What are pension plans and how do you identify the best pension plan in India? Is it the LIC pension plans or some pension plan policies from pvt companies or some unit linked plan from companies claiming to provide you with Rs. ‘X’ for ‘Y’ numbers of years once you retires? In this article we will see some of the disadvantages of pension plans in India and how they work.

A lot of investors think that retirement pension plans are the only way to go; and if they do not invest in these products today, then they will miss out on something. In this article let’s talk about pension products. Before I move ahead I would like to coin two terms used in Financial planning which are very easy to understand.

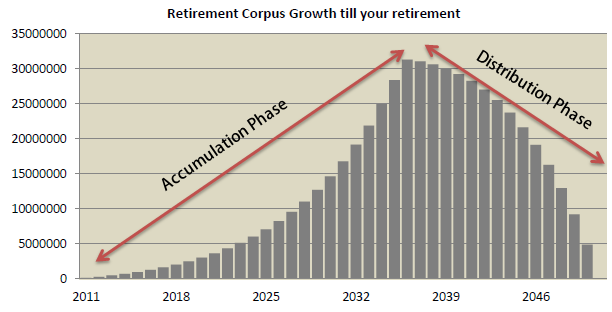

Accumulation Phase : Accumulation Phase is that period of your life, where you invest regularly each month and “accumulate” the Wealth. You start getting pension later in life. So when you invest your money in ULIP’s, Mutual funds, Direct Stocks or anything else you are into accumulation phase.

Distribution Phase : This phase refers to period when you start withdrawing money from your already accumulated wealth for consumption purpose. So at the time of your retirement or even before that, when you start taking out certain amount per month for next ‘N’ years, that’s called distribution phase.

Two major categories of Pension Plans

Let me start by taking about pension plans and their types. There are mainly two type of pension plans at broad level.

Deffered Annuity Plans : Most of the pension products in india are sold by LIC and all the private companies are deferred pension plans. These plans have accumulation phase inbuilt in itself and hence you first pay premiums for ‘X’ number of years. Once you retire, then you start getting pension income. You can see these types of plans all over the market. Some examples are LIC Jeevan Tarang, LIC Jeevan Nidhi, Bajaj Allianz Swarna Raksha ROC , New Pension Scheme (NPS)

Immediate Annuity Plans : These products are called immediate annuity plans because they start paying you the annuity right from day one once you make a lumpsum payment. So if a person wants a monthly pension and has huge lumpsum money, he can buy an immediate annuity plan and start getting pension. It’s a simple product which is not so much popular in India like deferred annuity plans. Some of the examples of immediate annuity plans are LIC Jeevan Akshay , ICICI Pru Immediate Annuity , HDFC Immediate Annuity .

4 reasons why you should not buy deffered annuity plans

Let me tell you 4 strong reasons why you should avoid buying pension plans in India .

1. There are better options for growth of your wealth

The accumulation of your wealth happens in a pension plan for many years, but it’s not the best way your money can grow, ultimately if you had to invest your money in equity (underlying asset class), you have simple and no-cost options like mutual funds, index funds. Also you can choose to put money in real estate. A regular SIP in an equity diversified mutual funds should give much better returns then accumulation in a pension plan (read unit linked products).

2. No predictable returns for annuity

The core function of a pension plan is to give you pension. But do you know how much returns you will get out of your pension plans when time comes for retirement? A lot of pension products do not give a clear idea on how much will you get at the end. What is the return earned is around mere 4%? What will you do? The same is true for NPS.

One major (I mean MAJOR) DRAWBACK is you have no clue what will happen once you finish the accumulation stage and go on to the withdrawal stage. Let us say you have accumulated Rs. 500 lakhs in a NPS account. They allow you to withdraw say 50% of the amount and the balance has to be invested BACK in an annuity. Let us say you ARE FORCED to invest Rs. 250 lakhs in an annuity which pays Rs. 11,000 per month as a pension…looks good? Well depends on what you are capable of doing with your own money!

At this point of time, the better alternatives would be old fashioned products like Post office monthly schemes , Fixed deposits with monthly payouts or even senior citizen savings scheme. these all give near inflation returns atleast .

3. Rigidness and no flexibiity

Almost all the pension products are rigid in taxation and what you can do with your money at the end. Under current laws you can withdraw only 1/3rd of your accumulated money tax-free, where as there is long term capital gains at the moment is 100% tax-free. Also it’s compulsory to buy annuity for the remaining money. What if I want all my money for some reason at the end? What if I don’t have a requirement for income later?

These problems won’t be there if you accumulate your money in plain vanilla mutual funds or PPF or other simple investment products.

4. High charges

Who does not know how ULIP’s and other similar products have charged so high costs for initial years without giving clarity to customers. These annuity plans also have high allocation charges many times and customers do not know about it and can’t do much later when he acknowledges it! So why do you want to pay high fees for these products?

Conclusion

It’s suggested that you invest in some instrument which does not have any rigidness on what can be done with your investments at some later stage, like Mutual funds, Direct Equity, PPF, Index Funds, Real estate or even old fashioned products like FD, NSC, KVP… You can create your own accumulation stage and when the time comes for “distribution phase” (pension), you can always buy some immediate annuity plans or create your monthly income through ways of renting out property, getting FD interest or plain dividends from stocks or any combination of these. I hope you have got a fair understanding of what are pension plans in India.

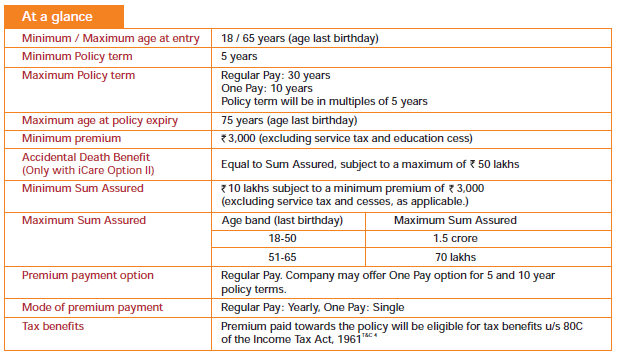

ICICI Prudential has launched their new online term plan called “I-Care”, which will replace its old term plan called the “i-Protect” (read iprotect review). This new i-Care term plan has some interesting features like no medical examination till the age of 50 and up to 1.5 crores of sum assured can be taken.

Features of I-Care Term plan

The biggest surprising feature of i-care term plan is that there is no medical examination for customers who are up to 50 yrs old. For all the health related information the company will depend on the declaration made by the customer as there won’t be medical tests applicable. This will make sure that the policy is accepted as soon as possible as there is no medical examination in between. Also there is something called “Policy acceptance” in i-care, which means that once you submit the application online and make the payment, it will be reviewed and finally it will be accepted, after which your insurance coverage will start. Some other features of i-care policy are as follows.

Additional features

There will be high cover available to those people who have active home loan in their name.

The premiums once declared will not be increased later, as there is no medical exam later.

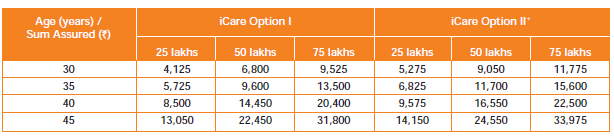

Riders in i-care term plan

There is only one rider in i-care term plan just like iProtect had and its accidental death rider. So here are two options one can go for while buying i-care term plan.

iCare Option 1 – Sum Assured

If you take option 1, then you just have a basic sum assured cover which will be paid in case of death. Even if you die in accident you will still get the basic sum assured.

iCare Option 2 – Sum Assured + Accidental Death Benefit

In this option, if one dies due to accident, then the nominee receives extra money equal to sum assured (subject to maximum Rs 50 lacs). This means that; if a person has taken second option with sum assured of 80 lacs, then he will get 80 lacs on death if the death is due to anything other than by way of accident. But if the death is due to accident, then nominee will get Rs 1.3 crores (80 + 50)

Below are the indicative premiums for both the options.

Note : Please make sure you read the terms and conditions properly (mentioned in the 5th and 6th page of the embedded doc above).

Do you know how you can use Hindu Undivided Family (HUF) to reduce your overall tax liability? In this article I will give you tips and real life examples on how you can use HUF to save taxes legally.

