Readers, I was working on building some basic calculators over the last month . They are ready to use now . The calculators are very basic and have a bare minimum look and feel , but works !! .

Please use them and provide any changes you feel should happen . one important point you should note is that all the figures are approx and the numbers you get might differ a bit from other calculators on net as the formula’s used might be on yearly compounding or payments have been considered at the end of the period rather than start . So don’t put much thinking on the exact numbers , take them as a general approx figures , anyways how does it matter if your retirement corpus is 4.53 crores or 4.58 crores !! 🙂

Look at this page for all the calculators listed at one place . Below is the list of all the calculators

Some days back I had written about GFactor concept for choosing a Financial Product based on 4 factors and formulating it in mathematics , Recently one of the writers for Business Bhaskar has copied the original idea of GFactor and republished it with same name “GFactor” and all the other names like “Trap Factor”, “R/R Factor” etc, without any permission from me .

This is not a general republishing of a general concept like SIP or Life Insurance that one can just change the wording’s and rewrite the same concept . It’s just the translation of the original idea and hence copyright violation. I have mailed the editor of the newspaper to look at it . The article was published in the online edition (Link) as well as print media (Newspaper Link) .

Update Jun 1 , 2010 : Business Bhaskar has resolved this issue with me and apolosized to me for whatever happened, they will republish the article with due credit to me .

Comments , please share your views on this issue ? How appropriate is it to copy content and translate it without permission ?

Last night I was having dinner with my friends and suddenly on of the friend realized that he has lost his wallet. The problem was not the cash in the wallet, or the cards. It was the misuse of the card and contacting card issuers to block the cards as soon as possible .

Have you found yourself in similar situation ever or have you lost your wallet which had many debit and credit card along with other important documents. Do you want solution for this problem ?

Here is the solution.

There is nothing like the shock of losing your wallet or purse with all the money and your Credit or Debit cards in it as these cards plays a significant role in our lives.

In India there are two service providers who provide this service of protecting your cards – Credit Protection Plan (CPP) and OneAssist.

If someone steals it by purpose or if you lost it and it goes in a wrong hand then there is a risk that the person may misuse your cards. To avoid this CPP is one of the good options.

What is CPP Card Protection ?

CPP Card Protection is India’s first comprehensive Card Protection service for use in the event of card loss, theft and related fraud.

If you lose your wallet or your handbag, simply make one free call to CPP. They will quickly notify the issuers of your cards to cancel your cards immediately, also they will provide emergency travel and hotel assistance to take care of you and help you get back home.

CPP Assistance Services is the part of CPP group which has already started services in other asian countries like Hong Kong, Singapore and Malaysia.

As per a report by Medianama, in January 2017 there are 28.8 Million credit cards and 818 Million debit cards in India

Every wallet on an average now a days contain one debit and credit card in cities . CPP has tied up with leading banks including Citibank, Standard Chartered, HSBC and Kotak Mahindra , Axis Bank , LIC and ICICI Bank to sell the CPP services. Read 5 tips for effectively using your Credit Card .

Features/Benefits of CPP:

Loss Reporting : Incase your cards are lost or whole wallet is lost you can call CPP on their helpline number and they will cancel all your cards immediately and will help you in replacing them after that

Fraud Protection : If your card has been misused then your get protection for it before or after the notification from your side . You are covered from 7 days prior to your loss report to CPP until your membership is valid.

Emergency Travel & Hotel Assistance : Incase you can’t pay your hotel bill or have lost the travel tickets or have money to buy travel ticket, CPP will arrange for your travel tickets for your return and will also help you pay your bills to the hotel . This applies to travel abroad as well. For Indian premium users they will also help you with Cash if you have lost cash in the wallet .

Document Registration : You can register important documents like passport, driving license, insurance policies with CPP which will ensure easy access if you should lose the originals.

Cash: For Indian premium users they will also help you with Cash of upto 20,000 if you have lost cash in the wallet.

PAN card & Driving License lost: In case you lost your PAN card with your wallet, CPP will also help you to get new PAN. There is no need to apply for that separately.

You can watch this video to know how CPP helps you..

Membership and Plans

They have three main plans and each plan have difference in the benefits they are providing. The plans are as follows:

Classic: single person membership

Premium: Additional membership to spouse only

Platinum: Additional membership to spouse and parents.

Besides membership they have differences in other benefits which they are providing and also their premium charges.

The membership plan is different as per the insurance companies or the banks from whom you are getting the CPP. The facilities provided by insurance companies are almost same.

You can pay the premium by master or visa card and the amount will be deducted from your account at the beginning of every year until you close for the plan.

There is a limit for ever benefit like Rs 1.5 Lac for Hotel Assistance and traveling and Rs.20,000 Cash in India only.

