JagoInvestor.com recently completed its 3 yrs in Nov 2010 and following is the interview taken by one of the fellow bloggers .

Yet another milestone for Manish Chauhan, founder of JagoInvestor.com. It’s been three years since Manish started blogging and on Nov 5th 2010, JagoInvestor.com celebrated it’s third anniversary. After three years of run up, JagoInvestor.com boasts of a massive 6500 RSS followers which is still growing and a treasure-house of articles where you can find almost anything on personal finance. On this occasion, here are some snippets of a tete-a-tete I had with Manish on his journey over the last three years and his vision for JagoInvestor.

Q1) Which is your best personal finance book and why ?

I have not read any book on personal finance nor I am aware of any pure personal finance book which gives a good idea of everything on personal finance at this point in India. However there is enough material on Internet and loads of good websites and blogs which gives great education on personal finance.

More than knowledge, Personal finance is about attitude and applying common sense in area of personal finance. There are few things which a person has to understand and on top of it he himself can build all the knowledge and analyze things . Incase some one has any idea about personal finance books in India , please give the names in comments section !

Q2) What is your vision for JagoInvestor in the next 5 to 10 years ?

Personal Finance is a huge area with opportunity. I see JagoInvestor being synonymous with “Financial Literacy” and “Psychology changing website” which along with providing personal finance knowledge also provides counseling in the area of personal finance, I want to build a program which would span over few months or may be 1-2 yrs which if any one who is interested in financial freedom can join and they can totally transform their way of looking at personal finance. The program can turn a novice into a pro in area of personal finance. (Would like to read comments from readers on this point)

Overall JagoInvestor’s main motto is to “change investors relationship with money” over time.

Q3) You did you manage running a personal finance blog despite being from a different background ?

There is Chinese proverb, “start doing what you truly love and you will never have to do any work !”. Common sense has no background and I consider personal finance as pure common sense fueled with a passion to change one’s financial life. As I like number crunching and I consider myself a logical person, I started a blog one fine day without realizing that it would become this big today, readers liked it and it was making difference in their life, which motivated me to work hard and make sure I keep running this movement of financial freedom.

Q4) What would be your top three advice for investors ?

Top 3 advice I can suggest some one is

Start investing time to understand how important personal finance is in one’s life, thats one thing we work for and our quality of life depends on.

Take pain of cross-checking each and every aspect promised by products, like investors in endowment plans should calculate what is the return they are getting and how 1% more return can impact their wealth in long run.

Shift from free advice to paid services and value them, paid does not mean costly, if you get more value than what you pay, thats even cheaper than FREE. This mind set of getting FREE FREE FREE in each and every aspect of life actually turns out to be very costly in long run.

Q5) Top 3 urgent changes required in the personal finance space ?

a) Shift from sales driven attitude to value-based model in selling : When even you get a call about some product, all you hear is how great the product is, how much return it gives and blah blah.. all the focus is on the sales and even the conversation you hear is driven by sales. The biggest change which should happen is the whole model should be based on how the product will help customers in achieving their goals, a client buys a product because it helps them in life, not because its GREAT.

b) Training to agents and IFA’s : There is good number of magazines/portal for investors to help them in taking informed decisions, however I don’t see anything which helps agents and other IFA’s/CFP’s to understand how they should change their strategy in acquiring clients and giving value service to them. We need some services like these.

c) Basic Financial Planning for each Indian : While financial planning is a detailed thing in general, each person should have access to cheap basic planning for their life goals such as child education and retirement at least. There has to be a model which gives them inexpensive plan for their most basic goals in life.

Thanks to all the readers of Jagoinvestor for giving me an opportunity along with them to create this platform for learning personal finance.

Comments

Would like to hear your comments on how do you feel associated with jagoinvestor and what changes has happened in your financial life ?

Are you confused about many things when it comes to Health Insurance in India ? Are you afraid of rules and regulation in Mediclaim policies ? Don’t you have a clear idea about how will you deal with various things in Health Insurance and delaying your decision of taking a Health Policy ?

Today we will look at most frequently asked questions in Health Insurance try to answer those questions.

1. Can a person get claim from his own company and spouse company if they are covered under both companies ?

Yes, if both husband and wife are covered from their employer, they can claim from insurance provided to them by both the companies.

For e.g. if husband is covered for 1 lac under group insurance policy from his company (and her spouse is also covered under her husband company policy), and the same situation exists vice versa, both of them are then, actually covered for 2 lacs each; 1 lac from their company and 1 lac from their spouse’s company.

Now if something happens and husband gets hospitalized and expenses are 1.8 lacs, then husband can make a claim of 1 lacs from any one of the company and remaining 80k from other company. If you have cashless facility then you just show both health cards. If you don’t, you can get reimbursed by insurance company.

One important point worth noting is that during reimbursement, one should apply for the reimbursement first to his parent company and then to the one of his spouse. See some hidden health insurance policies

2. Do we have to notify the company about any illness or habit developed in between?

No, we are not required to notify the company regarding any complication or health issue. If the policyholder is hospitalized, the company will automatically come to know of it. Otherwise, no need to inform the company about any such policy.

If you notify the company, your premium for year after notification will increase, if it is under their list of illness to be checked. If you don’t notify the company and when you go for a claim, they will come to know that it was developed earlier and the claim will be settled accordingly and from next year onwards they might put loading on it (All these reasons vary from company to company).

So whether you tell them or not, it’s the same thing. They have doctors panels with whom they check your details before giving you the claim.

3. Does Health Insurance cover everything from accident, surgery, normal hospitalization ?

Yes, Health Insurance covers you for everything, provided you were hospitalized, be it for any reason; due to accident, illness, or disease. If someone met with an accident and he is hospitalized, then his mediclaim policy will pay for his bills, no exceptions.

Watch this video to know what are the things to look for while choosing a health insurance plan:

4. What are the advantages of sticking to one Health Insurance company for a long time ?

The plus point of sticking with one company is that if someone is suffering from any pre-existing disease at the time of commencement of policy, those complications will be covered after 4 years. Until portability is introduced in India, this is the single biggest advantage to stick with one company for long.

Another advantage is that when you have a continued policy from any insurance company, after few years you get bonus or discount in premium.

For example: Suppose you have a policy of 3 lacs and you are with the same insurer for past 4 years you can get a bonus of 50% i.e. you pay premium for 3 lac only but you get coverage of 4.5 lacs. Similarly some companies don’t offer bonus but they offer discount in premium i.e. for coverage amount of 3 lacs you pay lesser premium than actual amount.

So if you don’t have any serious problems with the insurance company then it is better to stick to one company.

