“Investors will not have to pay an entry load for investing in mutual fund schemes anymore. They will instead pay a commission to their distributor or advisor directly and the quantum of the upfront commission would be mutually agreed upon.”

More Competition and hence little cheaper for Investors

Now agents will not be getting commissions from Mutual Funds companies which means that now there is direct competition among Agents. The agents can only ask for more if he really gives good service to buyers else they have to settle with a low commission which will be decided by customers.

This means now we can bargain with the agent on commission percentage and if he is not ready with what we offer him/her. We can look for someone else who is better and fits us.

Higher Quality of Service and more transparency in Market

Now agents will have to deliver much better quality of service and be more transparent with investors as their bread and butter is directly linked with Investors and not with the Mutual Fund Companies.

Lots of agents will now move to sell ULIPS rather than Mutual Funds

This move will also force lots of mutual funds agents to shift their focus on ULIPS and similar products which have commission linked with premium paid by customers rather than fee based model like we now have in case of mutual funds. This means more miss-selling in ULIPS is on the cards.

See the following New Video To understand

Update: thanks to income.portfolio for this.

AMC’s are allowed to use 1% of redemption in mutual funds for commission to agents and all the marketing costs. Its the money from exit loads which has to be utilized in commissions and other marketing costs. Most of the mutual funds have less than 0.5% of 1% of exit loads at this point and with this rule of SEBI, it can not go above 1% in future. Also it can be “up to 1%”. So this 1% will be used for every type of cost incurred by mutual funds.

Now most of the funds will have exit loads only if investor gets out in short term like 6 months or 1 yrs. Hopefully it will not be after 1 yr. So its a concern for those who are short term investors. Its not a matter of concern for long term investors as far as I think.

Also, now there is no need for PAN Card for investing in mutual funds up to Rs 50,000 through SIP as per SEBI new rules.

I am out for a 2 day weekend Trek to Kumaraparvata. So no article till Monday morning. I will post the 2nd article of “How a newcomer should start in Stock Markets?” Read Part 1 Here .

In this post, we will discuss on why do you require a Financial Planner to do your financial planning? Each and every area has an expert who understand and has skills for that profession whether it be Doctors, Engineers, Lawyers etc!

Likewise, we have Financial Planners. Now, don’t confuse financial planners with Mutual Funds Agents or Insurance advisers! NO!

Let us see some Important Points on why we need a Financial Planner.

They see your Financial situation as a whole and not just specific Parts:

One of the major issues with our country is, here each area is seen separately and not as a whole. An Insurance Adviser will randomly suggest you a policy without understanding what is your Insurance Requirement.

All that they will say is that your Insurance requirement is 8-10 times of your annual income, which is not the right way of calculating the actual Requirement. Mutual Funds advisers will just pick some Mutual fund for you without understanding your Risk-Appetite and your Future Goals.

They don’t take care of your Tax planning, Estate Planning (wills and Legal Documents) or your Cash Flow etc etc.

A Financial Planner on the contrary acts as a Doctor to your Personal Finance, who will very closely study each aspect of your Financial Life.

He will understand your Risk Appetite, your current outstanding liabilities, your Future Goals, your Future Needs and Requirements, your Insurance Requirement, your Investment needs and finally come up with a Financial Plan and Recommendations which will take care of each aspects in total.

Financial Planner will Educate you:

Financial Planners will make you logical reasoning behind every suggestion he makes. He will make sure that you agree and understand everything, so that in future you can take similar decisions yourself.

Has any Mutual funds adviser told you why SIP is better for you? Or Why You should expect great returns in long term from Equity?

Financial Planner wants to make your Financial Life Better:

Financial Planner’s goal is not limited to Insurance planning or Investment Planning. In fact a Financial Planner is trying to make your overall Financial Life better and paves a smooth financial path for you, which you can start walking on.

Your overall Financial life is made up of different components Insurance Planning, Investment and Retirement planning, Estate Planning, Tax Planning etc etc. He will take care of all these aspects.

