Good news for EPF account holders. Now you can check your Employee provident fund balance online using the new e-passbook service by EPFO website. EPFO has introduced a new concept called “EPF Account Passbook”, which will allow EPF Account holders to download their EPF Balance passbook at any time they want, which means you can now do EPF balance enquiry each month and see how it’s increasing.

Here are 4 simple steps to register for the Employee Provident Fund e-passbook online and after that you can do the EPF Balance enquiry anytime you want.

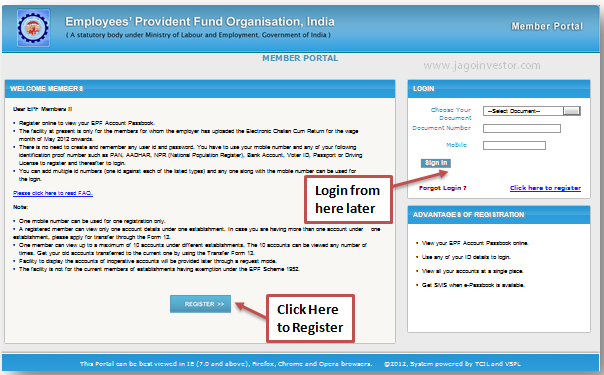

Step 1: Register yourself on the website

The first step is to go to the e-passbook members website – http://members.epfoservices.in/ and click on the registration link. Once you are taken to the next page.

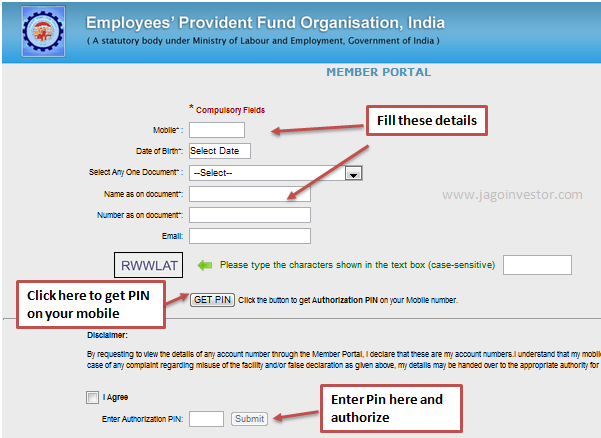

Step 2: Generate your PIN and login

You will be taken to the next page where you need to provide details like

- Mobile number

- Date of Birth (make sure it matches with EPF records)

- One of the documents mentioned in the drop-down

- Name and Number on the document (Like PAN card and the PAN Number)

Then you need to click on “Get PIN” button to generate a PIN which will arrive on your mobile and email. This PIN is required for authorization every time you want to download the e-passbook and check your Employee Provident Fund Balance. At this point in time, you will need to log in again which will take you to the main page where you can do your EPF balance enquiry and download the e-passbook.