5. Can NRI’s take health insurance? Can they travel to India for treatment and claim? What about emergency situations ?

Yes NRI’s can take Health insurance in India. They can definitely travel to India for treatment and can claim it. however they will have to show their residence proof, ITR and a few other documents. If they don’t have those documents, then they are not eligible to get insured in India.

The cost of treatment in India is different and cheaper than countries like USA, UK and other European countries. The premium amount computed depends on Indian conditions and parameters. So if a NRI has health insurance form Indian company, that person would be paying premium as per India actuaries and obviously cost of treatment in his residing country would be higher than India.

For example:

If a person get dengue and he is very critical and requires urgent hospitalization, the cost of treatment in India would come up to 1-2 lacs (and this is on higher side.) The same treatment would cost around 10-15 thousand dollars in US so this burns a hole in insurance companies’ pocket.

6. How to claim successfully in case of emergency and planned hospitalization?

The most basic fundamental for a smooth claim process is keeping all your documents up to date. If you have a past history of illness, make sure that you submit those documents too, because the TPA department will come to know whether it’s a pre-existing disease or not.

While submitting your documents make sure that all the documents are proper and there is no missing document pertaining to your illness. This will just give a chance to TPAs to make excuses and you will have to run for your money.

It’s worth noting that in case of planned hospitalization, if you inform your mediclaim company in advance and take prior authorization, everything will be settled by the mediclaim company or TPA, without the policyholder been required to submit any document.

7. Is it better to take accidental policy separately or mix it with term insurance as a rider?

If your accidental policy is a rider with some Term insurance (9 most asked questions about Term Insurance) then you must take care that it covers everything what accidental policy should cover. Generally when a policy is offered as a rider it does not cover each and every aspect.

For example: An accidental policy offers insurance against partial disablement, loss of limbs, hands and many other parts. But in a rider, many insurance company offers insurance against permanent disablement only and not for partial disablement and loss of body parts.

Also note that, because accidental rider is much less if taken with Term Plan as compared to the personal accidental policy taken stand alone. Under term plan, accidental death benefit could be taken for as little as Rs.1000 for a cover of upto 15 lakhs where as in a stand alone policy the same amount will be available for a premium of around Rs.2000. So it depends.

8. What are the top most things one should check in the policy documents ?

The first thing one should have a look at, is to check what the exclusions in the policy are. This is because, we get information on what is covered but no insurance company will give information on what is not covered and this creates a problem at the time of claims. So to avoid any surprises, one should have a thorough look at exclusions as well.

For example: A new circular was passed by many insurance companies few months ago in which they provided only Rs.20-24 thousand (different companies had different rates) compensation for cataract operation. Earlier there was no limit on it.

So sometimes in list of coverage for health insurance we just read the tabular format given by companies but don’t go inside to see the details and this can land us in soup sometimes. Many insurance companies now provide Maternity benefits but they limit it to coverage of only Rs.20-30 thousand, we just see that maternity benefits are given but sometimes fail to notice how much coverage is given.

9. If there are no loading charges, can premium still change on renewal?

This is a very big question with very easy answer..If you check the premium structure of any of the mediclaim company, either there premium is increasing every year or they have premium slab for different age groups; something like for age 30-35 premium is 4200 and from age 36-40 its 6700.

So under this second policy, when the policy holder moves from age 35 to 36, his premium suddenly jumps by Rs.2500 and this is not loading.

So yes, premium can/will increase irrespective of loading after certain age.

10. Is it a good idea to split health insurance into 2 policies? Tips?

No logic for doing this except personal preference. If you are taking another mediclaim policy just to increase your cover, why not get your cover amount enhanced in the existing policy/company.

Get another mediclaim policy only if certain other company is offering feature/features which your existing policy does not and you have surplus funds at your end to afford 2 separate mediclaim policies at a time. No other reason to, otherwise.

11 . During the course of my treatment, can I change the hospitals?

Yes it is possible to shift to another hospital for reasons of requirement, of better medical procedure. However, this will be evaluated by the TPA on the merits of the case and as per policy terms and conditions. Note that it would be prudent if you check the network hospital list and go to the best hospital in the beginning itself rather than changing midway.

12. What are the situations under which one may be denied cashless hospitalization?

If there is any doubt in the coverage of treatment of present ailment under the Policy if the information sent to TPA is insufficient to confirm coverage

When the ailment/condition is not being covered under the policy.

If the request for pre-authorization is not received by TPA in time. In such a situation, the Insured can take the treatment, pay for the treatment to the hospital and after discharge, send the claim to TPA for processing.

In case the hospital in not on the panel of the company or the disease/illness is pre-existing and not covered for 4 years.

13. Whom can I approach in case of a conflict with insurance company with regards to my claims?

The Grievance Redressal Cell of the Insurance Regulatory and Development Authority (IRDA) looks into complaints from policyholders. Complaints against Life and Non-life insurers are handled separately. This Cell plays a facilitative role by taking up complaints with the respective insurers.

Policyholders who have complaints against insurers are required to first approach the Grievance/ Customer Complaints Cell of the concerned insurer. If they do not receive a response from insurer(s) within a reasonable period of time or are dissatisfied with the response of the company, they may approach the Grievance Cell of the IRDA.

Private Insurers:

Shri K.Srinivas, Asst. Director,

Insurance Regulatory and Development Authority

Consumer Affairs Department

United India Tower, 9th floor, 3-5-817/818,

Basheerbagh, Hyderabad – 500 029.

E-mail ids: [email protected]

Public Sector Insurers:

Mr.R.Srinivasan, Officer on Special Duty

Insurance Regulatory and Development Authority

Consumer Affairs Department

United India Tower, 9th floor, 3-5-817/818,

Basheerbagh, Hyderabad – 500 029.

E-mail ids: [email protected] . As claims/policy contracts in dispute require adjudication and the IRDA does not carry out any adjudication, insured’s are advised to approach the available quasi-judicial or judicial channels, i.e., the Insurance Ombudsmen, Consumer for or the Civil courts for such complaints.

The list of Insurance Ombudsmen along with their contact details are available on this website under the heading ‘Ombudsmen

Here is the link

If you have a good broker from whom you have purchased the policy, then they will help you in coordinating with health insurance companies.