Before that let’s understand what HUF is.

The concept of HUF says that apart from individuals there is another separate entity called “Family” which can also have its own assets and liabilities and even regular source of income, which should be taxed separately.

For example :

If an ancestral residential property is rented out, then the rent arising would be considered as Family’s income and not as income of individual. In real life this rent is shown as income of one individual and he pays the tax on it, however a HUF can be formed and the rent can be shown as the whole family income (HUF) and it can be taxed separately.

Until a few years, many Indians used to keep multiple PAN cards and used to show Income under different PAN cards and used these tricks to avail the benefit of slab rates by showing themselves as different persons. This however is illegal by law and is a punishable offence as one person cannot have more than 1 PAN Card.

But, one legal way of obtaining an extra PAN Card is to form an HUF. As the Income of an HUF is taxable in the hands of HUF and not in the hands of any Individuals, a separate PAN Card is issued for an HUF and the benefit of income tax slab rates can be availed on this PAN Card.

Formation of HUF

A false impression amongst people is that HUF needs to be created whereas the truth is that an HUF comes automatically into existence at the time of marriage of an Individual and no formal action needs to be taken for the same.

However, in case a person who wants to specifically register for creating an HUF, he can furnish a creation deed on a stamp paper (The Format of Creation Deed can be downloaded from here).

As HUF is governed by the Hindu Law and not by the Income Tax Act, individuals belonging to other religions are not allowed to form HUF except Jain’s and Sikhs who can create HUF even though they are not governed by the Hindu Law. Two entities are extremely important for you to know in HUF are the coparceners and members.

Coparcener is someone who has the right to demand the share of the property of family; coparceners are generally the Karta (Main decision maker of family, usually the Father, but Manmohan Singh had 5 years ago brought an amendment which stated that Females can become Karta & there can be an all female HUF as well), then sons & daughters, grandsons and great grandsons in order of their first right.

Wife of the Karta is not a coparcener or even spouse are not coparceners and hence can’t demand/ ask for any share in HUF, they are just merely members of HUF.

Example of Tax Saving by forming an HUF

As discussed above, the main advantage of an HUF derives from the fact that an extra PAN Card is issued for the HUF. We’ll explain this tax saving benefit with the help of following example.

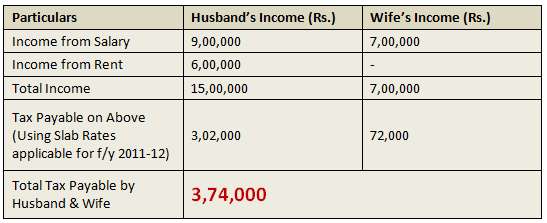

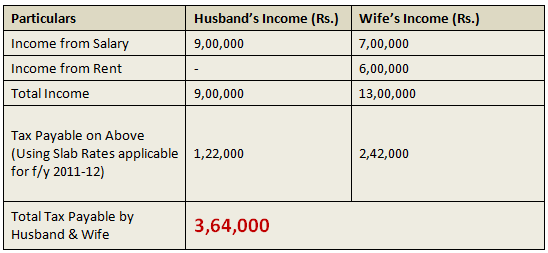

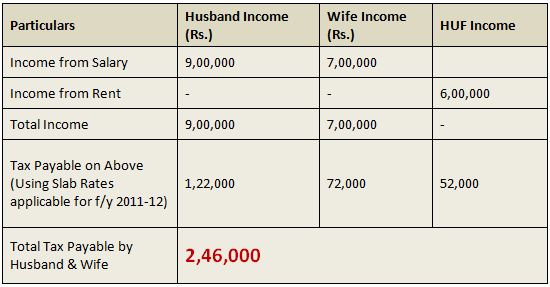

Lets say there are 4 members in a family

Husband – Salary 9 lacs

Wife – Salary 7 Lacs

2 Children without Salary

Additionally, one ancestral property which fetches them an annual rent of 6 Lacs p.a

Now the Question is – In whose hands should this Rental Income of Rs. 6 Lakhs p.a. be taxed? In real life, the most sought after solution is to show the rent as income of wife or anyone who has no income or less income so that the tax liability is least. But is it the best solution?

Let’s see 3 different cases here in which this additional rental income can be shown and how tax can be saved!

Option 1 – If this Rental Income is shown in the hands of the Husband.

Option 2 – If this Rental Income is shown in the hands of the Wife

As this Income is arising to the family as a whole, the Govt has also extended this option of taxing this Income in the hands of the whole Family. Although very few people in India know this fact family income can also be taxed in the hands of the whole family by forming an HUF.

Option 3 – If this Rental Income is shown in the hands of the HUF

The above 3 options clearly indicate that Option 3 is the best option as the least tax would be payable by the family if the Rental Income is taxed in the hands of the HUF.

The tax saved by showing this income in the hands of the HUF is Rs.1,18,000 (i.e. difference between “tax paid if rental income is taxed in the hands of HUF” and the “tax paid if shown in the hands of the wife which is the 2nd best alternative”)

Please Note: For the sake of simplicity, Taxes have been computed without taking into account the “Deductions available under Section 80C“ and “Education Cess applicable on the Tax Payable”

Procedure to create HUF

These are the steps to create capital of a HUF.

First one should open a bank account with the name of Hindu undivided family like “AJAY HUF” with a stamp, ID Proof and the proof of the members of the family of HUF.

Important :- While opening a Bank Account in the name of HUF – Banks always ask for a rectangular stamp which states the name of the HUF and also the Karta who is signing it. A round stamp is not accepted as per RBI Circular. The same applies at the time of opening of bank account of Sole Proprietor as well.

Next is to apply for PAN (Permanent Account Number) of the income tax.

Now transfer money by gifts etc to HUF capital keeping in view the clubbing provisions and tax on gifts under Income tax act, Remember there is no Tax on gifts in kind though they may attract clubbing provisions in some cases.

3 real life tricks of saving taxes through HUF

1. Saving tax by getting gifts

One way of saving tax is by transferring the money received from strangers or family are taken as gifts in name of HUF. So if Ajay starts his HUF called “Ajay HUF” and he is getting some gifts from his father, friends or anyone else, he can ask them to give it to “Ajay HUF” and not Ajay itself.

That way the gift will be treated as income/asset of HUF and taxed separately.

One important point here, if some stranger is giving gift to HUF, there is a limit of Rs.50,000 on which no tax has to be paid, but actually it can go up to Rs 1.8 lacs as the taxable limit is that much, and if one also has to do investments of 1.2 lacs (total 80c limit), then one can afford to receive up to Rs.3 lacs of gifts in a financial year and there will be no tax liability at all.

2. Assign ancestral properties and wealth to HUF and invest it

If family is going to receive an ancestral property or any wealth, then it’s better to transfer it on HUF name so that whatever earnings happen in future in form of rental income or capital appreciation of assets becomes income of HUF itself and taxed in its own hands.

That way the total tax liability of family can be minimized.

3. Use HUF income for expenses and Insurance for Family

As HUF enjoys separate tax benefit under sec 80C, one can use the income of HUF for buying Life & health insurance for family and the permissible deductions can be availed for tax purpose in hands of HUF, so if the total premiums for insurance requirement of family is Rs.50,000 per year, then It can go from HUF income and also the individual can exhaust his 1 lac limit separately via PPF, ELSS and other tax instruments.

Also family day to day expenses can be used from HUF income and hence it will leave other members with more disposable income which one can use to service higher EMI’s if required.

Watch this video to learn more about HUF and Tax saving:

Some important Points you should know about HUF

For creating the HUF one need to get married, there is no need to have child or children for creating the HUF.

An HUF can recieve any amount in gift from bigger HUF’s (HUF of Father, HUF of Grandfather) or any gifts received by the members of HUF (birthday, marriage, etc.) can be treated as assets of HUF , but stranger can gift HUF, not more than 50000 rupees.

Daughter also continues to be a Coparcener after her marriage of that family whether she also will be a member of HUF of her husband. So that way daughters can be co-parancers in two HUF’s 🙂

HUF can pay remuneration to the KARTA of family for the interest and expenditure to run the family business.