Procedure to apply for CPP services

Applying for the CPP service is a very simple procedure. Just follow the steps:

Fill the application form for the CPP service. These forms are available online on the website of the service providers or on the websites of the related banks.

Pay the premium fees as mentioned in the plan you have selected. Generally you need to pay full premium at the beginning.

Once you pay the premium fees the service providers will send you the welcome pack comprising the registration form, confirmation letter and a form of terms and conditions of your plan.

You need to fill the details of each card which you want to protect and come under the plan you have selected.

After filling the form completely, check it for the correction and send it back to CPP service providers.

Why Should you pay for CPP services ?

Incase you are using debit and credit cards heavily and carry bigger account balance than few thousands , It might make sense for you to protect your cards using their services .

It’s all about if you want to take risk or loss and fraud or not . The cost associated is not huge and can be considered, however I feel that card companies should have CPP built in with the card itself .

Things to remember before applying for CPP services

If you are paying for something then it’s your responsibility to check for every detail about that particular plan. Here are some important points you should check related to CPP:

Check for the benefits of each plan included in CPP before selecting any one of it.

Decide which plan you want to buy according to your needs.

Check for the premiums of the same plans at different service providers or banks.

Keep every detail of the payment of the premium.

Once you take the plan make sure you added each and every detail needed accurately.

Comments , Put your views on CPP and does it appeal you ? Do you think it will work with Indian Mindset ?

Retirement Planning is one of the most important aspects of financial planning. Here is a 3 part video series on Retirement planning which gives you a good idea of how to plan for it and how to think about retirement planning . Look at how to 6 Steps of doing Retirement Planning by yourself

Part 1

Part 2

Part 3

A very good book every one should read is “Retire Rich Invest” written by P V Subramanyam . Give your comments 🙂

How do you find out if a product suits your requirement ? What about a very simple calculation which can take into account most important requirements like lock in factor , complexity of a product , your requirement and its return and risk potential and tells you if it really suits your requirement. This Post will talk about a concept developed by me called GFactor , which is a score system for any Financial Product. You can input 4 factors and get a score for a product . So this GFactor score system will tell you about goodness/badness of a product. Gfactor stands for Goodness Factor .

What is GFactor ?

GFactor is a very simple rating system for Financial products which gives a score on a scale of 0-1 . 1 represents excellent , 0 means worse . There are mainly 4 factors which we consider when we design this GFactor .

Trap Factor (Liquidity)

RR Factor (Risk/return Factor)

Complexity Factor

Need Factor

Trap Factor

Trap Factor is nothing but its score for the product on scale of 0 – 1 for the lock in period. The more trapped you have to be in product , the more will be the Trap factor score. One important point you should note here is that you should also consider how much loss you have to take even after you can freely come out of the product . For example : Endowment policies trap you for long periods like 15 to 20 yrs . Even though there is an option to close the policies you loose a lot of money. So the trap factor of Endowment Policies will be more like 0.9 or 1 , where as Mutual funds (non tax saving funds do not have any type of locking period) . So they can have trap factor of 0.1 or 0 . In ULIP you are stuck for at least 3-5 yrs , only after the 5th year. So it can have a trap factor of 0.6 or 0.7 you can get out without any penalties . For term insurance there is no trap factor , you can stop the policy any time .

Years of Trap

Trap Factor

No Trap

0

1-3 yrs

0.2

4-10 yrs

0.5

10-15 yrs

0.75

15+ yrs

1.0

Risk/Return Factor

Risk/Return Factor is a factor which will evaluate a single digit score for its risk/return potential . This score takes into consideration both risk and return . You can look it as risk adjusted return potential . so this factor will determine the return potential considering the risk potential. To calculate this you should know average return and average risk figures of a product in its total duration . Lets see the calculation first .

Risk Return Factor = (Average Return – Average Risk)/Average Return

Lets see an Example in case of ULIP : Robert wants to buy some mutual funds for next 5 yrs . In these 5 yrs , as per the historical data , we know that he can expect an absolute 100% return on average (his money can double) , and if some thing bad has to happen hecan loose around 30% of value (the figures will differ for everybody) . So

In this case suppose the returns from FD are @8% .

Average Return = 16%

Average Risk = 0%

Risk Return Factor (FD) = (16 – 0)/16 = 1.0

Note : For term insurance , the return will be the max amount you can get and Risk would be amount you can loose all , which is total premium over many years.

Complexity Factor

Complexity score is a number you assign to the product, depending on the how complex of easy it looks to you . For example Mutual funds can be easy to understand for me , so I can put 0.1% for it a complexity, whereas NPS is more complicated to me , so I will put 0.5 . This means If it looks too complicated for you, then give a higher score, whereas if you understand it well, assign lower score .

