Do you want to invest your money more safely? Here is one of the best options for you. ETF i.e. Exchange trade funds are one of the safe way of investing your money in equity market.

It is an investment fund traded on stock exchange, much like stock. These are attractive investments because of their low cost and stock like features. It offers both tax efficiency and lower transaction cost.

What are ETFs?

Exchange Traded Funds are a basket of securities that are listed and traded on a recognized stock exchange. Simply, they are mutual funds, whose units can be bought and sold on the stock exchange.

Given that an ETF is traded on the stock exchange, its price may not necessarily be the same as the NAV of the underlying portfolio. In other words, an ETF could have an NAV distinct from its market price. The reason being that the market price is usually driven by the demand and supply of units.

Hence there is a distinct possibility of an Exchange Traded Funds units trading at a premium or discount to its NAV.

For Example Nifty BeES , whose underlying is NSE , may not have same price as its underlying , For example if Nifty is 4500 , it may be possible that The ETF’s value is 4600 or 4400 , depending on the sentiments and expectations.

Watch the video given below to know the current status of ETF in India:

How does ETF work?

Exchange Traded Funds are just like stock exchange. For that you need to open a Demat account by any medium like through bank, online brokers or through any consultancy. Check for the prize value of the share so that you will know which of them are in your budget and then you can buy or sell your shares at any time you want to.

It is so easy like suppose you buy some shares at 10:30 in the morning and sell it at 12 pm. then again you can buy another shares after lunch.

Benefits of ETF

ETF’s are the low cost simple solution for the generating good returns from stock market investment. The benefits of ETF are as Given below.

1. Easy to access:

ETF’s can be purchased with just a single transaction. In EYF’s you are buying mini portfolio’s so it is way more easier than buying a basket of Indexes.

2. Cost effective:

Commissions are generally low on ETF as compared to the other tools. Besides this it there is no load fee’s and managing fee is also very low.

3. Transparent:

The most important thing of your investment is transparency. You should know where have you invested your money and how’s it performing. In Exchange Traded Funds, your portfolio details and underlying are publisher daily.

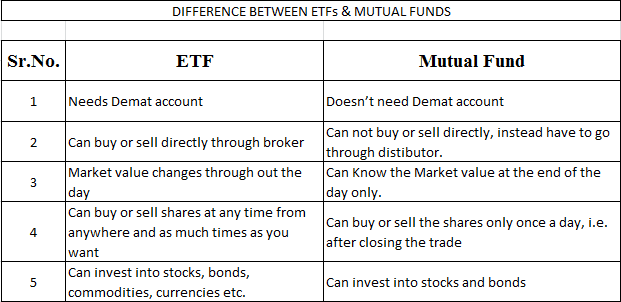

Difference between ETF and Mutual Fund:

Many beginners get confused between Exchange Traded Funds and Mutual Funds. Though ETFs are part of mutual funds, they are different in many aspects than Mutual funds. Lets see some of the differences between Mutual fund and ETFs:

ETF’s in India

Nifty BeES : Tracking NSE

Quantum Index Fund : Tracking NSE

ICICI SPIcE Fund : Tracking BSE

Bank BeES : Tracking CNX Bank Index

GOLD ETF’s or G-ETF’s

Gold ETF’s are the simple investments products that combines flexibility of stock investment and simplicity of Gold investment. Gold ETF’s are different from Gold savings.

IT tracks Gold prizes. Gold ETF’s are one of the best form of Gold Investments. Earlier investors used to invest in gold in metal form. Then comes paper bond and now you can invest in gold through electronic form.

BENEFITS OF GOLD ETF’S:

No risk of impurities.

Flexibility in buying Gold. Like one can buy in smaller lot.

Held in electronic form.

No storage cost.

No security concern like in physical form.

Transparent pricing and potentially cheaper.

Can track your investment values in real time.

No wealth tax like in Metal form.

Advantages of ETFs

1. ETFs tend to be more cost-effective vis-a-vis comparable mutual funds. The expense ratio of a passively managed ETF (tracking a benchmark index) would normally be in the range of 0.50%-1.00%; for an index fund, it can be as high as 1.50%. And for mutual funds the entry load is 2.25% .

