“An ounce of prevention is worth a pound of cure” I see that most of the people these days have bought wrong products like ULIPs, ULPPs, Endowment Policies and unsuitable Mutual funds (which they are not aware of most of the times) and then when they do come to know about it, they don’t have much choice left.

They either have to live with it or they have to lose a lot of money to correct the situation.

In this article we will see some thoughts on why we should focus more on “Prevention” and not “Solutions” for a bad situation from Financial planning perspective.

A Small Story

There once was a little boy who had a bad temper. His Father gave him a bag of nails and told him that every time he lost his temper, he must hammer a nail into the back of the fence. The first day the boy had driven 37 nails into the fence.

Over the next few weeks, as he learned to control his anger, the number of nails hammered daily gradually dwindled. He discovered it was easier to hold his temper than to drive those nails into the fence. Finally! The day came when the boy didn’t lose his temper at all.

He told his father about it and the father suggested to the boy that he should now pull out one nail for each day that he was able to hold his temper. The days passed and the boy was finally able to tell his father that all the nails were gone.

The father took his son by the hand and led him to the fence and said, “You have done well, my son, but look at the holes in the fence. The fence will never be the same. When you say things in anger, they leave a scar just like this one. You can put a knife in a man and draw it out.

It won’t matter how many times you say “I’m sorry”, the wound is still there. A verbal wound is as bad as a physical one. Friends are very rare jewels, indeed. They make you smile and encourage you to succeed.

They lend an ear, they share words of praise and they always want to open their hearts to us.”

The Story is encouraging and gives an important message. We all make decisions in life. Some of these decisions can prove very unhealthy. We make mistakes and then when we come to know about it, we try to figure out ways to fix the problem.

Making mistakes is not a wrong thing, we all do it at some point in life and taking measures to cure it is another great thing. But it will some times have drastic impact on you and your money.

Some of the mistakes we make are

- Buying Endowment Policies early in life due to pressure from our Parents and relative friends and continuing it for long.

- Taking less Insurance than required and leaving our loved one in risk of Financial instability

- Buying Risky and Costly products like ULIP’s without understanding them

- Not starting saving early in life when we could have done that easily

Watch this video of 4 biggest financial mistakes related to personal finance that every investor should avoid :

ULIPS

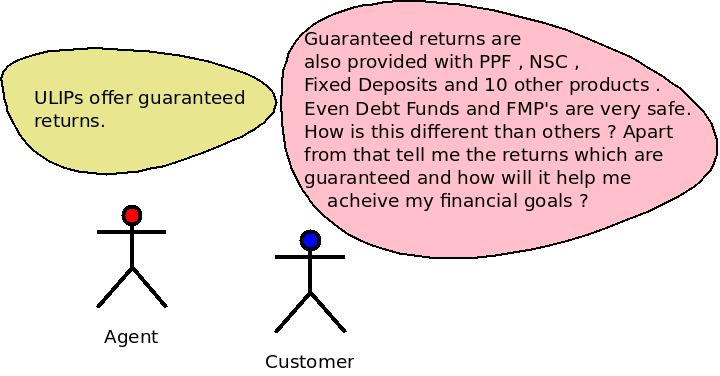

A lot of readers of this blog were sold ULIPs (they didn’t bought it, it was sold to them) without telling them the costs involved and sometimes promised with wrong returns (it was just an illustration and dependent on market condition, agents just said it was guaranteed).

Now when they come to know about it, they stop the premium payment and get out of it at right time, this getting cure for the problem but the damage has happened. You might not realise it, but the damage is big, some people have lost close to 80,000 – 1,00,000 in premiums or in costs.

One of the person I know has paid 4-5 lacs in premium and 60% was the cost in first year. Now he stopped the policy, that’s a loss of 2.5 lacs. If that same money is invested in some good Mutual funds for next 20 yrs and if we expect a return of 12%, it’s 24 lacs at the end.

This is opportunity cost. RS.2.5 lacs might look like a small or “chalta hai” kind of amount, think again, it’s opportunity you have lost. The amount can differ for different people but the lesson remains same.

Insurance

Another case can be of Insurance, most of us are still under-insured, even now!! Even after we know that Term Insurance is what we should take, still we are underinsured, that’s the risk. Once the disaster happens, it will be too late, you will never get the chance to cure it.

In fact you will not be there in this world to cure it and the outcome will be very horrible which you might not want to imagine.

Endowment Plans

Same with Endowment Policies, Investors who have taken Endowment Policies and are paying 50,000 per year for next 25 yrs. They do not realise what they are missing. You get 5-6% returns, that’s all! forget what agents promised or what was told to you. Endowment and money back plans are world-famous for “not able to beat the inflation” kind of returns.

So you are missing long-term equity returns of 12% at the least. So you are loosing 6% worth of returns. That’s loss of 45 lacs for the example I just gave you in long-term, what is the reason you lost that much, just simple laziness of not taking the action of “change” and restricting your mentality of “Equity is Risky”, that’s incorrect at least for long-term.

Late Investing

No matter what you always have some money to invest when you start. If you don’t want to invest, there will always be enough reasons to not have savings. Almost 99% of the people can live with their 90% of salary, whether they believe or not. Earning less is not a crime, it’s part of life, save what ever you can save, even Rs 100 is ok, but do something.

Some people can save more than 30-40% of their salary, but they are not doing anything about this! Don’t underestimate the power of early investing, Early investing is so powerful that it can compensate for big mistakes in investing later in life. If you are a 25 yr old person who needs 2 crores at retirement at age 60.

Assuming 12% return, you just need to invest Rs.6,000 per month to reach your retirement target. Imagine what happens if you feel that you can do a little late, how does it matter and all and actually start 5 yrs late, with the same saving of 6,000 per month, you will have just half of your retirement target, that’s 2 crores.

Imagine the cost of saving late by 5 yrs, You have to but down each of your retirement thing by 50%. That can be a big hit!!

What is the Solution

Taking measures to fix your messy situation is worth appreciation and we all should do it if we get into it. But on the first hand why to get in a messy situation. You don’t need to do fancy things to be in healthy financial condition.

A simple 5 things can save you from disaster

-

- Take proper Health and Life Insurance

- Make sure you don’t buy what you don’t understand

- Take products as per your risk appetite and proper time

- Do need based Investment Planning and Retirement Planning

- Start Investing Early in Life

Just practice these 5 Mantra’s and almost all of mistakes you make will go away.

Comments, what do you think about this? Please share your views.

You have to understand the real goal of financial planning first and then identify the areas you really need to concentrate on .

You have to understand the real goal of financial planning first and then identify the areas you really need to concentrate on .

This is not true! Any

This is not true! Any