Be cautious with HUF creation

While all the above points excites people on opening a HUF account immediately and start taking tax benefit, there are some caveats and one has to be little careful. Remember that HUF is a separate entity and represents the whole Family. So once some assets is assigned to HUF, then it becomes part of HUF only and one can be suddenly take money from HUF for personal purpose .

If other co-parceners of HUF demand the partition of HUF only then one can get his/her share of the HUF. Otherwise it will not break. Also for taxation point, a lot of people mislead the tax department buy using fake HUF transactions and therefore, HUF is looked with high degree of scepticism.

If the HUF is not formed properly and if the assets are income are fudged for evading tax, it can get you in trouble, therefore it’s highly advisable to hire a good CA and create your HUF in the best possible manner with right advice. There is no harm in paying 10,000-12,000 to a CA if HUF can give you 5-10 times tax savings.

It would be a great investment, not an expense!

HUF property cant be mentioned in the WILL

Though HUF is very useful tool but one has to use it very judiciously and thoughtfully. Don’t look for tax benefits only , but practical problems also. Be aware that you cannot make a will out of HUF property. Once transferred to HUF, the assets /property becomes of HUF and you no longer have any individual right on it.

To explain with example –

“A”, who has 2 daughters and a son.He long back ago purchased a house in the name of HUF and put that house on rent, so that the Rental income comes to HUF and will not be be added in his or his spouses’s income .

But now , he ‘s retired and wants that this property should be transferred to his son after his demise. But this is not possible as that property belongs to HUF. He can’t even write a WILL for HUF property and with the huge rise in Real estate prices, none of daughter is ready to leave her share in it.

HUF will be extremely efficient for those people who have a higher income and high saving rate and some form of ancestral assets which can be marked as “Family Assets”.

Evaluate if HUF can really give you that kind of tax advantage or not for people who do not have high salary or who do not have a big enough family. So make sure you can get the maximum out of the HUF and understand the limitations of opening HUF before you go for it.

This article has been authored by CA Karan Batra who blogs on charteredclub.com (Content added by Jagoinvestor with inputs from Karan)

Can you share how was the article and did it help you in understanding Hindu undivided Family? Are you going to open a HUF account?

LIC online Term Plan is soon coming to markets ! . There is some good news for all those who would either like to take up a term plan or who are looking to upgrade (increase) their life insurance cover! It is recently disclosed by LIC that Term Plans will be sold online and offline and the premiums will be cheaper than the current rates offered.

I personally never thought that LIC would come up with online term plan because of its dependence on agents’ network for selling its products. But this is a good move from LIC as their share of term plan market is eaten away by private insurers from last few years. At the moment, a person has to pay a very high premium for term plan through LIC. For example, the premium for 25 lacs cover with LIC term plan at the moment is around 7,000 – 8,000, whereas it’s around 3,000-3,500 in companies like ICICI iProtect & Kotak e-preferred.

“We are in the process of designing a pure term product which would be sold through both online and through agents,” LIC’s ED- marketing S Roy Chowdhury. “The rates will be lower than what is charged at the moment,” he added.

LIC uses mortality table 1994-96 at the moment

Do you know why LIC premiums are higher? One of the reasons is that they follow old mortality tables which has older death experience ratio. A lot has changed in last 10-15 yrs and we have much better access to health care and lifestyle, which has changed the number of death. Most of the new companies in Life insurance use the latest mortality data but LIC is still using old data and that’s pushing their premiums. Now LIC is planning to revise the mortality rates based on the last 10-15 yrs of experience and hence the premiums would drop down from its current level.

Note that mortality experience are different for different age groups and classes, so it’s not necessary that mortality rates will go down it might happen that mortality rates for age group 25-35 goes up because of the bad lifestyle and new age ailments (stress, junk food, etc). So keep that point in mind. (9 most asked questions about Term Insurance)

How cheap will be LIC online term plan ?

LIC online term plan will be cheaper than the current term plan they offer but expect it to be 15%-25% lower than current premiums. Do not expect a very steep decrease like 50%-60%, because LIC is a very different ball game than other life insurance companies. LIC has accessed in each corner of India and the new online term plan they will launch will be targeted at a very big group and scattered across various cities. It will be offered online and also offline (through agents).

How will this impact Insurance Industry ?

With whatever little I know I can see that urban class will welcome this move with open heart and a lot of people who trusts LIC like anything and even a lot of people who are not big fan of LIC will wait and watch for this online term plan from LIC and would like to go for it only. This move will lead to more sales of LIC term plans in bigger cities and reduce the term plan selling of different other companies (to some extent).

What do you think about LIC online term plan . Are you going for it ? Are you waiting for it ?

Most of the people investing in mutual funds through agent offline have this question – “How to redeem mutual funds ?”. mutual funds investors often do not know what the procedure to redeem these mutual funds. I redeemed some of my ELSS mutual funds (HDFC tax saver , Sundaram Taxsaver, HDFC long term advantage Fund and SBI magnum taxgain fund) which I had bought some years back from an agent, so I thought why not let everyone know what is the simple procedure for redeeming the mutual funds.

Process to redeem Mutual Funds

if you have bought the mutual funds from an agent or from the AMC directly, then you will have to fill up the mutual fund redemption form. This form is available from the mutual funds AMC office (you can get its office address from internet). You will have to go to their office in person. You can also go to the nearest CAMS office and fill up the mutual fund redemption form directly from there. It’s much convenient to visit CAMS office and directly redeem more than one mutual funds in one go (this is what I did in my case).

The redemption form is very easy to fill and all you need to put is your name, folio number (make sure you put correct folio number, else it will create issue later) and the number of units (exact number or ALL) you want to redeem. Just give this form to the CAMS processing assistant and they will put up your request.

Important Points

1. NAV Applicable: If you give your redemption request before 3:00 pm, the same day closing NAV will be applicable, else you will get next day NAV. So make sure you do the redemption well before 3:00 pm if you want same day NAV.

2. Bank accounts: Where will you get the money when you redeem the mutual funds? You will get the proceeds in your same account which is registered with your AMC (which you used to pay at the time of buying). If that account is not active, then there are few run around like you will have to attach the cancelled cheque of your new bank account or copy of pass-book etc and if you don’t have that, then a declaration from the bank and sign of some bank manager etc. So this can be a little frustrating if you are in urgent need of money. In my case my old account was active so it was pretty easy for me.

3. CAMS do not handle all the AMC’s redemption: CAMS do not handle each and every Mutual funds transaction. It can happen that you will have to go to the AMC office itself for redemption. Like in my case I had to go to Sundaram AMC office to redeem my Sundaram Tax Saver proceeds. So check with CAMS which all mutual funds they handle, you can shoot an email to your city CAMS (their emails and addresses are there on CAMS website

4. How much time it takes to get money? : It generally takes 3-4 working days to get the money credited in your account. But in my case I got it in next 2 days itself. So if you redeem the funds on Monday or Tuesday, you can safely assume that you will get the money by the weekend. But if you have weekend falling in between, then it can take some time.

Process of redemption if have bought Mutual funds online

If you bought your mutual funds from your demat account or some online brokers or if you activated your online account after buying from agent, then you can redeem your mutual funds online itself just by following the procedure mentioned by your online account. Most of the people who buy tax saving mutual funds (ELSS funds) online can also redeem tax saver mutual funds online only.

Did you activate your online account with the AMC ?

If not, I would suggest you to do it, so that you can take the redemption action as and when required. What was your redemption of mutual funds experience? What point’s people should keep in mind while redeeming? I hope you are now clear on how to redeem mutual funds ?

Do you want to increase the SIP amount for your mutual funds ? Or you want to keep it constant always ? A lot of people start with a SIP amount at first and then look forward to increase SIP amount later. This is a very common of every investor and its “how to increase sip amount”

Increase SIP amount

When we say “SIP”, it generally means constant SIP, which does not increase every year. When we calculate SIP amount using any SIP Calculator – the SIP value is generally very high and does not look realistic and at times and such high investment can trigger affordability issue. However there is a clear solution for this, which is used by financial planners and that’s called “Increasing SIP”, where one starts the SIP with a lower amount and then gradually increases them year on year. This looks more realistic as one’s income also increase overtime and ability to invest increases. We see this situation a lot while working with our clients under financial coaching program.

