Small is Big? Are you worried, about how will your financial goals be achieved, because you are not able to save more? Do you feel that small savings will not help you much to reach your big goals in life? If that’s the case, you are mistaken!

While it’s true that small savings won’t be able to help you much in short run, they can impact your financial life in a really big way and contribute significantly in long run.

In the tribal villages of Cameroon, there is a community called “Mofu“, who grow and eat millet’s all year. They store their entire crop for the whole year in their store houses made of mud and wood. Unfortunately, in some bad years, termites attack these store houses and no matter what the villagers do, termites destroy just about all the crops in a short span of time.

The only creature which can now save these villagers, are driver ants which they call “Jaglavak” in their native language. They search the village and try to find those ants. Just a handful of driver ants, kill all the half-million termites in a few days!

How are these ants able to destroy a big army of termites? The answer lies in their strategy and their team work! If they are not disciplined in their approach, it would not be possible to defeat the big army of termites. It’s not the power of a single ant which makes them winners, its numerous ants working together and following a few simple rules.

Small Expenses can help us grow wealth

Just like the story above, we in our financial life have a lot of small/medium expenses which keep rotting and destroying our wealth and many a times, our health too.

Some of them are smoking, drinking, too much eating out without any reason or out of sheer laziness in cooking at home, spending on items which give us instant happiness, but in reality we don’t need them, buying things just for ego-satisfaction (My neighbors bought it, so we should also have it!).

Small pains taken today by saving money and investing properly will help you generate enough money in future (read this story). Most times, we keep thinking about bigger problems in life and do not value or think about taking care of small things. We ignore them because we see them in isolation a lot of time.

My friends case –

One of my really good friends works in a finance company and earns around Rs.25,000 a month. Just graduated from college and found a decent job in Delhi. He lives a great life! Movies with friends, eating out, smoking and drinking.

His credit card bill keeps piling up month after month, but the instant gratification of paying “Minimum due amount” is much higher than the pains which will follow years later when banks will deny or ask for a very high interest rate when we will need a Home Loan or a Car loan.

I asked him his financial goals in life, and got this answer –

1. Retirement corpus of more than a crore by the age of 60

2. 40-50 lacs to open a restaurant once he retires

3. 6-7 Lacs for a vacation in Europe after 10 years with his wife.

How cutting some bad habits helps in long term

He was expecting a big laugh from me. He expected me to tell him, that he is living in fantasy world. With a salary of Rs.25,000 per month how is it possible to achieve these financial dreams in a situation where he was not able to save even Rs.1,500/month?

To his surprise I told him that if he is ready to compromise on bad habits and have discipline in investing from today, it might just be possible to get closer to his dreams! He thought that my advice and plan for him would be tough, complex, and full of jargon and he will have to spare next some days to understand what I was going to show him.

Here was my plan for him.

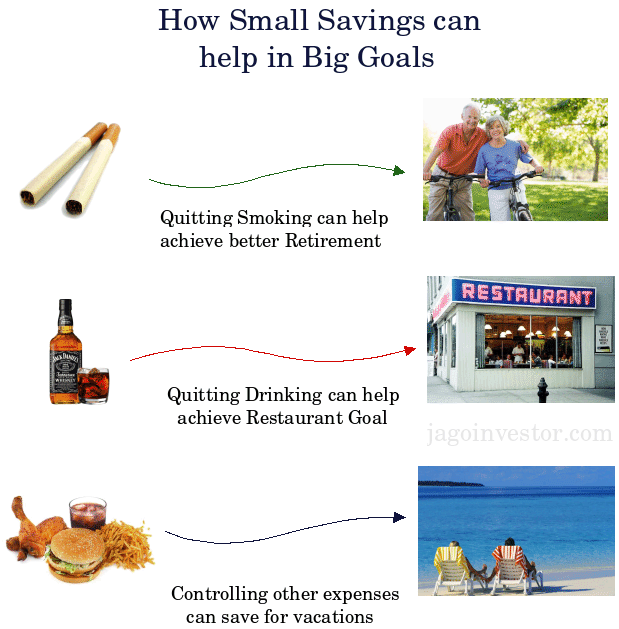

Goal 1: Retirement

His retirement can be taken care of, by just investing the money which will be saved by quitting smoking. I don’t know how much a quality smoker spends on his daily quota of smoking, but I guess I can safely assume Rs.50/day which turns out to be Rs.1500/month.

Instead of using this money to deteriorate his health every month for next 35 years, if he invests it in equity mutual funds regularly through SIP. Assuming a 12% return, he can make around 97 lacs (calculate). Note that this amount is without taking into consideration any inflation, if we incorporate inflation of 5% (in cigarette price); it would turn out to be 1.2 crores in 35 yrs.

Equities in long run might give excellent returns and a 15-18% return can be expected from equities if the time horizon is 30-35 years, especially from Indian Markets (Read why)

Goal 2: Restaurant

My friend’s plan for opening a restaurant in retirement can easily be achieved if he controls his drinking and starts investing that money. I have some idea on how much it costs to booze per week (no, I don’t drink, I actually thank my friends in college), I assume it to be around Rs.200/week. Let’s consider Rs.800 for a month.

If he invests part of this in PPF and rest in balanced funds, he might be able to generate 10% returns , and with 35 years in hand, it would be Rs.48 lacs assuming that he also increases this investments by 6%/year (come on, alcohol prices also increase!)

Goal 3: International Vacation in 10 years

My friend spends a lot on phone with his 10 “best friends”, eating out, shopping gadgets and clothes every month/quarter. Not sure why he keeps flying from Delhi to Varanasi every quarter when he can take an overnight train! And save thousands.

Cutting a bit on all these habits I mentioned, it should not be a big deal and he should be able to save few hundreds from each of those and save another Rs.2,000 in total months.

If he saves this money in balanced funds, he should again be generating 3-4 lacs in next 10 years and if not Switzerland, he can go on a vacation to some near-by destination :).

Conclusion

A bit of restructuring and prioritization in your spending habits can give you a good idea on what all things can you saves on. If you are disciplined in your approach, over the time these small savings if invested with proper plan can help you in a big way in your financial life.

Just like my friend in above example, we have many areas in our life where we can cut our expenses or stop them. If we use it and invest systematically for some goals in our life, slowly it can turn out to be a very big amount. If you are still confused and can’t think of where to cut expenses, another alternative for you is to live on 90% of your salary. It works!

Assumptions : It’s assumed that all the spending might have continued for all life which are saved and diverted to investments. Also the investments are assumed in Equities.

Can you think of anything similar in your life and how it can help you in saving some money? It can be asking small as Rs.100 or Rs.200. Please share! Also share how it can help you in achieving something, use our calculators to find out.

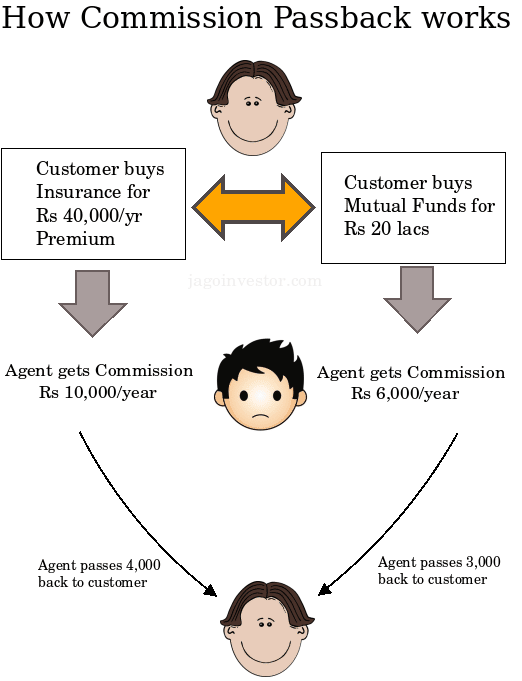

“Discount kitna doge ! Mishra ji mujhe 35% de rahe hain ” , as per Rakesh ,this is exactly how a lot of customers ask their agents commission to be shared with them in Insurance or Mutual funds. Have you ever asked your agent how much discount he can give you on the premium? This happens a lot with LIC agents and other insurance and mutual fund agents. Many times, even agents offer discount or some gift in return, if you buy the policy or mutual funds through them. This practice is illegal and totally against the laws of Insurance Act and SEBI. The agent can even face cancellation of his license if he is found to share his commission. (Read about agents commission in Insurance)

It kinda works like this. Suppose, an Insurance agent sells you a policy with a sum assured of Rs. 10 lacs, with a premium of about Rs. 50,000/- per year. An agent will make around 15,000 in commission for that year, out of which he might offer you a discount of Rs 5,000-10,000 for the first year or he offers you some gift! A lot of insurance agents do this to make sure they do not lose the business or get more and more business . In the same manner, if you have Rs. 30 lacs invested in mutual funds, your agent will get around Rs 10,000/- in trail commissions. It might happen that he can offer you 50% of that commission to make sure you stay with him .