For a normal person I would say ULIP is complicated , so we gave give a score of .7 or .8 or 1 ,depends on you, where as term insurance is extremely easy to understand, so it will get 0 or .1 , Mutual funds would be .2 or .3

Need Factor

Its a score given on the fact that how badly you need or require the product and will it be the best thing for you. One person may need it more than other, so the score will be different for different people. If you are not in a hurry, but your relative suggests you a policy , then it does not become a very high priority product for you, because you do not require it at that time, so you will assign a lower score to it . For a person who is in his 26-27 age and just married and has some financial dependents , His score for term insurance will be around .9 or 1 because he badly needs it . Make sure you know difference between your needs and wants

A person who is 45 , for him/her NeedFactor for Health Insurance would be .8 or .9

A person who is Extremely High risk taker and understands equity investing well , his need factor for NSC or FD would be low , say a score of .2 or .3 because he really does not need it and it does not suit his requirement also .

You should understand how the formula should be constructed. Out of the 4 variables, 2 scores shows strength of the product(Need Factor and Risk Return Factor), where as two scores are negative(Trap and Complexity Factor), so below formula should take care of this aspect .

GFactor Formula = (NF * RRF) – (CF*TF)

Lets take an example . Ajay is a 35 yrs old Indian working in a Software company, He has 2 kids and 1 wife 🙂 and 1 parent to support . His risk appetite is moderate and he cant take more than 20% downside in his investments at any given year . He has a home loan and a car loan at this moment and has just 10 lacs of overall savings . Below is the chart which calculates GFactor for some products considering Ajay’s situation. Understand that these numbers are for Ajay, it can change for you .

Products

Trap Factor

Return/Risk Factor

Complexity Factor

Need Factor

GFactor

Term Insurance

0

0.95

0

1

0.95

Health Insurance

0

0.85

0.3

0.8

0.68

ELSS

.25

0.5

0.1

1

0.48

ULIP

.25

0.5

0.4

0.4

0.1

Tax Saving FD

.5

1

0

0.1

0.1

Endowment Policy

1

1

0.5

0

-0.5

Rules

If GFactor value is more than .7 , you can consider that product as “Must buy. Go for it” .

If its more than .4 , you can consider it as “Average”

If its more than .2 , you can consider it as “Look for alternative product. Buy only if nothing else is available”

And if its less than .2 , then you must avoid it .

GFactor of a Portfolio

Just like we have Gfactor of a product , we can have GFactor of a Portfolio , which is average of GFactor’s of all the products in a Portfolio . Example

Term Insurance : 0.95

4 ELSS : 0.43

4-5 shares : 0.35

10 gm of Gold ETF : .72

EPF contribution : 1

3 months of Cash : 1

So average of all the GFactors = (.95 + .43 + .35 + .72 + 1 + 1)/6 = .742 . This is a good Score for a Portfolio , But I can do better than this . Whats your Portfolio GFactor ?

Conclusion

There are 4 main factors which matter when taking the decision regarding a Financial product , The above concept is my own thinking and It may not fit everyone criteria , but I am sure it would be true for most of the people , If you have disagreements , its fine . We subconsciously understand how there 4 factors affects our decision making process , but the idea is to put it into formula and get a Score out of it , so that we can compare and know how good or bad a product can be for us .

Ques tion

Can you design a better formula for GFactor which makes more sense that what I have given .

Do you think GFactor can be useful to general investor to take decisions .

Please share with me GFactor of your overall Portfolio .

Note : This is an old post , I am republishing it with changes

Do you read comments ? There is a huge amount of discussion doing on in comments section, however many readers do not find time or interest to dig into the comments and follow the discussions, I would say comments have more knowledge than the article itself , as there are personal experiences and knowledge from many different readers, there is a threaded discussion on some topic in comments, which are more lively and engaging. So if you are just reading articles and not comments, you are missing a lot of things . So I went through some articles comment one by one and consolidated some learning and facts for my readers . ( See Learning from Comments Part 1)

1) Partha Iyenger shares what will happen to your mutual funds units if you bought it from Demat account and Company went bankrupt

If your online distributer Financial institution and asset management companies in India are regulated by RBI and SEBI. They constantly monitor the balance sheets and other relevant data of these firms and the respective regulators have put together necessary steps to ensure that the investors are protected by taking corrective steps. For eg.. when global trust bank collapsed, it was merged with Oriental Bank of Commerce and clients/depositors who had funds/securities in dmat accounts were able to get it back or transferred to the new Oriental Bank of Commerce account.. The process takes a while but you would get it. In India, we have excellent systems and process (much better than developed world) partly due to conservative policies framed by RBI and others regulatory bodies. For more information on the GTB scam related to deposits and demat accounts, you can read the link here . Another interesting aspect is that your order verification (on equity and etf purchases/sales) is posted on the NSE site on the same day. Your can ask your broker for the unique order number for the trade executed by you. You can verify the stock, price, qty, etc through this unique order number in the nse site. The orders are archived for a period of 8 years!