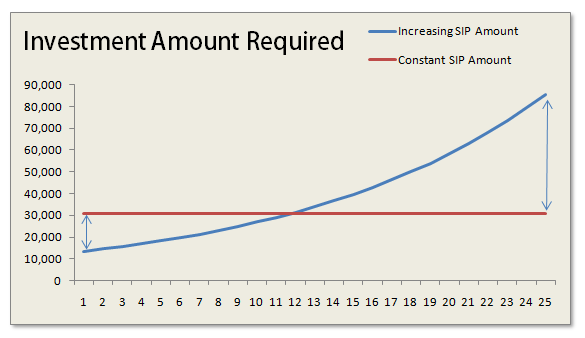

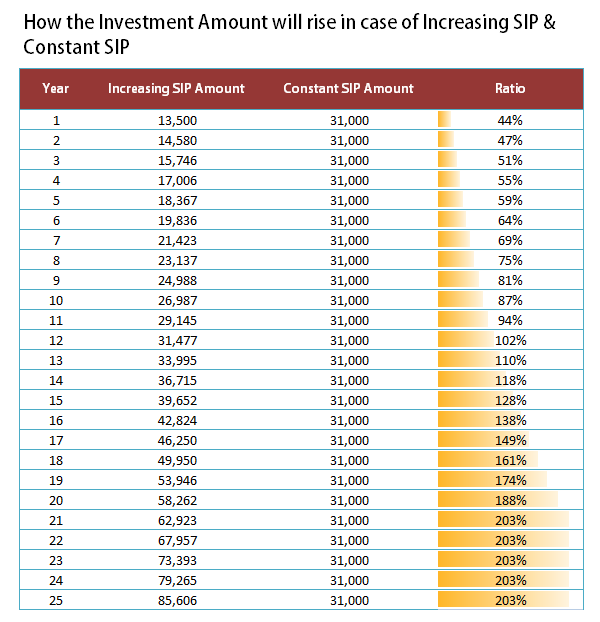

Let me show you the example : Ajay wanted to accumulate 5,00,00,000 (5 crores) for his retirement which is 25 yrs away. When he calculates the SIP amount, it’s coming around Rs 31,000 (assuming 12% returns from equity). Now it’s not possible for Ajay to invest Rs 31,000 every month, as it’s a very high amount. Rather he is fine if he can start with a small amount today and then increase it every year as his income would also increase with time. This is called as Increasing SIP model. If Ajay is ready to increase his SIPs by 10% every year, then he has to start with just Rs. 13,500. This amount is much more convenient for Ajay to arrange, rather than Rs 31,000 per month.

Should you increase SIP amount or not ?

At the first look, a general conclusion which comes into mind is that Increasing SIP is better than Constant SIP because it is much convenient and looks logical that investment should rise as the income increases. But there are different angles through which both the options can be looked at. Let’s look at two important points one by one.

1. Investment required in case of Increasing and Constant SIP

One of the most important factor one can judge both the situation is the amount of investment needed. If we take the above example we just discussed, one would need to start SIP of 31,000 per month to accumulate 5,00,00,000 in 25 yrs assuming 12% return. Now this amount will be constant throughout the all 25 yrs. Where as one can choose to start his SIP with Rs 13,500 and then increase it by 8% per year, but in this increasing SIP model, his SIP amount would reach 50,000 in 18th year and 85,000 in 25th year, which might look very big in numbers, but years from now, it would be worth a small amount considering the purchasing power of money and the annual income one earns. So don’t get surprised by numbers.

One should opt for increasing SIP, when his situation really does not allow him to invest a big amount and he is very sure that he would be able to increase his investments in tune with his salary increase. Truly speaking I am in favour of Constant SIP if one’s situation permits because that way you are investing more in the start of your life and that would help you keep your SIP in check later on in life. Imagine after many years in life, you have to just invest the same amount where as your Income has risen 3X. Isn’t it a big relief and freedom to do whatever you want from your money at that time. Imagine your salary is Rs 50,000 per month and you do SIP of 10,000 and even after 10 yrs, when your salary has risen to say 1.5 lacs per month and you are still doing SIP of Rs 10,000 only. I would choose to pay a little more today and then get into that kind of situation.

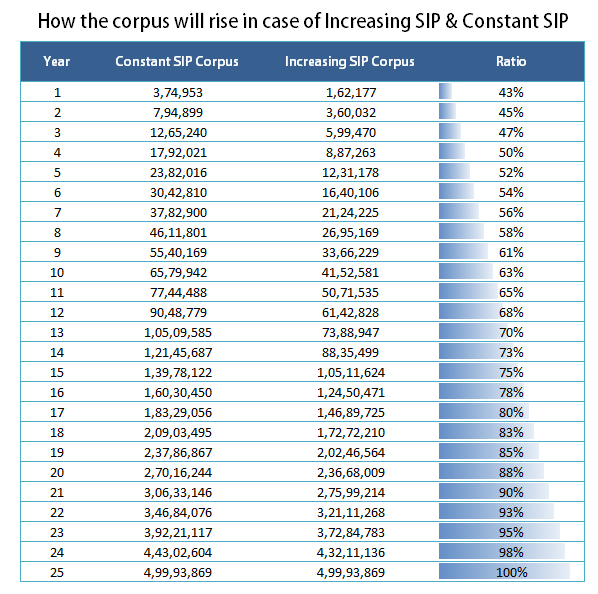

Most of the people who are not able to go for constant SIP, because of high SIP amount is because they are very late in investments and now their goals are near and they have less time for compounding. These people have high expenses already in life. Had they started long back when they started earning they could be in a better situation now. Below is the table which shows the Increasing and Constant SIP amounts required for the example discussed above and shows you the ratio of increasing and constant sip. You can see how it started with 44%, but rose to 203% later after 25 yrs.

Conclusion

One should start his SIP’s early so that he can keep his SIP’s constant through-out the tenure. If you are late, then your SIP amount will be very high and will look unrealistic and then you will have to increase your Systematic Investment plan (SIP) amount in future if you want to reach the goals.

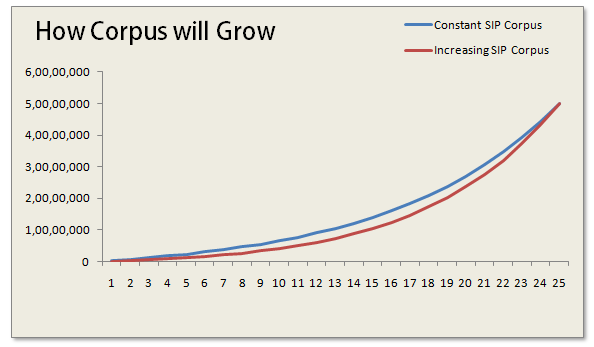

2. How the corpus will grow in case of Increasing and Constant SIP

The other major thing to look is how your over all corpus would grow in both the cases. Note that in constant SIP and increasing SIP, the final corpus is getting accumulated and they reach the same point at end, but in case of Constant SIP, the overall Corpus is always higher than the increasing SIP and it’s because you are investing higher amount in the start and that way the compounding factor is in your favour. See the chart below which shows, how the gap between the two narrows down at the end of the tenure and both the cases lead to same corpus.

If you look at the table below, you will see that the maximum difference between the two is 36,00,000 in 17-18th year and after that the difference starts coming down (not so clear in table , you need to calculate it) . As you are starting with lower amounts in increasing SIP, the overall corpus is obviously going to be less, but it’s very much above 50% all the time, so if you are saving for long-term, you should be interested in the final corpus.

Note that the example and charts above are assuming a 25 yr old tenure and equity returns of 12%. The numbers would change depending on tenure and the equity return, but the overall conclusions discussed above remains same. For a shorter tenure like 4-5 yrs, the constant SIP and increasing SIP won’t differ a lot; it would be a small number.

So the conclusion is that one should keep on increasing their mutual funds SIP amount as and when they can , preferably every year. So are you ready to increase sip amount ?