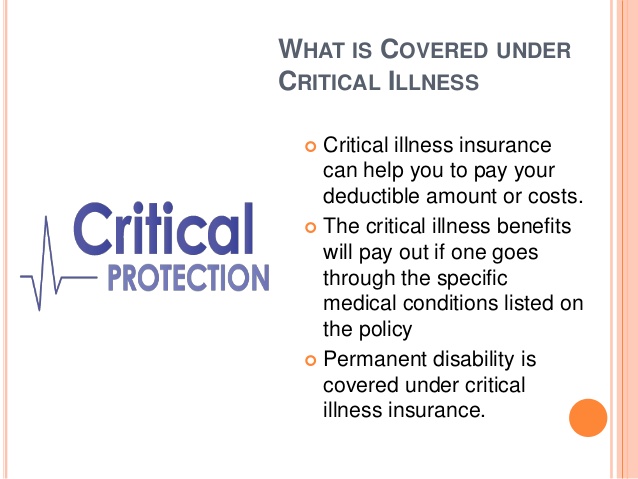

14. What is the difference between Critical illness insurance and normal health insurance ?

In a critical illness policy you are covered for certain mentioned critical illnesses only. Some of coverage’s are Kidney disease, brain tumor, and major organ transplant and many more depending on the companies.

If you have normal health insurance you will definitely get covered for critical illness but in critical illness you won’t get coverage for normal disease like malaria, typhoid.

For example: If your age is 25 and you buy normal health insurance from any XYZ company and let say its premium is Rs.3000 for cover of 3 lacs but if you buy critical illness policy for 3 lacs the premium would be less because considering your age the changes of you getting a critical illness is lesser than any normal disease.

Similarly for old age person the premium for critical illness insurance will be more than normal health insurance because chances of getting that critical disease are more at older age. One other option would be to avail critical illness rider in term plan itself.

15. What is the benefit of critical illness policy?

So as you grow older it is advisable to have another critical illness policy along with normal health insurance. So those at old age when undergo major operation or transplant, this critical illness policy can be used and for minor disease normal health insurance is used.

Image source: Slideshare.net

The reason for this is e.g. if you have normal health insurance of 5 lacs and you undergo tumor surgery with other complications and the expenses are around 4 lacs and after sometime you get hospitalized because of ill-health then you have nothing left in your health insurance.

16. What is Domiciliary Hospitalization?

Domiciliary Hospitalization means medical treatment for a period exceeding three days for such illness/disease/injury which in the normal course would require care and treatment at a Hospital/Nursing Home but actually taken whilst confined at home in India under any of the following circumstances, namely:

i) The condition of the patient is such that he/she cannot be removed to the Hospital/Nursing Home or

ii) The patient cannot be removed to Hospital/Nursing Home for lack of accommodation therein

For smooth claim process, just take care that all your documents are in place and to be on a safer side have a report from your family doctor, stating that this person cannot move to nursing home/hospital due to such and such reasons.

It just provides the proof and makes the process simpler. Note that every company does not offer this facility, you should check your policy document.

17. Some important exclusion under health insurance policy.

1 Pre-existing diseases i.e. Any condition, ailment or injury or related condition(s) for which insured person had signs or symptoms and/or was diagnosed and/or received medical advice/treatment within 48 months prior to his/her health policy with the company.

Pre-existing diseases will be covered after a maximum of four years since the inception of the policy

2. Any disease contracted during the first 30 days of inception of policy except in case of injury arising out of accident

3. Certain diseases such as cataract, piles, hernia, and sinusitis etc. are excluded for specified periods if contracted or manifested during the currency of the policy.

4. Injury or Diseases directly or indirectly attributable to War, Invasion, Act of Foreign Enemy, War like operations.

5. Cosmetic, aesthetic treatment unless arising out of accident.

6. Cost of spectacles, contact lenses and hearing aids

7. Dental treatment or surgery of any kind unless requiring hospitalization

8. Charges incurred at Hospital or Nursing Home primarily for diagnostic, x-ray or laboratory examinations, without any treatment.

9. Naturopathy or other forms of local medication

10. Pregnancy & childbirth related diseases

11. Intentional self-injury / injury under influence of alcohol, drugs

12. Diseases such as HIV or AIDS

13. Expenses on vitamins and tonics unless forming part of treatment for disease or injury as certified by the attending physician.

14. Convalescence, general debility, run-down condition or test cure, congenital external diseases or defects or anomalies, sterility, venereal disease.

Do you have all your mutual funds investments in different companies and are looking for aggregating them at a common place? If so, there’s some good news for you. Now you can convert all your existing Mutual funds into demat form, which means that you can now have it electronically stored in your demat account, just like shares! Note, that once your mutual funds are in demat form, you can sell them either through stock broker platform (your demat account) or through the normal way of selling it through your Depository participant (like you do, right now.)

Advantages of converting your Mutual funds into demat form ?

1. Centralization : Once you convert mutual funds in demat form, you will then get just a single statement for your holdings. Right now, if you have investments in say 10 AMC’s, you must be getting statements from all those AMC’s. How to choose a good mutual fund

2. Monitoring : Once you have all your mutual funds at one place, you will be able to monitor them better, & you can see the performance at one go. Compare that to when they were at different places; we tend to be lazy to look at all of them and just keep ignoring them.

3. Fast transactions : : If you have all the mutual funds in demat form, you will be able to sell those mutual funds in stock markets whenever you need money. Mutual funds are now, tradable in stock markets, so you can buy and sell them in stock exchange in real-time. If you don’t have them in demat form, selling them would not be as convenient.

Steps to convert your Mutual funds into demat form

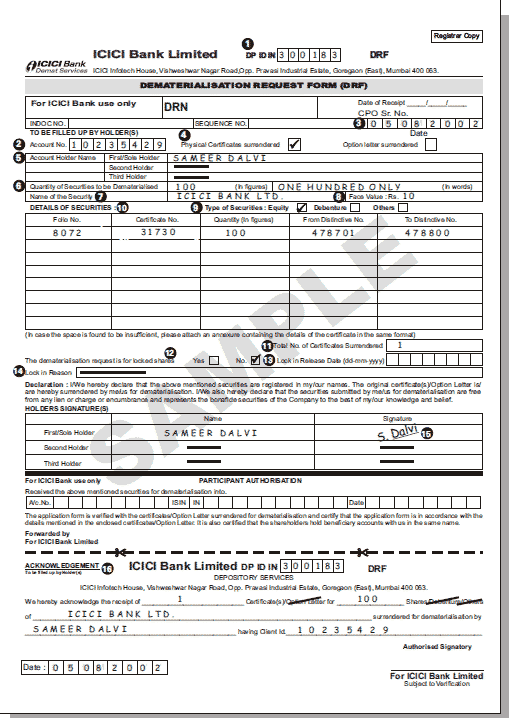

a) Obtain and sign DRF : The first step, is to ask your demat provider (like ICICIDirect, Sharekhan, Reliance Money) for a ‘Dematerialization Request Form’ (DRF) for conversion of mutual funds units held in physical form into demat form. Obtain it, duly fill it and sign it. You should be able to find the DRF form at your demat provider website. [DDET Click here to see a Sample DRF form][/DDET]

b) Sign all the statement of Accounts from your Mutual Funds : You will have to collect the statements from all the AMC’s which have the mutual funds names which you want to convert, once you have them, you have to sign it. You will get all these statements in your email box most probably. This step is important to make sure you have documentary proof that you own those mutual funds and have their names, so if you have investments in 5 different AMCs, you should collect all 5 statements.

c) Submit and Acknowledgement: Submit the duly filled and signed DRF along with and Account Statement issued by the Mutual Fund House to the Depository Participant. Acknowledgement will be given by the Depository Participant for the document acceptance, subject to verification.[DDET Click Here to see all Important points before submitting a Dematerialization Request]

1. The investor should check with their Depository participants (DPs) for the dematerialization Request Form to convert mutual funds units held in physical form into demat form.

