you have any more ideas or points to share?

On 23rd September, we received an email invitation from Deputy Commandant (Dr. Lokesh Khajuria) for leading a personal finance session specially designed for Border Security Force officers and jawans. We immediately accepted his invitation and started our preparation for the same.

Manish flew from Pune, we packed our bags, prepared the presentation and started our Road Trip from Ahmedabad to Jaisalmer. Two more special people who joined us was our business coach Mr. Ravi Iyer and Abhikumar.

We were happy to know that people from defense follow jagoinvestor, it is popular amongst many officers and they had full faith in our work and philosophy.

Our Intention

The intention was to give something back to our nation. I and Manish simply wanted to make a difference in the financial lives of those who are guarding 7000 km of Indian border.

The context set was very simple – “Ek nayi pehel, ek nayi soch ki shuruat”

The context got fulfilled and we could see that the participants got clear about things they should do and not do in their financial life. We went with an open heart and mind and shared all that we knew or have learned about personal finance in the last few years.

Download and read Over 250 messages for defense personnel

We wanted our readers to be a part of this journey and so we invited them to share one message for the border force and along with the message we also asked them to share one “Money Tip”. We got some amazing messages and some very interesting Tip from over 250+ Investors.

We do not have words to share what we experienced in those 4 Days. It was a space of discipline, commitment, and service.

The event positives were

Overwhelming Response from 100+ Participants

Curiosity to Learn more about ways to manage money

Event facilitated and supported by higher management

Check out our journey and some pictures

We would also like to share our journey to Jaisalmer and all the things we experienced there.

Some Thoughts shared by Dr. Lokesh Khajuria

We got an early morning Whatsapp message and I could not stop myself from sharing the same with you all.

Some years back, in the thinking mood, seating alone at BOP KHARIA… thoughts were flowing spontaneously..!!……

Desert has a natural and divine relationship with all human beings.

Almost all the major religions, prophets, saints originated from the desert. Immortal legendary love stories which are invoking human love even today originated from the desert. It is strange to find out what is it that desert wants to teach human beings?

……but if he searches hard enough, he returns with Oasis in his within !!!!! Deep in the desert, she is blessed with divinity… could make flowers bloom in the desert !!………

Dr. Lokesh

The circle of financial awareness is expanding

I and Manish are so happy to witness that the circle of financial awareness is expanding.

Very soon we intend to create the little army of people who are committed to spreading financial awareness. We will need your support in this work and we will ask for your help and support in the same.

If you wish to organize financial awareness program in your organization or company you can get in touch with us on [email protected]. Let’s get together and create a world that works for everyone.

Once again we thank Mr. O.P Sharma, Dr. Lokesh Khajuria, Birbal Sir, Manoj Sir and BSF Jaisalmer Team Gladiators

Recently, the government has asked mutual fund companies (and many other financial institutions) to link Aadhaar card number of their customers with their financial investments.

This means that if you are a mutual fund investor, you are supposed to link your aadhaar numbers to your mutual fund folios.

How to link Aadhaar number with the mutual fund?

There are various online and offline options of linking your Aadhaar number with a mutual fund folios. You can do this linking process through the transfer agent’s platform like CAMS and Karvy who provides services to multiple mutual fund companies

We will mainly look at just CAMS (15 mutual funds) and Karvy (17 mutual funds) serviced mutual funds in this article.

UPDATE: How to check your Aadhaar linking status?

Now you can check your Aadhaar linking status with CAMS and Karvy online. Here are the links :

CAMS services 15 mutual funds companies right now as follows. You just need to follow the process of linking your aadhaar once and it will be automatically updated in all the mutual funds. Here is the list of CAMS serviced funds.

HDFC Mutual Fund

DSPBR Mutual Fund

Birla Sunlife Mutual Fund

HSBC Mutual Fund

ICICI Prudential Mutual Fund

IDFC Mutual Fund

IIFL Mutual Fund

Kotak Mutual Fund

L&T Mutual Fund

Mahindra Mutual Fund

PPFAS Mutual Fund

SBI Mutual Fund

Shriram Mutual Fund

Tata Mutual Fund

Union Mutual Fund

The process to link Aadhaar number in CAMS website

We have created a short video showing the process to link aadhaar with your folios.