2. ETF’s can be bought and sold anytime during the market hours , unlike the Mutual funds NAV at the end of the Day.

3. Given ETFs are traded on the stock exchange, and can be bought/sold on a real time basis; they tend to have low tracking error (deviation of ETF’s performance from that of the underlying index) as compared to index funds.

Disadvantages of ETF

1. Investors need to have a demat and a trading account, with a SEBI registered stockbroker, for investing in ETFs

2. Costly to operate – You need demat account to buy ETF and the charges for demat account might compensate the low expense ratio of ETF. One of our blog readers comments on that

While promoting ETFs it is argued that their 1% edge of expense ratio over mutual funds will be significant if it is compounded over a long period of time, say 20 years. So this advantage of less expense ratio is not there if the calculations in the previous comment are true. What I am trying to say is that the only advantage that ETFs have is that they are like mutual funds that will guarantee market related returns. Nothing less and nothing more.

If you have any query related to this topic you can leave your reply in the comment section.

The term health insurance is generally used to describe a form of insurance that pays for medical expenses. It is sometimes used more broadly to include insurance covering disability or long-term nursing or custodial care needs.

To understand it in simple words, you pay some amount of premium every year to a company and if some thing happens to you like an accident or if you have to through an operation or a surgery, they will pay for it provided, its covered under the Health Insurance.

Why do I need a Health Insurance?

This is the most common thing you can hear from a person who wants to avoid Health Insurance in India, but its one of the most important part of any ones portfolio or plans. People concentrate on the fact that what if nothing happens to them, but they fail to imagine the situation when some thing can happen.

Body is a complex thing, and no one knows what can happen in future, Even things like accidents is not in your hand, you can take try to avoid it, but what about others, what if some car hits you?

What if accidentally fell from some place? It can happen and it happens, and when you have to pay hefty bill for the treatment, you will realize that its a good idea to get covered by paying a small premium every year.

Consider this :

In Mumbai, businessman Manas Kumar rushed his wife Anita, 38, to hospital in January this year because she complained of breathlessness and shooting pain in the chest. Sure enough, it was a heart attack and Anita had to get an angioplasty done.

The cost of the procedure and stay at Hospital: Rs 1.5 lakh. But he didn’t have to shell out a single coin as he and his wife were covered under the Health Insurance with limit up to 4 lacs.

Why is Health Insurance more important now compared to earlier days?

Yes, Health care cost has increased many fold in last 20-30 yrs, Also now more and more younger people are complaining of Heart and other diseases which were seen in older people earlier.

Because of high stress jobs, bad eating habits and other similar problems, more and more cars in the city, pollution etc, the chances of getting some disease meeting with an accident etc have increased compared to earlier days.

More about Health Insurance

You get a good coverage for diseases and surgeries, so most probably you will be covered for most of the things.

You have to pay the premium which you can plan ahead and manage it, else if some thing unexpected happens, your finance gets in problem and impact your plans.

Also you get tax deduction under section 80D up to Rs.15,000 (Rs.20,000 for senior citizens).

You can also go for group insurance, its a ideal thing for a family with spouse, parents, kids … With group Insurance every one is covered and you pay less premium, also its more advantageous because there are many things which are covered in group insurance and not single person health insurance.

Make you buy a good cover which suits you, do good research and then choose the product.

If you want to save money it needs to be invested somewhere. But lot of people makes some mistakes in investing which seems very small at that time but they can prove a disaster to your financial life.

This is my favorite, because it is the mistake done by majority of people, Most of the people are highly under insured. By default, a person must be at least covered for 10-15 times his annual expenses. So a person who has a yearly expenses of Rs 2.4 lacs (20000 per month), must have a cover of around 25-35 lacs at least.

But they have insurance like peanuts, 2 lacs, 5 lacs, or 10 lacs. The biggest reason for this is that they take wrong type of insurance. Most of the people need Term Insurance , but they end up with Money Back plans.

to read more at :

2. No Diversification in Investments

Most of the people don’t pay good attention at diversification. They are either in Debt or Equity. They must understand that they have to diversify along different types on investments to minimize risks and also to boost up there returns.