Financial Planners are Certified or they under Certification and have deep knowledge:

How many agents or any kind of Adviser you have seen is competent enough to advise you? What is their relevant experience in that field? Most of them are just under their respective company’s Training.

A Financial Planner should be a CFP or undergoing CFP qualification. CFP is the highest level of certification all over the world in the field of Financial Planning. You can also look for people who have deep understanding of Financial Planning and are undergoing the course.

As CFP is new in India, there are many students who are under the learning process and are very good Financial Advisers (You can count me one if you like).

They have good network base:

Good Financial planners will have excellent network of Agents and Other professionals who can be helpful to you in the best possible way. Like for example, if he recommends you to go for a Term Insurance, he may also recommend you some company’s Term Plan and may recommend you to some good and trusted Agents.

This will again be an important thing which you should consider. A Financial Planner may or may not have share in the Commissions.

Watch this video to know the importance of financial adviser:

What is the general Process Financial Planners Follow?

The first step they will follow is to get out each and every strand of information out of you that will help them to understand your situation correctly and in depth. They will try to capture each aspect of your Financial Life through a Questionnaire.

It’s like a Doctor trying to get every information about you to give you a prescription. Then they will analyse each aspect and come out with the Plan and recommendations.

They will not simply come to you and recommend you some mutual fund or insurance policy understanding if you need it or not. Infact they will do your Financial planning in the same way as you would have done yours if you were a Financial planner 🙂 .

They can also assist you in future in monitoring your Financial plan depending on your agreement with the financial planner. Just like you have your dedicated Family Doctor, see him as your Family Financial Planner.

I have enough knowledge about Products and Financial Planning, I constantly Read Financial Magazines and Blogs and keep updating my knowledge. Why should I hire a Financial Planner in that case?

Great!! If you are doing this, it’s much appreciated. You have to understand that

Financial planners are dedicated Professionals in the field. They have undergone tough training and may have much better detailed understanding of the nitty-grittes of Financial Planning which you may lack.

You may have good knowledge and understanding and you may your self take care of your Financial life to great extent. It’s you who have to answer how your Financial Life must be, “Not Bad” or “Excellent” & “Perfect”!

Also it may happen that its your un-true understanding that your understanding is very good. You may have good understanding in one field, but what about other fields?

A financial planner may also have good competence in understanding of Financial markets, Derivatives Markets, Law governing tax etc and these keep on changing and one needs to be updated with the information.

However if you have great interest in Personal Finance and already have great understanding and knowledge, you can enroll for CFP and start a new Career! Dont forget to keep in touch with me!! 🙂

What about the Cost?

Everything comes with the cost. Definitely and if you need Quality then you need to pay quality cost for it as well. But don’t be horrified by the fees you pay to Financial planners, you have to understand the difference between Price and Value.

Just seeing the numbers may make you feel over-charged, but when you concentrate on the value it adds to your life, you will be amazed. If you pay Rs X as fees to Financial Planners you will save many times of that because of the alterations and changes he has brought into your financial life.

Its like if you fall sick then you pay for medicines. No questions asked!! Either pay and save yourself and be happy OR just live in hope of it getting cured by itself, but it will actually get worse and one day kill you.

But my Financial life looks great to me, I don’t see any issues, my insurance cover is fine, my Investments are great…?

Baby, you don’t know a lot of things in that case… Life is waiting for you. There are many people who think they are totally fine and at last they are diagnosed by Cancer and most of the times its at the last stage, don’t wait so long get it checked now!!

My Family and Friends are forcing me to see a Financial Planner? what should I do?

No! You should only see a Financial Planner when you yourself realize that you need one. This is an issue with our country, most of the people do not know and do not realize that their Finances Stink!! Only when it goes out of control they will realise that time has come and by then its too late.

What is stopping you to at least get your financial checkup done by a Financial planner? He will make you realize first that you need it badly and once you agree you can hire him to fix it.

Conclusion

Majority of Indians are totally clueless about Financial planning and only it has happened that in recent years some awareness has been created about it. Most of us try to fix finances on our own without accepting that we are not competent enough to do it all!

