Last month we launched Questions Forum, which is a place where you can ask your personal finance doubts . There were some prizes which I am going to announce today . JagoInvestor Forum is a place where anyone can ask a personal finance question and get its answer within 24 hours from experts present there .

So if you have any doubts on your Insurance policy , Banking, Mutual-funds, stock market , tax related or any kind of money related query , feel free to ask it . JagoInvestor Forum has got great response in this last 1 month with more than 250 people asking 300 questions and with 1200 answers overall .

First Prize : The winner is Mr. Gopal Krishan Doda. He has been a great help in providing good answers and has answered more than 150 times. He wins a free one year subscription toMProfita desktop portfolio management software worth Rs. 1488.

Second Prize : The second Prize goes to Mr Naveen Arichwal for asking maximum questions. He wins the book on retirement Planning named “Retire Rich Invest” or any other book of choice .

Bonus Prizes : Jagadees and Rakesh (rakeshnwo ) , they also win the book “Retire Rich Invest” , or another book of their choice . They have also contributed well in answering the questions of others . Good job .

Free-Stuff to all Members of the Forum

As promised I also sent some free stuff to all the registered members of the forum. Here is the list of things I sent to them.

HouseHold Budget Spreadsheet to maintain your holdhold budget and see basic analysis

A research report on a Mid-cap Stock (Not made by me)

Do you want these free stuff ? I am planning to mail this to all the members who are subscribed to this blog in coming week , so if you are not yet registered on the blog you can register by putting your name and email on the subscription form on the right side sidebar or Click Here to directly go to the Subscribe Form

Note : Make sure you click on the subscription Link you get in your email after you fill in the information , Its required step to get subscribed

Win Prizes every month

You can now win every month! , You you heard it right . There will be total of 2 prizes every month from now onwards. Just ask a question on the forum for any personal finance related doubts and the question which gets the maximum number of comments will win the first prize. So make sure you ask an interesting questions which is of everybody’s interst and make the question very clear. Apart from this first prize , there will be a second prize for a member who will give the maximum number of good answers and helped other to solve their queries . I will choose the winner based on every month data . So every-month you can win prizes by asking your questions . Let me know how do you like this concept.

First Prize : The person who asks a question and gets the maximum number of comments wins a free one year subscription to MProfit– a desktop portfolio management software worth Rs. 1488.

Second Prize : The second prize would be the person who gives the maximum good answers and helps others in clearing their doubts . He wins a personalised Tshirt or a book of his choice worth Rs 500 .

I would like to hear back the feedback of readers on the forum , Is it useful ? What changes are required to make it a better community ?

Winners Please contact me for claiming the Prize 🙂

Are investors in India spoiled a lot? Does it look like we have enough regulations for the investor to make sure his money is safe or do you think that laws still need to be made to make investing a happy experience?

The stock market looks robust and we haven’t seen a major scam for quite sometime now; IRDA and SEBI have and are still sorting out the ULIP mess; SEBI has made Mutual Funds cheap – is there more the investor wants?

Sure they do – there is always room for improvement at the top! To assist the regulators, the investor needs to increase his awareness too. Here are my top 3 wish lists for the small investor in the personal finance space which will make investing a memorable experience for him.

#1 Introduce Stringent Real Estate Regulations

A home is often the most prized possession for the small investor today. But often he finds himself at the receiving end of the deal. The modus operandi is the agent or builder will sweet talk you into booking an apartment after you have shown interest in the project.

Once you shell out the booking amount, you are locked in with the builder and the project you bought into. Future demands of money come in; you pay up through a home loan and the builder delays the apartment delivery, in many instances routing your money to launch other projects. A home is the biggest asset the small investor buys in his lifetime( Also see Tips to Buy house).

Paying the home loan is a huge burden to begin with.

Given this, it is but anybody’s guess what a nightmare he goes through when the real estate builders delay the projects by years – the investor has to pay the rent and pre-EMI together. That is a huge drain on his finances.

The regulators ought to come out with a mechanism to stem this rot. Builders need to be rated and penalized for late or shoddy delivery. There needs to be a mechanism in place to penalize builders who cannot deliver the most prized and costly possession for the investor.

CRISIL has already come out with its Real Estate Star Ratings in August 2010 – we will have to wait to whether this helps the real estate industry in a positive way or it becomes just another rating mechanism without serving any useful purpose for the buyers. Till that happens, the investor has to suffer and fight the battle himself.

#2 Sell Insurance to protect against risks, Don’t just make commissions

The old adage “Insurance is never bought, it is sold” holds true even today. Seldom does one buy insurance for protection purposes; it has been mostly sold as an investment vehicle. And whenever a product is sold, it is commissions that drive the sale, not the investor’s profits.