Here are steps are given below to link your Aadhaar number with a mutual funds portfolio.

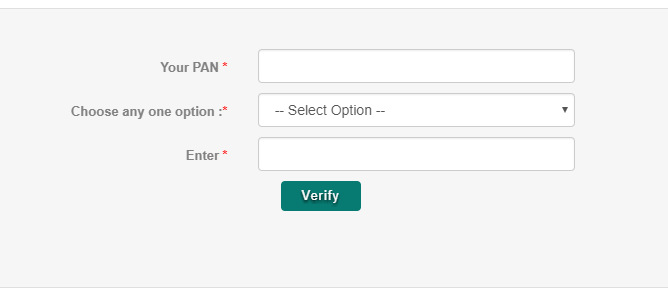

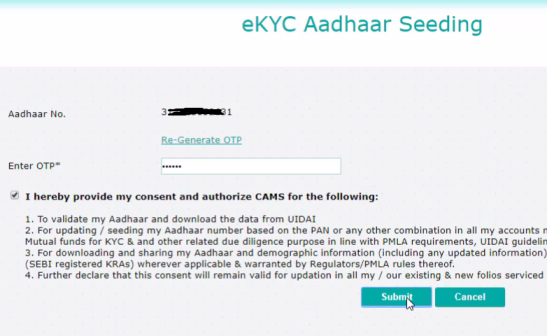

Step 1: Visit this page on the CAMS website and enter your PAN number and select Mobile in the 2nd option and enter the mobile number (you can also select a date of birth or email in the 2nd option).

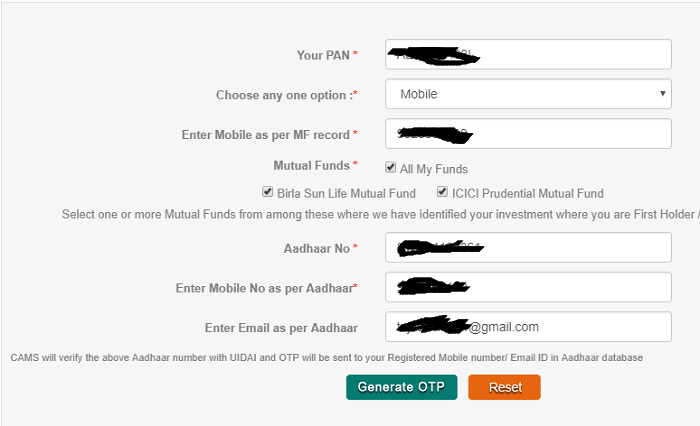

Step 2: On the next screen it will ask for your aadhaar number, a mobile number linked with your aadhaar and email id (which is optional). Then click on submit

Step 3: You will receive one OTP which is to be entered on the next page

So this was the process to link your uidai number with your fund folios in various AMC which are serviced by CAMS.

Link Aadhaar in Mutual Funds (from KARVY website)

Let us also see how to link aadhaar to mutual funds using the Karvy link. Below is a video explaining the process if you don’t want to look at screenshots.

Karvy is the first organization in this field of business providing service to over 90 million investor accounts. A list of the mutual funds is given below to which Karvy is providing service.