If am not wrong, NSE is probably only one or very few exchanges to have this facility for investors. This is a valid documentary proof for transactions done by you, which you can use in case your broker fails to send you the contract notes or ledger statements or if there are any discrepancies. Apart from this, the clearing corporation ensures that investors are protected from defaults by members by acting as third-party and your transactions are cleared. For more information you can read the RBI circular here . Next, all asset management companies have to follow strict guidelines in terms of their financials as prescribed by SEBI. The foremost criteria is 40% of net worth of the AMC has to be brought in by the sponsor. A sponsor is a company/consortium/institution which would like to float the asset management company. It also appoints trustees who oversee the amcs. The trustees have the authority to monitor and replace the asset management company , if they fail to perform their duties effectively at any point of time.. This is apart from the regulators and government.. Of course, one needs to be more careful while choosing your broker and investment companies and constantly monitor news and events related to the company.. If at any point of time you get uncomfortable, you could pull out your investments and park it in other stronger firms. (Link)

2) Milind Kotibhaskar shares his experience with a ULIP Agent (over email with me)

Many years back, I was studying in the college and staying in hostel. One evening, one decent looking young man entered my room. He told me that he was from my home town and gave me few references. He thus established a good rapport with me. Then he gently told me that this night he has to leave for Delhi ( or Bangalore or such place ) to attend a job interview. But he has lost his train ticket and he does not have money to buy new one. This job is a lifetime opportunity for him, but he will not be able to make it due to lack of money. So would I be so kind as to lend him some money so that he can travel and attend the interview ? He looked sincere and genuine. I gave him whatever money I had. He thanked me and said that he will return my money as soon as possible. Later when I told this to my friends, they started laughing at me and said I will never see him again in my life, and that is what happened.

Years after, 6 months back, ABN Amro people visited me ( I have salary account with them ). All dressed nicely ( tie and all that ). They wanted to sell me ULIP. They made impressive speech, talked about the returns that I would get etc. All this to a fellow who has crossed 50. I think these people were no different from the conman that duped me in the hostel. I know mutual fund agents who persuaded their clients to sell their existing MF schemes and buy NFOs ( agents used to get very good commission on NFOs ). I know LIC agents who ask their clients to surrender existing policies and buy new one so that these agents can meet their annual targets and to earn hefty commissions on Insurance policies . I feel sorry for the conman who took few rupees from me, and if caught in the act, would have faced police action. Instead he should have become an LIC agent or ULIP agent. He then could have conned more people without fear of police action and got more money in return.

3) Partha Iyenger shares How Real Estate prices gets manipulated by handful of big players .

During the period of Nov 2007-January 2008, large number of high net worth investors got carried away by the bull market assuming that they could make quick returns by booking profits when the sensex moves to 25,000. A large sum of the money allocated for real estate investments (in parts or full) by these investors were moved to stock markets and commodity markets. When the markets crashed immediately, which they did not expect, they were struck. The couldn’t pull out the monies, due to losses. The real estate market which was also on a bull run till then, found the buyers who had shown interest earlier [some of them made advance payments], specifically in premium apartments, backing out. Read Real Estate Returns in India

Hence the Mumbai markets went through a period of correction (though the cycle was shorter) and picked up again gradually when the markets started its rally since April 09..In fact, some of the developers to speculate [through leverage as well] in the stock markets and move it back to their business.. As usual timing is very difficult and that’s why one of the problems faced in the last two years by real estate markets is ‘cash’.. Which means not completing projects in time!

The single word for this phenomenon is ‘liquidity’. I am afraid you could get reliable statistics on real estate, since India lacks transparency[ be it in title deeds or transaction mechanisms] and we are yet to have real estate investment trust vehicles or REITS which would help track data and give a better picture. It should happen soon… (Link)

4) Pramod Moudgill shares his excellent insight on how to look at Fund houses and Fund managers

a) Whether it has some discipline and process set for investments or it is only a One man show i.e. fund manager is calling all the shots. The former is always better.

b) Whether the fund is keeping an eye on the funds if they are being true to their mandate and the fund manager is not deviating from the mandate for the sake of returns.

d) What is the performance and association of the investment team with the fund house. Is it changing fund managers every year ? if so then a big problem.

e) I dont know about others but to me the important point is the credibility of the parent company.

