Today’s article is my favorite, Today we will see that what is the biggest secret of Generating Long term Wealth.

Most of the people run after choosing great Mutual fund and choosing right policy, but they do not understand the most important element of Investment Planning, which is Early Investing.

In this article we will discuss how important is Early Investing, We will see that what you contribute early in your Life is what matters the most.

I did some Excel calculations and found out some important Rules you should remember. All the Examples in this articles assumes 12% or 15% CAGR annual return over long term (30+ yrs). Lets see some Important Ideas you should keep in Mind.

If you are reading this article in Email, you wont see important charts and graphs, make sure you visit the blog for this particular post. thanks

The amount you invest does not increase drastically when you cut your Tenure by huge Margin.

What I mean to say here is that if you have a goal of generating a fixed amount at the end of a long period like 30 yrs and If there are two cases

- Case 1 : You invest amount A per month for 10 yrs and then let it grow for next 20 yrs .

- Case 2 : You invest amount B per month for all 30 years .

In this case amount A will be too big compared to amount B. It would definitely be more, not by great extent. Lets take an example. If you want to generate a corpus of 2 crores in 30 yrs and you assume a return of 12% annually.

You need to invest Rs.5666 per month to achieve this target if you can invest for whole 30 yrs. But what if you want to invest only for 20 yrs or 15 yrs? In that case how much money you need to invest per month?

The answer is Rs.6065 (20 yrs) and Rs.6611 (15 yrs). So you can see that the monthly contribution required to meet the same goal does not increase drastically even if you reduce the tenure by 10 or 15 yrs. See the chart below (Click to Enlarge)

The Tenure and amount required are :

The Tenure and amount required are :

30 yrs : 5666

25 yrs : 5801

20 yrs : 6065

15 yrs : 6611

10 yrs : 7903

In the above chart you can see how “Monthly Contribution Required” increase at very small amount if you want to save the investing years later in your Life . Download this Monthly Contribution Calculator to calculate how much you need to invest monthly for your Financial Goals.

Even if you cut your Contribution at the end of the Tenure, It wont affect the final Corpus Drastically.

What this means is that If you want to invest for long term and in case you are not able to invest for many years at the end, the final amount generated will not be drastically less .. The difference will not be worth a concern.

Lets see an example, If you want to invest Rs.4000 per month for next 30 yrs (retirement amount, see 6 steps of Retirement Planning) and you assume 15% annual CAGR return, you would be able to generate a corpus would be 2.8 crores, But in case you just invest for 20 yrs and don’t invest for rest 10 yrs, in that case your corpus will still be 2.69 crores, 96% of the original amount.

If you invest for 10 yrs and don’t do anything for 20 yrs, still you will be left with 2.19 crores. You can see that how your corpus is not getting affected a lot because of laziness in investing.

If you are successful in early investing, your 90% job is done, even if you are not able to invest money in later years, your final amount will not be affected a lot.

See the chart Below (Click to Enlarge). See this Video to understand the CAGR or Annuity Calculation, Or see this Article if you are on Slow Bandwidth.

If you see the chart above, you can clearly see that in the first 15 yrs, the total corpus at the end does not decrease with great rate. Its more than 2 crores even if you miss 22 yrs (thats more than 70% of total tenure).

If you like the knowledge we share on Jagoinvestor, Fill the Fan book to tell us why and how much you like it

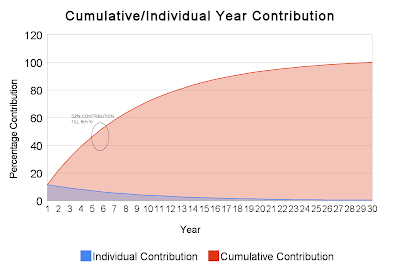

Investments Done in Initial years are the main chunk of your Final Corpus

What this means is that what you in the start has major chunk in your final corpus , the money you invest at the end generally has no major contribution because the money compounding has done its work on the money you invested in the start , not end .

See the chart below . .

The time frame of this example is 30 yrs investment with assumption of 12% annual CAGR return. You can see two kind of lines here. Blue Line shows contribution of a particular year in the final corpus and Red line shows cumulative share of years till then in the final corpus.

The time frame of this example is 30 yrs investment with assumption of 12% annual CAGR return. You can see two kind of lines here. Blue Line shows contribution of a particular year in the final corpus and Red line shows cumulative share of years till then in the final corpus.

If you see the chart and concentrate on 6th yr, you will realize that what ever you invested till 6th yrs contributes to 52% share of your Final corpus which means that if you stop at 6th year, you will still be able to make 52% of original amount.

You can also see that last 12 yrs contribution helps in 10% of final corpus, this we saw in the first chart itself.

So at the end, lets see some numerical facts which will help us understand power of early investing.

- “Investing 1500 per month for 10 yrs and letting it grow for next 20 yrs” will generate more than “Investing 1000 per month for 30 yrs” @12% return.

- “If your Original time frame was 30 yrs and later you want to cut your Tenure by 50% , you corpus will decrease just by 14%” @12% return .

- A : “Investing 5000 per month for 30 yrs” B : “Investing 6,000 per month for 15 yrs and do nothing for next 15 yrs” C : “Investing 11,000 per month for just 5 yrs and do nothing for next 25 yrs” Here, C will make 1.95 crores.

If you are a young person below 25 and you have 35 yrs in your hand and want to make 5 crores, If you start right now, you will have to invest just Rs.3,400 per month, But if you are later by 10 yrs, then you will have to invest more than 15,000 per month to achieve same target.

Are you on Facebook? Like and follow the Jagoinvestor Page or Join our Facebook Group

Conclusion

Start Early, The secret of Sound Financial Planning is Early Investing, not making excellent return or choosing great funds or buying multibagger stocks. If you can take little pain and invest more money now, then better do it, It will save you from lot of trouble later.

Please spend a minute to take these polls

Please put your comment and let me know how was the article and if you liked it? What do you think that early investing is not the most important element of Investment planning, if not, what other thing do you think is the Key 🙂

Source: Valuereserchonline.com

Source: Valuereserchonline.com