Some people have only FD’s, PPF’s or NSC in there portfolio, then there are people who hold only Shares or mutual funds. While the former misses on the returns, the later on is exposed to high risk. Combining both of them can decrease risk, increase stability of returns.

3. Tax investment because of Last month rush and not Financial Planning

Most of the people rush for tax saving only in the month of Feb-March, when they get a letter from company saying that they need to submit proofs of investments under section 80C, and that’s the reason why people end up taking wrong products, just because they don’t have time to plan there investments. The best thing is to start planning for tax saving right at the start of financial year.

4. Starting Late

This is another big mistake people do, they do not start investing at the right time. A lot of time people actually can save some money but they feel that its not worth to save a small amount, they think that when they will be in condition of saving enough per month, that would be the right time to start, which is far from truth.

Watch this video learn more about 4 biggest financial mistakes:

Consider this:

Ajay Started his career at 22. He has worked for 8 yrs and now he is 30 yr old, He wants retire at 60, and can invest for another 30 yrs. He want to generate 4 crores for his retirement. He has 3 choices

1. 6000 every month for next 30 yrs.

2. Invest 10,000 every month for next 7 yrs and then leave it to grow for another 23 yrs.

3. Invest 20,000 per month for 3 yrs and leave it for 27 yrs.

Guess which choice will give him maximum money , The one where he is investing more for less years !!! . Yes .. The corpus generated is as follows:

1. 4.2 crores

2. 4.59 crores

3. 5.11 crores

So the idea is, start early and invest more … remember:

Start Early, Invest less = Start Late, Invest a Lot

Btw, Had Ajay invested 4,000 per month right from the time when he was 22, and invest for next 8 yrs and waited for that money to grow till retirement, He can generate more than 6.5 CRORES !! That’s better than all the 3 choices 🙂

Also see this example :

Considering return of 15% per annum from Diversified Equity Mutual fund, If you invest 10,000 per month for 10 yrs and then leave it to grow for 20 yrs, your investments worth will be 4.5 crores, But before that if you also invested 5,000 for 5 yrs and then 10,000 for 10 yrs, your money will be 7.5 crores.

One of my good friend had a small argument with me, that she would not invest in Term Insurance, because she will not get any “returns” out of it. I believe investing in a term plan looked a very unprofitable thing to her as she never gets back the money she paid as “premiums”, if she survives.

Endowment plans looked nice to her, because they provide money if you are dead and even if you survive. You get back money as the prize for not dying !!!.

With respect to Term insurance, she understood the fact that her family will get the money from insurance company in case of her death, but she was concentrating on the fact that she would not get back anything if she survives.

What is the return in that case? Nothing !!! and looked like some one is fooling you with a product called “Term Insurance”, where you are “investing” premiums to get nothing at the end.

Let me now tell why this happens and some give you some insight on this matter.

I have already talked earlier in my last post “Life Insurance and how to go about it”, about Term Insurance. Let me now take more deep dive into it and talk about the reasoning part.

I will first talk about fundamentals of Insurance and then talk about Endowment Policies and why are they popular, and what people don’t realize about them. and how Term insurance is the right thing for most of the people.

Basics of Life Insurance

What happens in a average family :

There is someone who earns and his family comprises of wife, kids, parents. if not all there is a subset of these family members. The head of the family earns and his family lives happily. All the expenses are met from the earnings of this main member, most of the time the husband. Now consider this person dies in an accident or for that matter because of any event.

What happens?

What happens to his family members other than the psychological trauma. If they don’t have money to take care for them selves, either some one from family have to take up the job and start working which may not be possible for them, or They have to decrease their standard of life to maintain the expenses.

They are now totally unsecured from future’s point of view. In short they are totally messed up, which should not have happened. I gave this detailed explanation for the circumstances because i wanted you to understand how bad can happen and proper measures must be taken care for this.

What is the Solution?