2. The details in the DRF, i.e. Name(s), holding pattern and signature should match with the details as appearing in the account statement.

3. The form is duly filled and signed by all unit holders as per the holding nature and is complete in all aspects.

4. All the schemes as available in a folio are mentioned in the DRF and the unit balances as specified are matching with the closing balances available in the folio. No partial units or selected schemes available in the folio will be accepted for conversion.

5. Units requested for dematerialization should be should be free from credit hold, lien or any other hold. In case any units are under hold for want of credit status, conversion will be processed only after clearance of such hold.

6. Dematerialization request should not be submitted if the units are lien or locked for any Income Tax or other legal purpose.

7. Rejection letter will be sent by the Depository Participants if the documents are not in order, units are under lock, or rejected by the Registrar during the conversion process providing reason thereof.

8. Investors can check with their Depository Participant on the status of the request if no intimation has been received within twenty-one days.

9. No separate confirmation letter will be sent by the Registrar for successful transfer of physical units in demat form.

10. Post dematerialization of units the investors can only transact through the stock exchange platform. They will have to approach their broker for purchase / redemption of units.

11. Physical requests received by the Registrar of DSP BlackRock Mutual Fund for purchase/redemption of units will be rejected.

d) Processing : The Depository Participant will process the application for conversion of physical units into electronic form. For this, the DP would sent the request form and Statement of Account to the Asset Management Company (AMC) / Registrar and Transfer Agent (RTA).

e) Confirmation : The AMC / RTA will after due verification, confirm the conversion request sent by your DP and credit the mutual fund units in your demat account.

Selling Mutual funds in Demat form

Note that converting the mutual funds will require you to have a demat account first, so incase you don’t have a demat account , you will not be able to convert them , because unless you have a demat account, how can it be stored . Now once you have converted the mutual funds in demat form , you can sell them through your demat account in stock market , which would attract brokerage as per defined by your Depository participant, however you can also sell your mutual funds through the normal old way where you put a request for sell through a Redemption Form .

Conclusion

This is one of those simple and small steps, towards simplifying your financial life. Once you do this, it can motivate you to take further steps in automating many things which will improve your financial life. Dematerialization of mutual funds will make sure your documentation will improve . Let me know if you plan to do this on comments section .. also lets discuss if anything is not covered in article . Has anyone done this already ?

Last month we launched Questions Forum, which is a place where you can ask your personal finance doubts . There were some prizes which I am going to announce today . JagoInvestor Forum is a place where anyone can ask a personal finance question and get its answer within 24 hours from experts present there .

So if you have any doubts on your Insurance policy , Banking, Mutual-funds, stock market , tax related or any kind of money related query , feel free to ask it . JagoInvestor Forum has got great response in this last 1 month with more than 250 people asking 300 questions and with 1200 answers overall .

First Prize : The winner is Mr. Gopal Krishan Doda. He has been a great help in providing good answers and has answered more than 150 times. He wins a free one year subscription toMProfita desktop portfolio management software worth Rs. 1488.

Second Prize : The second Prize goes to Mr Naveen Arichwal for asking maximum questions. He wins the book on retirement Planning named “Retire Rich Invest” or any other book of choice .

Bonus Prizes : Jagadees and Rakesh (rakeshnwo ) , they also win the book “Retire Rich Invest” , or another book of their choice . They have also contributed well in answering the questions of others . Good job .

Free-Stuff to all Members of the Forum

As promised I also sent some free stuff to all the registered members of the forum. Here is the list of things I sent to them.

HouseHold Budget Spreadsheet to maintain your holdhold budget and see basic analysis

A research report on a Mid-cap Stock (Not made by me)

Do you want these free stuff ? I am planning to mail this to all the members who are subscribed to this blog in coming week , so if you are not yet registered on the blog you can register by putting your name and email on the subscription form on the right side sidebar or Click Here to directly go to the Subscribe Form

Note : Make sure you click on the subscription Link you get in your email after you fill in the information , Its required step to get subscribed

Win Prizes every month

You can now win every month! , You you heard it right . There will be total of 2 prizes every month from now onwards. Just ask a question on the forum for any personal finance related doubts and the question which gets the maximum number of comments will win the first prize. So make sure you ask an interesting questions which is of everybody’s interst and make the question very clear. Apart from this first prize , there will be a second prize for a member who will give the maximum number of good answers and helped other to solve their queries . I will choose the winner based on every month data . So every-month you can win prizes by asking your questions . Let me know how do you like this concept.

First Prize : The person who asks a question and gets the maximum number of comments wins a free one year subscription to MProfit– a desktop portfolio management software worth Rs. 1488.

Second Prize : The second prize would be the person who gives the maximum good answers and helps others in clearing their doubts . He wins a personalised Tshirt or a book of his choice worth Rs 500 .

I would like to hear back the feedback of readers on the forum , Is it useful ? What changes are required to make it a better community ?

Winners Please contact me for claiming the Prize 🙂

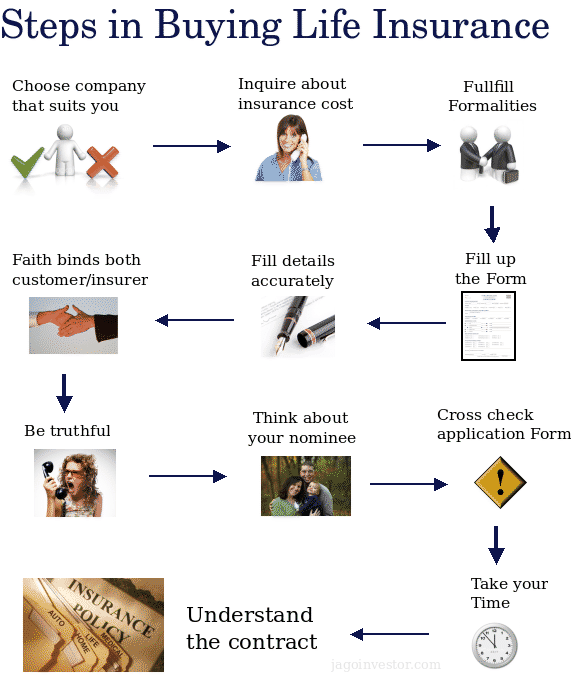

Have you already bought Life Insurance ? Though you might have done the sin of being underinsured, I would say its fine, because today we are going to look at detailed steps of buying Life Insurance and we will also learn a lot of things.