Let us evaluate fund houses on above parameters

1) Sundaram has a strict cap that none of its diversified funds will invest more than 5% in a single stock (Except select focus – Its mandate is to remain focus), At FT the stock selection is done by a team of experts and the same is true with HDFC. These things make sure that one person can not skew the investments to his will.

2)Sandip Sabharwal is arguably the shrewdest fund manager India have ever seen. If you see the portfolio of SBI funds then you can observe that all the diversified funds had 90% stocks in common, so a global fund a contra fund a midcap fund and others were same despite their different mandates. Now look at DSP top 100 it doesnt have a single midcap stock, DSP midcap not a single large cap. Same with HDFC Top 200 and Sundaram midcap or Growth fund. When I invest in a large cap fund I know that I will be geting a large cap fund for sure. FT blue-chip and Prima do not have a single stock in common. Look at some good Equity Mutual funds

3) DSP has only seven equity funds and is winning so many awards based on that only. HDFC has only one sectoral fund. Sundaram recently has launched some new funds but if you compare these houses are conservative with new launching. They have every kind of funds and that is good. Look at Tata , Birla, Reliance they work like NFO Factory. The sole aim is to get money via NFOs.

4) Fund managers, – Prashant Jain is with HDFC for 10 Years, Naganath with DSP for a decade, Sukumar ans Siva Subramaniam with FT for over 12 Years. other that Anup Bhaskar no fund manager has left Sundaram in a long time. Can others (of course Nilesh Shah and Madhu Kela are there) boasts of such long relations.

5) Finally the corporate governance, Check yourself about the credibility of Sundaram and HDFC. Other two are internationally acclaimed.

OK that is the criteria I used, There are some others which may be fitting in these parameters but then performance is foremost and you can check about the consistency for these funds over many years. It has not been a flue. Keep a watch on IDFC and ICICI. Former is transforming itself and the latter is relatively new. Somehow I feel that 2010 will belong to these two guys. In the first quarter fall they have shown character. (Link)

Comments please , Did you like these comments and the learning ?

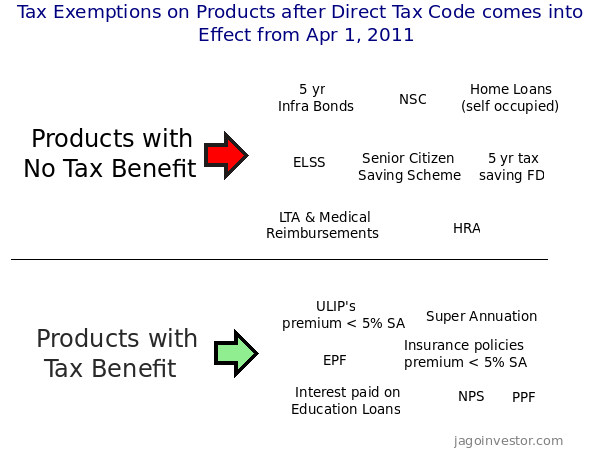

Direct Tax Code is the new proposed bill for changing the tax rules in India. If it comes into effect from April 1, 2011, it will change the whole taxation system and will change the way our taxes are calculated from years . The new tax code will have impact on Insurance Policies, Home Loans, PPF, Ulip, Mutual Funds, Shares and Taxation slab. A common man has to understand whats there in future for him so that he can plan accordingly. However the Direct Code tax is still in draft and might come into effect, but there is no guarantee. Experts feel that it can not come in its original form. Lets see what are the impacts on different investment products if DTC comes into effect .

Effect on Endowment/Moneyback insurance policies

As per Direct tax code, any amount you receive at maturity from an insurance policy (including bonus) will be taxed. However this rule will not apply for policies where;

In any given year , premium paid in a year is less than 5% of Sum Assured , and

The policy runs till maturity.

So if you have anyEndowment Policy or Moneyback Policy and in any year if you paid or will pay more than 5% of Sum assured as premium or make your policy as paid up in between, all the money you receive in the end will be taxed at the time of maturity. For policies where premium paying term is lesser than the total tenure, still all these rules will apply. For example , if you have a policy where sum assured is Rs 5,00,00; then there can be two cases where you will be taxed at the end.

First : If you pay more than 25,000 as premiums .

Second : Even if you pass this 5% rule , but you do not run your policy till maturity.