Call it the insurance agent’s smart tactics or the gullible investor’s ignorance, insurance, and especially ULIPs, continues to be mis-sold. This seems to be the most talked about topic in every personal finance corridor. There are regulations to stem the dirt from spreading and there are investor awareness programs out there; the regulators fight and introduce more regulations but at the end of the day, the investor continues to still suffer.

Given the history around this, I think no amount of regulation can eradicate this illness. The only answer is investor awareness. If the investor empowers himself with what is best for him, he will buy the best insurance and probably look at money back, endowment plans and ULIPs the last!

We need to get to a state where insurance is sold only for what it’s meant to be bought for – protection!

#3 Educate themselves about Equity, Don’t just have a short-term view

It’s a very old saying – “It’s not timing the market that matters, its time in the market that matters most”. Equity is meant for the long-term but most investors buy and sell equity to make profit in the short-term.

The investor’s lure is milked high and dry by brokerage houses that earn on brokerage charges which investors generate for them by buying and selling securities.

All brokerage houses will bombard you with SMSes and calls about a hot stock tip, in fact, we recently had the same brokerage house giving a buy and sell signal on the same stock on the same day, one to institutional investors and the other to retail investors.

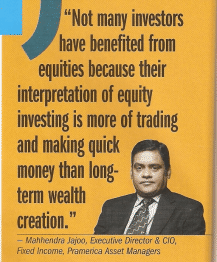

More churning and constant buying and selling never made anyone rich except the broker. Look at what the Executive Director and COO of Pramerica Asset Managers was quoted in Money Today as saying.

Active and passive trading:

It has been proved that the amount of money that one could generate by active trading is usually less than the amount you could generate by passive investing over a long period of time.

Despite this, most of us still lose money by trading; brokerage houses still walk away with our hard-earned money and we keep thinking “How did the guy next door get rich quickly ?!”

IPO’s are issued using the book building process with the idea that the price discovery will happen by buyers but it’s anything but that. Investors still lose money in IPOs. It’s not just insurance that is mis-sold, its equities too !

As a nation bursting at it seems with a young population, the regulators, investors and product sellers need to make sure that investors can have the confidence in investing in products that suit their over all portfolio – its only then that we can pass on the baton of confident investing to the next generation.

This is the 3rd series of learning from comments ,where I handpick some of the best comments which gives some very good insight and useful information. Following four comments talk about Gold ETF’s , Education about finances to Children , Real estate prices relation to supply of land and KYC .

Gold ETF’s might not be safe

There are serious allegations on various gold etf’s & custodians like GOLD across the globe of using very high leverage for gold holdings. I was going through the fact sheet of SBI GETS & UTI GOLD FUND. Susprisingly all indian ETF are using Bank of Nova Scotia as the custodian for Gold. If you just try to find out the repute of this custodian in financial blogosphere by typing ‘Bank of Nova Scotia is the custodian for Gold’ in google search, you will get to know the kinds of risks involved in GOLD ETF’s – mainly technical risk (its a technical default if gold is not held in reality). So as they say Let the buyer beware. Since most indian families usually keep atleast one locker, i would suggest its better to buy physical 100gms /coins from a reputed jeweller with bill. Its also more easy at the time of selling if bought frm a jeweller than buying coins frm bank also its costs less. – Shared by Rahul .

Money should be discussed with Children

You are right Manish as everybody must teach the children about money but the biggest dilemma people face is how they will be treated back if they start talking about money. Our society treat Money as necessary evil with more stress on the evil so 9 out of 10 times a person is feared to be called Money minded or Kanjoos if they just try to stick to a discipline of Budget within their family. So many parents just avoid asking their kids how they spend money for the sake of their image. We have always thought money as a bad thing which must not be discussed (Mard se uski kamaai aur aurat se Umar nahin Poochte 🙂 ). In our films Rich has always been a villain but things have to be changed. I still wonder that rather than showing hero taking a loan from money lender and then becoming a Daku for revenge, why dont our films show that taking a loan to spend lavishly on your daughters wedding beyond your means is bad thing and the best solution to keep lala away. Secondly we always think that kids are not mature enough to talk about sex and money. (Often not knowing how smart they are 🙂 ). We must respect their senses and impart knowledge to them gradually. If you dont teach your kid about these things he will seek Pornography and Financial Pornography is much more dangerous. Can we compare “double your money schemes in one year” with Pr*******tes in the world of finance. So every parent has to cross these mental blocks and take up this duty to empower their kids to face the real world. – Shared by Pramod