Almost everyone has his own set of doubts regarding Life Insurance contracts, but in this article we will not just look at detailed procedure of buying Life Insurance, but also see why most of the people have the doubts which they have. This is probably going to be the last article on Life Insurance you would need.

So here we go. Today for the savvy life insurance buyer, it is possible to buy the policy on the web – it saves money for sure.

Choose company that suits you

The first step in buying Term insurance is to shortlist the company from where you wish to buy the product. There are many companies in India selling life insurance and almost all of them have a Term cover available. Let us call them companies A to M.

Now let us say you like to deal only with A, D, F, G and H. Visit these companies’ websites and find out how much a term insurance for you costs. If you are 35 – look for a policy that will protect YOUR INCOME till the age of say 55 years (choosing age 65 will increase the premium) if your retirement age is 55.

However, if you think you will be earning till the age of 65 years, choose a 30-year plan.

Formalities to fulfill

If you are savvy and patient enough, you could fill up the form online – and a person will get in touch for the formalities. Or you could call up and ask for an agent. On an average the agent will not be very well qualified – but most of them will try to dissuade you from buying a term insurance.

Just say, ‘give me a term insurance form’. There will be other documentation like income proof (3 years IT return), one photograph, pan card etc.

#Filling the form

Next is the process of filling the form. This is one crucial thing that people are normally too lazy to do – so they delegate it to the agent. The life insurance form, the medical insurance form and the embarkation form when you are landing in the US or Israel should always be filled by you personally!

You know about yourself – not the agent whom you have just met. Many of them are worried that you will not be eligible to be insured. So in order to protect their commission (and to please you) will take short cuts, be careful.

#Fill details accurately

Every word, every column in the life insurance form is crucial – that is the reason why they are there in the form. All details should be accurately filled. Make sure that the name in your passport, pan card and the life insurance form are EXACTLY the same.

To the authorities K Balakrishnan is not the same as Balakrishnan Kumar. It may sound trivial, but let me assure you your nominee will not find it amusing.

Besides, check your height, weight (I have seen some agents argue with the doctor to show a few kilograms less and some doctors oblige!), number of cigarettes you smoke, the amount of alcohol you drink, parents illnesses before they were 65, and also your own medical history.

Watch this video to know the steps to buy LIC term insurance plan online:

Faith binds customer, insurer

Let us start from the very beginning. The Life insurance form that you are filling in is called a ‘Proposal form’ – which means you are proposing that you want a life insurance cover. Life insurance business is based on utmost good faith.

The Latin word for utmost good faith is Uberrimae Fidei – which means you (the applicant) is under a basic duty to disclose all material facts and surrounding circumstances that could influence the decision of the other party (the insurance company) to enter the agreement.

Non-disclosure or a partial-disclosure makes such agreements voidable – the insurance company can choose to ignore it, but they have a right to cancel the contract.

As per the contract, you are proposing and giving all your details that are asked for in the form. This includes your age, height, weight, your smoking and alcohol consumption habits.

#Be Truthful

You should be truthful because of two reasons – one it is necessary to be truthful. The second perhaps the more important reason is when you are not truthful and you were to die, your nominee will not get any money. If a person has taken a policy just say 8 months before the claim happens, there is almost a 100 per cent chance that the claim will be investigated.

Here the company literally looks at the application with a fine comb and anything that has not been correctly stated will be used against the claimant.

If for example: A person dies in a road accident – and what has been hidden was say blood pressure – Insurance companies have said ‘his blood pressure may have caused him some inconvenience while crossing the road…’

Think about your nominee

One very important thing which most life insurance buyers forget is that by lying on the proposal form they are telling a lie to their nominee, not to the life insurance company! If on death the claim amount is not paid (IMMEDIATELY), it is almost like the policy did not exist.

Cross-check copy of application form

Apart from the critical questions, there are some other questions like caste, spouse’s name, spouse’s occupation and children’s names, especially if the nominee is more than one person.

When the company issues a policy, they are bound to send you a copy of the application form – please check whether it is the same form which you had filled. A while ago I heard of a case where the agent had changed the form – and removed the illness clauses before submitting the application to the company.

As the case involved an employee of the company – the critical illness claim was paid without a murmur. What helped was the fact that the client had kept a copy of the application!

Take your time

Please remember even if you are paying a small premium (term premiums are not large), the sum assured is normally a critical amount and your dependents are waiting for that cheque to carry on their lives. It is quite all right for a person to spend some more time while taking a policy but any delay at the time of claim settlement is bound to unnerve the dependents.

Everything that you say in the form – your job, income, past illnesses are all critical to the whole process of underwriting of your policy. The life insurance company also collects data – if it finds that a certain occupation is prone to a particular type of illness, they may ask you to go through some more tests before they issue a policy.

Understand the contract

There is a big difference between a mutual fund ‘investment’ and a ‘life-insurance’ contract. In case of a mutual fund, the asset management company is making an ‘Offer’ to you. This means if you issue a valid cheque, units will be allotted to you. They are making the offer, and you are accepting.

In case of an insurance contract, you are ‘Proposing’ saying that you want life insurance. If your cheque goes through, then the life insurance company calls you for a financial and a medical underwriting process.

If they are satisfied that your life is a normal life, they will issue you a policy. Once a policy is issued by the company it means you have a contract that is binding. On you the liability is to pay the premium regularly, and on them is a duty that in case of death, they should pay the sum assured amount to the nominee.

This is critical and a very important contract which you should understand reasonably well.

Conclusion

Life Insurance is an important decision in life and each step in this whole process is critical to make the whole decision successful and free of any hassles later. Lets look at the whole steps once again through the diagram.

(This article appeared on moneymantra.co.in and has been republished on this blog with their permission. The article is written by PV Subramanyam who also blogs at www.subramoney.com)

Today we discuss two concepts in Health Insurance, generally present in the policy document, which policyholders are not normally aware about, because they don’t care to look at those clauses. We are talking about concept of Loading and Co-Pay . Let’s talk about both the concepts one by one.

What is Loading in Health Insurance ?