Axis Mutual Fund

Baroda Pioneer Mutual Fund

BOI AXA Mutual Fund

Canara Robeco

DHFL Pramerica Mutual Fund

IDBI Mutual Fund

Canara Robeco

INVESCO Mutual Fund

JM Financial Mutual Fund

LIC Mutual Fund

Mirae Asset Mutual Fund

Motilal Oswal Mutual Fund

Peerless Mutual Fund

Principal Mutual Fund

Reliance MF

Quantum Mutual Fund

Taurus Mutual Fund

UTI MF

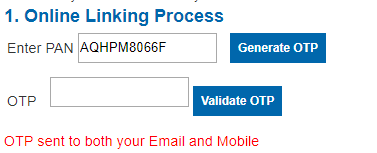

Step 1:Click here to go to the Karvy platform. There you need to enter your PAN number and you will get OTP for verification. Enter that to move to the next step

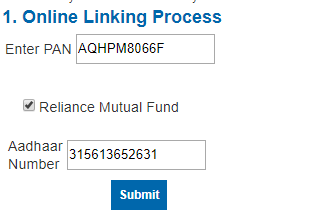

Step 2: On the next page, you will see all the AMC’s where you have the investment and a space to enter your aadhaar number. Make sure all the AMC’s are checked marked.

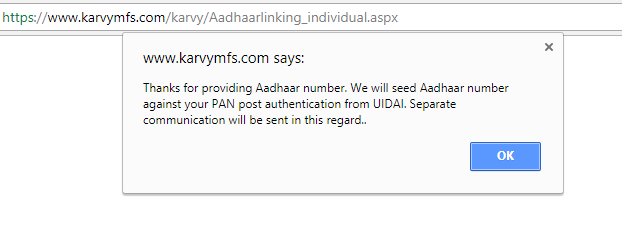

Once you click on submit, you will see the final acknowledgement that the processing will take place now.

You can also update Aadhaar using the SMS facility

Linking your Aadhaar number with your portfolio using SMS service is the easiest way. You just have to send an SMS which includes ADRLNK<space>PAN number<space>Aadhaar number and send it to 9212993399 from your registered mobile number.

Karvy will do the further linking procedure by considering this as valid information.

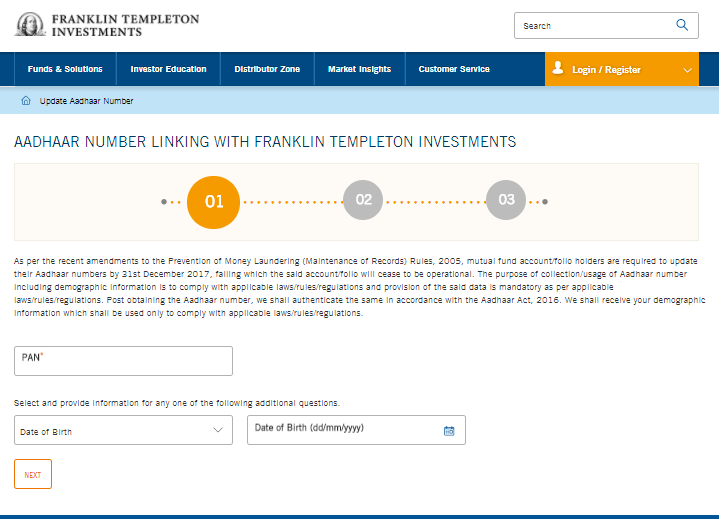

Update Aadhaar in Franklin Templeton mutual fund

Franklin Templeton mutual fund is not serviced by CAMS or KARVY, hence you need to do the process for it separately on its website by visiting this link

You need to enter your PAN and other details to start the process.

Note that it looks like Sundaram mutual fund has still not started the process for aadhaar linking as I was not able to get any information on this. If you have invested in Sundaram funds, kindly get in touch with their customer care to complete this.

How to link aadhaar number with folios by filling up a form?

Both Karvy and cams provide an option of linking your folios with the aadhaar by filling up a form. This will be helpful for those who don’t have a mobile number and email linked with a mutual fund folio. You just need to download the forms and fill up all the relevant information and submit it to CAMS or KARVY office.

According to PMLA i.e Prevention of Money Laundering Act SEBI has made it mandatory for each and every investor to link their Aadhaar number to the mutual fund portfolio. This step is taken forward to prevent money laundering and keep track of all the investments and transactions within the country.

If you don’t do this linking then your folios will the frozen and you will not be able to redeem the money or make any transactions unless you update the aadhaar number. So please take this on priority.