Why you should stop asking share in Agents commission ?

Mutual funds : As per SEBI mandate, sharing the commissions received from AMC is illegal and should be avoided . Pass-backs, the practice of sharing a part of the distributors’ commission with the investor, have been made illegal under the code of conduct issued to distributors. “Intermediaries will not rebate commissions back to investors and avoid attracting clients through temptations of rebate/gifts etc” – As per a SEBI circular.

If a mutual fund agent shares his commission with others, it opens a big hole, not just for mis-selling, but also dilutes the whole industry atmosphere. There have been rampant cases, when an agent asks customers to leave their current agent and transfer their funds with them as a new agent (link) and they are ready to transfer a part of agent commission to them (the customers). For example, if a person has Rs 30 lacs invested in a mutual funds, an agent would get around Rs. 10,000/- as trail commission in a particular year. A lot of agents offer 5,000 (50%) back to the customers to attract them. A lot of agents pass back a part of commission and customers get into wrong & ill-suited mutual funds because of their greed!

Insurance : Other than the fact, that it’s illegal, you should not encourage or engage in sharing the agent commissions because, for one thing, it hampers your relationship with agent. Don’t forget that your agent will be the one to help in claim settlement when you are dead. If you snatch his share of commission today, it might leave him with a bitter taste in the mouth and not result in a healthy relationship. So please live and let live! The other important reason, you should avoid asking for agents commissions, is that it leads to mis-selling. If you ask for a share in commission, it will leave agents with less earnings and that would encourage them to sell more by any means, which in turn fuels mis-selling. So in a way the whole “asking commissions back” will hamper investors in the long run. What you sow is what you reap!

As per section 41 of the Insurance Act, “No person shall allow or offer to allow, either directly or indirectly, as an inducement to any person to take out or renew or continue an insurance in respect of any kind of risk relating to lives or property in India, any rebate of the whole or part of the commission payable or any rebate of the premium shown on the policy, nor shall any person taking out OR renewing or continuing a policy accept any rebate, except such rebate as may be allowed in accordance with the published prospectuses or tables of the insurer.”

Real Life experience

As per Dhawal Sharma, a Delhi based agent shares his experience

I face this problem day in and day out and many a times have to miss out on prospective clients because they want “passback of commission“. This practice (Sorry to say, but started by LIC agents) is so much part of the Insurance selling culture that 99.9% of the public thinks that it is obligatory on the part of an agent to part with his commission. But even LIC agents were quite smart at that time as they use to pass back comission mostly on ENDOWMENT or MONEYBACK policies which generate hefty renewal commissions as well (Unlike ULIP) and reversely, would be of little or practically no use to the client in the long term. This practice is actually pound foolish , penny wise approach..

I know at least 100 people, regularly buying insurance for their entire family (father , mother, brother,uncle, aunty) for last so many years from SHARMA JI or OFFICE WALE CLERK who passback 20% commission, and if we make a thorough study of their Insurance portfolio, they are underinsured (No term plan), not properly equipped to handle retirement (their agent never knew that annuity fund is tax exempt only upto 1/3 amount), and no proper child planning (In many cases, child plans where child is life insurand and not father).

Violation of law using Multi-level marketing in Insurance Policies

For some years now, a new way of selling is evolving. It’s called MLM. Here a big agent sells a policy to some one and makes him a customer. Now, this customer also acts like an agent and starts adding new people in the network and sells them policies. This goes on to many levels, a person earns a part of commissions earned from every person under his personal network. This whole idea of multi-chain selling violates Insurance law and is illegal.

As per Section 41 of the Insurance Act, “A licensed agent, whether individual or corporate, can’t appoint a sub-agent and pass on a commission to another person or entity. Any passing of commission by an agent is construed as rebating and is prohibited under the Act.”

There are many companies operating in different part of our country like TLC Insurance (India) in Bangalore, RMP Infotec in Chennai, Golden Trust Financial Services in Kolkata and SecureLIFE out of New Delhi (read more here and here)

Responsible Investor = Health Industry

We as buyers, shape this whole industry based on how we act. Over the years, we expected and asked for share in agents commissions, without realising that it will one day work against us resulting in misselling. So please do not support it! A couple of hundreds or thousands is not going to make you rich or poor, but it sure dilutes the whole environment!

Have you ever experienced a situation where agent has tried to give back his commission? Do you think if everyone stops asking for any agents commission back, it can really have any impact?

What do you do when you are facing un-ethical practices by some company officials and You are not getting justice anywhere? You should reach out directly at the top of the management somehow because, believe me customer care just does not work ! . This is exactly what I did, when one of the readers complained on our forum that one of his friend is facing issues with India Bulls Real Estate from last some weeks. Here is his complaint

Dear Forum Members,

I’m writting this on behalf of my Friend-Colleague, Ravikumar GovindaNaik, who had a very Bad experience with Indiabulls Home Loan division.

Application Ref no with IndiaBulls – 150625

Name: Ravikumar Lamani GovindaNaik

In August 2010, he initiated the process to buy a 30×40 site near Hosur road, Bangalore. Since the property had only B-Khatha and loan amount was only 10 Lakh, most the major bank representatives denied his enquiries.

Then one Mr. Sivakumar from IndiaBulls Home Loans have appeared as life saver to him an agreed to get him the loan amount approved, with the whatever B-Khatha he have. Every now and then he asked for somany documents copies and it went for almost for a month. In between my friend got an SMS from indiabulls informing that his loan got approved. When he asked about this to Sivakumar he told, Loan is approved by Finance Division but Legal team still have to approve. Also he asked my friend to pay Rs. 5,000/- so that lawyer from Legal division would approve the loan amount. My friend disagreed to pay and asked the contact details of the Lawyer to talk. He refused to gave and tried to divert our attention.

When there was only few days to expire the sale agreement with the Land owner, Sivakumar again appeared and told Loan in COMPLETELY approved and shown photocopy of the cheque favoured the Land Owner. Later Land owner had some dispute on the registration amount and canceled the Land deal.

On October 05, 2010 My friend send a mail to Sivakumar and Indiabulls to cancel the Loan, since he no longer needs it. Nobody responded to mails and phone calls even after repeated attempts, and my friend was scared about the blank cheques he have given.

As he feared, on 13-Oct-10 Rs. 2,216/- was withdrawn from his bank account using the cheque claiming as Pre-EMI, eventhough the Loan Amount cheque was never delivered to him. Immediately my friend contacted Sivakumar and his Manager Praveen enquiring about this, but they suggested to contact customer care. When he contacted the customer care they told him to contact Praveen, The MANAGER. Many e-mail written to Sivakumar, praveen and customer care fell into deaf ears.

On top of that, again on 8-Nov-10 Rs. 20,275/- got withdrawn from my friends bank account using another blank cheque claiming as EMI of the Loan Amount, when the loan amount was never disbursed. Now they have stopped answering my friends calls. Do the Financial Institute have the rights to do like this?

The representative was from Indiabulls that we confirmed, called up the customer care, they also have the application reference number. The cheque’s were in favor of Indiabulls Housing Finance Ltd., only the amount was unfilled. They told that cheques are required for security and to initiate EMI-ECS facility. After the second incident of cash withdrawal, my friend used the “stop payment” facility of his bank. When I searched in Google, I could find lots of complaints against Indiabulls Loan services. In this case they have looted the money on top the processing charge Rs. 5,000, charged earlier.

Yesterday, my friend spoke to the representative Sivakumar again and threaten to send the details to RBI and would file a case, he was least bothered. He just told “Do it!”

What should my friend do now? Anybody knows a Higher official in Indiabulls, who could help? Or writing to RBI about this would help?

Please Help, Thanks, Surabhi R

What action I took ?