WE need a professional. Don’t you pay to Doctor or Lawyer or any other Professional then why not hire a Financial Planner? Go for it!! Jago Investor!!

Note: For people who need my Financial Planning services can mail me

In this post we will discuss why one should really be cautious about NFOs and why in general its better not to invest in any NFO. Have you heard about NFOs and IPOs hitting the markets while markets are doing bad? Why is it so? this is a question we must answer to.

The reason why most of the NFOs and IPOs hit the markets when markets are doing extremely good is to exploit the emotional buying of investors. Its a common thing that investors tend to get in rising markets then falling markets.

So when markets are flying high and all kinds of NFOs with fancy names (some good funds and some junk funds) will hit the market claiming how different they are and how they are ought to be a huge success.

Every NFO will come with its own idea and logic, but investing is never easy and you can see true colors only after few years. They can be success or failure!

So why to go for something which can either fail or succeed, instead why not go for some existing fund which already has proven its mettle, which has given superb returns over long term and has excellent management. These funds have high probability to continue their performance.

Its like: what would you prefer? Take risk of marrying someone you don’t know or someone who is already a good friend and you know him/her over years?

Cheap NAV at Rs 10:

Most NFO offer comes with NAV of Rs 10 and the biggest myth of investors is that its a cheap fund and hence better than a fund with NAV of 20 or 100. NAV growth is nothing but growth of investments and it does not matter what NAV rate is! Rs 10 NAV mutual funds and Rs 100 NAV mutual fund will grow with same rate if their investment quality is the same. There is no reason to invest in a fund that has low NAV.

Myth of High Dividend from Low NAV Fund:

Majority of our “Educated” Agents will tell you that buying low NAV fund will help you in getting more Dividend (if you choose Dividend option) because Dividend is declared on number of Units held. So you will get more units of mutual funds if you invest in low NAV funds!

Whatever he says is true, but he himself does not know that it’s the investor’s money coming back to him and NAV value will again go down by that much value. So in real money terms, there is no benefit of dividend option. See difference between growth and Dividend options

Agents will market it very well and try to push the NFO’s for Sale:

Everyone wants to make money! What other product can be better for a mutual funds agent than an NFO!!! Agents get High commission on selling NFOs and hence they will do anything to sell it. They will spend money aggressively for Marketing as its taken back from Investors eventually and not the AMC. Caution, Be-aware!

Does that mean all NFO’s are Bad?

No! Every existing mutual funds was NFO once upon a time. You should go through the NFO Offer prospectus to find out whether the offer seems interesting and logical enough for you to invest in it. Only then you can go for it. But just understand that only a handful of all NFO’s become good funds.

So out of 1000 mutual funds only a few like 20-30 will be extremely outstanding funds. So the decision is yours! Do you want to take the chance? Or you want to wait and let it show its true colors before you get into it.

Which is the new hot NFO in the Market?

Reliance Infrastructure Fund is the new name in the market these days. All the things which I talked above applied to this too. Before Investing in it read about it in acute detail. I will provide my short view on this.

Reliance Infrastructure Fund is a Sectoral Fund (Infrastructure). This sector looks attractive over next few years. The picture would be more clear after the Budget is out because that’s when we exactly know what is Govt plan in this particular sector.

If its a bad news then the stocks in these sector will take a hit and suddenly it can become a reason for suicide for its investors. Why not wait till the budget and then 😉

Conclusion: Investing in NFOs can be like shooting in dark for retail investors! A better idea for them is to invest in something which has more probability of performing well. NFOs can be extremely successful because of their unique idea or investing style but its too tough to choose them successfully. Better to avoid them!

Before anyone asks, I must tell that its taken by a normal point and shoot camera 🙂 Its just a result of Interest and Willingness to take some good pic + Macro Mode 🙂

I did a short and crisp review of some mutual funds for a friend . thought of sharing this here.