Effect on ULIP’s

The same rule applies to ULIP also. The first point is exiting before 10 yrs will badly hurt you from cost point, as all the Ulip’s are heavily front loaded and exiting before 10 yrs means the total cost is (commissions) turns out to be too much for you. Only if your total premium per year is less than 5% of the Sum assured, you can save yourself from getting taxed. But most of the Ulip plans in the country will not meet that criteria as majority of the policyholder’s pay much more than 5% of sum assured as premiums. A big number of policies have sum assured as 5 times of the premium, as it’s the minimum requirement of a Ulip policy . Read about recent war between SEBI and IRDA over ULIP control

Effect on PPF

For PPF account any amount you have accumulated till 31 Mar 2011, will be tax free in any year of withdrawal. However any new contribution made after 31 mar 2011 will be taxed in any year when its withdrawn . All these rules will apply to existing as well as new accounts. One important point you should consider here is that PPF will still remain one of the best debt product, because this “tax on maturity” rule will be applicable on all the products, so from that point , PPF will still have one of the best returns in debt segment. This whole rule applies to your EPF as well . (Tip : Read Why you should open a PPF account even if you dont need it right now)

Strategies

Deposit more this year (2010-2011, so that amount becomes tax-free at the end .

Invest in your child who is below 3 yrs, so that you get benefit of tax on amount contributed for next 15 yrs, and after 15 yrs , when your child is age 18 , he/she will get that amount and it will be considered as his/her income , but at that time the tax outgo will be lesser as they will not have any other source of income , so the tax outgo will be less . This will not be a significant, but still 😉 (Read Clubbing Rules of Income tax)

Dont withdraw big partial chunks in between. Better withdraw smaller amounts so that in any particular year your taxable incomes remains low

Effect on Home Loans

Self occupied house

The tax benefits on self occupied home loans will be withdrawn once DTC comes into effect . At present Rs 1 lac is exempted for principle repayment and Rs 1.5 lacs for the interest repayment. After DTC comes, you will have not get tax benefits (Report on Returns from Real Estate in India)

House given on Rent

1.5 lacs interest deduction will be applicable for the home loans where the house is the second one and is given on rent. You might want to reconsider taking home loans if tax break was one of the major deciding factor .

In true sense tax break on home loans should always be secondary factor while deciding the purchase of house, because if you look back in your home loan documents, it’s clearly written that tax benefits are always as per the applicable rules of the year. So dont feel cheated and yell on govt for this.

Effect on Mutual Funds & Stocks

DTC does not differentiate between short-term and long-term capital gains, which means that any withdrawal after 31st Mar 2011 will be taxed in the year of withdrawal. Currently any profit earned after 1 yrs of investment is tax-free in Equity mutual funds and Stocks , this will not remain so . So if you have any Equity mutual funds or stocks with you, better sell them just before 31st Mar 2011 , so that current tax rules apply to that part of your investments .

Effect on Kisan Vikas Patra(KVP)/NSC/Tax Saving FD

All of these will loose the tax benefits

Effect on Income Tax Slab

The following tax slab will be applicable

Income Level

Tax

Upto 1.6 Lacs

NIL

1.6 – 10 Lacs

10%

10 – 25 Lacs

20%

25+ Lacs

30.00%

Effect on 80C

Sec 80C will be replaced by Sec 66 and limit will be raised from 1.2 Lac (20k for Infa bonds) to 3 lacs . Have a look at following classification of profucts from taxation point .

What do you feel about Direct Tax code ? Are you Happy about it ? Do you think it would be easy for Govt to bring Direct tax code without much fuss ? Share your thoughts

Do you want your children to be smart when it comes to Finance? Don’t you want them to learn all the things, which you’re learning today, from this blog & other resources? And that they don’t repeat the mistakes, we made in our lives?

Financial Education for Children is as important as their regular education. Sadly, we do not have in our school curriculum. However, you can start teaching your children, the basics of money, so that they become, more aware, more responsible and think in a better way about finance.

It’ll not just help your children, but even you as a parent in many ways. Here, I present 9 things to teach your children.

How to save money

Most kids today are indulged, like never before. All they do, is spend. The money mostly comes from one of the parents. The kid asks you for a 100 bucks to buy the latest thingamajig, you question them why, they answer you, and you give them the money.

This generally, makes them believe that once they give you a “good enough” reason, the money’s in the bank (or their grubby li’l hands) 🙂 . You need to make sure, that kids understand how you save money. This will happen only, when they themselves, understand how to save money.

Let them save some money for their little goals (even big ones’). If your kid wants to buy something, which you think can wait, encourage them to save towards its purchase. Whenever you give them some money for anything, ask them to save 25% of it for that goal.

Apart from this, you can give them some small amount weekly to save for that goal directly. Please buy a piggy bank for your children. You can buy a fancy one or the clay one we had in our days 🙂 It works!

How to keep track of money

You should teach your kids where the money at home comes from, where it goes and how much is saved. I’d ask them to maintain a simple table where they can write how much money they received, & when, from whom, & where it was spent.

These 4–5 things are good enough for a small child to start with. If you have a computer at home, you can make an excel sheet and ask your kid to maintain the account, while making sure, that things are very simple for the kid to understand. Don’t over do it 🙂

Once they start doing this exercise, they’ll gain an awareness of where they spend their money & to what extent. You can sit with them each quarter, and review the sheet. Don’t try to point what’s right or wrong. Just gently point out facts; that’s all.