I emailed the whole incident as it is to Sucheta Dalal of Moneylife, who helped in escalating the whole issue directly to Gagan Banga, CEO of the company . Moneylife got the reply directly from CEO within same day that he will look into the issue and by next day itself .

—– Forwarded Message —- From: Gagan Banga <> To: Sucheta Dalal Sent: Sun, 21 November, 2010 1:31:12 PM Subject: Re: Bad experince with Indiabulls Home Loans

Ma’am, this will be sorted out by tomorrow. Thanks for your feedback and for escalating this issue to me. Regards, Gagan

IndiaBulls had talked to the customer and apologized, they also handed over the refund cheques towards Pre-EMI & EMI the same day. They also dispatched Post dated cheque’s & loan cancellation letter to customer the same day. Here is a reply

From: “Gagan Banga” <> Date: Mon, 22 Nov 2010 17:09:28 +0530 To: Sucheta Dalal

Subject: Re: Bad experience with Indiabulls Home Loans

Dear Ma’am, Firstly I would like to accept the mistake of my team and our system . We have already apologised to the customer for the inconvenience caused and handed over the refund cheques towards PEMI & EMI today. The remaining PDCs & loan cancellation letter are being dispatched today and should reach him in a day or two. Once again thanks for bringing this to my attention, such feedback will surely help us in improving our processes. Regards, Gagan

This was a reply made from Gagan Banga to Sucheta Dalal of moneylife and she forwarded to me later. Sucheta Dalal has been in journalism from last 25 yrs and its because of this fact that Moneylife has strong ability to reach top management. Moneylife has been helping investors like Ravikumar get justice from many years now and they routinely do grievance redressal with success rate of over 80%. Moneylife also conducts various Financial literacy initiatives for common public in association with Industry experts .

Customer finally got Justice

After I got an email from Suceta Dalal that finally the issue is resolved, I personally talked to the Ravikumar (customer) on phone. Here is what exactly happened (as per the telephonic conversation)

Ravikumar went to Koramangala IndiaBulls office on Saturday (20th Nov) and the Manager-Praveen was not in office. One gentleman at office connected Ravi to Praveen over the office phone, and Praveen was not happy to talk with Ravi. He told that, today I’m on leave, will be back to office on Monday only, would look into then. There was nothing much to do for Ravi so came back home.

I think after that moneylife sent mail to Indiabulls CEO and he acted on it. On Sunday morning Ravi received a call from Mr. Praveen Pradhan (some other Praveen) , we claimed to the Location head of IndiaBulls in Bangalore. The other manager Praveen reports to this Praveen Pradhan. He might have received the communication from CEO by that time.

This Praveen Pradhan spoke to Ravi for 10-15 minutes, and collected the whole information about the story. He promised to Ravi that, he would receive money on Monday morning without fail. The interaction with Pradhan was pleasing and he apologised for the whole mess.

Monday morning (22nd Nov), Ravi visited Indiabulls office at Koramangala again, and he was directed to finance division. Straight away they have handed over the Refund-Cheque of Rs. 22,491 and as a latest update, while I was drafting this mail, some executive from Indiabulls called up and informed that he is coming down to our office in hour and would deliver the rest of the documents and those blank cheques collected.

– Ravikumar Govindanaik

Problem lies at Bottom level most of the times

This whole incident and what happened opens some questions . Is the problem mainly at lower levels or bottom of the pyramid which involves employees, and managers at lower level ? When we face any issues its never entertained by them or even customer care as they are just not bothered about the company ethics and only interested in their salary and day-to-day activities . However top of the management takes these issues very seriously and acts upon them faster ? What is your opinion on his point ?

Also what are your comments on this whole story ? Do you know some one who has faced these issues ? According to you, what can reduce these kind of frauds or un-professional behavior ?

You also make no mention of the fact that I told you in my email that Moneylife Magazine (www.moneylife.in) routinely does grievance redressal and that our success rate is over 80%.

Are you thinking of entering the equity markets now? Are you thinking of buying some equity mutual funds? You must have heard by now, how the markets are back in action, reaching highs again.

Today, I am not here to discourage you and say “Don’t enter markets” or “Its time to exit” — because neither I or anybody else can predict it. We are here to take decision based on what we can control; and the market is definitely something, which no one has control over.

However we can control our actions, greed or fear! I am here, just to remind you about the last crash and how stupidly we all behaved out of greed or fear. (read my story)

The first thing you should understand clearly, is that it’s not the best time to enter the markets for the long-term, because markets are not back in action from last few weeks. It was back in action 1-1.5 years back when markets started rising from 8000 to current levels of 20,000.

It has already given 150% return on an absolute level or 100% CAGR 🙂 and the retail public is now waking up like always to enter with all its money for “long-term”.

Lets us see in this article some good practices and what you can do at the moment .

We, as investors have to be very cautious and not lose our control. It has been 30 years now, that markets are in existence and these kind of situations have come along loads of times. Let’s make sure, that this time we do not regret like we did before. IPOs have started coming in and we recently saw one of the biggest IPO of Coal-India in the history of Indian markets.

All the news channels are back with all the so-called analysts and discussion on how markets can reach new heights and logical explanations about economy booming, deep valuations and what not.

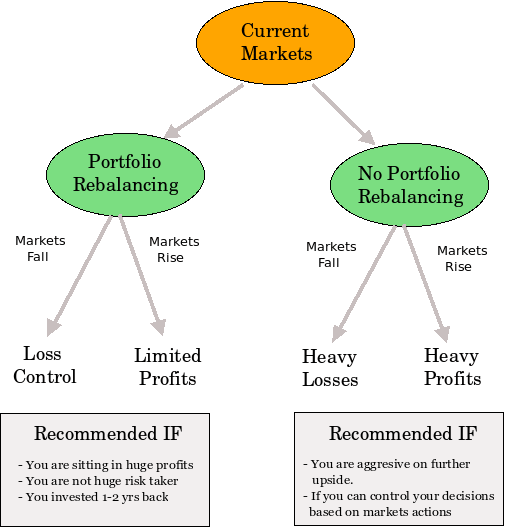

Good time to Rebalance your Portfolio

Markets are nearing an all time high of 21000! It has come a long way from 8000 to 21000 in last 18 months. For investors who bought equity funds or direct stocks at lowest points, it would be a good idea to book profits or rebalance their portfolios.

Look at your investments in Equity as growing a tree. When you invested 1 yr back, you had started with a plants which over these 1-2 yrs have grown to a tree and now is the time for you to pluck the fruit; at least book the profits partially if you don’t want to sell everything.

Note that it does not mean that markets will fall or should fall. But rather than trying to control what markets are going to do, concentrate on what you can (and should) do at the moment. Don’t loose your sleep over what will happen in markets, reduce your tension by booking your profits partially atleast.

Incase you had bought stocks, mutual funds randomly without any proper study, you should immediately get out of markets.

Two dimensional possibility in markets

Right now, there are two really important influences that can affect your investments. One of those is Market direction and the other is Self-Direction. Market direction is something you can not control and it’s almost impossible to predict.

However, self direction is something you can control. Let’s look at a couple of different scenarios and what they mean!

For simplicity purpose we will assume that following two things can happen in Markets-direction and your Self-direction

Market-Direction

Markets can go DOWN by 50% in next 1 yr

Markets can go UP by 50% in next 1 yr

Self-Direction

Rebalance your portfolio from 100% equity to 50% equity and 50% debt

Leave it 100% equity

Case 1 : Markets go Down by 50% in 1 yr

If your Rebalance :: In case you rebalance right now , you will have 1 lac in equity and 1 lac in debt, The equity component will go down from 1 lac to 50,000 and debt component will rise from 1 lac to 1.08 lacs. Your total worth would be 50k + 1.08 lac = 1.58 lacs. That would be a 21% loss overall .

If you Dont Rebalance : If you don’t rebalance right now, you will have 2 lac in equity and it will go down from 2 lac to 1 lacs – a 50% loss overall .

Case 2 : Markets go UP 50% in 1 yr

If your Rebalance : In case you rebalance right now , you will have 1 lac in equity and 1 lac in debt, The equity component will go up from 1 lac to 1.5 lacs and debt component will rise from 1 lac to 1.08 lacs. Your total worth would now will be 1.5 lacs + 1.08 lac = 2.58 lacs, a 29% profit overall.