Franklin India Prima Fund – Dividend

151/208 138/157 61/75 are the ranks for 1 ,3 and 5 year . Not a great one to cheer about .

Risk Grade: Above Average

Return: Grade Average

Tata Infrastructure Fund-G

Not a very old fund but its a good one. Infrastructure space can be a big hit considering 4-5 yrs time frame and with the blessings of UPA. Better diversify money in this space along with other infrastructure Mutual Funds.

With 25% CAGR returns since launch , its looks good.

Franklin India Flexi Cap Fund – Dividend

Numbers look good but there are better funds available.

Birlasunlife Frontline Equity Fund-Growth

Extremely good fund to have in portfolio. It has shown strong performance in all the time frame of 1 ,3 ,5 yrs and 30% CAGR return since launch. Better to stop Franklin India Flexi Cap Fund and redirect the money to this one.

HDFC Equity Fund – Growth

Again a good fund to have in portfolio.

What would I do If I were at your place.

– Stop Franklin India Prima Fund

– Stop Franklin India Flexi Cap Fund – Dividend (5k)

– DSPBR Equity or DSP Black Rock top 100 or HDFC Top 200

– Increase your Exposure in Birla Sunlife Frontline Equity Fund

– Share your 10k in UTI Infrastructure and Tata Infrastructure

This post will tell you all about why Planning is the most important and first step in the process of Financial Planning!

Any action that is to be taken needs a proper and precise planning before implementing it. I have seen many people pinging me about their investment plans or decisions to take Term Insurance or Investment plan through mutual funds for next 10 yrs through SIP.

I would like to congratulate them on their decision and action. They are ahead of most of the other people.

“A good plan today is better than a perfect plan tomorrow”

But is it enough? Is that all? Is that the initial step everyone should take? The answer is NO!! A lot of people have gone directly to the second level and skipped the very first basic level, which is Planning!

First Step of Financial Planning

The first step not making investments but planning for everything and then executing it, Why is planning important? Most of the time people concentrate too much on action and not planning. If you take actions without planning things, there will be lack of clarity ,and it will bring doubt in your mind about investment.

A friend of mine invested in mutual funds through SIP. For the last 6 months markets did good and his portfolio showed upward movement, later the market crashed and he stopped his SIP payments. I asked him why is he not continuing his SIP. To this he answered that markets are going down.

But he also said that he don’t need this money any sooner and he is making investments for his Child Education which is 12 yrs later and his investment is for long term in stock market.

His decision of starting investment is great, but investing without any planning and not knowing exactly why you are doing it is like driving without knowing were to go. You will eventually go somewhere, but that may not be your desired destination.

So what are the steps that needs to be taken before the action of Investment?

Knowing your Goals: First plan that why are you investing; what is the goal associated with your investment; Is it Buying Home? Buying Car? Vacation after 3 yrs, Retirement, Child marriage? etc…

Knowing your time frame, when you need money: This is very important because this will decide a lot of things

– The product you can invest in

– The risk you can take

– The amount you need to invest per month or year

This will make your path very clear, after this you just have to follow it without any doubt in mind.

Action and monitoring: Now you just have to take action and don’t doubt it again and again because you have cleared every doubt beforehand.

Case Study

Case 1: Unplanned Investment

Ajay is a regular reader of Jagoinvestor and after reading some articles on this blog, he decides finally that he will invest k per month through SIP

He starts a SIP with a mutual fund and now he is happy that he has been investing finally. He invests for 2 yrs and markets have gone up and down and at the end his investments are at same place where they started. So there is no appreciation in value.

He decides to take half the money out of his investments and uses in buying a car which was his plan from many years. Markets finally starts recovering, but as usual he realizes very late that this is the time to put money in markets (as all the general public realize this very late).

He starts his SIP again and now continues this for some years. He periodically takes money out of his investments on many occasions like for his vacation and his child education costs.

What is the problem with this approach?

– No predefined goals and hence no clarity on investment plan- No idea of how investment should be divided for different financial commitments and not investment as per risk-appetite and goal’s importance.