Adequate Coverage !!! this cant be compromised… You must have a backup plan which can give your family the same kind of income which confirms that they are not short of money in case the main earner is gone. If there are some debts like Home Loan, or any other tasks which need money apart from regular income, the cover must be good enough to cover that too..

For example :

Robert has a family expenses of 25,000 per month and there is a Home loan of Rs.25 lacs to be paid within 10 yrs. He is 27 yrs old. He has a wife, 2 kids and parents. All of them are dependent on him financially. He has investments of 5 lacs. Now in this case. In case he dies, who will take care of Home loan, how will provide them enough money to live life comfortably. They need 25k * 12 = 3 lacs per year.

Which they can get per month if they have 35-40 Lacs of money. If they put this in bank, they will get Rs.25,000 per month as interest which they can use. Considering inflation it will not be enough after some years, but lets leave it now for this example.

Add home loan of 25 lacs to this 40 lacs and what we come to know is that this family must be covered with minimum Rs 65 lacs . Rs 75-80 Lacs is a decent cover for this family. Now if he takes a cover of 80 lacs for his family, from that day he can happily live all his life without any tension , thinking what will happen if he is not there.

He will be attain peace of mind , and not be worried for it.

He must get a lot of internal peace because his Family is protected with a good enough cover to take care for them. And this is what you get in “return” from Insurance. No monitory return can give you more satisfaction than peace of mind.

So before doing anything else, his first step is to give adequate cover to his family and that’s the most important responsibility for him as a Husband, Father, Son. He must understand that this is not an investment for monitory benefit later in his life, but its for his family happiness and future.

Life insurance under MWP act is also one of the better option for married man. One point to remember and not forget is that this is the minimum cover required for family and anything less than this will be taking risk with family future.

Endowment or Money back Policies

Lets discuss the problems with these plans with respect to the above example.

High Premium : For an 80 lacs cover for say 30 yrs, the premium payable will be At least 2-2.5 lacs/year (this is a conservative figure). So now premium so high is not possible for anyone like Robert, so what they do?

They go with a kind of cover for which they can pay premium easily, can then they take cover for 5 lacs, 10 lacs or maximum 20 lacs. And guess who suffers in case of his death : HIS LOVED ONE’s.

It might also happen that they are compromising on a lot of small things which are important at that moment in time, like buying a bike for son, which they cant buy because of the insurance they have to premium, or some vacation they could have gone to with family, but compromise on that because of premium.

Money back at the end of the maturity is like a penny after so many years :

This is some thing most of the people overlook. They just see the numbers, 5 lacs 10 lacs or 20 lacs. And at the time of taking Insurance it looks good figure to them, because they see numbers, they dont see its value after many years, They don’t consider Inflation into account.

In case of above example, if Robert takes a cover of 15 lacs by money back policy, what happens if he survives the tenure. He gets 15 lacs at the end, Great Money after 30 yrs. Isn’t !!!

Lets see how great this money is? His monthly expenses will grow from 25,000 per month to 1.5 lacs per month (considering inflation of 6%). Now this money will help him survive for not more than 10 months … For so many years he pays high premium each year, just to get back money to cover his 10 months monthly expenses? What the hell !!!

Under Insurance :

Because of the fact that people want money back on survival and because of high premium, people end up taking policy for which they have to pay premium under there budget, which means less cover.

Without realizing the fact that they are highly under insured, the reason for this is that they see Insurance as investment product and not a protection cover for there family. When they die, there family get the money from Insurance company, but most of the time its not enough for them and it erodes very soon.

Term Insurance Policies

Lets discuss the features of Term Policies with respect to above example.

Cheap Premium : The premium is very low for Term insurance Policies. For above example. The yearly premium for Rs.75 lacs cover for 25 yrs is just Rs.20,000 yearly or just 1,600 per month !!! .

This is in any way affordable for most of the people. Its providing the fundamental requirement of Good cover and low premium and if you think of returns, Good cover and low premium can themselves be seen as good enough return. You family protection at low cost is the return you get.

Watch this video to learn more about Term insurance and it’s benefits :

Opportunity to invest rest of the money in High return Investments :

With term Insurance you save a lot of money in premium and now you can invest this money as per your wish in high return instruments, anyways in Endowment policies you put money for long term and you get it after so long time. So you can now always put your saved money in things which are long term investment products and return great returns.