If you don’t : You will have 2 lacs in equity and it will go up from 2 lac to 3 lacs – 50% profit.

Results

You can see by this small exercise that in one case you are going to see 50% loss or 50% profit and with another case you can see 21% loss or 29% profit. Now it’s your choice. Which situation are you more comfortable with? I personally feel, retail investors should concentrate more on limiting their losses.

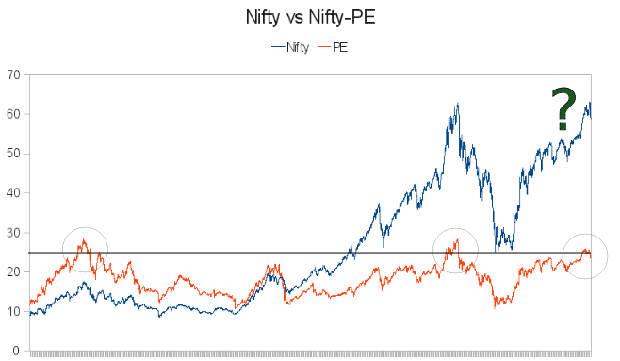

Where is Nifty PE ?

The Nifty PE has been a good indicator in the past to judge overbought and oversold situations . One problem with Nifty-PE though, is that it can’t give you precise a timeline, for when markets can start rising or falling. Nifty PE right now is somewhere around 25, which has proved to be an overbought situation historically.

In the past Nifty PE has reached this level before markets fell after few months. It happened in 2008 crash. On the other hand, a high Nifty PE also indicates strong momentum and can be seen as an opportunity to make some quick trades by entering on the weaker days.

So it’s your choice on how you want to look at the situation .

Note that Nifty PE at the moment is very much near that previous high’s of 25, where markets crashed, but it can still go to 27-28 or even 30 in worst case, which can take another 3-4 months and then market can fall ! severely .

Some views from Market Experts

“This current fall of 1200 points on sensex is an obvious downside which always happen after a spectacular upmove and it is nothing but a pure profit booking correction which has happened in last 1-2 weeks.

There is still 1 leg of major upmove remains in markets and unless Nifty breaks support levels below 5700-5800, instead of panicking its a good time to take some positions for short-term of 3-4 months, markets can break the previous levels and reach upto 25000-25000 levels” – As per Hemen Kapadia, a noted technical analyst (I met him at a seminar in Bangalore).

Another friend of mine and a technical analyst Nooresh Merani shares his similar views “Unless nifty breaks down by another 200-300 points, we can see it as a trend reversal pattern, and it still have steam left for another next few months, there after we have to look at charts again to give views”

So If you are an aggressive investor, don’t sell. Just ride the trend; you can also add some money when market cools off a bit and then ready for the move upwards again.

But anyway, you have to be cautious and make sure you have control on yourself. And you should be selling if there are major indications of markets being weak.

JagoInvestor.com recently completed its 3 yrs in Nov 2010 and following is the interview taken by one of the fellow bloggers .

Yet another milestone for Manish Chauhan, founder of JagoInvestor.com. It’s been three years since Manish started blogging and on Nov 5th 2010, JagoInvestor.com celebrated it’s third anniversary. After three years of run up, JagoInvestor.com boasts of a massive 6500 RSS followers which is still growing and a treasure-house of articles where you can find almost anything on personal finance. On this occasion, here are some snippets of a tete-a-tete I had with Manish on his journey over the last three years and his vision for JagoInvestor.

Q1) Which is your best personal finance book and why ?

I have not read any book on personal finance nor I am aware of any pure personal finance book which gives a good idea of everything on personal finance at this point in India. However there is enough material on Internet and loads of good websites and blogs which gives great education on personal finance.

More than knowledge, Personal finance is about attitude and applying common sense in area of personal finance. There are few things which a person has to understand and on top of it he himself can build all the knowledge and analyze things . Incase some one has any idea about personal finance books in India , please give the names in comments section !

Q2) What is your vision for JagoInvestor in the next 5 to 10 years ?

Personal Finance is a huge area with opportunity. I see JagoInvestor being synonymous with “Financial Literacy” and “Psychology changing website” which along with providing personal finance knowledge also provides counseling in the area of personal finance, I want to build a program which would span over few months or may be 1-2 yrs which if any one who is interested in financial freedom can join and they can totally transform their way of looking at personal finance. The program can turn a novice into a pro in area of personal finance. (Would like to read comments from readers on this point)

Overall JagoInvestor’s main motto is to “change investors relationship with money” over time.

Q3) You did you manage running a personal finance blog despite being from a different background ?

There is Chinese proverb, “start doing what you truly love and you will never have to do any work !”. Common sense has no background and I consider personal finance as pure common sense fueled with a passion to change one’s financial life. As I like number crunching and I consider myself a logical person, I started a blog one fine day without realizing that it would become this big today, readers liked it and it was making difference in their life, which motivated me to work hard and make sure I keep running this movement of financial freedom.

Q4) What would be your top three advice for investors ?

Top 3 advice I can suggest some one is

Start investing time to understand how important personal finance is in one’s life, thats one thing we work for and our quality of life depends on.

Take pain of cross-checking each and every aspect promised by products, like investors in endowment plans should calculate what is the return they are getting and how 1% more return can impact their wealth in long run.

Shift from free advice to paid services and value them, paid does not mean costly, if you get more value than what you pay, thats even cheaper than FREE. This mind set of getting FREE FREE FREE in each and every aspect of life actually turns out to be very costly in long run.

Q5) Top 3 urgent changes required in the personal finance space ?

a) Shift from sales driven attitude to value-based model in selling : When even you get a call about some product, all you hear is how great the product is, how much return it gives and blah blah.. all the focus is on the sales and even the conversation you hear is driven by sales. The biggest change which should happen is the whole model should be based on how the product will help customers in achieving their goals, a client buys a product because it helps them in life, not because its GREAT.

b) Training to agents and IFA’s : There is good number of magazines/portal for investors to help them in taking informed decisions, however I don’t see anything which helps agents and other IFA’s/CFP’s to understand how they should change their strategy in acquiring clients and giving value service to them. We need some services like these.

c) Basic Financial Planning for each Indian : While financial planning is a detailed thing in general, each person should have access to cheap basic planning for their life goals such as child education and retirement at least. There has to be a model which gives them inexpensive plan for their most basic goals in life.

Thanks to all the readers of Jagoinvestor for giving me an opportunity along with them to create this platform for learning personal finance.

Comments

Would like to hear your comments on how do you feel associated with jagoinvestor and what changes has happened in your financial life ?

We will learn about creating a WILL in India today, but before that you need to answer this question – “Do you want to leave your wealth and let your loved one’s fight with each other to get their shares (a la the Ambanis!)?” –

I guess not! . If you nominated some one in all the financial products you bought and thought that it will be passed to them legally without any issues, you are living in the world of fantasies (kind of :). It’s a common misconception). You need to create a WILL to distribute your wealth in the manner you want to, and having nominated someone ain’t the answer!

Lets fine out in this article, how to make a will in India ?

What is a Will ?

A will can be made by anyone above 21 years of age in India. You can make the will on plain paper in India. It’s not legally necessary to make the will on stamp paper. It is advisable to write your will in your own hand writing, as the same can be verified later in case of any doubts raised by relatives.

It might happen that according to your family structure and your preferences, you want to divide your wealth unequally or make a provision for a close friend or a faithful servant. This isn’t possible if you die without a will.

A lot of us feel that talking about “Making a Will” is pretty morbid, and hence, we don’t look at it with right attitude.

“A will is a sensitive topic to open up to. People are not comfortable discussing a will in India. There is a misconception that if someone tells you to make a will, the person thinks that indirectly you are telling him that his end is near or that you are eyeing his property. However, all apprehensions disappear when I tell them the consequences of not making a will.”

– Says Shankar Pai, who has done some commendable work in area of spreading awareness on making wills.

How to make a WILL in India and its importance ?

A will is so important, that it should be your first step in your financial life. If your family structure is diverse, and you want to leave your wealth to different members of family like you want to, you should prepare your WILL today, not tomorrow, not later.

To wit, if you die without preparing a WILL in India, your wealth will then be distributed as per ‘Hindu Succession Law’ (Government rules, on how wealth should be divided among family members). A common misconception, is to believe that all the estate is automatically passed on to the spouse, because children and sometimes even relatives can stake a claim to the property.