There are so many LIC policies with different names ? For example – LIC Jeevan Saral , Jeevan Anand , Jeevan Tarang and many more LIC policies. So almost every person in India holds some LIC policies, but majority of them do not know how these LIC policies works ?

How LIC Policies Work ?

Most of the investors just take things for granted and keep dragging the policies assuming it would be the best thing in their financial life. In this article I will show you how Life Insurance Corporation (LIC) policies work and talk about few aspects like LIC bonus, LIC premiums and different other aspects which will help you in understanding how these policies work.

Moneyback Plans or Non-Moneyback Plans

A lot of LIC policies pay you on a periodic basis like at the end of 4th, 8th and 12th year, and then finally at the end of the maturity period. These policies are Money back policies, the example can be LIC Jeevan Surabhi or LIC Komal Jeevan. A lot people get attracted to these moneyback plans because they get money “many” times in between and it looks attractive to them, but the premiums are generally higher for these policies.

Then there are LIC policies which do not pay you back periodically but only pays you at the end of the maturity period. They are generally termed as normal Endowment plans. Some examples are Jeevan Anand and Jeevan Tarang

LIC Bonus & Additions to your Policy

The biggest confusion I see is generally in Bonus by LIC. One thing which investors in these policies don’t know and don’t care for to find out is that there are different kinds of bonuses in LIC policies and they are calculated differently. Let’s see them one by one.

1. Simple Reversionary Bonuses

Generally when we say “Bonus”, it is this “Simple Reversionary Bonus”, which is declared per thousand of the Sum Assured on annual basis at the end of each financial year. This bonus is declared today, but is paid at the end of maturity period only or on death, whichever is earlier. So for example if you hold a policy of Rs 10,00,000 Sum assured and the bonus for this year is Rs 60 per thousand sum assured, then your bonus amount is Rs 60,000 for this year, but you will only get it at maturity (after many many years) or on death, but by then it’s worth would be much lesser than today (this 60,000 today and 60,000 after 20 yrs).

A very important point to note here is that, if you surrender the policy, you don’t get the actual accrued bonus because it’s the future value, you will only get its reduced amount in today’s term and its very less. Also note that you are eligible to get reduced Accrued Bonus only if your policy has completed 5 premium paying terms. (This thread on our forum discusses Jeevan Anand in good detail)

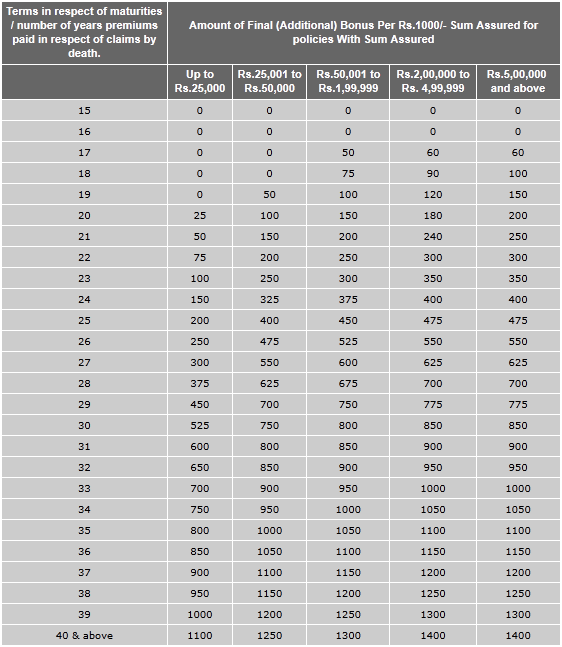

2) Final Additional Bonus (FAB)

There is another kind of bonus in LIC which is generally called as “FAB” or Final Additional Bonus and it’s paid to those policies which are of a longer duration and has run for more than 15 yrs (The premiums are paid for all 15 yrs). This is generally a token of appreciation for being with the policy for long duration. The FAB is generally not paid for policies which have “Guaranteed Additions” (explained below). Here is an indicative list of FAB.

3. Loyalty Additions

This is again a bonus which is declared for being loyal to the LIC and completing a longer tenure. Generally it’s declared at the end of the policy, but for some policies it might be applicable after completion of 5 or 10 yrs. For example – In Jeevan Saral, the policy holders will earn such additions after a minimum of ten policy years have been completed. This is usually an amount declared per thousand of sum assured depending on the corporation’s performance. Loyalty additions are totally non-guaranteed.

4. Guaranteed Additions

For a lot of LIC policies there is a term mentioned like “Guaranteed Additions”. These are assured sums which are given to policyholders for a specific period at start or end of some event along with the sum assured at the end of the term. Like for example, , Jeevan Shree-1 policy provides for the Guaranteed Additions at the rate of Rs. 50/- per thousand Sum Assured for each completed year for first five years of the policy. The Guaranteed Additions are payable along with the Basic Sum Assured at the time of claim.

Surrender Value

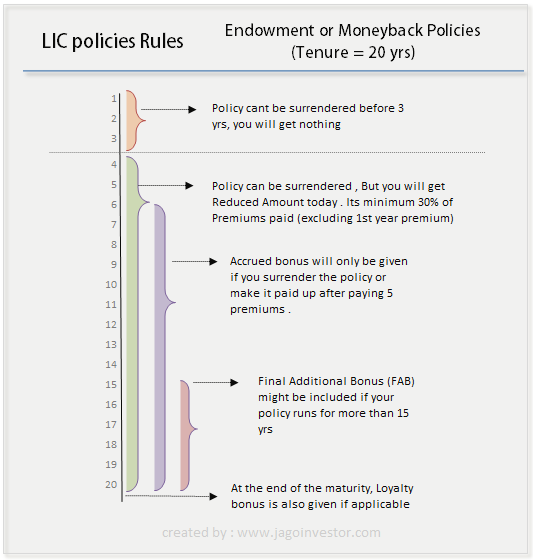

Most of the people who buy any Traditional Policies from LIC or any pvt companies’ don’t think a bit about terms and conditions on exiting the policy much before maturity. A general assumption is that they will at least get their paid premiums back with sum interest. I have seen so many cases like that where people are literally shocked to hear that they will get peanuts or nothing from their policy if they choose not to continue the policy. Surrendering of the policy works this way –

You will not get anything back if you stop your policy without paying for 3 years. Almost every traditional policy attains minimum surrender value after the policy has run for 3 yrs.

After 3 yrs, if you surrender your LIC policy, still you will only get a small fraction of your total paid premiums that too excluding first year premiums. So suppose you have a policy which has Sum assured of 10,00,000 for 20 yrs term with Rs 50,000 premium per year. If you have decided to surrender your policy after paying 5 premiums (you paid 2,50,000 in 5 yrs i.e. Rs 50,000 each year), then you will get around 30%-40% of 4 premiums paid (first year premiums are excluded), hence the total would work out to be only Rs 60,000 – Rs 80,000 only + proportionately reduced amount of accrued bonus if any (only because you completed 5 yrs, else you will not get this also).

A very important point to Note : A lot of people do not like to close their LIC policies after paying for 1-2 premiums because they will not get anything back for the 1-2 premiums already paid. They think that they will surrender the policy after completing 3 yrs, so that they will get at least something back. This is total emotional decision and not mathematical, because if you do maths you will see that surrendering the policy after 3 yrs is the worst decision if you have already realised that you should not continue with the policy. For example, if you are paying Rs 10,000 premium per year and completed 2 yrs, you paid Rs 20,000, If you close this policy now, you will lose all money (Rs 20,000), but you can save Rs 10,000 as third premium. If you choose to complete 3 yrs and then surrender, then you have paid Rs 30,000 and you will get back 30% of 2 premiums (first year premium not included), so you get back Rs 7,000 (loss of 23,000 as you paid 30,000 and got back 7,000). Do the math if you completed 1 yr only yourself, its more worst!

Note that surrender value is nothing but your future maturity value reduced to today’s value, so if the maturity value is Rs 10,000 after 20 yrs and if you want it before LIC will pay you the Net present value as per today’s term.