One of those things is Equity Diversified Mutual funds and Direct Equity (depending on persons ability and interest). In long term Equity Diversified gives fabulous returns (15-20 yrs) and the risk is minimized because of long term.

And if you consider India growth story , it looks great in long term , hence Equities for long term is the most obvious choice. They will give you return of 15%+ CAGR. (15-20 yrs)

Also it will be flexible , you can not invest for a year or two, if you want to use the money for your family vacation or some important event.

Conclusion :

Insurance is not an investment product, its a Protection instrument for your Family or any one your want to cover. There are other products for your investments.

Let your finances be the way you want your life to be , SIMPLE !!!

Don’t mix Insurance and Investments. There are products like ULIPS(What are ULIPS) and Endowment or Money Back policies which never excited me. They complicate things, confuse people. They can be good if you understand how to make most out of it, but it require knowledge and expertise. They offer some flexibilities, but still they are not worth it.

Read more on Term Insurance at my Old article. I would be happy to read your comments or disagreement on any topic. Please leave a comment.

Disclaimer: All the opinions are personal and shall be taken as knowledge sharing and not as encouragement

Finally many people like me have chance to take take plunge in the rising and booming Real estate sector , Any one who does not have Crores and Lacs to invest in flats , plots etc , to earn the capital appreciation will to be able to invest even small amounts like 5,000 or 10,000.

What are Real Estate Mutual Funds ?

They are simple close ended mutual funds which will invest in Real-estate , as simple as that … The lock in period will be 3 yrs. These REMF will invest in properties and they will be owners of those properties , they will also rent out these properties and pass on the rents to the investors as dividend. And when the mutual fund matures , it sells its holdings and pay us the returns.

REMF’s will be listed on Stock Exchanges and they will be traded just like shares.

How do they work exactly ?

Lets take simple example :

You invest Rs 20,000 in some ABC REMF and one unit costs Rs 10 at the start , so you get 2000 units. many people like you will also invest and Suppose the total money they get from investors in 10 crores. Now they invest this money as per the laws defined for them. Suppose they receive 50 lacs as rental income from their investments in a year and the total investments has grown to 12 crores (because of rise in value of properties and other factors).

From this 50 lacs they will distribute dividend and you will recieve your share for 2000 units and the unit value will be around Rs 12.

Rules and Restrictions for REMF’s

– They will have to invest atleast 35% in completed projects , ready flats , shops , houses etc.

– At least 75% should be invested in real estate and related Securities.

– They can partner with real estate developers and invest maximum of 15% in the project (not in company).

– The NAV will be published on daily basis.

– Most probably they will be in category of debt funds. Tax treatment not clear at the moment.

– Further caps will be imposed on the fund on investments in a single city, project or securities issued by associate companies and sponsors. Funds are not allowed to invest in assets owned by the sponsor or the asset management company or any of its associates during the last five years the aforesaid entities hold tenancy or lease rights.

– The cities for investment by real estate mutual funds would include 35 cities in million-plus urban agglomerates and 27 under the million-plus category as per the Census 2001

They are still to be launched , keep a watch !!!

I would be happy to read your comments or disagreement on any topic. Please leave a comment.

ULIPS are investment cum insurance products, You take an insurance worth XYZ amount and then you pay some premium every year. Out of your premiums some amount is cut as administrative expenses (Premium allocation) and out of rest the mortality charges are cut for your insurance and the rest is invested in market linked things.

Some important points about ULIPS to note here :

1. You decide the tenure of your Insurance and the insurance amount, depending on which mortality charges are cut from your premium you pay.

2. The Premium allocation charges are very high in initial years (especially 1st year) and then reduces in later years. That’s the reason one should be invested in ULIP for long period to get maximum benefit.

3. The investor can switch between the investment style as and when he wants (max 4 free switches in most of the cases, there after some nominal fees).

4. ULIPS must be considered for long term investment products, so that the high cost in initial years are averaged out over longer period.