Laws of inheritance and succession, are complicated and diverse in nature, and are different in case of Hindus and Muslims.

Inconvenience for the family members:

Another point you should consider, is the inconvenience caused to your family members because of your laziness, in not making a will for them. In case of a dispute, your family members have to produce the proof about their relationship with and also have to go helter-skelter to lawyers and spent money and energy.

Much better then, to gift them some time of yours, and creating a will! This will save them a lot of headache.

Watch this video to know why it is necessary to get a registered will:

How do you make a Will in India?

A will has several parts, which duly completed, make up a complete Will. Though there is no legal or defined format, there is a template, which has been generally used for ages. It’s simple, it’s very logical and derives from common sense. Let’s look the whole format and some important points while creating a will.

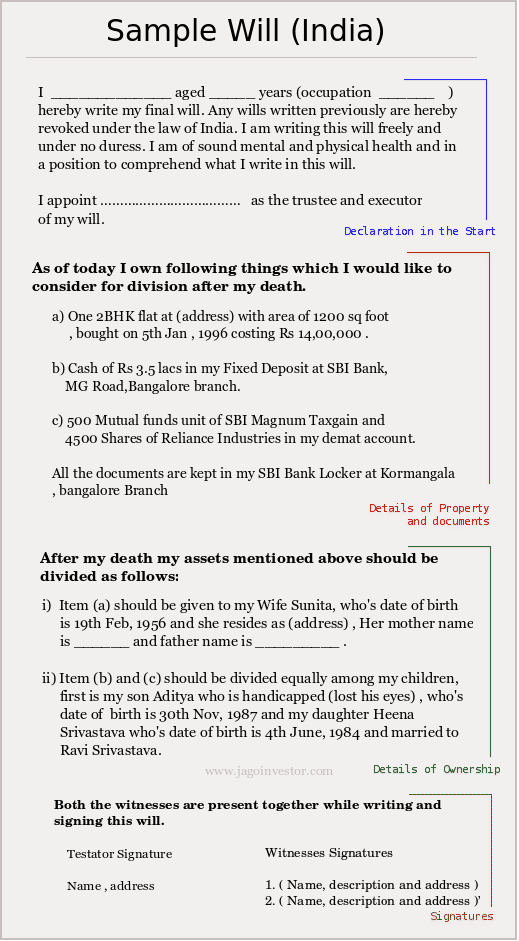

Step 1 : Declaration in the beginning :

In the first paragraph, you have to declare that you are making this will in your full senses and free from any kind of pressure. You have to mention your name, address, age, etc at the time of writing the will so that it confirms that you really are, in your senses 🙂

Step 2 : Details of Property and Documents :

The next step is to provide list of items and their current values, like house, land, bank fixed deposits, postal investments, mutual funds, share certificates owned by you. You must also indicate, where all these documents are stored by you. In all probability, these are in your bank safe deposit box.

Even the will should be stored in there! Make sure, you take the details from the bank manager, about the procedure and rules of releasing your will from the safe deposit after your death. Make sure you communicate it to the executor of the Will or your family members.

I am sure, they’ll be pretty interested in this 🙂

Step 3: Details of ownership :

At the end of the will, you should mention who should own your assets items and in what proportion, after you have gone. If you are giving your assets to a minor, make sure you appoint a custodian of your assets till the individual you have selected, reaches an adult age. This custodian obviously, has to be a trustworthy person.

Step 4 : Signing the Will :

At the end, once you complete writing your will, you must sign the will very carefully in presence of at least two independent witnesses, who have to sign after your signature, certifying that you have signed the will in their presence. The date and place, also must be indicated clearly at the bottom of the will.

Make sure you and the witnesses sign all the pages of the will. One important point while choosing witness, is that they should be your friends, neighbors, or your colleagues and not the direct beneficiaries in the Will. They only certify, that you yourself have signed the will in their presence and are not a party in making the will in India.

The envelope has to be sealed after completing all the formalities and the seal must bear your signature and the date of sealing. The witnesses need not sign on the seal of the envelope.

See another Template from Department of Stamp and Registration, Karnataka here, thanks to Babu .

Execution of Will in Court ?

When you are dead, there is someone called an “Executor” who will be responsible for dividing your wealth amongst the beneficiaries and he will make sure the whole process is smooth (You must have seen this in Hindi movies). It is not legally required to get the will executed in a court of law in presence of a judicial Magistrate in India.

However, if you wish, the will can be executed in the presence of Magistrate or the public notary, nominated by the government authorities and sealed in their presence.

Changing the WILL in India ?

You can change your will any time you want to. However, make sure that when you make a new will, you mention that this will is the latest and supersedes all earlier wills. If you don’t, it can complicate the situation, cause major confusion, make such matters go to the court of law and take several years before arriving at any final verdict.

Making a Will through Lawyer

“Do-it-yourself” wills often do not contain all the necessary components as required by law and many times ruled as invalid by courts (for example no signatures from witness or no witness at all). Many a time, it can happen that while creating the will, you use such ambiguous language that it results in lengthy legal battles (“My House should go to Sunita.”

Now if both mother and wife are called Sunita, which Sunita ought to get it?. Anyone who might benefit from the ambiguity of the will can jump in to claim a share! And if the courts decide in his/her favour, you wont like that situation 🙂 (not that, you’ll be around!)

What is a Probate and it’s importance?

A probate is nothing but a copy of will, certified under the seal of court. The executor (someone who is responsible to execute the will) has to file a probate petition in the court of law and if all goes well, the probate takes six months to a year. No right as executor or legatee can be established unless a court has granted the probate of the Will.

Probate can be granted only to the executor appointed by the Will. The cost of getting a probate includes legal fees as well as stamp duty on the value of the property being willed. The stamp duty varies from state to state. Probate is very important in case of Real Estate.

Legal heirs to get possession of the property from the nominees have to go through a legal process called probate. In Maharashtra this means, the will have to be submitted to Registrar and one will have to obtain a probate. The Registrar may ask the claimants to put an advertisement in newspaper to ensure that they will not be contested.

They may even ask the witnesses who have signed the will to come to their office and sign documents. After all this, and some court affidavits, the claimants have to pay the necessary tax to the state govt. which is hefty and based on property value. After Goverments takes its cut, then finally the probate order is given. Only then will the legal heirs get their property.

Note that, probate requirements differ from state to state. Hence even when making a will a Lawyer should be consulted. I know of fights between Nominees and Legal Heirs. Roadblocks put up by Goverment ( some times they ask for Registered Will etc.).

So just writing a will is not the end of the story. Better consult a lawyer before drawing a will.

Further please note especially in case of land or house property, the society will not transfer the flat without a probate and tax paid certificate. Many times, a prospective buyer will not buy a flat or land, if the holding is not clear and if the property had not been cleanly transferred and if there are disputes between nominees and legal heirs.

Flat may still stay in the dead person’s name till their heirs and nominees settle their disputes. Till then, the flat may be used by Nominees or any other person. But Society will not transfer the flat to prospective buyer till the process of probate is settled first. Hence such property cannot be sold easily.

Please proceed with great care in this matter.

Important points while making a Will

If possible, have the two witnesses be a doctor and a lawyer. A doctor signing a will, won’t raise any question of you, being of unsound mind. The lawyer, will vet the will and make sure you dont make stupid mistakes at the time of writing and signing it. 🙂

The attesting witness and his or her spouse should not be a beneficiary under the terms of your Will. This might create vested interests and some times make your will invalid. Also, make sure the witnesses are younger than you and not very old as your will might be in effect for several years! And you want them to be present in this world 🙂

Write your will on good quality thick white paper so it doesn’t get spoiled over a period of time. It should be stored in a plastic envelope in full size, without folds.

Note that you should keep just one more copy of will and stored separately from the original will. The will must be stored very safely in your bank, in safe deposit box. You must also inform your next of kin, as to where you have stored your will. Do not make many copies of your will.

In case of Hindus, it should be clearly stated if the property is inherited or not, because it makes a huge difference, as no ancestral property can be assigned to any person through a will. All rights on inherited property are acquired by birth. So if you inherited a property from your Father, you cannot say in a will, that you want to assign it to person X only! It will go to all your legal heirs as it is “Inherited”

A will must always be dated and if more than one will is made, the one with the latest date will nullify all the previous ones. In fact, there should be a statement in your will, nullifying all other previous wills. The pages should be numbered to avoid fraud.