Conclusion: He started investments which was a good idea but Ajay jumped on the second step of the ladder. The first step was to plan for things.

Case 2: Planning everything

Ajay now knows that he can invest 20k per month and have to plan how to make proportionate investments for his financial commitments. He identifies his goals and how much money he would need for each.

Now he exactly knows that for which goal where & how much he has to invest. There will be no distraction in between by equity markets going up and down or any other factors because in the start itself he has factored in all the possibilities. In short Now he has a clear path and he knows how fast or slow he has to walk on it. At the end if he keeps on walking on it the way he planned Success is guaranteed.

Conclusion

Planning your finances can be boring, but its vital and most crucial part of financial planning. A person who gives much time planning things has higher chances of achieving it. Take action is second step. Planning things in advance reduces doubts about certain things, provides clarity in financial life and hence reduces a lot of issues.

Question :

How much difference do you think will happen without planning as per your view?

It simply means that we will be left with some extra surplus every year .

A male who has taxable salary of 4 lacs per year and has 1.5 lacs as exemption limit , pays around 40,000 as tax . Now , after the exemption limit is raised to 2 lacs (assumption) , there can be 2 scenarios .

Scenario 1 : Exemption limit is raised but tax rates are not . Current tax rate is not

10% for 1.5 – 2.5 lacs

20% for 2.5 – 5 lacs

30% for 5+ lacs

In this case , he will have to pay 35,000 as tax (assuming tax rates for 2008-2009) . This means a saving of 5,000 on tax from previous year .

Scenario 2 : Exemption limit is raised and tax rates are also adjusted. A common sense guess would be

10% for 2-3 lacs

20% for 3-5 lacs

30% for 5+ lacs

It must be something like that , this is the minimum we will/should get

In this case , the tax would be 30,000 , and savings would be 10,000 per year.

What can this small amount do ?

So we can save in range of 5,000 or 10,000 or someother amount depending upon the changes. What can be the value of this for us as investment point of view.

this money can be invested in a mutual fund through SIP monthly for next 30 yrs ,

5000 can make

14 lacs at 12%

29 lacs at 15%

10,000 can make

29lacs at 12%

58 lacs at 15%

Assumption is that the money can be divided in 12 equal installment and can be invested per month .

This is a Video post by me , where I have tried to teach some basic formula’s for starters who should know important calculations using which they can calculate important stuff like Maturity value of Investment when they make SIP payments , or one time payments .

I am getting some questions like “I want to invest 2k per month for 10 yrs in mutual funds , Can i generate 20 lacs” type of questions . Seems like many readers do not know how to apply and use simple formula’s to calculate these stuff when they calculate how to generate wealth for long term . Often you might have felt that you have to depend on others for calculations , because you don’t know it themselves .

I have made a video myself where I explain 3 important formula’s which everybody should know .

1. Compound Interest

2. Annuity

3. CAGR

Lot of you might have learned this school , but many have forgotten it . So in this video post I have explained it with examples . I hope that it will help beginners or new readers . I am also giving a Calculator below the video where you can do your own calculations , If it gives any error , please go to the link I provide and calculate it there . I will also put presentation here , so that people who have very low bandwidth can view the presentation at least.

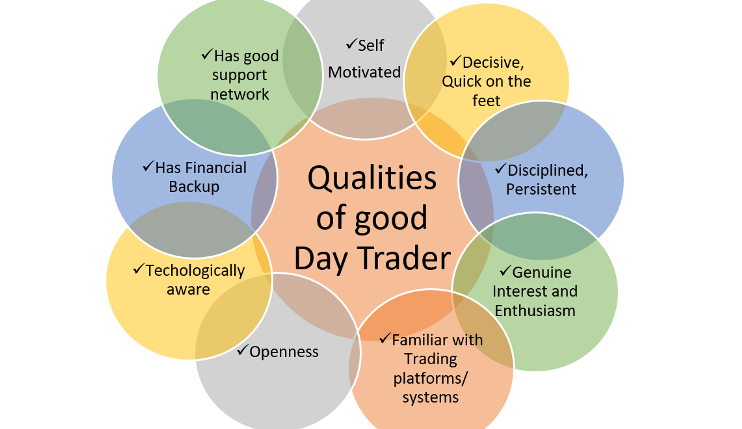

This is a guest Article from a fellow blogger friend and a very good Technical Analyst, Nooresh Merani. This is an interesting article where he presents how a profile of a Day trader looks like.