Is this applicable to NRI Investors?

No, This is not applicable for NRI investors, HUF and even non-individuals (like companies and partnership firms)

Let us know if you have any questions regarding this in the comments section or you can also read this FAQ list to get more clarity on this issue

Job loss is a scary situation because it’s a big disruption in your life. If you lose your job, you need to suddenly look for another job quickly because you have to meet your household expenses and also deal with the emotional crisis.

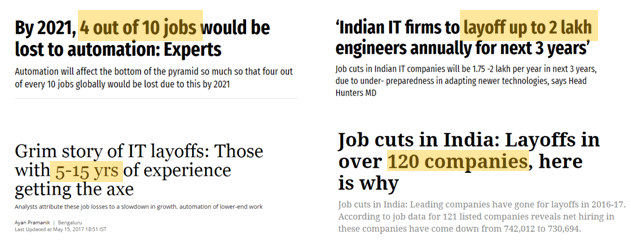

In case of a layoff, you also lose self-confidence and start doubting yourself and keep wondering what the future is going to be now. Look at these news headlines which talk about so many job losses in India. While all the sectors have layoffs, these headlines are more from the IT sector.

Are you prepared enough for a job loss?

Have you ever thought about this situation? Have you ever visualized about losing the job?

We all are so confident subconsciously that something like a job loss is never going to happen with us. We hear that it has happened in someone else life, but we consider ourselves so lucky for no reason.

Our lives are smooth and our planning for the future is perfect, but it’s critical to check if you can take the bad news of job loss? Is your financial life strong enough to handle that situation?

Have you ever thought about this?

Have you ever thought about how you will be paying your EMI’s, your kid’s school fees, rent, various other household expenses and how you will deal with stress and the insecurity which will come with the job loss. If we pick the software industry, there is enough bad news coming in from the last many years.

The industry is going through tough times (and even good times) and it’s not very uncommon to hear that thousands of employees got a pink slip and lost their jobs!

If we talk about you, are you skilled enough to find a new job in the same industry with the same pay package? Can you afford a lower salary? Do you have enough savings to deal with the stress of living without a paycheck for the next 6 months?

I found some real-life experience of people who are sharing about their job loss and how they felt about it. Please read them to understand how it feels and what it means.

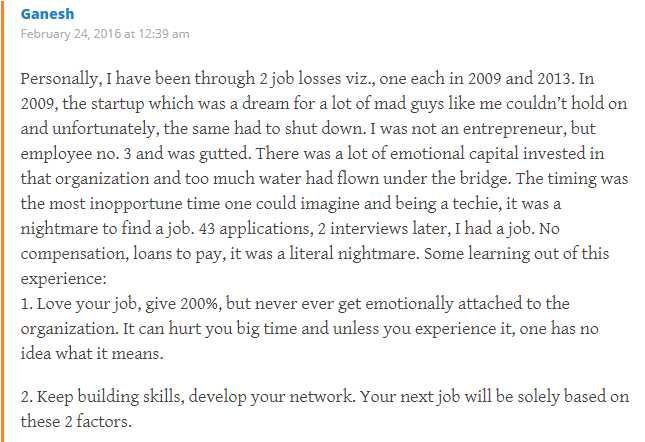

Story #1 – How Ganesh felt when he lost the job in a startup

Below is an experience of Mr. Ganesh who shares how he lost the job and had to face issues in his life.