Is Short supply of Land responsible for High Real estate prices

Who says land is in short supply in India ? It is kept in short supply in India by the builder politician nexus. Have you ever tried to look at Delhi’s satellite image from Google maps. Mind you 50 % of the land within boundaries of NCR is vacant. The mechanism is – You (Farmers or forest or something else) have land. You want to build a house over that land. Govt will not allow you and will force you to buy some expensive piece of land in an “approved” area. Once all the land is sold then the same land where you or any other ordinary citizen was not allowed to build houses (becuase the land was meant for farming, forest, green belt Archeology blah blah blah) will be captured (acquired) by the govt and will be given to builders by changing status of the land use. Then you will buy the plot at sky high price and new land will freed once all the plots are sold and the cycle goes on. If govt declares its master plan at once and free all the land which is marked for residential use in one go then there will be no shortage and no high prices. BTW All of the population lives on 30% of the land. Rest 70 % is covered by ice, deserts, high mountains etc. Just wait Global warming will ensure that if 10% of the world sinks in water 20 % will become available to mankind as ice shields will go away 🙂 Wait till Unitech starts buying Norway and Siberia. – Shared by Pramod

How to Check if you are you KYC compliant

For those who are not sure if they are KYC compliant can check the http://www.cvlindia.com/. Click on ‘enquiry on kyc’ option (Direct URL) and enter the pan card number. Invalid data means the person is not KYS compliant. Shared by Raj Panda .

From the Budget, infrastructure bonds are also eligible for additional tax exemption upto Rs 20,000 over and above Rs 1 lakh under Section 80C. IFCI Ltd was the first company to issue these infrastructure bonds and they have collected a substantial amount in the last few months. Now, IDFC Ltd has introduced its infrastructure bonds and there are a lot of investors, who are considering these bonds as an option to save additional tax for this year. Rajendran and Prashant have also asked the questions related to Infrastructure bonds some days ago on Jagoinvestor Forum. In this article, I give you brief information on IDFC Infrastructure Bonds.

The maturity period of these bonds is 10 years and the lock-in period is five years. These bonds will be listed on the Bombay Stock Exchange and National Stock Exchange. After completion of five years, you can keep these bonds for additional five years and withdraw money at the time of maturity. In case, if you need to withdraw money before maturity, then you always have an option to sell these bonds on stock exchanges. Thus, these bonds can be traded like stocks on the stock exchanges but only after the lock in period of five years is complete. You would require a demat account and Permanent Account Number (PAN) to invest in these infrastructure bonds. The face value of each bond is Rs 5,000. The minimum application has to be for two bonds and in multiples of one bond thereafter. Hence, the minimum investment required is Rs 10,000. You can invest more than Rs 20,000 in these bonds but the tax-exemption would be only upto Rs 20,000.

Taxation on Infrastructure Bonds

You will get tax exemption benefit up to Rs20,000 when you invest in these bonds. However, the interest gained will be taxable. The interest would be added to your income and taxed at the existing slab rate. this taxation rule will be same even after Direct Taxes Code (DTC) Bill comes into effect. Both, the current Income Tax Law and DTC require you to pay tax on the interest earned.

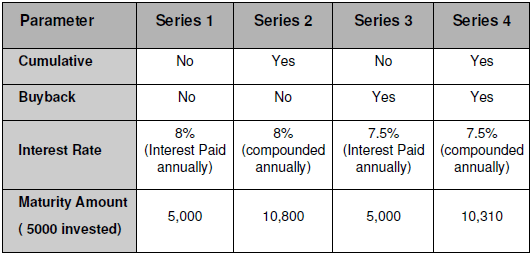

Infrastructure Bonds in different series

Note that these bonds come in 4 different flavors and they are called as Series 1, 2, 3, 4 . Each of these series is different from each other in some way. There are two main things you should understand , which might be of concern to you.

Interest Cumulative : Series 1 & 3 do not provide cumulative interest. They will pay interest annually. For example, if you invest Rs 10,000, then after completion of 12 months, the interest amount will be paid to you every year and the bonds maturity value would be same as your investment. However, bonds which have cumulative interest will keep accumulating interest. And this interest would be compounded every year. (see CAGR)

Buyback : Series 3 & 4 have buyback option. Buyback option means that you can sell your bond back to issuing company after five years; once the lock in period is complete. In return, you will get back your original invested amount and the interest accumulated for five years. You would notice that interest rates for series 3 & 4 is 7.5%, which is because they have an added advantage of buyback facility. If you don’t want buyback option, you will get 8% interest. People not opting for buy-back options will depend on secondary markets to sell their bonds if they require money urgently before maturity (10 years). Thus, after lock-in period (five years) is complete, they will have to find a buyer in secondary markets else wait till maturity, when they will get the money back from IDFC.

Other features of IDFC Infrastructure Bonds

NRI’s cant invest in these bonds (Only available to Resident Individuals and HUF’s)

The bonds don’t attract any TDS

The bonds are rated LAAA by ICRA, However high rating is not something you should be very excited about. (Link)

The interest accrued on the bonds will be credited to the respective bank registered with the demat account through ECS on the due date for interest payment

Interest on the bonds shall be payable on annual or cumulative basis depending on the series selected by the bond holders

The bonds can be pledged for availing loans after the lock-in period of 5 years

Subscribe to the Bonds in physical form

If you do not have demat account and want to apply for these bonds in physical form , you can still apply for them using these steps (link) , Thanks to Srinidhi for giving this info .