Paid up Policy

A lot of times when you have completed 3 yrs of policy, you might not want to get your money back immediately, in which case you can made your policy paid up (just stop paying premium and it becomes Paid up). When you do this, you can stop paying further premiums but you will get your total premiums paid + accrued bonus any at the end of the maturity period. This might work out better sometimes compared to surrendering if you were going to invest the proceeds in some debt instrument.

What are mortality charges

A lot of agents advertise these policies under the head “Free Insurance Cover“, But all the policies charge premium or charges for providing Insurance cover and it’s called “Mortality Charges”, these are the same charges which are there in Term plans and ULIP’s, but may be in a different way, so nothing is free, some part of premium goes in covering you and rest of it is invested in Debt instruments which can give you assured returns at the end of the maturity.

Loan on LIC Policy

You can also get loans at the time of crisis on your LIC policies, but the maximum loan amount available under the policy is 90% of the Surrender Value of the policy (85% in case of paid up policies) including cash value of bonus. The rate of interest charged on loans is at 9% to be paid half-yearly. Is there any other terms and conditions which you dont understand in your LIC policies ? We can all help you understand it in comments section .

Are you looking for surrendering your LIC Policies ?

By now you must have got a good understanding of your LIC policies and how they work. You can find out the return of your policies using the IRR method taught in this article. If you feel that you want to continue your Policies then well and good. But if you feel that you want to close your policies, do it soon because delaying the decision will cost you a lot in long run. I hope its clear to you how your LIC policy works for you .

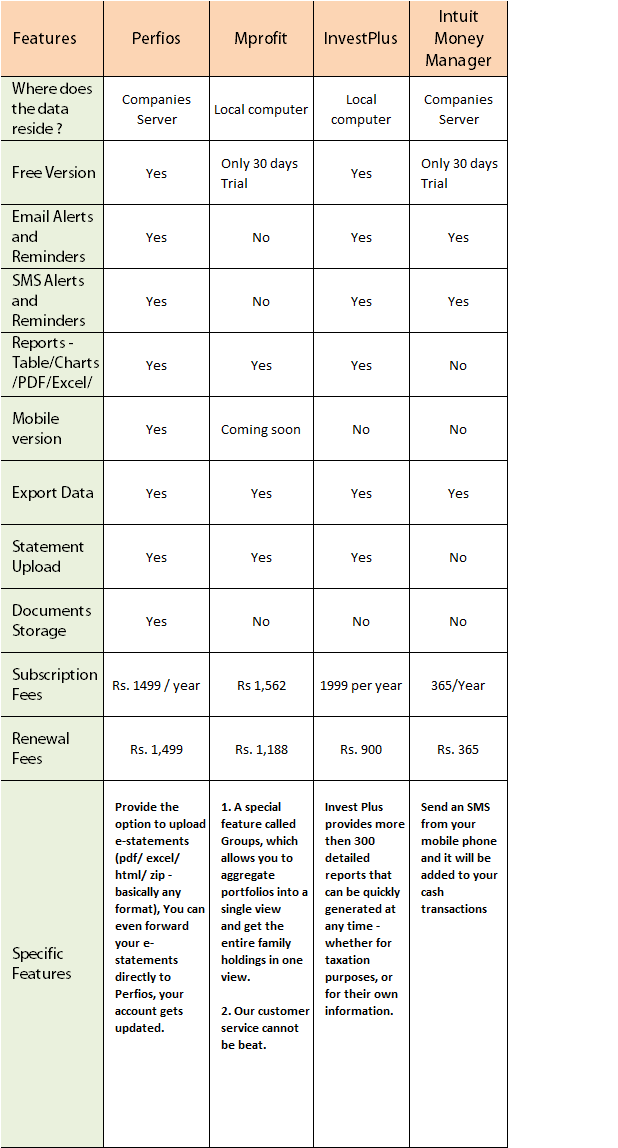

Which Portfolio Management Softwares do you use ? Some of the Portfolio Management Softwares in India are MProfit, Perfios, Intuit and Investplus and we will see a detailed review of these portfolio trackers in detail. Portfolio Management & monitoring is an important part of managing a good financial life and if your financial life has different components like Real Estate, Loans, Life Insurance Policies, Mutual funds, stocks and ULIP’s. You can also track your portfolio using Excel and there are lot of templates also, but it can be a tedious task to monitor which part of your financial life is doing well and how much worth do you have at each level using an excel template for Portfolio management. Hence, you can use portfolio management software which suits your needs. There are tons of Free portfolio management softwares which you can start with

There are many paid as well as free portfolio trackers available in the market which you can use to track and manage your financial data. I really recommend using one of these so that you have all the data at one place and you don’t need to struggle every time to find out your own information. Once we put all the information at one place, we get a clearer and a complete picture, which we don’t get otherwise… We are amazed to see our clients find out that they are worth so much or worth so less once we start discussing with them their financial life data.

Some important features of Portfolio management softwares

Now we will discuss some of the most important aspects of portfolio management softwares in India . These points are top level concerns of customers.

Data Security of Portfolio Management Softwares

A very big concern which most of the people have is where will their financial data be (example) ? Will it be on their local computer or will it is at third-party server and this becomes a big blocking point for them to go for those products which stores their data at their end itself. Here I am not talking about the login & password, but the actual numbers of their financial details. A lot of people don’t want their info to reside on other servers. I personally don’t buy that argument, but that’s a big concern for a lot of people. In a survey done by JagoInvestor last month, the number one concern which people had was data security, ahead of pricing and features.

Regarding the security of login credentials, with the advancement in technology and strong security advancements, it has become virtually 99.999% secure if not 100%. A lot of solutions also give an option for users to link their bank accounts, credit card and other online accounts by providing the passwords. A lot of people do not know how it works internally…

An online money manager will work well only if you provide online access to banking accounts for a one-time setup. This raises security concerns, but here is how it works. The login username and password for individual online banking accounts is used to retrieve read-only data. The ‘transaction password’ for online banking should be different from the ‘login password’ for greater security. You don’t have to reveal your ‘transaction password’. Customers do not have to give any personally identifiable information, making the process safer. Moreover, the account is completely anonymous and requires only a username and password. All the banking accounts are linked to provide consolidated data. In the consolidation process, vendors will have access to your financial records on a read-only basis, but privacy policies of these entities should prevent abuse of information. – source : moneylife

Features provided

I was surprised to see that in our survey, most of the people voted for high features and less on simple features. I personally thought that most of the people will love to have something which provides them less, but rich data. But actually people look for lot of features giving them number of reports and graphs. It’s very important for someone using the software getting more analysis and suggestions on what one should do in their financial life rather than just getting some plain info which they would have done on their own. Most of the software providers give good analysis along with different type of reports and charts which you can download in excel formats.

Easy to use

It’s extremely important that the softwares are easy to use because no one would put a lot of time to feed the data at the start and on ongoing basis. A lot of players provide statement upload facility where you can just upload your Bank Statement, Credit card statement or other demat statements and the software will put out the information and feed it automatically, thus reducing your work. Some softwares like Perfios allow you to link your accounts with them so that they can pull your information and feed it themselves (read only).

Below is a comparison of 4 major Portfolio management software’s in India market and used by thousands of people (you can read their reviews on their website). They are Perfios, mProfit, Investplus and Intuit MoneyManager

Look at the above video done by me and Manish Jain from Mprofit .

Free and Trial versions

I would say you should take advantage of Free and Trial versions of softwares, Like Mprofit gives away a full functional 30 days trial, where as Perfios and Investplus have free versions which are good enough. If you don’t want to use any software, you can manage your finances at very basic level in an excel sheet, but you will have keep updating the values etc from time to time as the situation changes, which is not the case with softwares, as they auto-update the values.