The value of assets often fluctuates, so it is better to mention how much each beneficiary will receive, in percentage terms rather than absolute numbers. Unless it is pure cash.

So what appeals to you more ? Writing a will your self or hiring a lawyer for this and pay to him ? I hope you are clear about the rules and procedure for writing a WILL in India ?

Over time, we have seen a lot of products, and figured out some good ones. In the process of understanding them, we now believe that some things are always good — which sadly, is never the case.

So today, let’s have a look at just the flip side of all the products and concepts. This post is going to talk about the problems and issues associated with financial products & services.

Term Insurance

Term Insurance, as you know is pure risk cover, with a cheap premium. The problem with Term Insurance, is that many people get over insured because of the fact that premiums are cheaper in case of term insurance. Many people who need coverage of 25-30 lacs might end up taking higher amounts of insurance as it costs very less.

They might think that nothing is lost — What you lose, is the extra premium over the years for over insurance. At the end, your chances of death increases drastically (duh!). A lot of people on the other hand are severely under-insured because they think that just because term insurance does not return your money its a bad product , but these people are totally wrong (read why)

Equity Mutual Funds

Equity Mutual funds are taken as the best investment option by many. And they are, but not for everyone! A person needs to understand, that they are long term products, due to their inherent nature, equity funds should be invested in, for the long term.

Over a short period, like 2-3 yrs, Equity Mutual funds can be risky and can give you jitters whenever markets make a heavy movement to either side. Also your choice of funds matters! Choosing any equity mutual fund will not help you grow your money, since nearly half of the equity funds, under perform their benchmark indices themselves.

Debt Mutual Funds

Remember this, No Mutual fund is safe! There is always some kind of risk with every mutual fund, unless stated otherwise. Does any debt fund mention clearly that it’s 100% safe? No!

Watch this video to know more about debt mutual funds:

Debt funds are of different kinds and they are depend on several factors like inflation, price variation in bonds (More), the ability of corporate’s to repay the debt on time, and other economic indicators some times.

Overall, debt funds do not give negative returns and mostly perform better than plain FDs, but there have been instances of debt funds giving very low returns like 3-4%. Negative returns in short term, can’t be ruled out either. (link). Risk with debt funds though, is usually very small.

Many people also put money in Debt funds for very short term, just as an alternative to Fixed Deposits (FMP ?), which earns them marginally better returns but at what cost? How much in absolute terms? The quantum is so less, than it’s not worth the hassle.

Real Estate

“Real Estate is the best Investment!” – While that’s open to debate, let’s looking at the negative aspects and issues. First of all, real estate transactions are really complicated and as an investment it means you have to figure out a lot of things at every step of the transaction, else you might pay more than what it takes, every time if you don’t know the game.

There’s also no proper regulatory body in real estate, so things are unaccounted for, with no proper sound rules for the whole process. This means, every step has its own price depending on the city.

Another major issue with real estate is liquidity. You buy a flat, you spend 2-3 months on the whole deal and once things settle down, you live happily in it. But life takes a wrong turn, it can take several months to find a prospective buyer for your asset at the price you want.

It may be frustrating to see prices move down and no body ready to buy at your price, in which case you have to settle for less. You might have to compromise for a really low ball offer too, if you need money urgently for some emergency need, unlike fixed deposits, mutual funds and other products. (Returns from Real Estate)

PPF

PPF is considered to be the most secure and best debt product. However, putting money in PPF for 20 yrs can be just as idiotic as anything else. At the end, you are not getting more than 8% on your money, so only invest as much as is good & needed your asset allocation.

For a young starter his/her debt component is generally taken care of, by the EPF in the company. It makes no sense to put another 70k every year in PPF. It will just increase their debt percentage share in their portfolio to no good end.

Use PPF to build some debt component (Read a tip), but it’s not always prudent to put the whole 70K every year religiously. At the end, its not going to fight inflation very well. Want to open a PPF account at SBI , read here

Endowment/Money back Plans

They are totally secure products.., true, however the returns you get on your Endowment/Money back plans are pathetic . The worst part of these plans are that they trap you like anything.

Ask some one who has bought them recently, paid a couple of premiums and now wants to get out. The products are designed in a way that err, discourage you to move out of. If you do, you get a very small sum in return.

You cant beat inflation with these products, as the returns for all type of plans range from 3-6%, at the most 7% once in a while, depending on the bonus (and probably the phase of the moon :)) Don’t let the trust factor influence your thinking so much, it makes your financial life miserable.

ULIPs/ULPPs

Nothing wrong with the concept, but the costing of the product is such, that they are highly prone to mis-selling (and they have been mis-sold/mis-bought heavily.) You make some profit in a ULIP, but get out soon & the cost of the product will be very high. They are complicated products and 99% people don’t use ULIPs the way they should be (switching is not used by most people) .

A 3 year lock in period is often taken as “I can sell after 5 yrs and I will get 100% of my money”, which is not true. 5 years is just lock in, from a taxation point of view. If you sell the ULIP before 5 years, first you have to pay surrender charges and the the money you receive, will become taxable in the year of receipt.

Watch this video of Term plan vs Endowment plan vs ULIPS:

Direct Equity

The biggest problem with direct equity is that a very small number of people can do it right. Most of the people just feel they’re alright, till they get really screwed big time. Direct equity demands too much attention at times.

Also depending on your time frame, it can be addictive! And when you can’t control yourself, it can ruin your portfolio and wipe out your savings.

Gold

Too much confidence from investors. At the end of many years gold should be giving around 8-9%, a little more than inflation, but in this new generation, gold has done so beautifully that it might outperform earlier returns and end up giving 10-12%. Fingers still crossed though. Read a study on gold

SIP

SIP is sometimes seen as the ultimate solution for generating good returns, but SIP can give lesser returns in growing markets, so for people who have that ability to sense the movements in markets, SIP will prove to be wrong thing to do. These kind of investors can take a call on direct investment.

SIP is good for investors who does not have much idea about how markets functions but want to invest in equities without worrying about movements in the markets. So the best learning is, don’t start SIP after a bear market !

Diversification

You should always diversify your investments. Whats the problem with that? The main problem is that this is not true for a person who understands the ins and outs of an asset class and has all the time to closely look at his investments.

In that case, diversification will prove to be very costly. I know people who have 96% in Equity and they are doing wonderfully well, because they are masters of the subject and closely follow what’s happening to their money. So diversification is not the ultimate solution.

As Warren Buffet says, diversification is for one who does not understand what he is doing, which actually means that a person does not have much knowledge about an asset class to exploit it’s full potential. Most people fall in this category and for all those, it would make sense to diversify in Equity, Debt, Gold and Real estate etc.

I don’t see much negative in Health Insurance, other than the dilemma customers have, in choosing the right products for themselves. There are many things which a customer should look into a health insurance product which would suit him, but because of plethora of products & options, customers are confused and end up taking the inappropriate policies.

See 17 most asked questions and answers in Health Insurance here.

While we should cover ourself with health insurance, the best health insurance is good health by eating well and doing exercise everyday, read this ebook for more .

Saving Account

Though there is nothing called as “investing” in Savings accounts, maximum number of investors keep their money in their savings account unintentionally over and above their emergency needs and it’s like loosing your money to inflation , prices are rising at rate of 8-10% and your money is rising at 3.5% or even less. So in a way your money is depleting over time .

Fixed Deposits

While fixed deposits are excellent and easy short-term investment option, it leaves your money handicapped when you invest in it for very long duration like 10-20 yrs and many investors actually do it especially in smaller cities and towns , for them its the only investment option .

Though the number goes up in your bank account , the purchasing power remains at the same point or at worst decreases sometimes due to inflation and taxes overtime. So use Fixes deposits for short-term investments not very long-term.

Portfolio Management Services (PMS)

The biggest problem with PMS is that there are rare PMS which can be called good. PMS is also managed just like Mutual funds where some person or team takes the decision of buying and selling , the only difference is that its meant for HNI’s, who have minimum investments of 5-10 lacs.

There are high costs involved and most of the people fall in trap thinking that it’s some premium product which would deliver better returns . However there has been cases where PMS delivered great returns, in most of the cases they turn out to be a hype.