Don’t fill up the demat details in the application form

Compulsorily provide the following three documents with the application form:

Self-attested copy of the PAN card;

Self-attested copy of a cancelled cheque of the bank account to which the amounts pertaining to payment of refunds, interest and redemption, as applicable, should be credited.

Self-attested copy of the proof of residence. Any of the following documents shall be considered as a verifiable proof of residence:

Ration card issued by the Government of India; or

Valid driving license issued by any transport authority of the Republic of India; or

Electricity bill (not older than 3 months); or

Landline telephone bill (not older than 3 months); or

Valid passport issued by the Government of India; or

Voter’s Identity Card issued by the Government of India; or

Passbook or latest bank statement issued by a bank operating in India; or

Leave and license agreement or agreement for sale or rent agreement or flat maintenance bill; or

Letter from a recognized public authority or public servant verifying the identity and residence of the Applicant.

Should you Invest ?

Though, it’s mentioned that the interest rate on these bonds are 8% or 7.5%, the interest earned would reduce further to 5.5%-6% range when you count the tax paid on interest. But if you look at it from a different angle, and count your money saved due to the tax-exemption at the time of investing, in that case the return would turn out to be around 9.5%-10%, but do you think it’s the right way of looking at returns?

What do you think about these bonds ? Are you investing or not and why ?

We had Mumbai and Ahmedabad meets in last month and I am sharing Presentations and Pictures of those meets . We have done around 5-6 meets in total in Pune , Mumbai and Ahmedabad as of now and we are looking forward to do more in coming months with more better structure and more enthusiasm .

Mumbai 3rd Meet Presentation

Ahmedabad 2nd Meet

Give your opinion on these meets and presentations . Readers from Mumbai/Ahmedabad are invited to Join our Facebook group and also attend future meets. We will try to do the next session by this month end or the next month end depending on how much we can do it with everyone support. We would like to hear your suggestion about the meets in cities and what you all are looking for these meets which we do face to face. Should it be more on basic level or at advanced level ? What topics should be cover in coming sessions . We would do Bangalore session soon .

How does claim settlement work in case you have more than one term insurance policy? Does term insurance provide cover outside India? What if I suffer from some major illness or start smoking after buying a term insurance policy? How easy is it to get a claim from a private insurance company as compared to the state-owned Life Insurance Corporation of India (LIC)?

I am sure you must be concerned about all these questions if you have a term insurance policy or planning to buy one.

Today, I will answer some of the most asked questions, which an individual has in his mind, about term insurance. These questions if left unanswered would not only lead to fear, but may also delay one from taking the right decision.

Please note: The following questions and answers are only for term insurance policy and are generally true for any company’s term plan. However, very rarely these questions and answers may differ across insurers.

1. Do Term Insurance pay in case of Accidental Death?

Yes, term insurance pays in case of an accidental death. The sum assured or cover taken under the term plan will pay the claim if the death has occurred due to any reason, be it natural or accidental death, or death due to some illness.

There are certain riders (additional benefits) such as accidental death benefit, permanent disability rider and critical illness rider. By buying/adding these riders to the policy, a policyholder can ensure that his nominee will get an amount over and above the basic sum assured (due to any of the rider-related incidents).

2. Does Life Insurance covers death outside India?

Yes, term plans cover death outside India provided the policyholder has updated this fact with the insurance company. He needs to mention that he now lives outside India. Just like change of phone number, address or nominee, there is a facility in the policy service form where the policyholder has to mention that he is going abroad.

However, if he is going to a country that is marked as unsafe like Pakistan, Burma, Somalia etc., then the company will decline this facility. Otherwise, this cover will be valid in other countries like US or UK.

3. To what extent Pvt Insurance companies investigates death compared to LIC?

There is a difference between early claim and normal claim. If a claim arises within the first two years of buying the policy (This period varies from company to company), the company investigates extensively before settling the claim.

You can very well understand if someone has a cover of Rs.50 lakh by paying Rs.7,000 annually (And he has taken this policy on monthly basis, i.e. paying around Rs.600 monthly), then the company is at a great risk. Hence, the company will doubly check everything to settle the claim.

In normal claim, premiums are paid regularly and the policy is in force for a long period, say 12 to 15 years. In these cases, there are not much issues in getting a claim, be it LIC or any private company.

4. If I buy a term insurance policy today, can its premium change in the future?

Unless and otherwise it’s mentioned in the policy document. Premium of a term insurance remains the same throughout the term of the policy provided everything remains the same with the policyholder. That is, the policyholder has not developed any illness or any smoking/drinking habit.

On declaring any such thing, company might apply loading and thus the premium amount changes.