How to pay what its worth for something

Have you ever faced a situation when your kid bought something and they were cheated & charged exorbitantly? Or demanded something from you, but they thought that it’s wasn’t that expensive? Kids don’t always realize, just how much something costs. They just want it.

The best way to deal with this situation, would be to ask them upfront, what they think, is the price of something. If they demand a video game from you, they might not know how much it costs. So ask them, what they think is the price, & what is the maximum they’d like to pay for it.

Many times, you will find that the price is much more than they themselves think. In which case, they might want to reconsider buying it.

My experience:

I remember, when I was young, my brother & I demanded a video game from my dad. He fobbed us off a couple of times, but later he asked us, “Pata bhi hai kitne ka aata hai?” (“Do you know how much it costs”) . We were puzzled, as we really didn’t know the cost.

We assumed it’d cost us something like a 1000 bucks, but we later found, that it actually sold for more than 3,000 at that time. Once we knew the price and compared it to the value it delivered, it didn’t make sense to buy the game. We had much better, healthier entertainment options.

And guess what? Dad bought us the game, next year! 😛

How to spend money wisely

Ask them their priorities, what they need this year, what their wishes are, and help them sort out their desires and their requirements. Ask them, what is more important? What’s secondary? This way, you encourage them to think in the right direction.

You are giving them an opportunity to understand difference between needs and wants. This might not be true for small kids below 10, but will be more relevant for children in between the ages of 10 & 18. Kids often times speak or figure out amazing things, which we adults don’t think about. Do this exercise and you might find, that your kid has real smarts!

Please share examples from real life if any 🙂 .

How to think about money

You should make sure that your child’s attitude towards money is shipshape; that they respect money, understand that it takes an effort to earn, and also understand the fact that, while money is important, it’s only secondary, as far as happiness & a content life are concerned.

Talk about money in front of them in a way, which gives them an appropriate view. Make sure, you don’t give them an impression that the family’s happiness isn’t as important as your job or business. Read Personal Finance Mistakes

How to live on a budget

If you give your children pocket-money, make sure they live on it, the entire month and they do not come to you smack bang in the middle of month, asking for more, for things they could have managed with the same pocket-money.

This happens only when children deviate from their monthly needs and carelessly spend on what they don’t need. While, they may ask for more, because of some emergency need sometimes, over a long-term, you should make sure they stretch with that pocket-money.

Children will understand budgeting better, if you yourself practice it (ouch!). When they see how you allocate expenses each month, and stick to it, chances are, they will replicate it at their level. While, this whole thing can be tough initially, help them out, by giving them the extra money they need in first 2-3 months and then restricting gradually.

Watch this video to know how to raise a smart child about money:

How to invest

Start teaching your child, the different ways of investing. Teach them basic banking, how banks operate and what it means to earn interest on an amount. You can also buy them some games which teach investing. Ask them to deposit some amount with you and you can pay them interest per month.

When you give them pocket-money, say Rs.500 per month, ask them to deposit back Rs.250 with you, with the assurance that next month you will pay them 10% interest on that amount, i.e : Rs.275. Though you might be out-of-pocket by Rs 25, the knowledge you impart to them is priceless !

This Rs.25 gives them the important message, that saving their money and investing regularly can increase their money many times over.

Don’t tell me you want your children to do regular 9-5 jobs! Don’t you want to instill some entrepreneurial skills in your children right from start, so that they know what they want to do in life and take an initiative to work along those lines?

The first step:

First step is to talk about different ideas your children have. When they are small, they can have weird ideas, but listen to them, & ask them how they can make money from some idea. Ask them questions like “Can you think of some idea, using which, you can make money?”

My own brother who is 13 yrs old makes weird stuff out of junk which can act like a toy gun! He once said, that if he can make 10 of those and sell at Rs 20 each, there will be many friends of his who will be ready to buy it. Though he didn’t do it, he surely has the right attitude.

You can encourage your child to do some random / different / creative stuff for a few hours every day (during vacations at least) and pay them extra money for it. This will help them earn some money and also help you do some work for which you wanted to pay someone!

If you have a garden, you can ask your child and his friends to do some random things for which you wanted to hire a guy anyway. This has some advantages; First – your children will understand, it’s not that easy to earn money and they have to work for it.

The second step:

Here, you will help your kids to spend some time constructively, which they would have spent playing or roaming around or playing video games. And finally, your money stays at home 🙂

Thinking a bit bigger, maybe you can really involve your child and his friends and work on some month-long project… one, that has a whole business plan, revenue model and which then earns money for 1 month (may be this can be done in summer holidays). Wow… this seems exciting, talk to your child about this today and see the response.