A part of this article was published in May 14th Issue of Money Today Magazine. I hope it would be a good read for everyone , Even If you are not related to Trading , you will come to know what is Day trading and how it can be a full time profession and very rewarding one . Read the article Below .

THE JOB = Day Trading

Job description: 6 hours a day / 5 days a week which requires hardly any physical activity apart from grunting or swearing in anger or thumping hands, tables and chairs in happiness.

Desired Profile: The desired candidate should be good at accounts and quick at using the computer keyboard or mobile keypads. No formal education or age bar.

Company Profile: It’s one of the oldest organizations (BSE is formed in 1875!) which is open to all candidates provided they have capital to trade with.

Remuneration: The salary has no upper limit but the candidate has to forego a small amount as brokerage/ taxes on the transactions.

The above job description seems a dream job!!

The profile of a day trader is not as rosy as it seems as they don’t have a fixed salary, instead they have to risk a security deposit (trading capital) paid up with the company (exchanges/brokers) which may be blown off in few hours, days or weeks or years.90% of Traders pay salaries for the rest 10%.

Trading is one serious business and a highly disciplined profession but, a large section of traders who don’t have this attitude get thrown out of the system very quickly. A trader learns from the mistakes, accomplishments through his trading career and by honing his technical and intuitive skills.

Initial grind:

Every traders goes through the initial grind (sometimes recurring) of losses, depression, self -realization and more.

A must Quote for every traders’ desk, “People who learn from their own mistakes are Wise, People who learn from others mistake are Wise and Lucky and, those who do not learn at all are Traders (Suckers)”

So, to be successful in trading, the most dynamic profession, where even a richest man can’t afford an hour’s lunch break (the Gujarati Thali would cost somewhere in Lakhs!!), one needs to learn, evolve, adapt and be disciplined. Always learn from the past, apply it to the present so that you can gain in future!!!

A Traders Day!

Pre-Morning work:

First thing a trader checks is how Dow Jones, European indices performed overnight and the current situation of Asian markets. SGX Nifty in Singapore opens up much before India so a trader gets hint of Nifty opening.

The trader makes modifications to the stock lists and observations made for the day. Technical, Pivot and data traders are ready with a list whereas system traders rev up their mechanical engines which generally don’t deliver much.

Trading Hours:

Although every trader has to see the ticker on his computer monitor for prices, but, there is a section of traders who only rely on ticker reading, which is a study of price & volume fluctuations. For best results, a combination of intuition, ticker reading and knowledge of technical analysis is a must.

Indian markets are one of the most volatile ones and it’s a common saying out here – Nazar hati durghatna ghati (Moment you get your eyes off you will meet with an accident). So a trader has to be attentive and nimble footed to make split-second decisions and follow the personal trading style/rules.

Post Trading Hours:

This is the best time for the trader to catch up on a snack or freshen after finishing of the calculations and noting down the open trades or the profits made in the day.

Analysis and Self-Evaluations:

The amateur traders don’t realize that this part of a trader’s life is equally important. Technical traders go through their charts; mechanical traders test their system to come out with a list of possible stock trading ideas for the next trading session and evaluate the current positions.

Trading as a profession has the most ups and downs with terribly bad trading sessions and equally high performance sessions. Every trader needs to keep evaluating, modifying and optimizing their trading styles to stay in the loop or the market knows a way to kick you out.

Latest Experience with the Screen!

Although I and many of us traders do follow the above plan but human nature is frail and one does make mistakes. One thing I have realized with experience is if you make a cheap mistake (small loss) early you would make a killing next time around by not repeating it.