5. What if a person becomes a smoker after some years of taking the policies?

If the policyholder has developed any habit, like drinking or smoking, after buying the policy, he generally does not have to disclose this fact to the company at all, unless it’s clearly mentioned in the policy document

6. What if a person was a smoker long back but not at the time of taking the policy?

Depends on the policy, but just for example, the Kotak Life Insurance proposal form mentions that the client has to declare whether he was a smoker or drinker earlier also even if he has left that habit long ago. Please see page 4, question 10.3 of this document . However, I am not sure about other companies. Also, it depends on the company whom they consider as a non-smoker at the time of issuing a policy.

For example: Max New York Life Insurance, for its Platinum Protect (term insurance), considers people, who have left smoking more than three years ago, as non-smokers. So please check the company’s rule 🙂

7. What kind of deaths are not covered in term insurance?

Some important facts, which most of the people are unaware of, are that most companies exclude “Death due to Terrorist Attack”. Although such claims are settled on humanitarian grounds later on when the nominee approaches Insurance Regulatory and Development Authority (IRDA) but such exclusion is there in most companies.

Other important fact, which public at large is unaware of, is that insurance companies do not cover death due to war or natural disaster like earthquake/tsunami. Because in these cases, death toll is high and the claim to be settled runs in crores of rupees which is difficult to settle by the company all of a sudden.

8. How to take care of claim settlement in case of more than two policies?

The very first thing, in these cases, is to declare in the proposal form that you already have a policy from an XYZ company. (There is a column in every company’s proposal form, which a client has to fill if he has an insurance policy from the same company or any other company).

Once such information is provided, then at the time of claim, the usual practice is to submit the Death Certificate to the insurance company with whom the policy is running for the longest period. Other companies are then informed of the procedure due and an acknowledgment from the FIRST Company is provided to them which are accepted by other companies.

Moreover, of late, it has been reported that generally insurance companies do not ask for an original death certificate to settle the claims, even a photocopy of the certificate will do. So be alert while filling the form and provide all the information about your previous policies to prevent even a minor problem later on.

9. Can NRI’s buy Term Insurance?

They can, but there is a catch. As a general rule, a person has to be resident in India to take up insurance policy from an Indian Company, reason being the documents required by the company like Address proof/age proof are to be for some place in India.

Moreover, if the Sum assured required is more than 50 lakhs or so, customer is required to submit his financial papers such as last 3 years ITR or Form-16 which again should be done in India only. Last thing, medical tests would be done at some medical center affiliated to the insurance company near the address of the client which again should be in India.

So these are reason why insurance might have been declined to some NRI.

So one way which might work is this , If a NRI wants to take Insurance, then on his/her next visit to India he should submit his proof of residence, age, last 3 years ITR etc. and get his medical done at his Indian address. This way he can get his policy issued very easily.

However, there is no need to complicate it and in-case you are out in some country and plan to be there for next couple of years, the best thing would be to take term insurance from your country of residence and later when you come back to India, you can buy term insurance that time.

Watch this video to know some more FAQ’s about term plan:

Comments Do you have any other doubts in Term Insurance which are not covered here? Which one out of the above 9 did surprise you most?

The inputs are provided by Dhawal Sharma, who is an agent for Kotak and Max Bupa.

From long I could see that their is a need of a good platform for you all to ask questions and get them answered . We have a lot of smart people on this blog and why not utilize their knowledge in answering everyone else doubts. So I was working from last few days on a Question & Answer platform which has neat interface structured way of asking questions and other cool features. So finally I have have a forum which is very neat and has a very simple interface to ask questions. Users can register there and then become a member and help others to solve their queries and also share new things which they learnt. Dont forget to register and ask questions to win some prizes (read till end) . Click Here to go to Forum

Some features of the forum

You can ask a question and give a category like mutual-funds , real-estate , life-insurance etc along with tags to them .

Other readers can reply to questions asked

The best thing about forum is that you earn points when you give a great answer and others like it (There is a thumbs up or down button with each reply.

Top 5 users with highest points are displayed on the forum

For each user you can see all the questions asked and answers by him.

Another best thing about the forum is that each user can have his profile page and can showcase his information about his website , twitter and Facebook profile and all the questions and answers he has contributed to. It also shows how many votes you have got from other users who liked your answer and this helps in showcasing your knowledge. You can also provide your description about your self in detail so that others can know you . I would request every one here to get involved in the forum and ask questions , how ever silly they are and there are many (really many) smart people around who can answer those questions . I can guarantee they will not be unanswered (may be late answered) .