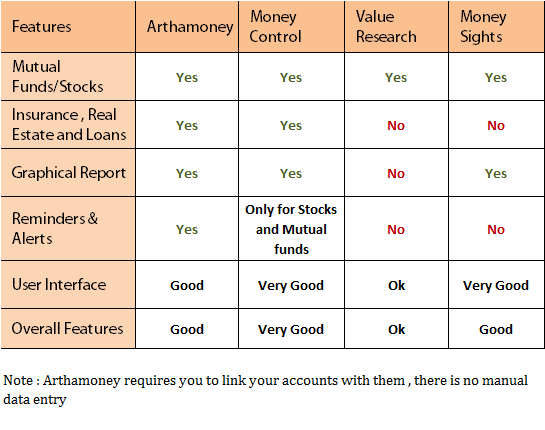

Free tools for Portfolio management

A lot of people don’t go for advanced tools and use free tools available in market which does a good enough job. Tools like money-control tracker and Valueresearchonline tracker are used by lacs of people to track their mutual funds and stock holdings. But they do not give you all the functionalities which fully fledged software’s give to you. Below is the chart explaining Arthamoney, Moneycontrol , Valueresearch and Moneysights portfolio trackers. I hope liked this review of Portfolio management softwares !

I would say you should definitely try out some softwares which provide a free version and also explore the free options, there is lot they provide free of cost and all you need is to put your data there. Some other tools which you can use are rediff money (only for stocks and mutual funds, but I like the UI), myirisplus, yodlee and rupeex.com. Please share what more do you look from these softwares and what do you think about the value you get out of these management softwares?

6 Free Portfolio Management Software Licence from Perfios

Update 12 Aug : The 6 winners are selected and this giveaway is not valid now

Perfios is willing to give away 6 free Platinum licences to Jagoinvestor readers for the first year (worth 1499). The first 10 commentators who share this article on their Facebook profile will get those licences (just cc manish at jagoinvestor dot com) (to share it on Facebook, just “like” this article below and put your comment in the box which opens).

Health Insurance sector is such a new thing in India that a lot of people have dozens of health insurance myths regarding various things and because of that they feel that this whole thing is so complicated. Today I will burst some of your long-term medical insurance myths which will help you choose right products and also build right expectations from health insurance policies.

24 hours Hospitalization is necessary for making a Health Insurance Claim.

This clause always reminds me of an incident. A little over a year ago, we were having our weekly meetings, when a doctor friend who owns a hospital in Mumbai frantically called us. A woman was making a ruckus in this friend’s hospital, insisting doctors continue hospitalization of her son and discharge only after 24 hours, as her “advisor” had informed her that they would get the claim only if the hospitalization is over 24 hours. This incident brought to light the magnitude and the level of fallacies customers have about Health Insurance. Advisors, Representatives, Telemarketers, and even hospitals and customers have frazzled their throats out on the 24 hours clause, while explaining or even using the product.

Though, the policy does mention this as one of the clauses, the 24 number in real world of claims holds lesser importance. The clause, in spirit, requires the hospitalization to be “necessary” more than it to exceed “24 hours”. This was purely from the general understanding that most hospitalizations less than 24 hours are treated under “Out-patient” (treatment at the Doctor’s Dispensary) not covered under a Standard Mediclaim. Hospitalizations (like Cataract), though required 2-3 days earlier, which are now possible due to advancement in medical science in less than 24 hours are covered, while, hospitalization by an insured for more than 24 hours for getting his routine diagnostic tests done, while no active treatments are being carried out, would not be payable under Mediclaim.

Conclusion

The thumb rule of a whether a claim is payable is not 24 hrs hospitalization but whether the hospitalization was medically “necessary” or not?

You must compare Pre-existing waiting period, always.

This is a clause that most people looking for a Mediclaim are confused about (17 Most asked questions in Health Insurance). I speak to many customers whose requirement with mediclaim is that they do not want a waiting period for pre-existing ailments. This, in spite of their entire family being completely fit, without any ailment, whatsoever. Somehow, the clause again being so popular has brought in its own confusions for customers. In reality, the 4 year Pre-existing exclusion on ailments is applicable to ailments existing at the time of applying for the policy, and not any other ailments. If you do not have any ailments or conditions, you have no pre-existing waiting period.

Conclusion

When applying for a Mediclaim, if you are completely healthy, the Pre-existing exclusion clause is not applicable to you

Cashless is an on-call Emergency Service.

Ever since it was introduced as a value addition to Mediclaim, Cashless has remained a buzz word. To a level, that for a lot of people, Cashless became a prefix, or, even synonymous to Mediclaim. The reason for the cashless concept getting popular was obvious; it was a great value add, which helped customers tide away the burden of large payments on their bank account, documentation and of course, the stress of waiting for the claim cheque. Yes, Cashless can do all this, but expecting it to work when there are emergency funds required for Hospitalization is asking for too much.

You should understand the Cashless mechanism as a concept to know why it cannot be depended on at the time of emergencies. Cashless is an arrangement between the Health Insurance Company/TPA and the Hospital where, the Hospital agrees, under contract, to grant credit facility to the Insurance Company/TPA against authorized claims. Such an arrangement is only for authorized Claims, and not for all claims. TPAs/Insurance Companies, hence, need to assess every claim received, against the policy terms and conditions, to authorize payment. Such an authorization could require additional information as well as documents and hence can take anywhere for 4 hours to 2 days of time. In their role, the TPA or the Claims Team at the Insurance Company would have to do its job of evaluation of the claim, irrespective of how urgent the medical admission or treatment is. Cashless will help you save the burden of processing a reimbursement claim, but it cannot provide you the convenience of on-call emergency funds.

Moreover, one should also note, unlike the hospital cashier, Insurance Desks in hospitals (which coordinate for cashless claims) have fixed work-hours from 10.00 AM to 7.00 PM. Cashless process and approvals after 07.00 PM are processed by the Hospital the next day. Hence, though the TPA provides 24/7 service, the cashless process may not move, once the Hospital stops working on it.

Conclusion

Expecting Cashless to work as an on-call Emergency Service is foolish. You should plan your emergency medical fund, as well as ensure you have good unutilized credit card limits, always.

You must compare no. of Day Care Procedures covered

Most Insurance Companies (specially the Private ones) flaunt a large list of more than 100 Day Care Procedures being covered under their policy. In fact, it is a highlight of their product pitch. The truth is comparison of such numbers can be very misleading. One company could list every procedure, while another could list macro-level treatments, including the listed procedures of the former. For instance, a person who compares Apollo Munich’s Easy Health Insurance which covers 140 Day Care procedures, with an Oriental Happy Family Floater which covers only 26 procedures would feel that Apollo has wider cover on Day Care Procedures. Believe me, but it could actually be the reverse. How? Oriental promises to cover Eye Surgery (a broader definition) in its daycare list, compared to say an Apollo which lists 15 specific eye treatments, which results in a larger number. Now, if the treatment being carried out is an eye surgery, which is day care but not a part of the 15 specific treatments, Apollo or many other Private players may not pay, whereas, in the case of Oriental it would get paid in the broad definition of eye surgery. By providing a specific list of surgeries instead of a macro area of treatment, the coverage under Apollo may actually be more restrictive in the long run than Oriental’s wide area of treatment wise list.

Conclusion

A short list of procedures could be wider than a long one. Do not compare the no. of Day Care Procedures.

You should check the list of Network Hospitals.

Many customers, we have interacted with demand Hospital network lists. They select the mediclaim product depending on whether their preferred hospitals are part of that Insurance Company’s list. What they fail to realize is that a Hospital Network is ever-changing. Insurance Companies regularly blacklist defaulting Hospitals. Hospitals blacklist or refuse cashless of certain Insurance Companies/TPAs for delayed payments. What is clear from this is that there is no fixed or contracted list of hospitals between your Insurance Company and you – which means there is no assurance that the hospital name in the list, which you are depending when you buy the policy, would exist in the network when you have a claim, say 4 years down time.

Conclusion

Network List of Hospitals are not fixed or contracted through policy terms. Do not depend on the network hospital list to decide a suitable product for your family. The list could change even tomorrow, in fact it could change any moment.

Capping on Room Rent is bad:

Public Sector (PSU) Mediclaim products and their current terms and conditions are evolved from experiencing and analysing millions of claims spread over more than 20-25 years. Hospital Rooms are classified into various categories like General, Shared, Private and Deluxe Rooms. Earlier without the room rent limits, for the same treatment, a person with a sum insured of 1 Lakh paying a measly premium of say Rs. 2000, would have access to the same category of room, as a person who pays 5 times the premium, and takes a Rs. 5 Lakhs cover for himself. The 1% and 2% Room Rent Limits in Mediclaim brought a clear sync between the kind of premium one pays and the eligibility of room. With such cappings, an individual who pays a high premium gets a better room, than one who pays a smaller premium, for the same treatment, which is fair. It’s like any other product with categories, like Indian Railways, providing you better facilities/services, as you move from 2nd Class to 3rd AC to 2nd AC and so on. In my opinion, sooner or later, Insurance Companies would either have to hike premium for lower sum insured or bring in a capping of some kind. For instance, the newest health insurance company – Max Bupa, has a restriction on the type of room according to the sum insured selected, instead of a “no capping on room rent” feature.