Ideas? Anyone?

How to handle credit

You should also start teaching your child, to handle credit.

If you pay them Rs 500 pocket-money and in the same month they demand Rs 200 extra, you can give them that money, but now introduce them a concept of “credit”. Tell them that it’s not going to be free and you are cutting Rs 50 for next 4 months from their pocket-money and paying them just Rs 450.

If you want to add some horror and suspense, make it 5 months (charge interest). This will make sure they ask for extra, only if they need to. Stick to this with discipline, and don’t fall for emotional atyachaar from your children,(they are really good at it, especially girls!)

The previous point’s example can also be used here. If you are making some small project for them from which they can earn money, loan them some seed money like Rs 1000-2000 (as a venture capitalist) and then demand the money back after 1 month with interest. (I come up with crazy thoughts at times 🙂 )

Conclusion

Teach your children basics of money from the very start. These tips will act as a foundation for your child’s financial education and they can build upon these learnings in the future. Most of these tips are for children, but can be used for your spouse, who may not be that good at personal finance. What say?

Comments, Can you also share your tips ? Do you think these tips will be helpful to your children? If no, then what are the obstacles?

There are many newcomers in Personal Finance who have no idea of very basic things . So I thought of doing a video presentation covering topics like Section 80C , HRA , HRA Example , LTA and Medical Exemptions , Tax Calculations , Tax Slab and example , Power of Investing Early , Understanding Equity and Debt , Investments Options , What is Insurance , Insurance Options , 4 most important things in Personal Finance . Lets see how everyone likes it . I would love to hear your views and suggestions so that I can create much better video tutorials in future .

In this article we will see the commission structure of Insurance Policies . We will look at Endowment/Moneyback/ULIP plans and how much commission an agent earns per year out of those policies.

As per Insurance Act, 1938, The insurance companies are allowed to pay a maximum commission of 40 per cent of the first year’s premium, 7.5 per cent of the second year’s premium and 5 per cent from there on. The commission paid is limited to 2 per cent in case of single premium policies. In case of pension plans, the commission is limited to 7.5 per cent of the first year’s premium and 2 per cent there on. Currently most of the policies are very much paying these kind of commissions . Let us quickly look some of the facts on Life Insurance .

Average sum assured of the insured Indian is around Rs 90,000

1 trillion worth of policies lapsed in 2008-09 , this is mostly because investors have discarded their old policies to buy new one’s , thanks to agents who tell people about another “hot” plan in market. Another reason is that investors buy policies which have higher premium than what they can afford in reality and later feel that its time to stop it .

India Insurance penetration is around 7.5% of global numbers . i.e: 0.16% of the GDP, which is , against a global average of 2.14

As per IRDA report 2008-09 , Insurance Industry had 29.37 lakh agents by the end of Mar 2009 , out of which 13 lakh agents were added during 2008-09 .

Life Insurance Commission Example

Policy Type

Premium Paying Term

Upfront Commission (1st Year)

Trail Commission (2nd & 3rd yr)

Trail Commission (from 4th yr)

Endowment / Term Plans

15+ yrs

25% – 35% *

7.5%

5%

Endowment / Term Plans

10-14 yrs

20% – 28% *

7.5%

5%

Endowment / Term Plans

5-9 yrs

14%

5%

5%

Endowment / Term Plans

Single Premium

2%

0%

0%

Money Back

15+ yrs

15% – 21% *

10%

5%

ULIPs

Regular Premium

20 – 40%

2%

2%

ULIPs

Single premium

2%

0%

0%

Note : Some of the numbers are in range, which means the commission can lie between that range . Mostly its minimum commission + Bonus if any

Agents have to make sure that they follow-up with clients and track the premium payment, this leads to overheads and regular feedback from agents side , apart from that there are operational expenses incurred by agents , so we should not forget those points . As a customer , you should be knowing how much an agent is making out of you , this should form the basis of the quality service for you . An agent should help you understand your Insurance requirement and provide you the best solution , He should assist you in buying the Policy and over the years he should update you/ help you with all the changes .

Hot discussion topic

As per a govt-appointed committee , Insurance commissions should totally be removed by 2011 . “Immediately the upfront commissions embedded in the premium paid (to agents by insurance companies) be cut to no more than 15 per cent of the premium. This should fall to 7 per cent in 2010 and become nil by April 2011”, said the consultation paper prepared by Committee on Investor Awareness and Protection. (Link) .

What do you feel about removing the commissions from Insurance products totally ? Will it impact the Insurance Industry , how much ? Do you think it will lead to fall in premium payments or new policy getting issued ? I personally feel YES . What are your views ?

{kind=link}