Prizes

Top 3 winners

Within next 30 days starting from today, the top 3 users will get book called “Retire Rich Invest” by PV Subramanyam delivered to their home 🙂 . The 3 winners will be

User with top number of points One random user from the list of all users

User with most number of answers given (one liners just for the sake of answering will not be considered)

User with most number of questions asked

100 Complimentary gift for registrations

For the first 100 people who ask any question, I would send them

A personal finance management excel sheet

An ebook on Mutual funds 🙂

Winners will be announced after 1 month . Note that users who have already registered would be considered 🙂

Do you face issues while dealing with your Insurance Companies ? Do they dont answer you on time or dont entertain your genuine concerns on time ? Are you having a problem with Claims or other issues with an insurance company ?

Should you Complain ?

Incase you are facing issues like unsatisfactory answers , no replies on time , delay in replies, taking matters for granted and not treating you properly, any misselling in Insurance, you can complain to IRDA about all this , its just a call away, hence better use the facility and dont feel like you are not powerful enough. You can also mail Insurance companies and cc the IRDA email id for complaints for faster and better reply, but only incase you are facing issues , dont spam them 🙂 . Here is a nice Video Advertisement from IRDA called IRDA – Apki Suraksha ke Liye . I hope they do things in real life also the way they show in video 🙂

Call centre

IRDA (Insurance Regulatory and Development Authority) has started a new service where you can approach by phone or E-mail and complain against your Insurer. There is a call centre started by IRDA for registering grievances on policy-related matters. The call centre will provide an easy and convenient way to bring complaints to the notice of the IRDA. the Toll Free Number is 155255 and Email for complaints is [email protected] . Before the complain, you can approach the Insurance Ombudsman where the dispute involves amount lower than Rs 20 lakh. You can find the contact mail address of the Insurance Ombudsman of your region from IRDA’s Web site.

Do you think its a good resource and would be of help to consumers or will fail just like other projects ? Comments ?sha

We have discussed Buying vs Renting in previous articles. This post is not about saying which method is superior. While buying a flat/house is everyone’s dream, there are some very important questions one needs to think about before buying real estate property. Most buyers aren’t putting in enough thought, about some critical points (which they need to). One reason could be that they are far too obsessed with increase in value, are overconfident about the returns they can generate in real estate in long run or probably because these critical points haven’t yet crossed their mind. But if you are thinking about buying real estate, you should be aware of these points…

1. What is the Construction Quality of the house & what will be its condition after decades ?

If a property comes from a great builder, does it mean it will be in existence or in great condition after 40-50 yrs? What will be the condition of the building or how much it will be in demand by others at that time? Most of the buyers think about immediate requirement and may be 10-20 yrs hence. But should your vision be just 10-20 yrs when you are putting such a huge amount in Real estate? Also real estate construction is going to continue for next 20-30-40 yrs for sure given the amount of demand in our country . So who all are going to invest/prefer in your house which is 30 yrs old in 2033 ? Will there be a situation when the prices instead of appreciation, actually starts depreciating because of bad condition ? To understand what I am saying just look at some building/flats which are constructed before 20-25 yrs in your city , look at that and ask yourself “At what price are you ready to buy it? , or do you at the hand want to buy it or not?”

How many of us have seen houses which are 50 yrs old today? Not many; houses which are 50+ yrs are a handful. I know when I say this, it’ll cast a pall on the quality of builders in these times. Already there are enough instances where quality construction is compromised and owners do not get the property in the same condition as they were promised! . (Learn some tricks of understanding construction quality here and here)

Another thing which happens is when a person gets a house in possession the house is all well-built, its shining and everything looks perfect. But is a healthy looking person also with high stamina? Can we judge a houses’ stamina and internal strength on how it looks, how jazzy its tiles are and what a wonderful balcony it has? No! . We really need a long time like 30-40 yrs to really have a good insight in how strong a house is. Anything will last first 10-20 yrs . Here is a video which shows how a real estate buyer got his Flat in bad condition from one of the most reputed Builder and not at all in what they were promised . Looking at the video , I don’t think the house will last for more than 30 yrs .

2. Where are you going to be there after 20-30 yrs ? what are your future plans ?

Most of the people keep changing our jobs in starting of their career . An average situation would be that a person changes his job in atleast 3-4 yrs (in the software industry at least). But at the time of buying a property, a lot of people do not think much about this. They make believe that this, is the final job or at least a “long-term job”. Then, once they buy the house, they are almost stuck (Link) .

A lot of times, they don’t take risks in career and don’t want to take up another exciting job or a better opportunity in other city or much far place in same city, because of the “Comfort Zone” they have created for themselves.You have to be really clear about this point. A lot of people travel back from abroad to start their new life/business in India and the first thing most of them do is buy a house. I would recommend better get settled properly first, start your new work, make sure the stability is there and then go for commitment of a house. (Read this comment)

Not just from career viewpoint, you also have to think about retirement and the post 50+ age point of view . If you are age 30 today, are you going to work for 30 yrs in Bangalore/Delhi/Mumbai etc and then live in same city to enjoy your retirement? Do you think your retirement life would be wonderful in City of Mumbai or Bangalore? If yes , then go ahead.