The last mistake I made off late was to pre-empt and anticipate a big down move in 2nd week of March which didn’t come but luckily got saved because of stop losses and the screen. The next time around I did the simpler thing of re-acting to the ticker sense.

My one such encounter with markets was on 15 April 2009 when Indian indices outperformed global indices.

Many traders were yet again caught on the wrong side of the trade by watching the performance of Dow Jones overnight.

The index opened lower and drifted lower. But, ticker did not show signs of weakness and out of index counters continued to gain strength. What lot many traders missed out was, that Hang Seng (Hong Kong) was up 600 points on 14th March, the day Indian markets were closed due to a holiday.

Any technical analyst would confirm Hang Seng bears the closest co-relation statistically with India. So, this simple observation kept my bias bullish though the index was negative to start with.

The ticker was purely biased towards the mid cap segment in the last few sessions so my focus was on them.

We kept on holding to the previous open positions (namely Crompton, ks oils, guj nre, gtl infra, ghcl).

Also, seeing the momentum, added on to my technical picks Dishman Pharma, Everonn & Crompton for the day at higher levels then opening which gave awesome moves of 10% + in the day!!

Sensing that the up move was backed by nervous morning sellers squaring up, we booked out of previous positions to reduce the risk exposure and raising stop-losses to cost to conserve gains. A combination of aggressive buying along with disciplined money management did the trick as index closed 200 points lower the next day.

The learning from above experience was “Respect the Screen & Markets are Supreme”. A Trader looks for intuitive hints from the screen and doesn’t ask why it’s performing so, but, just follows it on the path to making money.

Above all would like to end this with few words of wisdom in Gujarati – Market Ni kamai market ma samai – (Money made in the market, stays in the market). A wise trader makes money and takes it home regularly!

Keep reading , don’t thin’k its not related to Personal Finance, After you read the paragraph below and read further you will come to know. This posts talks about the state of knowledge of Indian ulip and mutual funds agents.

The Indian Cow

“HE IS THE COW. “The cow is a successful animal. Also she is 4 footed, and because she is female, she give milks, [ but will do so when she is got child.] She is same like-God, sacred to Hindus and useful to man.But she has got four legs together. Two are forward and two are afterwards.

Her whole body can be utilized for use. More so the milk. Milk comes from 4 taps attached to his basement.[ horses don’t have any such attachment.

What can it do?

Various ghee, butter, cream, curd, why and the condensed milk and so forth. Also she is useful to cobbler, waterman’s and mankind generally. Her motion is slow only because she is of lazy species. Also her other motion.. gober] is much useful to trees, plants as well as for making flat cakes [like Pizza ] , in hand ,and drying in the sun..

Cow is the only animal that extricates her feeding after eating. Then afterwards she chew with her teeth whom are situated in the inside of the mouth. She is incessantly in the meadows in the grass. Her only attacking and defending organ is the horns, specially so when she is got child.

This is done by knowing her head whereby she causes the weapons to be paralleled to the ground of the earth and instantly proceed with great velocity forwards.

She has got tail also, situated in the backyard, but not like similar animals. It has hairs on the other end of the other side. This is done to frighten away the flies which alight on his cohesive body hereupon she gives hit with it.The palms of her feet are soft unto the touch. So the grasses head is not crushed.

At night time have poses by looking down on the ground and she shouts. Her eyes and nose are like her other relatives. This is the cow. ”

Most of the agents in India who sell Mutual Funds or ULIPS talk in the same way about it . They know very little about it , only to an extent which can make ignorant people feel that these agents know a lot . They have no understanding of How to choose a good mutual fund or How to manage Ulips effectively

And these agents work for big houses , I have often came across agents who explain me mutual fund or ULIP in the same way you read “what is COW!” . They don’t have communication skills to sell a product or convince a person who knows something about the product .

If you are slightly informed person , just call an agent and ask him internal questions about the product . you will see in how much water they are in .

What should be Done !!

