This is a guest Article from a fellow blogger friend and a very good Technical Analyst, Nooresh Merani. This is an interesting article where he presents how a profile of a Day trader looks like.

A part of this article was published in May 14th Issue of Money Today Magazine. I hope it would be a good read for everyone , Even If you are not related to Trading , you will come to know what is Day trading and how it can be a full time profession and very rewarding one . Read the article Below .

THE JOB = Day Trading

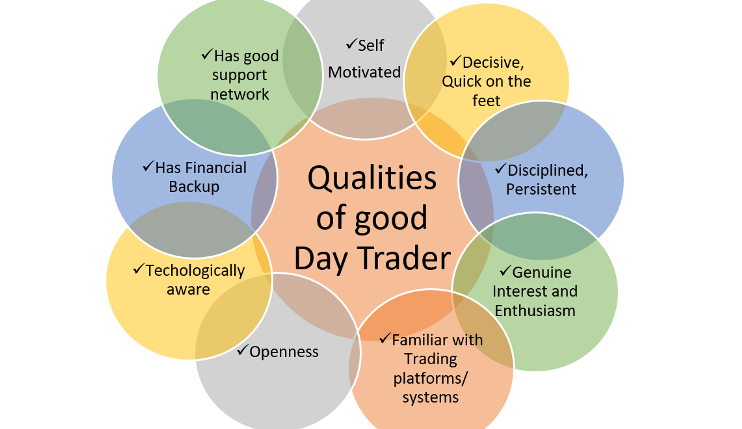

Job description: 6 hours a day / 5 days a week which requires hardly any physical activity apart from grunting or swearing in anger or thumping hands, tables and chairs in happiness.

Desired Profile: The desired candidate should be good at accounts and quick at using the computer keyboard or mobile keypads. No formal education or age bar.

Company Profile: It’s one of the oldest organizations (BSE is formed in 1875!) which is open to all candidates provided they have capital to trade with.

Remuneration: The salary has no upper limit but the candidate has to forego a small amount as brokerage/ taxes on the transactions.

The above job description seems a dream job!!

The profile of a day trader is not as rosy as it seems as they don’t have a fixed salary, instead they have to risk a security deposit (trading capital) paid up with the company (exchanges/brokers) which may be blown off in few hours, days or weeks or years.90% of Traders pay salaries for the rest 10%.

Trading is one serious business and a highly disciplined profession but, a large section of traders who don’t have this attitude get thrown out of the system very quickly. A trader learns from the mistakes, accomplishments through his trading career and by honing his technical and intuitive skills.

Initial grind:

Every traders goes through the initial grind (sometimes recurring) of losses, depression, self -realization and more.

A must Quote for every traders’ desk, “People who learn from their own mistakes are Wise, People who learn from others mistake are Wise and Lucky and, those who do not learn at all are Traders (Suckers)”

So, to be successful in trading, the most dynamic profession, where even a richest man can’t afford an hour’s lunch break (the Gujarati Thali would cost somewhere in Lakhs!!), one needs to learn, evolve, adapt and be disciplined. Always learn from the past, apply it to the present so that you can gain in future!!!

A Traders Day!

Pre-Morning work:

First thing a trader checks is how Dow Jones, European indices performed overnight and the current situation of Asian markets. SGX Nifty in Singapore opens up much before India so a trader gets hint of Nifty opening.

The trader makes modifications to the stock lists and observations made for the day. Technical, Pivot and data traders are ready with a list whereas system traders rev up their mechanical engines which generally don’t deliver much.

Trading Hours:

Although every trader has to see the ticker on his computer monitor for prices, but, there is a section of traders who only rely on ticker reading, which is a study of price & volume fluctuations. For best results, a combination of intuition, ticker reading and knowledge of technical analysis is a must.

Indian markets are one of the most volatile ones and it’s a common saying out here – Nazar hati durghatna ghati (Moment you get your eyes off you will meet with an accident). So a trader has to be attentive and nimble footed to make split-second decisions and follow the personal trading style/rules.

Post Trading Hours:

This is the best time for the trader to catch up on a snack or freshen after finishing of the calculations and noting down the open trades or the profits made in the day.

Analysis and Self-Evaluations:

The amateur traders don’t realize that this part of a trader’s life is equally important. Technical traders go through their charts; mechanical traders test their system to come out with a list of possible stock trading ideas for the next trading session and evaluate the current positions.

Trading as a profession has the most ups and downs with terribly bad trading sessions and equally high performance sessions. Every trader needs to keep evaluating, modifying and optimizing their trading styles to stay in the loop or the market knows a way to kick you out.

Latest Experience with the Screen!

Although I and many of us traders do follow the above plan but human nature is frail and one does make mistakes. One thing I have realized with experience is if you make a cheap mistake (small loss) early you would make a killing next time around by not repeating it.

The last mistake I made off late was to pre-empt and anticipate a big down move in 2nd week of March which didn’t come but luckily got saved because of stop losses and the screen. The next time around I did the simpler thing of re-acting to the ticker sense.

My one such encounter with markets was on 15 April 2009 when Indian indices outperformed global indices.

Many traders were yet again caught on the wrong side of the trade by watching the performance of Dow Jones overnight.

The index opened lower and drifted lower. But, ticker did not show signs of weakness and out of index counters continued to gain strength. What lot many traders missed out was, that Hang Seng (Hong Kong) was up 600 points on 14th March, the day Indian markets were closed due to a holiday.

Any technical analyst would confirm Hang Seng bears the closest co-relation statistically with India. So, this simple observation kept my bias bullish though the index was negative to start with.

The ticker was purely biased towards the mid cap segment in the last few sessions so my focus was on them.

We kept on holding to the previous open positions (namely Crompton, ks oils, guj nre, gtl infra, ghcl).

Also, seeing the momentum, added on to my technical picks Dishman Pharma, Everonn & Crompton for the day at higher levels then opening which gave awesome moves of 10% + in the day!!

Sensing that the up move was backed by nervous morning sellers squaring up, we booked out of previous positions to reduce the risk exposure and raising stop-losses to cost to conserve gains. A combination of aggressive buying along with disciplined money management did the trick as index closed 200 points lower the next day.

The learning from above experience was “Respect the Screen & Markets are Supreme”. A Trader looks for intuitive hints from the screen and doesn’t ask why it’s performing so, but, just follows it on the path to making money.

Above all would like to end this with few words of wisdom in Gujarati – Market Ni kamai market ma samai – (Money made in the market, stays in the market). A wise trader makes money and takes it home regularly!

Happy Trading!

Nooresh Merani , Analyse India

Blog: https://nooreshtech.blogpost.com

Website: www.nooreshtech.co.in

Email: [email protected]