But personally I think I will be working in a bigger city and then post retirement. I would like to settle in a smaller city or may be my home town. So if you also think that come coastal region or some smaller town or home town village is your post retirement destination, then not buying a house can be your choice.

3. Compromise on Living style and Mental Fear ?

You also have to be clear on what kind of life style you want to live in your life, because after you take Home loan , then comes all kind of issues like

Fear of losing the job and not able to pay off the loan

Not able to live your life comfortably and not doing all the things in life which needs more money as you are committed to your Home loan

Not able to take high risk and satisfying job in life because of the commitment , One reader who owns a company told me that a lot of talented people do not join his company even though they have better work and opportunity to do what they truely love , just because of the uncertainty a startup brings with itself .

The finding of an exclusive CNN-IBN poll on the economy reveals that one out of two Indians is scared of losing the job. The poll, conducted across seven metros, also shows that Mumbaikars are one of the most worried about their job prospects. Link

A lot of people take more risk than they can handle and it leads to traumatized life , which effect health, Strainful life at Home, unejoyable life for many . Though on extreme end, but some cases might also end in Death .

Pune: A 31-year-old man allegedly committed suicide by hanging himself from a ceiling fan at his residence in Indrayaninagar in Bhosari. The incident came to light only on Wednesday morning.The Bhosari police have identified the deceased as Piyush,alias Kishore Muralidhar Mahajan,of Indrayaninagar,Bhosari. The Bhosari police said that Mahajan had been disturbed ever since he had lost his job.

He was finding it difficult to pay the monthly instalments for the flat he had recently bought.The police have recovered a suicide note which said he was committing suicide because no one was coming forward to help through his bad times, the police said.

Source : TNN

How to Save if you are living on Rent ?

Incase you are not planning to buy the house, you can always invest the money in a way that you can buy it later after some year or at the time of retirement. Long term returns from real-estate have been in range of 10-12%, but even if we take it to be 12-15% , We can invest our money in some equity which can deliver similar returns . You can put money in ETF’s or Index Funds and let your money grow overtime and buy real estate at some later point .

Conclusion

As I said previously, it’s not a buying vs renting debate. It’s all about thinking well in advance about your decision and knowing all the aspects of buying a house. If you are clear about all the points mentioned , then you can go ahead and buy anything.

Want to invest in the best mutual funds in India? Read on. I have compiled a short list of Mutual Funds which are top mutual funds in the Equity Diversified category. These are long-term winners in their categories and have proved their performance over the years by beating their benchmark and category average by a good margin. These are non-tax saving Equity diversified mutual funds that are large-cap oriented. Remember that I am giving a list of funds. These are funds that have more than half allocation in large-cap oriented companies and around 50% of their money in the top 3 sectors they hold. Based on these criteria, I am putting 7 best mutual funds along with analysis, some of these are very old and some are relatively newer. (last year list)

List of Best Equity Mutual Funds

Source: valueresearchonline.com

Portfolio & Sector Allocation

All the above funds have returned around 20% or more in different time frames consistently, which is very encouraging when you want to invest in these funds. However our concentration this time is large-cap oriented mutual funds, we are not including funds that have a high concentration in midcap or small-cap funds. Let’s look at these mutual funds share in Large or Giant Companies. My criteria were to have at least 60%+ in Large/Giant Companies and around 50% allocation in the top sectors they invested in. We also have funds expense ratio which is around 2% for each of them. Read Magic of SIP

Source: valueresearchonline.com

Fund Manager and a Brief Overview of Mutual Funds

Past performance is just one of the criteria we can look at, but it’s not enough and not a guarantee of how it will perform in the future. Let’s also look at who manages it and how these funds have done so far overall as per their mandate and investing philosophy. Please note, that we are talking about the Growth option here and not the dividend option.

HDFC Top 200

HDFC Top 200 is one of the most well-known Mutual Funds in the country. It’s an amazing performance of 26% CAGR in the last 14 yrs is proof. 10 lacs invested in HDFC Top 200 since Inception is worth 2.54 crores (non-taxable) today compared to 30 lacs in FD (taxable). Some achievements of funds are that in the 2008 bear market, HDFC Top 200 was able to restrict its fall to 45% only, which was 11% less than its benchmark and 8% less than its category. Prashant Jain is the Fund Manager of HDFC Top 200 and one of the best known and famous Fund managers in the country with a long term experience.

Prashant Jain’s Investment Approach: “The criteria that go into selecting stocks/sectors are quality, our understanding, growth prospects, valuation of businesses and the composition of the benchmark – BSE 200.”. The fund has good 20% allocation in Midcap or small-cap stocks which gives a kicker in returns.