Loading, in terms of Mediclaim Insurance means the Insurer (Company) will charge more amount than the regular premium from the policy holder after a claim has been made. Suppose, for eg., you have an Insurance policy and you pay Rs 8,000 each year in premium, and now suppose in 3rd year you make a claim, then from the 4th year onwards, your premium increases by a certain amount which can range from 5% to even 300%. The increase depends on the company terms and the rules. If the loading is 50%, your premium will increase by 50%, which is Rs 12,000. Loading can apply with every claim you make. Please check the brochure off loading is 50% , your permium will increase by 50% , which is Rs 12,000. Loading can apply with every claim you make.

Please check the broucher of ICICI Lombard mediclaim policy stating different slabs for different amounts of claim made. One more product, I would strictly advice all the readers to stay away from, is Star Health’s Red Carpet policy for Senior citizens. This is one of the most fictitious policy, I have ever come to known. Not only is this policy, making an option of Co-pay up to 30% but also has Loading as well. So, a senior citizen, who is normally retired and must also be suffering from one ailment or the other, will be forced to shell out a huge amount of expenses for hospitalization in addition to the premium paid. According to me, it is of prime importance, for the prospective client to look for the clause of Loading in the policy document of said company.

But it doesn’t mean that all Mediclaim Policies in the market come with the Loading clause. There are a few companies in the market without such Hidden Riders like United India(Gold and Platinum only) and Max Bupa. This concept of Loading defeats the very purpose of Mediclaim. An individual takes a Mediclaim Policy, just so that he won’t pay anything extra, out of pocket but ultimately, he is spends more by way of Loading after the claim has been made..

Why Loading concept is there from Insurance Companies ?

Generally, the insurance company is of the view, that once a policyholder has made a claim due to any illness or some major illness, he might make the claim again in future (if not near then in the distant future), so just to be prepared to face those recurring claims, the company tries to safeguard itself, by procuring a larger premium by way of Loading. Sometimes, it make sense but most times, it does not! The only justification on the company’s part, is that they make this loading thing clear, at the very inception of the policy, in its brochure as well as its policy documents and they do take, a declaration from client that they knows about it with his/her signatures. If the client doesn’t read/go through these details and is later on required to shell out more from his pocket, then it is his mistake not the company’s.

So my advice for all the readers out there; Dear friends, don’t get fleeced! By the sheer laziness of not reading/going through the policy brochure or documents, we will be facing heavy Loading, both of money and of tension.

Is loading acceptable ?

On the brighter side, companies can not just have any kind of unreasonable loading in policies. These have been challenged by consumers, and often the consumer forums have taken decisions in favor of consumers. Here’s a case in point –

Amina Sheikh, an octogenarian, was insured for Rs 1.5 lakh for a decade by the National Insurance Co. Ltd. under its Mediclaim Policy. When her policy was due for renewal in 2007, the company increased the premium from Rs 5,305 to Rs 32,787. This was done to make it financially unviable to continue with the policy. Her daughter protested, so the premium was brought down to Rs 23,845, which too was very high. She was forced to pay this premium and renew the policy to avoid a break in insurance. Her daughter wrote to the company demanding an explanation for the arbitrary increase. The divisional manager replied that the policy now stood cancelled as Amina did not seem happy with the firm. He also clarified that the premium doubles immediately when a person crosses 80 years of age and for her, the premium had been loaded by another 100% in anticipation of claims arising due to advanced age.

CWA then filed a consumer complaint. Rendering the judgment on behalf of the bench, the forum president observed: “Managers of public sector undertakings are duty-bound to take decisions based on facts and not in an arbitrary and irresponsible manner based on their emotions.”

The Forum held that the loading of the premium was arbitrary, unjustified, and contradicted the terms of the policy, which is deficiency in service and unfair trade practice. The forum directed the firm to continue the policy by charging Rs 13,112 and to refund the excess premium collected. It also directed the company to continue renewals without loading as long as the insured paid regular premium in time. Also, compensation of Rs 15,000 for mental agony and Rs 2,500 as costs were granted. Source : TOI

[DDET Click to Read 2 more cases]

Case Study 2: In Dr Rupali Shirke’s case, the insurance company loaded her premium by 50%, increasing it from Rs 7,727 to Rs 11,824 and decreased the sum insured from Rs 5 lakh to Rs 2.5 lakh. This was done because of two claims lodged by her, which were genuine and settled by the company. This was considered as an “adverse claims ratio” by the firm. When she protested, the insurance firm ignored it.

CWA filed a complaint challenging loading of premium and reduction of the sum insured by United India Insurance Co. Ltd. The Forum held that the firm was bound to renew the policy on the same terms and conditions. It directed the firm to restore the sum insured and charge regular premium without loading. A compensation of Rs 5,000 and costs of Rs 5,000 were also awarded.

Case Study 3: In the case of Hoshang Khan, after a claim was lodged, the insurance firm imposed a loading of 400%, increasing the premium from Rs 10,558 to Rs 55,952. Khan could not afford the high premium, so he sent the premium cheque without the loading, but the insurance company returned it. CWA filed a complaint against United India Insurance Co. Ltd. The Forum held that loading of premium was arbitrary and unjustified. It directed the company to accept the premium without loading. On receipt of the basic premium, the firm was directed renew the policy with retrospective effect from 2006 onwards to maintain the policy’s continuity.

[/DDET]

What is Co-Pay in Health Insurance Policies ?

Co-pay, as the name signifies is the payment made by two parties, even if that is not in equal proportions This is another important factor to be kept in mind while selecting the Mediclaim policy for oneself. Under this clause, the insured is also required to bear a certain percentage of expenses incurred on illness/disease while hospitalized, either conditionally or under certain conditions..

Usually, in our country, the concept of Co-Pay only comes into picture after a certain age. Most of the companies levy this clause once the policyholder enters the Senior citizen category, that is after the age of 60. Mostly this percentage is mentioned as 20% pay – i.e., policyholder is required to pay 20% of the expenses out of his own pocket. For eg, if Mr X, who is 63 years old falls sick and has to be admitted to the hospital for 5 days, for which hospital bills come out to be Rs 80,000 and his Mediclaim Policy mentions 20% co-pay, then Mr X has to pay Rs 16,000 and rest Rs 64,000 will be borne by the company. The basic understanding behind this clause, is that the company is expecting an increase in claims from this particular section of the policyholders, – the senior citizens. The company’s thinking is that as the age progresses, the chances of policyholders getting sick increases. The expenses on his treatment for a given complication will also be higher as compared to the same treatment for someone who is much younger, say age 38 or 40. Looking at it from the prospective of the company, this clause seems logical but as an individual policyholder, I believe this is one of the main thorns in the flesh of the policyholder who is entering the age bracket of 60s. I believe this percentage has to go down, or associated to some very major complications/illnesses, or senior citizens should given some rebate on premium year on year just to balance out this Co-Pay clause.