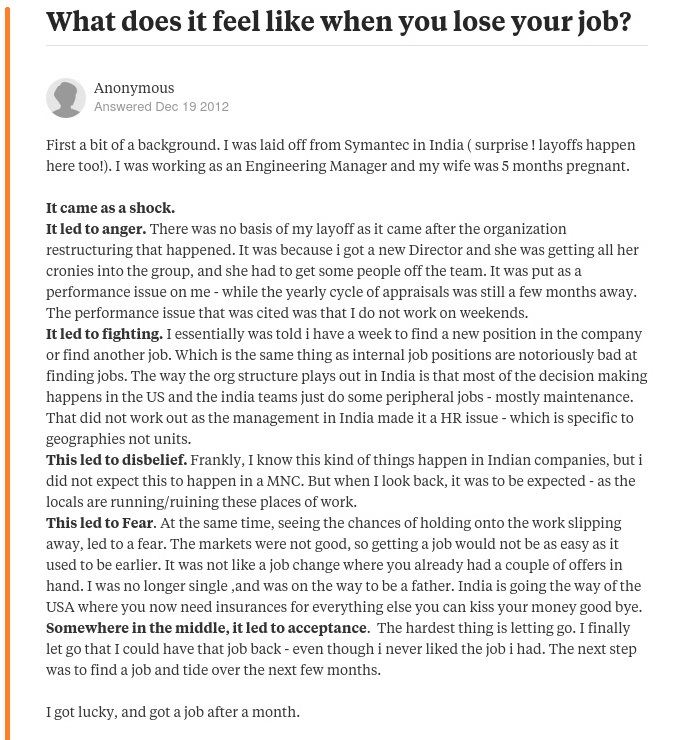

Story #2 – How a software engineer felt after a job loss

Here is another experience of a quora user who worked for Symantec and lost a job when his wife was 5 months pregnant.

How to prepare for bad times?

We don’t wear a helmet while driving because we want the accident to happen. We wear it so to make sure we are protected if something goes bad accidentally.

In the same way, we should design our lives in such a way that even if we lose our jobs, the impact is limited and the emotional and financial loss is in control.

I know losing a job is not a great thing. Most of the wake up when they actually lose the job and start thing on what to do.

Don’t be that guy!

While you can’t stop someone from fire us, you always have control over what you can do to face that situation. So let’s talk about a few things you can and should do today to be ready for that scenario.

Action #1 – Have 6 months worth expenses in an emergency fund

When you lose the job, the immediate question which comes to your mind is – “How will I pay my bills?”

You have EMI’s, household expenses and many more things to deal with. You already know how messy it can get. I don’t want to get into details of it, but you need to pay all the bills. At best you will be able to stop a few things for a while, but how long?

You should have enough liquid money with you which can last for a few months. It’s like the emergency fuel (6-month expenses) you need in your car to reach the petrol station (new job).

One more reason why you need to have enough emergency funds with you is that it gives you more power to choose your next job.

If you do not have money at your end to last another month, you are too scared. It’s a panic situation which forces you to choose any job which comes next. It’s like being desperate for marriage and then saying YES to the first person you meet. Not a good thing for the long term.

Action for you: Just multiply your expenses by 6 and keep that amount invested somewhere which can be available at short notice (like few days). The focus has to be more on availability and not returns. You can choose a debt mutual fund or a simple fixed deposit for this.

Action #2 – Don’t have a neck to neck expenses

A good habit for any investor is to make sure that their income is 1.5 times of their expenses. You should not be living a life where every penny you earn is getting spent.

I know it’s easier said than done for many people, but at least start taking action towards this.

There are two benefits here.

Benefit #1 – You will have good surplus each month which you can invest in for the future. It keeps you worry-free and you also can save good amount.

Benefit #2 – When you lose your job someday, you at least have an option to take up a job that is paying you less. Imagine you are earning Rs 1 lac per month. In case your expenses are neck to neck, you will not be able to accept a job that is offering you Rs 80,000 a month. Can you?

I strongly suggest that your total expenses (including EMI and everything) should not cross 60% of your income. It’s a good habit to practice in your financial life.

Action for you: Find out the ratio between your income and expenses. How much are you saving each month right now? If it’s less than 40%, focus your energy on earning more income. If not immediately, give yourself 2-3 yrs of time when you will increase your income to the next level.

Action #3 – Be awesome in what you do

Don’t be mediocre in what you do. Don’t be average in what you do.

Are you a java developer? Then be the one who knows everything inside out and make sure you are among the top 5% in the entire world

Are you a marketing guy? Then make sure you are the one who can really transform the marketing of a company if you take that task in your hand.