DSPBR top 100 is not a decade old fund, but its performance is strong enough to say that it’s one of the best in the category as of now. The fund has given enough proof of its performance like even in the first year of its launch it gave an amazing 129% return beating its benchmark by an “oh my god” 29% return:). It also showed its capacity to restrict loses in the bear market of 2008 by falling by only 46% compared to its benchmark which fell by 55 %, thereby giving a better performance by 9 %. The best thing I liked about this fund is that this fund has provided very strong performance by mainly focusing on large-cap companies, the fund allocation in Large-cap companies stands at 94% which is outstanding. This clearly shows the competence of Fund manager Apoorva Shah who is managing the fund for the last 3 yrs.

Birla Sun Life Frontline Equity A

This is another winner in the long run. Over the years Birla Sun life frontline equity has consistently outperformed its benchmark by a good margin. During the market falls of 2004, 2006 and the big crash of 2008 and early 2009, This fund was able to restrict downsides better than its benchmark. The fund is largely Large Cap oriented, however the fund is known to take some risks in Midcap space and hence has seen one-quarter and its first year lagging behind its benchmark, but that was not a prolonged behavior, over all it has done great. The main reason it came to top in performance was the entry of Mahesh Patil as the fund manager in Nov 2005.

HDFC Equity

This fund is for long-term investors because HDFC Equity does not hesitate to take risks. Having a good allocation in midcap/small-cap companies, Its performance comes by being invested for long-term, which means short-term volatility in its performance. Being 15+ yrs old fund, have shown its performance over and over again, this one is for people who really like to play with mutual funds on a long-term basis. The fund manager is again star performer Prashant Jain, who took over this fund in 2003 and the fund has never looked back. Just to give you a flavor, the fund in 2009 has given 30% more than Nifty Index and in the last 1 yrs itself, it has given 42% return compared to just 15% from Nifty. You can count this one as an aggressive large-cap fund for investors with a strong heart and long-term vision

UTI Opportunities

As the name suggest, UTI opportunities are for you, only if you a risk taker and like to bet on different opportunities available in the market. As per the mandate of UTI opportunities it looks at the gaps available in the market and the sector and pics the stocks which are really undervalued and might outperform in the future. As per the fund mandate, the Fund manager dynamically shifts between sectors depending on the macro economic outlook and opportunities available in the market. This means the potential of a huge upside as well as the risk of getting wrong. After Harsh Upadhyaya took over in 2007, the fund has done wonders and has given returns double than its benchmark, which is impressive. So if you a kind of investor who likes to take chance on opportunities, UTI Opportunities should be in your Portfolio.

Reliance RSF Equity

Reliance RSF has shown some impressive performance over the last some years. However the fund is fairly aggressive in nature and is known to take risky calls whenever it finds good opportunity, despite being called a large-cap fund, Reliance RSF has large amount (45%) of portfolio in small and mid-cap stocks at the time of writing this article, The fund did not really do very well when it started, but within a year it came on track and then showed good performance. Remember that this is a risky fund and can be actually compared to mid-cap funds in some sense given its nature of taking risks. So it might not suit you if you like to take long-term calls and want to be on the safe side. The fund is also known to churn its portfolio faster, so be cautious.

UTI Dividend Yield

This fund is really special. UTI Dividend Yield is another gem in the basket of Diversified mutual funds with a different style of investing. This is one fund, which has a woman for a fund manager in Swati Kulkarni, who has done a wonderful job in managing the fund till now. As per the mandate, the UTI dividend yield fund should make an investment of at least 65 percent of the portfolio in equity shares that have a high dividend yield at the time of investment. The fund has managed to successfully deliver on its commitment and has never deviated from its words. That’s called ethics and focus. Due to this, the fund has given a strong performance and because of its nature of strategy, the downfall is always restricted well. Ladies would like to invest in this fund given they like to play safe and it also comes from a lady fund manager 🙂 (Women & Personal Finance in India)

Which one should you invest in?

Remember that you have to take a call based on what your time frame is and which fund suits your requirement, Overall, if you are too confused in choosing the fund, I would say the best thing would be to choose any, randomly and invest rather than delaying your decision because of confusion. Another thing which you should understand that this is not an exhaustive list. There are enough funds other than these which could have been here in the list, but I have not included them as these 7 funds were the one which came on the top as per my criteria and also because I wanted to limit the number of funds to a single digit so that one can choose with less confusion. Also, make sure your asset allocation is correct

Disclaimer: Note that these funds are pure equity funds and just because they have performed excellently in history does not make them future star performers. This is just an assumption, that they will keep doing great even in the future given their investment style and integrity in management till date. Also, you have to make sure you review your investments every year so that you throw out the laggards and pick better funds. Expect around 12-13% in the future even though they have high potential. This article should in no way be treated as an encouragement to invest in these funds. Your decision is purely yours 🙂

Comments: Which other funds did you expect in this list? Do you have other funds’ names which deserved to be here according to you? Do these funds suit your requirements?