Most of the big companies in financial services run PMS schemes which do not have that strong performance or are half-baked . Read a review of ShareKhan PMS.

Comments ? Do you think I have left anything or any product ? Which was your favorite one ?

Do you remember your first stock market trade and how you behaved at the time? Just like you, even I, have made some really stupid mistakes in stock market Investment.

Today, I would like to share some mistakes (only the big ones 🙂 ) which I made during my first trade in stock markets. Its worth discussing, how I could have avoided those mistakes. You can learn from them too!

Mistake 1 : Buying on Others Recomendation.

27th Nov 2007 : I had just got my spanking new trading account and I was so eager to trade and make lots of money(How to start in Stock Market) .

I saw an Orkut community recommending GTC India – a “Buy” Recommendation. There were several good reasons discussed there, and an extrapolation on how it can reach from current price of 600 to 2000 in some months. It looked like a “don’t-miss” trade. I bought 10 shares @ 560/-.

Mistake : Buying only on recommendation and not analysing the opportunity well, over relying on others recommendation, buying a company which I do not understand enough .

Learning : Never buy, just on recommendation! Do your own study and analysis. When you buy on others recommendation, you don’t take responsibility if there is any loss, which is dangerous in markets.

Hear others but listen to your self. See other factors like market trends, sector view, global markets, future prospects et al. Once you are fully confident that its a good trade and you feel comfortable with it… go for it.

Mistake 2 : Being too greedy

After 3 days : Just after I bought the shares, it went up from 560 to 800 in 3-4 days. I thought that its moving as expected, and bought 10 more shares at 800. Within another week, it went up more to 950! Now, I was flying!

I bought 10 more shares @955 again, to reach the target of 1500+ . My average buy price was now 772 . I was feeling little bad for not buying 30 shares directly @560 in the start .

Mistake : Greed! Pure & simple… This is a very common mistake, a big mistake at that – so big that it will be among the top mistakes investor and traders do. Buying more wasn’t wrong. It was the intention behind the buy. There is nothing wrong in increasing the position once it moves to your target, but it has to be backed up with strong reasons and study.

It should be a trade with high probability of success. In my case, it was not. It was just a recommendation from someone in an orkut community, with a couple of lines, explaining, why it will go up .

Learning : There was no need to buy more shares that point in time. I should have just sat back and watched. The Stock market is just like our life, you need to have a level of satisfaction in your life and stock markets.

If you want more and more and more, you might not get anything. In fact, you can lose heavily. Because of greed, I invested more than I could afford to lose. I took an unwanted and unaffordable risk, because I only saw profits and never the potential losses.

Mistake 3 : No profit booking on Time

After 1 week : The prices were not moving now. It was going up a bit then coming down again and was stuck in a range of 900-1000. It went up to 990 once. For a time being there was doubt in my mind if it will not move up to 2000 and will return back to my buy price levels.

Mistake : No profit booking. There was a sharp rise in shares price from 550 to 900 in just 2-3 weeks and that is rare. It doesn’t happen to every stock, it was an excellent return, but i did not book profits.

Instead of making the best of the situation and taking the (not so bad) profits, the market was offering me, I wanted more and more and lost even what I was getting. The reason was Greed, again.

Learning : The better thing to have done, was to book profits, at least partially… Situations change in markets, I never checked on any news regarding the company after i bought the shares, and I was never updated about it. Every time you get some good profit, its a wise idea to at least book some partial profits out of it (Unless you have really strong reasons to hold it for long) .

Mistake 4 : Having Ego

In next 1 week : Prices now started coming down. It came to 900 first, I was scared and told myself that I will book profits once it goes back to levels of 950+. It never did! Then it came back to 800 and I regretted not booking a profit at 900 and said to myself again “I will book it for sure when it comes to 850.”

Guess what? It never did! Then it went up a bit again and went up to 850 . I forgot my promise to myself & allowed my greed to take over my promise. It went down again after that and now it was near my average buy price. This was the time I was feeling, “What a big fool am I, for not booking Great profits!”

Mistake : Ego ! Fear of losing part of profits, another mistake was the fear of not making any profits and fear of losing some money . Fear! Fear! Fear!

Learning : “When your boat starts sinking, you don’t pray… just jump” Once you are doubtful, surrender to markets wish. See what markets are showing you, not what you wanted to see. Markets are supreme and no one can be smarter than the markets.

Leave your ego at your home, when you go in front of Markets. The markets tell you what’s going to happen, not vice versa. Accept that you are wrong and you made a mistake. Then move on.

Mistake 5 : No Patience

After few days : Then the prices started falling and plummeted to 600 (my original buy price). Now I was in loss. I was proven wrong, but I just couldn’t accept it. I kept trying to prove myself right by holding it and hoping it would come back up. Yea, you know… It never did 🙂 .

It went lower and lower and lower and I was just praying & hoping that it’d return back to a level where I’d be happy to sell it. It never did! It went up to 300 and I sold it all in frustration. Then, I saw it go down to 250 and bounce back to 500! Now, I was feeling like I was cheated by the market for not giving me the right opportunity to exit.

Mistake : Impatience, Fear and not cutting my losses short. I exited at a very bad time, at almost the lowest price then. There was an opportunity for me to exit at small loss, but taking a loss hurts the ego and it did. Not cutting my loss in time was the result, of my not defining my loss early enough.

I should have had thought of it earlier. Then, I’d just pull a trigger, when it reached that level, without emotions. Fear overtook common sense, Fear overtook logic .

Learning : I should have defined my Target and Losses before taking the trade. I should have been realistic and logical. I should have waited little mo.re time and then exited at a better price. I should have consulted someone, better than me (At that time though, even a street dog could have given a better advice than me :))

Price of GTC INDIA after this Incident : It never went above my price levels after that and went to Rs 55 after couple of months , even today (Nov , 2010) , its hovering below Rs 65 only .

Conclusion and Summary

My first trade was not at all planned and “no plan” is “a plan to fail”. Fear ! Greed ! Emotion! Ego ! Impatience! These are the elements of Failure in Stock markets. Manage them well and you’ll do better !

We love Diwali—with its wonderful feeling of a fresh new start. And, it came just in the nick of time. A lot of people always want to know the best investments they can make? This Diwali, we want to share one of the greatest investment tip with you. If there is one single investment with the potentially highest payout, we would argue that it is maintaining a healthy body. All too often in the pursuit of financial health, we forget that we also need to invest in caring for our physical health.

We don’t stop playing because we grow old; we grow old because we stop playing.”

Everybody is running around the best 4 star, 5 star rated mutual funds, stock or the cheapest term plan or any killer tip which will make them wealthy. However we often forget more important things in our life like Education , good values and great health which is more critical part of our life , Health is our True wealth and today we want to share an e-book which will help you understand how you can make your life more simpler and healthy using some basic suggestions made in the book.

If you want to invest this Diwali, the best thing I would recommend is to invest some hours of your time to read this valuable ebbok (atleast go through the content page and you will love it) , and your will reap the benefit all your life.

Thanking you all to be part of this awesome community 🙂 . Happy Diwali to you all

Are you confused about many things when it comes to Health Insurance in India ? Are you afraid of rules and regulation in Mediclaim policies ? Don’t you have a clear idea about how will you deal with various things in Health Insurance and delaying your decision of taking a Health Policy ?

Today we will look at most frequently asked questions in Health Insurance try to answer those questions.

1. Can a person get claim from his own company and spouse company if they are covered under both companies ?

Yes, if both husband and wife are covered from their employer, they can claim from insurance provided to them by both the companies.

For e.g. if husband is covered for 1 lac under group insurance policy from his company (and her spouse is also covered under her husband company policy), and the same situation exists vice versa, both of them are then, actually covered for 2 lacs each; 1 lac from their company and 1 lac from their spouse’s company.

Now if something happens and husband gets hospitalized and expenses are 1.8 lacs, then husband can make a claim of 1 lacs from any one of the company and remaining 80k from other company. If you have cashless facility then you just show both health cards. If you don’t, you can get reimbursed by insurance company.

One important point worth noting is that during reimbursement, one should apply for the reimbursement first to his parent company and then to the one of his spouse. See some hidden health insurance policies

2. Do we have to notify the company about any illness or habit developed in between?

No, we are not required to notify the company regarding any complication or health issue. If the policyholder is hospitalized, the company will automatically come to know of it. Otherwise, no need to inform the company about any such policy.