Some other companies, preferably PSUs, charge this co-pay clause if the policyholder is taking treatment in out of network hospitals. Earlier, they would apply this co-pay concept, in case the policyholder chooses a higher-end hospital with air-conditioned services or someone from smaller city getting treatment in costly cities like Delhi, Mumbai, Chandigarh, Bangalore etc. At that time, co-pay clause was built in to ensure that the policyholder choose the appropriate hospital/doctor/room level relevant to his economical status as well as the premium paid by him to ensure there is no overspend just because of the existence of the mediclaim policy.

So dear all, please keep an eye for co-pay clause in the policy which you are thinking of buying for yourself as later on, it may negate the very concept of cashless or reimbursement later on as later on! And in the 60s when people have mostly retired with no real source of income, to pay even 20% of the total expenses out of own pocket would be a considerably big amount.

So should you choose a company without co-pay and Loading clause ?

No, not always , you should not make co-pay and other clause as the sole criteria for choosing the policy because even if a company does not have co-pay and loading clauses today , it can include them at later stage . As per Medimanage company

“Again in our opinion, a clear loading policy is better than those policies where there is no explicit loading clause. This is because every policy wording has a term where it clearly mentions that “all terms including premium are subject to change on renewal, based on claims or otherwise.” – this makes you exposed to an unlimited extent, when you grow older. Bajaj Allianz implemented a new loading clause in August 2010. The most scientific loading policy is that of ICICI Lombard, which has classified claims into Chronic and Non Chronic. Non-chronic claims like an accident or Malaria etc. would have a loading only above a certain threshold claim amount, which is not carried forward in the subsequent year. Whereas chronic ailments will have a loading of 75% and carried forward upto 200%.

Finally remember, even if you are buying a policy without loading this year, nothing stops the Insurance Company to add a loading clause at the time of renewal. Dont choose a company only because it does not have loading, choose a company which is stable in its services, and does not make frequent and big changes in their policy conditions.”

Please let me know your comments on this topic . Do you feel its ethical to just mention in the document and not make customers aware about it from their own side ? Do you think if companies disclose about it while selling the product face to face, it would create more respect for companies ?

The inputs are provided by Dhawal Sharma, who is an agent for Kotak and Max Bupa .

We had Mumbai and Ahmedabad meets in last month and I am sharing Presentations and Pictures of those meets . We have done around 5-6 meets in total in Pune , Mumbai and Ahmedabad as of now and we are looking forward to do more in coming months with more better structure and more enthusiasm .

Mumbai 3rd Meet Presentation

Ahmedabad 2nd Meet

Give your opinion on these meets and presentations . Readers from Mumbai/Ahmedabad are invited to Join our Facebook group and also attend future meets. We will try to do the next session by this month end or the next month end depending on how much we can do it with everyone support. We would like to hear your suggestion about the meets in cities and what you all are looking for these meets which we do face to face. Should it be more on basic level or at advanced level ? What topics should be cover in coming sessions . We would do Bangalore session soon .

How does claim settlement work in case you have more than one term insurance policy? Does term insurance provide cover outside India? What if I suffer from some major illness or start smoking after buying a term insurance policy? How easy is it to get a claim from a private insurance company as compared to the state-owned Life Insurance Corporation of India (LIC)?

I am sure you must be concerned about all these questions if you have a term insurance policy or planning to buy one.

Today, I will answer some of the most asked questions, which an individual has in his mind, about term insurance. These questions if left unanswered would not only lead to fear, but may also delay one from taking the right decision.

Please note: The following questions and answers are only for term insurance policy and are generally true for any company’s term plan. However, very rarely these questions and answers may differ across insurers.

1. Do Term Insurance pay in case of Accidental Death?

Yes, term insurance pays in case of an accidental death. The sum assured or cover taken under the term plan will pay the claim if the death has occurred due to any reason, be it natural or accidental death, or death due to some illness.

There are certain riders (additional benefits) such as accidental death benefit, permanent disability rider and critical illness rider. By buying/adding these riders to the policy, a policyholder can ensure that his nominee will get an amount over and above the basic sum assured (due to any of the rider-related incidents).

2. Does Life Insurance covers death outside India?

Yes, term plans cover death outside India provided the policyholder has updated this fact with the insurance company. He needs to mention that he now lives outside India. Just like change of phone number, address or nominee, there is a facility in the policy service form where the policyholder has to mention that he is going abroad.

However, if he is going to a country that is marked as unsafe like Pakistan, Burma, Somalia etc., then the company will decline this facility. Otherwise, this cover will be valid in other countries like US or UK.

3. To what extent Pvt Insurance companies investigates death compared to LIC?

There is a difference between early claim and normal claim. If a claim arises within the first two years of buying the policy (This period varies from company to company), the company investigates extensively before settling the claim.

You can very well understand if someone has a cover of Rs.50 lakh by paying Rs.7,000 annually (And he has taken this policy on monthly basis, i.e. paying around Rs.600 monthly), then the company is at a great risk. Hence, the company will doubly check everything to settle the claim.

In normal claim, premiums are paid regularly and the policy is in force for a long period, say 12 to 15 years. In these cases, there are not much issues in getting a claim, be it LIC or any private company.

4. If I buy a term insurance policy today, can its premium change in the future?

Unless and otherwise it’s mentioned in the policy document. Premium of a term insurance remains the same throughout the term of the policy provided everything remains the same with the policyholder. That is, the policyholder has not developed any illness or any smoking/drinking habit.

On declaring any such thing, company might apply loading and thus the premium amount changes.

5. What if a person becomes a smoker after some years of taking the policies?

If the policyholder has developed any habit, like drinking or smoking, after buying the policy, he generally does not have to disclose this fact to the company at all, unless it’s clearly mentioned in the policy document

6. What if a person was a smoker long back but not at the time of taking the policy?

Depends on the policy, but just for example, the Kotak Life Insurance proposal form mentions that the client has to declare whether he was a smoker or drinker earlier also even if he has left that habit long ago. Please see page 4, question 10.3 of this document . However, I am not sure about other companies. Also, it depends on the company whom they consider as a non-smoker at the time of issuing a policy.

For example: Max New York Life Insurance, for its Platinum Protect (term insurance), considers people, who have left smoking more than three years ago, as non-smokers. So please check the company’s rule 🙂

7. What kind of deaths are not covered in term insurance?

Some important facts, which most of the people are unaware of, are that most companies exclude “Death due to Terrorist Attack”. Although such claims are settled on humanitarian grounds later on when the nominee approaches Insurance Regulatory and Development Authority (IRDA) but such exclusion is there in most companies.