Conclusion

Cappings are good for Health Insurance as a community fund. Cappings could actually be helpful to customers in the long run.

Health Insurance Plans sold by Life Insurers are the same

The highly advertised Health Plans from LIC are Defined Benefit Health Insurance Plans, sold as “hassle free” alternatives with guaranteed payments. These plans should not be considered as a substitute to Standard Health Insurance plans sold by General Insurance Companies. These plans provide fixed benefits against no. of days of hospitalization and/or surgeries. These plans do not take care of healthcare inflation. For instance, with 18-25% healthcare inflation, a fixed benefit for Angioplasty at say, Rs. 1,50,000/- would miserably fall short in 10 years. Defined Benefit products are actually supplementary plans which provide a cover over allied costs of hospitalization including loss of earnings, if any, but such products surely cannot be a substitute to the good ol’ traditional mediclaim. Read more about the difference here.

Conclusion

Beware of what you buy. A Traditional Mediclaim should be the first product you buy to cover the financial risk of healthcare expenses of the future. Defined Benefit Products are supplementary and not substitute to Traditional Health Insurance.

Health Insurance is a Tax Saving Tool:

A large Healthcare expenditure can severely affect your financial planning for the future. The goal when you buy Health Insurance should be to financially insure your family against such large scale healthcare expenditure. Buying a health insurance product blindly, for the 80D tax benefits, is a wide-spread fallacy, which has left a large no. of people underinsured or insured with products which are not suitable. The worst part is most of them are unaware of this.

Conclusion

Health Insurance at its core is not a Tax Saving Instrument. It could save you much more than your tax, if you invest wisely.

There will be no changes in the terms of the Mediclaim I bought:

Expect changes in your product, terms. Don’t be surprised. The Health Insurance companies and other stakeholders in India are going through a mindset change. Losses in Health Insurance are no longer acceptable by key stakeholders at Insurance Companies. A lot of streamlining and normalizing in premium, terms, benefits and procedures, which have already begun, is expected in the next 5 years. Group products would turn expensive, and restrictive. Parents would be out of most Sponsored Employee Mediclaim Covers. Large and small tweaks are expected in Retail/Individual products and processes, especially from new and private players who are till experimenting and understanding how to make a long term sustainable (read profitable) product for the Indian market.

For instance, last year, PSU Insurance companies tightened the procedure of intimation and submission of reimbursement claims. Customers who were not aware of such a change faced harsh action of denial of claims, and lost good money.

Conclusion

Ensure you are updated with changes in the terms and procedures of your Mediclaim Product. Ensure you have recruited a good advisor who keeps you posted on such changes.

I can destroy Mediclaim Policies once they have expired.

Don’t know how many of you have observed at the time of renewals, but PSU companies and their divisions are infamous in the industry for changing their TPAs year over year. With TPAs being the custodian of claims, change in TPAs could result in scattered claims information amongst various TPAs across years of continuous renewals. Hence, when there is a claim, the TPA in all probability won’t have information regarding how long you are continuously covered, an essential data point to approve claims, especially, and those treatments which had a waiting period at entry into the policy. TPAs for evaluation of continuity may demand policy copies of past 3 to 4 years. Hence, destroying policy copies records have cost many customers lot of stress in proving continuity of cover. Yes, we know that it is ridiculous for the Insurance Company or its representative to ask for their own record from the customers, but then this is how it is. A good health insurance advisor knowingly would keep a repository of all policy copies, to ensure such queries do not create roadblocks in a smooth claim settlement.

Conclusion

In addition to the current one, keep copies of at least 3 previous year policy copies. Ensure your advisor also records them.

My Friend, My Health Insurance Advisor

No offence to agents, but in our interaction with Customers, we have noticed time and again, that most customers, who were found with a wrong health insurance product, bought these either from a friend, a friend’s relative, or a relative, or a relative’s friend. Most of these customers did not spend enough time in selecting an advisor, and relied on pure reference. Most of these agents selected were Life Insurance agents, who did not have a detailed understanding of mediclaim products, neither were they providing any real expert assistance (beyond picking of forms, and providing the TPA’s no.) at the time of claims. The advisor selected should have the capability and the intention to provide unbiased advice, the advisor should forever own the product they sold you, and provide services across the Health Insurance service cycle, including Purchase Assistance, Records management, Claims Assistance and Renewals. A good advisor would be able to hand hold you through the dynamic transformation that the Health Insurance industry in India, is witnessing and will continue to witness for the next 2-3 years.

Conclusion on Health Insurance Myths

Select an advisor on merits and the services he demonstrated, and just not merely on reference.

What was the biggest and most valuable learning for you out of this article ? How many of your health insurance myths were really broken ? Please share it on comments section .

Is your under-construction flatin Noida Extention in danger? No! But there are thousands of buyers who have invested their hard earned money in flats that are being constructed at Noida Extension. In this article I will talk on the issue of Noida Extension and what learnings can we take from this whole issue. For people who are not aware on the recent Supreme Court decision to stop construction in a part of Noida Extension and give it back to farmers from whom it was taken by the Noida Authority in the name of “Land Acquisition”. Now thousands of buyers who booked their flats are in danger of not getting their homes which they had booked.

Background

So the whole issue goes back to 2005-06 when Noida Authority snatched land from farmers saying that the land will be used for “Development” purposes, Industries will be put in, there will be factories which will further help villagers and their future generations get employment and their life will be “great”. They were given pennies for that land. Then later this land was given to Builders for construction purpose and thousands and lacs of investors bought their dream homes in these projects.

The land was under dispute and after a lot of construction has already happened and people have put their hard earned money in lumpsum or through EMI’s. Now Supreme Court says that the land acquisition was illegal and was not done in the right way, so the land now should be given back to farmers. This is only for one part of Noida Extension issue which still affects thousands of buyers and later again there was a judgement passed in favour of farmers for another village.

Now this has given farmers the confidence that even they have a big say in this issue and someone is there to listen to them. All villagers now want a revised compensation at high rates (which I feel is totally right and it should always have been that way) or they want their land back. The builders have already spent crores of rupees in construction buyers have already paid the money for flats or have taken a home loan and paying the EMI. Now if all the land is given back to farmers what will happen to builders and thousands of buyers who bought the homes? Who will bear the loss of the mental agony and financial setback which will come as part of this package?

Recently, the judgement has been postponed till mid Aug 2011, when Allahabad High court will decide on the final judgement for the dozens of villagers land. If it says that the land has to be given back, the situation will get uglier. This whole issue is now engulfing whole of Noida and Greater Noida.

Who is to be blamed ?

Now assuming you have understood the situation, who do you think is the real culprit here? Is it the builders lobby who are known (or I would say secretly known) to manipulate the land acquisition part and then do construction there? Or is it only Noida Authority (read Mayawati Sarkar) and their policies for land acquisition? Or if you allow me to say, is it buyers who didn’t spend too much time to foresee the future of their houses if legal dispute gets uglier later? Who among all took things for granted?

I personally feel that there are two main parties who are really suffering here and those are Farmers and the home buyers. Farmers plight is from long time who are fighting for their rights from years and not even living a life of dignity even after feeding me and you and the whole country. Buyers are those who had spend their life earnings in their dream homes and now are seeing chances of delay, in their dream to own a house. More than financial loss, I see it as a big emotional breakdown. No one is there to hear and address their issues. They are skipping their work and business to give Dharna’s and by showing their outrage in masses.

What do you think is the solution in this case? Do you think incident like these are going to change the way people look at real estate buying? Can this Noida Extension issue teach people to pay more attention in what they are buying?

What do you think about this? Open your heart on comments section and let’s discuss it?