Are you a chef? Then make sure you are worth inviting to master chef show!

Whatever you are doing right now in your life, just make sure you are ONE OF THE BEST.

I am not saying that you should do something extra ordinary in life, but whatever you are doing, strive to be one of the best in that field.

If you focus on this, then you probably will never lose your job. And even if you do, you will quickly get another, And if you don’t get another job quickly, you will at least be calmer and composed than others who know that it’s just a matter of time. Your panic level will be low.

Action for you: Make a list of things you need to do to go to the next level in your profession. List down which are the training you need to attend, list down which all certifications you need to complete. List down if you need to change your job to learn new skills? List down if you want to ask for help from someone more awesome than you. List down all the points and complete that in the next 12 months.

Action #4 – Start saving money and build a good portfolio

There is this concept of human capital and money capital.

Human capital is our ability to work and earn money, it’s about the potential and how much you will bring in the future.

Money capital is your portfolio which gets build over time, you keep earning money and save from it and start increasing your money capital.

When we start our career, we are high on human capital and zero on money capital. When we retire, we have money capital and very low human capital (maximum cases).

Start building a good portfolio

Focus on investing and saving money from a long term perspective. It’s better to lose a job with 50 lacs lying in your mutual funds and deposits in the bank. It’s a much better panic situation compared to just having some money in your bank account.

I know it’s very tough to have any portfolio at the start of the career but do whatever best you can do. Focus on creating your first 1 lac, then first 10 lacs, then first 50 lacs.

But at least take actions to reach there.

If you have good amount in your portfolio it feels safe. You can fall back on something which can last you for many years in the worst case. Imagine not having much in your portfolio and losing a job. Even Rs 10,000 invested per month can give you 25 lacs in 10 yrs if done in the proper way.

So ask yourself, if you have enough money capital as per your situation? Have you built and saved your money capital or not?

In the case of job loss, most of the people who are in extreme panic are those who have no sufficient money capital and human capital. Even if you save 10% of your money income on a consistent basis over your working life, it’s going to be a very huge amount. But most of the people even fail there.

Action for you: First slow down. Then see how much is your monthly surplus each month? Are you investing that money on a regular basis? If not, it’s time for you to start your SIP (our team will help you in building wealth in a systematic manner).

Don’t make these 5 mistakes at your work

Let’s quickly look at a few points which lead to a job loss. Many people just do wrong things at work and expect to never get fired. If the points below are true for you, its time you relook at your approach and take corrective steps.

Not updated yourself as per job requirement – Are you still acting as if you are in 2007? Are you refusing to learn new skills that are required in your job? Are you into that comfort zone? If yes, it’s a signal that you may lose your job because you are getting stale day by day.

Not able to work with others – Are you a team person? Any work is done by a group of people and not a single guy. Make sure you know how to have good relations with your teammates and work with others. If you are not a team guy, you might not be part of the team soon.

Failure to do your work – This is a no brainer. Are you consistently failing in the work assigned to you? Are you not able to complete it in a given time and with the expected results? Get more trained, ask for help from others if that’s the case. It’s ok to fail once in a while, but if it’s happening very frequently you are on a list of non-performers and you might get a pink slip very soon.

Failure to take initiative – Are you just doing what you are supposed to do? That’s all? Are you taking new initiatives yourself and showing that eagerness to go out of your way and surprise your employer? Remember, the pyramid is smaller at the top and you want to move to the top like many others. You will be the first tree to get cut if things get ugly.

Failure to demonstrate productivity – Are you busy or productive? A lot of people do lots of things at work only to produce very little at the end of the day. Make sure you are doing more and highly useful productive work. Also, make sure you show that to your employer. Get it noticed and recorded.

I hope I was able to reignite your thoughts on these points. Do let me know how many marks out of 100 will you give to yourself on preparedness for job loss?

If you are 100% prepared and ready to cope up with it, you score 100/100, else 0/100 at the extreme end. I would like to hear about this from you and what you are going to do about it.