Advantages of buying ULIPS :

– The switching over different styles is not costly, you are not charged when you switch, which make them flexible.

– ULIPS are innovative products and suits people who want long term wealth creation with some insurance too..

Disadvantages of buying ULIPS :

– They are not good product for people who require high cover and can pay less cover, because premium depends on the cover. Higher the cover, higher the premium. So these people must take term insurance for there life insurance.

– For people investing only for tax benefit must avoid them as they will prove to be costly in short term because of there high allocation charges.

5 Benefits of investing in ULIPS

1. Tax benefit

ULIPS have sec 80C benefit, but for that you have to pay minimum of 3 years premiums to avail this tax benefit. You can not stop ULIPS before 3 years to get tax saving benefit. You will get the tax benefits at 3 different stages –

Entry level: You will get tax exemption on the premiums you are paying for ULIPS

Switch advantage: You don’t need to pay any taxes if you switch the policy from equity to debt or vice versa.

Exit level: The amount you will be getting after maturity period will also be completely tax free.

2. Goal based investing or planning

ULIPS also helps your to secure your future goals like retirement planning, wealth creation or your child’s education planning.

3. Freedom to choose your cover

You can choose the cover for your policy. In most of the insurance companies, the cover provided is 10 times your premium, however some of the insurance companies are providing the insurance covers of upto 40 times of your premiums.

4. Liquidity

ULIPS also provides you the benefit of partial withdrawal which will help you in case of emergency.

5. Option to choose your investment type

The money actually invested is invested as per your directions … ULIPS have different plans with different risk-return profile. One plan may have allocation of 80-20 to equity and debt, some other can have 50-50 and some can have 20-80 and like this.

ULIPS have become very popular in last some years as agents have put there life and souls in advertising them and making people believe that they are wonderful product. Every product is wonderful for some or the other. If you can take good risk , need less insurance and closely want to monitor markets and economy so that you can switch your investments from one plan to other, ULIPS are great for you … else they are not..

Evaluate yourself and dive 😉

I would be happy to read your comments or disagreement on any topic. Please leave a comment.

What is Financial Planning? Its a little stupid definition, but its just planning you finances. You plan your Investments in such a way which meets your financial goals over time.

You must be very disciplined when you do this, you must know from where you the money is going to come to you and how are you going to save or invest it, and in future how are you going to achieve your goals.

Steps in Financial Planning

1. List down your Goals

Prepare a list of financial goals. It can be any requirement like Buying Home, Car, Child Education, Child Marriage, Vacation, Retirement etc. Along with this there must be a very clear timeline associated with the Goal. Something like “I want to buy a Car after 3 years, which will cost 10 Lacs at that time”.

2. List down Your Cash Flows

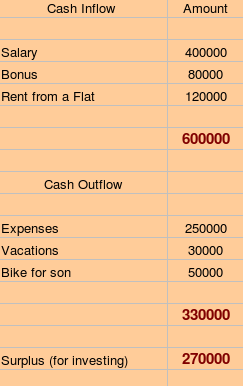

Prepare the list of your cash flows, cash flow means, how money is coming and going? Any money coming in is Cash inflow and Any Expenses is Cash outflow.

It it help you understand how money is coming to you and how is is utilized and how much is remaining for investing purpose.

Example (yearly) :

By Doing this , you can get very clear of how you are going to get money and how you are going to spend it, and how much you are left with to spend.

3. Understand and figure out your Risk-appetite

This is a very important part of financial Planning, Risk appetite is the amount of risk a person can take while investing. How much money you can afford to loose in order to earn high returns defines your risk taking ability.

For Example:

If you are ready to loose 60% of your money , your risk appetite is high

When you are ready to loose 25% of your money , your risk appetite is moderate

If not at all ready to loose your money even 1% , you are not at all a risk taker.

It depends on you which category you belong in. it depends on individuals Psychology, Family Conditions, Attitude etc.

Generally people in there early age have more risk appetite as they have less responsibilities and more freedom to invest. Later when they get married and have responsibilities, they cant risk money to loose.

4. List down your Financial Goals

At this point, you must be clear with your goals. Financial goals are the list of things for which you need money and you must have a predefined target time.