If you notify the company, your premium for year after notification will increase, if it is under their list of illness to be checked. If you don’t notify the company and when you go for a claim, they will come to know that it was developed earlier and the claim will be settled accordingly and from next year onwards they might put loading on it (All these reasons vary from company to company).

So whether you tell them or not, it’s the same thing. They have doctors panels with whom they check your details before giving you the claim.

3. Does Health Insurance cover everything from accident, surgery, normal hospitalization ?

Yes, Health Insurance covers you for everything, provided you were hospitalized, be it for any reason; due to accident, illness, or disease. If someone met with an accident and he is hospitalized, then his mediclaim policy will pay for his bills, no exceptions.

Watch this video to know what are the things to look for while choosing a health insurance plan:

4. What are the advantages of sticking to one Health Insurance company for a long time ?

The plus point of sticking with one company is that if someone is suffering from any pre-existing disease at the time of commencement of policy, those complications will be covered after 4 years. Until portability is introduced in India, this is the single biggest advantage to stick with one company for long.

Another advantage is that when you have a continued policy from any insurance company, after few years you get bonus or discount in premium.

For example: Suppose you have a policy of 3 lacs and you are with the same insurer for past 4 years you can get a bonus of 50% i.e. you pay premium for 3 lac only but you get coverage of 4.5 lacs. Similarly some companies don’t offer bonus but they offer discount in premium i.e. for coverage amount of 3 lacs you pay lesser premium than actual amount.

So if you don’t have any serious problems with the insurance company then it is better to stick to one company.

5. Can NRI’s take health insurance? Can they travel to India for treatment and claim? What about emergency situations ?

Yes NRI’s can take Health insurance in India. They can definitely travel to India for treatment and can claim it. however they will have to show their residence proof, ITR and a few other documents. If they don’t have those documents, then they are not eligible to get insured in India.

The cost of treatment in India is different and cheaper than countries like USA, UK and other European countries. The premium amount computed depends on Indian conditions and parameters. So if a NRI has health insurance form Indian company, that person would be paying premium as per India actuaries and obviously cost of treatment in his residing country would be higher than India.

For example:

If a person get dengue and he is very critical and requires urgent hospitalization, the cost of treatment in India would come up to 1-2 lacs (and this is on higher side.) The same treatment would cost around 10-15 thousand dollars in US so this burns a hole in insurance companies’ pocket.

6. How to claim successfully in case of emergency and planned hospitalization?

The most basic fundamental for a smooth claim process is keeping all your documents up to date. If you have a past history of illness, make sure that you submit those documents too, because the TPA department will come to know whether it’s a pre-existing disease or not.

While submitting your documents make sure that all the documents are proper and there is no missing document pertaining to your illness. This will just give a chance to TPAs to make excuses and you will have to run for your money.

It’s worth noting that in case of planned hospitalization, if you inform your mediclaim company in advance and take prior authorization, everything will be settled by the mediclaim company or TPA, without the policyholder been required to submit any document.

7. Is it better to take accidental policy separately or mix it with term insurance as a rider?

If your accidental policy is a rider with some Term insurance (9 most asked questions about Term Insurance) then you must take care that it covers everything what accidental policy should cover. Generally when a policy is offered as a rider it does not cover each and every aspect.

For example: An accidental policy offers insurance against partial disablement, loss of limbs, hands and many other parts. But in a rider, many insurance company offers insurance against permanent disablement only and not for partial disablement and loss of body parts.

Also note that, because accidental rider is much less if taken with Term Plan as compared to the personal accidental policy taken stand alone. Under term plan, accidental death benefit could be taken for as little as Rs.1000 for a cover of upto 15 lakhs where as in a stand alone policy the same amount will be available for a premium of around Rs.2000. So it depends.

8. What are the top most things one should check in the policy documents ?

The first thing one should have a look at, is to check what the exclusions in the policy are. This is because, we get information on what is covered but no insurance company will give information on what is not covered and this creates a problem at the time of claims. So to avoid any surprises, one should have a thorough look at exclusions as well.

For example: A new circular was passed by many insurance companies few months ago in which they provided only Rs.20-24 thousand (different companies had different rates) compensation for cataract operation. Earlier there was no limit on it.

So sometimes in list of coverage for health insurance we just read the tabular format given by companies but don’t go inside to see the details and this can land us in soup sometimes. Many insurance companies now provide Maternity benefits but they limit it to coverage of only Rs.20-30 thousand, we just see that maternity benefits are given but sometimes fail to notice how much coverage is given.

9. If there are no loading charges, can premium still change on renewal?

This is a very big question with very easy answer..If you check the premium structure of any of the mediclaim company, either there premium is increasing every year or they have premium slab for different age groups; something like for age 30-35 premium is 4200 and from age 36-40 its 6700.

So under this second policy, when the policy holder moves from age 35 to 36, his premium suddenly jumps by Rs.2500 and this is not loading.

So yes, premium can/will increase irrespective of loading after certain age.

10. Is it a good idea to split health insurance into 2 policies? Tips?

No logic for doing this except personal preference. If you are taking another mediclaim policy just to increase your cover, why not get your cover amount enhanced in the existing policy/company.

Get another mediclaim policy only if certain other company is offering feature/features which your existing policy does not and you have surplus funds at your end to afford 2 separate mediclaim policies at a time. No other reason to, otherwise.

11 . During the course of my treatment, can I change the hospitals?

Yes it is possible to shift to another hospital for reasons of requirement, of better medical procedure. However, this will be evaluated by the TPA on the merits of the case and as per policy terms and conditions. Note that it would be prudent if you check the network hospital list and go to the best hospital in the beginning itself rather than changing midway.

12. What are the situations under which one may be denied cashless hospitalization?

If there is any doubt in the coverage of treatment of present ailment under the Policy if the information sent to TPA is insufficient to confirm coverage

When the ailment/condition is not being covered under the policy.

If the request for pre-authorization is not received by TPA in time. In such a situation, the Insured can take the treatment, pay for the treatment to the hospital and after discharge, send the claim to TPA for processing.

In case the hospital in not on the panel of the company or the disease/illness is pre-existing and not covered for 4 years.

13. Whom can I approach in case of a conflict with insurance company with regards to my claims?

The Grievance Redressal Cell of the Insurance Regulatory and Development Authority (IRDA) looks into complaints from policyholders. Complaints against Life and Non-life insurers are handled separately. This Cell plays a facilitative role by taking up complaints with the respective insurers.

Policyholders who have complaints against insurers are required to first approach the Grievance/ Customer Complaints Cell of the concerned insurer. If they do not receive a response from insurer(s) within a reasonable period of time or are dissatisfied with the response of the company, they may approach the Grievance Cell of the IRDA.

Private Insurers:

Shri K.Srinivas, Asst. Director,

Insurance Regulatory and Development Authority

Consumer Affairs Department

United India Tower, 9th floor, 3-5-817/818,

Basheerbagh, Hyderabad – 500 029.

E-mail ids: [email protected]

Public Sector Insurers:

Mr.R.Srinivasan, Officer on Special Duty

Insurance Regulatory and Development Authority

Consumer Affairs Department

United India Tower, 9th floor, 3-5-817/818,

Basheerbagh, Hyderabad – 500 029.

E-mail ids: [email protected] . As claims/policy contracts in dispute require adjudication and the IRDA does not carry out any adjudication, insured’s are advised to approach the available quasi-judicial or judicial channels, i.e., the Insurance Ombudsmen, Consumer for or the Civil courts for such complaints.

The list of Insurance Ombudsmen along with their contact details are available on this website under the heading ‘Ombudsmen

Here is the link

If you have a good broker from whom you have purchased the policy, then they will help you in coordinating with health insurance companies.

14. What is the difference between Critical illness insurance and normal health insurance ?

In a critical illness policy you are covered for certain mentioned critical illnesses only. Some of coverage’s are Kidney disease, brain tumor, and major organ transplant and many more depending on the companies.

If you have normal health insurance you will definitely get covered for critical illness but in critical illness you won’t get coverage for normal disease like malaria, typhoid.

For example: If your age is 25 and you buy normal health insurance from any XYZ company and let say its premium is Rs.3000 for cover of 3 lacs but if you buy critical illness policy for 3 lacs the premium would be less because considering your age the changes of you getting a critical illness is lesser than any normal disease.