There should be strict accountability from agents . Though you can never put all responsibility on agents for any loss of yours , at least there should be some quantifiable measure for the standard of there recommendation .

I am not saying that all agents are like this , but majority are . Some of the agents are very nice . like the one I dealt with while buying for me for the first time .

Apart from this , the biggest responsibility lies with you , you have to be well informed yourself . If you are your self an idiot , agent has all the right to make you one . So be informed , knowledgeable and understand what to do . You have to understand how to Find out if a product fits you, (Look at GFactor )

Question for you :

Do you think that eliminating agents (one who recommend products) will make situation better or Worse !! .

I think it wont affect a lot in current scenario !! , what do you think ?

I wrote a post on how does a common man think about money , read it

How much do you want to earn ? What kind of Financial life do you want ?

Don’t we claim to lot of people that Money is not important to us in life ? We want happiness, We want time to do things which we “like”. We are interested in health , happiness and peace of mind, We want to spend time with our family, play with kids, take our spouse for a world tour and a lot of similar things.

Average person thinking

Most of the people will claim that money is not the biggest thing in there life , but still we see most of the people working consistently for 50-60 hrs a week , some work 70 hrs+ . We are free only on weekends and that too goes in household chores and planning for next week and may be one evening which one can claim to be the way “they wanted it to be” .

The truth is most the people can achieve there financial goals but are not fully committed towards it . This may be true because of lack of knowledge or attitude towards this .

We all have desire to achieve our goals in life , and that will happen only when we are financially independent , No wonder that we will have to work in the starting period of our lives . Every will have to do that , but better financial management can help in achieving your goals earlier than average .

So take out some time to work on your personal finance , thats what you are working for whole your life !! , incase you dont know 🙂

People Invest and then forget

Most of the people invest or take decisions and then forget about it , they feel that there job is done . this may be because of the fear of loosing money or coming to know that they made a wrong decision .

How many times it happened that you took a share , mutual fund or a policy and it didn’t work for you , didn’t give you returns as expected and actually made losses . Did you care to find the reason for making a mistake , did you take any step to confront the situation and take measures to fix the mess . Or you just left it to destiny saying “I will just give it some time , it should be fine in 1 yr or so”

Successful people take hard decisions , they work for there money , they read , they go to websites to find out things , they take out time to contact people and get information about it .

My experience

I took a Term Insurance from SBI (SBI Shield Plan) last year . It was the best plan which suited me .After some months there was news that term insurance premiums have come down and there is a new entrant “Aegon Religare ” in the market . I calculated back and saw that Reliage premium was Rs 1,000 cheaper than SBI (for my policy) .

I contacted my Agent and asked him to provide me the numbers (premium) for this year and told him straight forward that I will surrender the policy this year I I dont get a good deal . Atleast I will not choose them for my additional Insurance cover .

I don’t think many people care to find this out and take the “pain” of doing it all over again for the sake of small money . remember that its not small money … Small is Big !!

People make fortunes by investing regularly small chuck of money . So if get a chance to save even a small bit , do it . It will show in future .

What to do ?

Money can be generated but with discipline , you have to understand this and act on this . Invest systematically for a long period of time and use well know principles of Asset Allocation and Portfolio Rebalancing (read what is it) , portfolio rebalancing .

Just like we have lots of data , confusion and noise in Stock market , in the same way we also have it in personal finance . There are thousands of products claiming to be better than others . There are mutual funds who claim to give 25% consistently (there are many which have actually given) .

You have to get out of the noise , and understand that you dont need much to make long term wealth . You just need better than average returns .

Let us see some components required :

– Strong Planning

– Stick to the plan and follow it with Discipline

– you dont need 20% or 30% returns (and don’t even look for it) . Just 5-6% above inflation is good and that’s what you should expect .

So plan your finances well in advance , have a path to follow and then just follow it without deviating in between . Dont get greedy .

Please let me know how do you like this new look for the blog , I am sure many like it , It gives better look and feel .

Answer me following question

– Do you have any financial plan for future ?

– What kind of returns do you expect from your investments as per your thinking ?