Example:

Ajay earns Rs 3,00,000 per year with Rs 1,00,000 left for investment, he has moderate risk appetite.

Goals:

1. Buy a Car within 2 years worth 5 lacs.

2. Vacations in New Zealand worth 8 Lacs within 4 yrs.

3. Buy home worth 40 lacs in 10 years.

Here, Goals are not compatible with amount invested per year and with that kind of risk-appetite.

Therefore, Goals must be realistic and achievable, it must not look totally irrelevant.

Watch this video to know the financial planning services by Jagoinvestor :

5. Make sure your Goals are realistic

At this point you must make sure that your goals do not look unrealistic and unachievable. If they do, then you must either lower your goals or increase risk appetite or increase the investible amount per year. This gist of the matter is, Be Realistic !!!

6. Make the Plan

Once you are done with all these steps, Its the time for the planning.

But for a short term goal like vacation in 1-2 yrs, don’t invest in equities, rather go for a debt fund or a fixed deposit.

In this way, you have to be clear how you are going to invest for achieving your goals.

7. Review and Take advice

Revise your steps and make sure everything is correct. If you are unclear about anything meet some one who is more knowledgeable than you, See a financial planner or a knowledgeable friend.

8. Take Action and keep Reviewing

The last step is to take Action and start executing the plan with discipline and make sure you change you goals, risk appetite as time passes and these things change over time.

I would be happy to read your comments or disagreement on any topic. Please leave a comment.

Do you remember the price of a movie ticket or any or your favorite thing few years back? It is the same today also? I don’t think so. It has increased by some numbers. This increase in the price is known as inflation. In this article I’m going to tell you what is inflation and how it can affect your investment.

Inflation :

Inflation is the increase in the rate of prices caused because of devaluation of the currency. Is is also known as the decrease in purchasing power of the currency.

Its a tool to measure the increase in prices. If inflation is 6%, it means on an average the prices have increased by 6%, means anything which had cost of Rs.100 last year will cost 106 this year. (Its a average price and not exclusively for some item)

For example:

Considering inflation at 6%, the value of Rs.100 will go down to Rs.53.86 in 10 yrs and to 29.01 in 20 yrs. In order to keep value of you money same, the absolute return earned must be greater then inflation.

Inflation vs returns on different financial products

Fixed Deposit :

Investing in Fixed Deposits just retains its value, but people feel that they get good returns upto 8.5 or 9.0%.

There is a tax of 3.5% on your FD returns and then if you adjust inflation of 6% after that, you will realize that though your Rs.100 has become 109 in a year, you have to pay 3 or 3.5 tax on that, and then if you have Rs.106 after that, you can purchase the same thing which you could have purchased in Rs.100 a year ago.

Hence, FD don’t give returns in real sense, they just keep your buying power. (considering inflation + tax = return from FD)

Gold investment :

Investing in GOLD is considered the traditional way of investment and also it is consider as the best way to beat inflation. Historically Gold has always outperformed inflation. It has generated 13.66% annualized return since 15 years, which is almost double of the inflation rate.

See the graph given below, in this graph the returns of gold investment since 20 years is given. You can see that how gold prices have moved or increased in last 2o years.

Image source: www.Bemoneyaware.com

Cash in bank :

The worst thing one can do is to keep Cash in Bank account, instead of investing it in any product. The returns generated from this saving can not beat the inflation rate.

For example: Suppose you have some cash in your savings account on which the interest rate applicable is around 4-4.5%, whereas the inflation is around 6%. Here the returns can not even meet inflation rate.

Cash must only be kept to a limit which may fulfill your emergency needs (preferably 3 times of you salary). Any extra amount must be invested.

Mutual fund :

Mutual fund is an investment in stocks so the returns are volatile here but if you consider it as a long term investment product then you will realize that it has given returns way higher and beat the inflation rate by almost double.

So this is the difference between the inflation rate and the returns of different financial or investment products. Now you can compare the returns and choose which product is suitable for you to invest in.