Other important fact, which public at large is unaware of, is that insurance companies do not cover death due to war or natural disaster like earthquake/tsunami. Because in these cases, death toll is high and the claim to be settled runs in crores of rupees which is difficult to settle by the company all of a sudden.

8. How to take care of claim settlement in case of more than two policies?

The very first thing, in these cases, is to declare in the proposal form that you already have a policy from an XYZ company. (There is a column in every company’s proposal form, which a client has to fill if he has an insurance policy from the same company or any other company).

Once such information is provided, then at the time of claim, the usual practice is to submit the Death Certificate to the insurance company with whom the policy is running for the longest period. Other companies are then informed of the procedure due and an acknowledgment from the FIRST Company is provided to them which are accepted by other companies.

Moreover, of late, it has been reported that generally insurance companies do not ask for an original death certificate to settle the claims, even a photocopy of the certificate will do. So be alert while filling the form and provide all the information about your previous policies to prevent even a minor problem later on.

9. Can NRI’s buy Term Insurance?

They can, but there is a catch. As a general rule, a person has to be resident in India to take up insurance policy from an Indian Company, reason being the documents required by the company like Address proof/age proof are to be for some place in India.

Moreover, if the Sum assured required is more than 50 lakhs or so, customer is required to submit his financial papers such as last 3 years ITR or Form-16 which again should be done in India only. Last thing, medical tests would be done at some medical center affiliated to the insurance company near the address of the client which again should be in India.

So these are reason why insurance might have been declined to some NRI.

So one way which might work is this , If a NRI wants to take Insurance, then on his/her next visit to India he should submit his proof of residence, age, last 3 years ITR etc. and get his medical done at his Indian address. This way he can get his policy issued very easily.

However, there is no need to complicate it and in-case you are out in some country and plan to be there for next couple of years, the best thing would be to take term insurance from your country of residence and later when you come back to India, you can buy term insurance that time.

Watch this video to know some more FAQ’s about term plan:

Comments Do you have any other doubts in Term Insurance which are not covered here? Which one out of the above 9 did surprise you most?

The inputs are provided by Dhawal Sharma, who is an agent for Kotak and Max Bupa.

Do you face issues while dealing with your Insurance Companies ? Do they dont answer you on time or dont entertain your genuine concerns on time ? Are you having a problem with Claims or other issues with an insurance company ?

Should you Complain ?

Incase you are facing issues like unsatisfactory answers , no replies on time , delay in replies, taking matters for granted and not treating you properly, any misselling in Insurance, you can complain to IRDA about all this , its just a call away, hence better use the facility and dont feel like you are not powerful enough. You can also mail Insurance companies and cc the IRDA email id for complaints for faster and better reply, but only incase you are facing issues , dont spam them 🙂 . Here is a nice Video Advertisement from IRDA called IRDA – Apki Suraksha ke Liye . I hope they do things in real life also the way they show in video 🙂

Call centre

IRDA (Insurance Regulatory and Development Authority) has started a new service where you can approach by phone or E-mail and complain against your Insurer. There is a call centre started by IRDA for registering grievances on policy-related matters. The call centre will provide an easy and convenient way to bring complaints to the notice of the IRDA. the Toll Free Number is 155255 and Email for complaints is [email protected] . Before the complain, you can approach the Insurance Ombudsman where the dispute involves amount lower than Rs 20 lakh. You can find the contact mail address of the Insurance Ombudsman of your region from IRDA’s Web site.

Do you think its a good resource and would be of help to consumers or will fail just like other projects ? Comments ?sha

On 15 September 2010, the Employees’ Provident Fund Organisation (EPFO) raised the interest rate for EPF accounts by 1% for 2010-11. The organisation increased the interest rate to 9.5% for 2010-11 from 8.5% in the previous year. This 9.5% is the highest in the last five years. However, one needs to understand that the 1% increase is only for EPF accounts and not for Public Provident Fund (PPF) accounts. A PPF account interest rate will continue to remain 8%. The EPFO is one of the largest provident fund institutions in the world. An EPF is a retirement benefit provided only to the salaried class. Each month, a small amount of money is deducted from an employee’s salary which is invested in his EPF account. The employer also contributes an equal amount.

Note that from 2011, EPF will become the top product in the debt fund category as there is no other “safe” products which gives 9.5% or anywhere closer to that post tax. Also, the money received from EPF is tax free after five years. Hence, in the long run EPF is the best option to invest your money. Thus, make sure you invest part of your salary in EPF account. A lot of employees take their entire salary and prefer not to invest in EPF accounts. Also, many employees withdraw their EPF money after they get a new job or just leave their account inactive.

Be Happy but don’t be very happy

“EPF becomes the best debt instrument” is surely good news from return point of view. But, the 9.5% interest rate may not be for long-term. The 1% increase in the EPF has happened because the EPFO has Rs 1,700 crore of surplus money lying in the interest suspense account. Suspense account is the account which has all the unclaimed PF money.

What about Trusts managing their own Providend Funds ?

Note that all the companies do not contribute to EPFO-managed EPF, but they manage their employees provident funds through their own trusts, Now they will have to match this 9.5% interest and it would be a tough thing to achieve . Most probably , a lot of trusts are going to appeal to the finance ministry, that this 9.5% interest rate proposal is taken back , but it looks unlikely to happen (Read more)

EPF money investment in Stock Market ?

An EPF is a long-term investment which salaried individuals have. Hence, some amount of it can be invested in long-term equity instruments. According to the finance ministry, some amount of EPF can be invested in the stock market. But, the central board of trustees (CBT) don’t agree with the same. The CBT has decided not to invest in the stock market. The labour minister Mallikarjun Kharge, who also heads CBT, says, “We had received a letter from the finance ministry asking for parking of a portion of EPFO funds in the stock market. We have received huge opposition from CBT members who oppose the idea of investing in stock markets.” As of now, the EPFO maintains a huge corpus of approximately Rs 3 lakh crore.

No Interest on Dead Accounts ?

Earlier, employees would just leave their jobs but, their EPF accounts would earn interest. However currently, that’s not the case. Now, the accounts, which are not operated for the last three years, will not earn interest. So make sure you either withdraw money from your EPF account or maintain the account. According to EPFO estimates, there are a total of 47 million accounts, of which 30 million, which means 60%/around 57% are inactive accounts. Out of the 30 million inactive accounts, around 10 million accounts (that is 33%) have less than Rs 500 balance.

The EPFO mentions that maintaining inoperative account is quite expensive. Hence, the organisation has decided to stop crediting interest in all the inactive accounts which have not received contributions in the last three years. (Read this article.)

[/DDET]

[/DDET]