We can help you to improve your portfolio by making a perfect financial planning for you. If you have any doubt or query you can ask us by simply leaving your concern in our comment section.

People give 100% time to there work, but not even 1% for the motive behind the hard work they put, which is to generate long term wealth, for buying home, children education.

I have seen people who earn well, but fail to invest it properly, in fact in a wrong way, and hence they loose on that. Whats the use of working so hard if you cant invest it properly to achieve you goals, Is there any use of your working for so many years, and after all we work for money, and if we cant manage that money or don’t take some serious time to manage it, I personally consider it as waste.

One of my friend has taken a ULIP policy to save tax without knowing what it is. The insurance he gets on that ULIP is 1.25 lacs with yearly premium of 25,000 with health insurance premium of 4.5k.

he didn’t pay any attention to what he is buying, Does he really need it, how is it going to be beneficial to him.

One of my other friend took a Endowment policy with insurance of 10 lacs for 15 years with premium of around 90,000, when i asked her, how many financial dependents she had, she was clueless and when I cleared what i am asking she said, “No one”.

People don’t take any interest in knowing/learning/asking about financial instruments from anyone and take idiotic decisions, loosing there hard earned money. It does not take 1 hr / week or 4 hrs/month or 1 day / year to take fair decision (if not best) regarding your finances.

If people start giving 1% time to there investments and finances and 99% to there work compared to 100% time to work, they can do much better. A person earning 20,000 per month can generate more wealth than a person earning 50,000/month, with better investment technique.

“Money does not grow just by investing more, but disciplined and great investing technique.”

What do you think is the biggest reason for people in India for not taking financial planning serious?

SIP is a way of investing in Mutual Funds where you pay a fixed amount each month for a fixed tenure.

Like If you take an SIP of 5,000 for 1 year on Jan 1, 2008, you will be paying Rs 5,000 per month for next 12 months.

Please understand that its not a financial instrument, but a way of investing in mutual funds, some people confuse SIP with PPF, NSC, and mutual funds, they think they can invest in “SIP”, its just a mode of investment.

SIP CALCULATOR :

When to invest in mutual funds through SIP?

Investment through SIP must be done only when markets are uncertain or very volatile, when you don’t know which side they are headed to ..

SIP will be beneficial only if markets really are volatile or going down after you invested. If it happens that markets turns bullish and starts going up, in that case SIP will not be beneficial and will give less return compared to lumpsum investment in start.

SIP is a simple concept and hence very powerful, lets see some reasons why its worth investing through SIP

Reasons to invest through SIP in Mutual Funds?

More convenient for average person on wallet

Its more easy for a person to invest in small amount every month, rather than a lump sum amount. Investing through SIP is lighter on wallet. Its easy to pay Rs 5,000 per month for 1 years, rather than investing 60,000 at a same time.

It brings your average cost price for unit down (in volatile market)

The biggest advantage of SIP is this part, There is a concept of rupee-cost averaging, In SIP you buy less when market and NAV are UP and you get more units when they are low. When this happens, the average cost of per unit is lower.

Lets take an example of “Ajay” who invests 1,000 per month through SIP starting Jan 2, 2007.

How SIP helps in this case ? See the result below :

ADVANTAGES of SIP

Makes you a disciplined Investor

The other advantage of SIP is that it makes you a disciplined investor. Once you start SIP, each month you have to contribute certain money in mutual fund and that habit is cultivated.

DISADVANTAGES OF SIP :

It will not work in bullish markets or when market goes up over time

When market goes up and keeps growing over time, the units bought every time will be at high price then the previous one, which will ultimately bring the average cost up , compared to the lump sum investment at the start.

In case of tax saving fund, the lock in period gets extended for every investment.

Tax saver mutual funds lock your money for 3 yrs, When you invest through SIP, each of your investment is locked separately for 3 yrs from the date of investment. So if you pay your first installment on Jan 2007, it will locked till Jan 1 2010, then the installment paid on Feb 1, 2007 will be locked till Feb 1, 2010 and like this each installment will be locked with the gap of 1 month.

In which type of markets do you think SIP will not work?

If you have any query related to this topic you can leave your reply in the comment section.