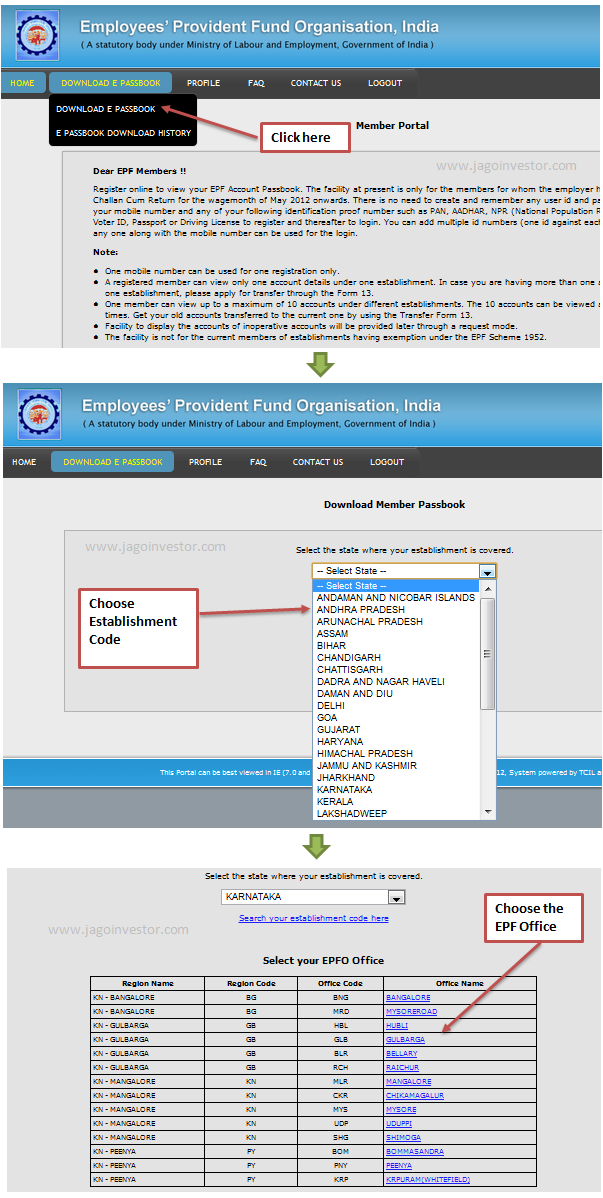

Step 3: Download the EPF Passbook which has your balance

Now on this page, you need to go to option which says “Download E-passbook” and under that click on “Download E-passbook”, It will ask for the state where your establishment is covered like Maharashtra, Karnataka, Delhi etc.. Once you click on the state, it will ask you to choose the exact EPF Office.

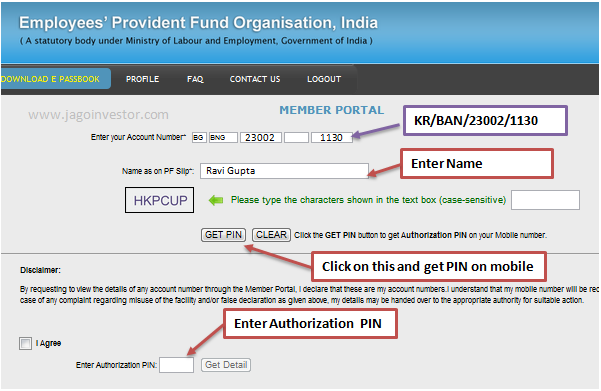

Step 4: Enter your EPF details

Now you need to enter your EPF account number and name of the account holder, and click on “GET PIN”, which will generate the PIN on the fly which will come on your phone and email. You need to now enter this PIN below and you can download the PDF which has your current Employee Provident Fund Balance and other details. Make sure you do not close this page unless you get the PIN. One of our Financial Coaching Client, Jassi tried this whole thing and his experience was good

I followed the same steps. Yes the PIN is received in your mobile after some time, so one needs to be patient. And the page should not be closed until one receives the PIN, to access further. After receiving the PIN, log in to the application. If e-passbook is available, it should be shown immediately. Otherwise, one might have to wait. – On Email from Jassi

Checking your Employee Provident Fund Balance from time to time?

Now with this method, you can keep checking your EPF account balance from time to time, you can check it each month after your salary is deducted and some days pass, or you can also check your PF balance on a quarterly or yearly basis, whatever works for you. I hope you are clear about some hidden and must-know facts about your EPF

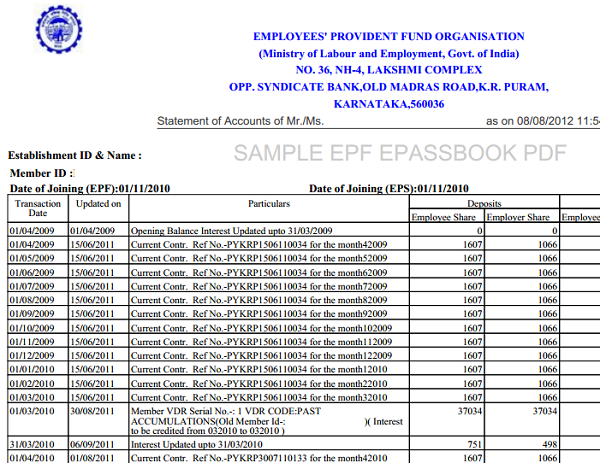

Sample EPF e-Passbook

Below is a sample EPF passbook which you can view and download. It shows how EPF e-passbook looks like and different entries made by the employer. But you will see only those entries which were uploaded and updated by your employer. It might happen that some people see their old data only.

12 Important points to know about EPF passbook

Here are some of the very important things you should know about the Employee Provident Fund e-passbook facility.

1. One Mobile number

One mobile number can be used for one registration only. However, you can change this mobile number later if you want so in case your mobile number changes, no worries.

2. One EPF account per establishment

You will be able to view only one EPF account details per establishment, means if you have two EPF accounts under Maharashtra (suppose you had a job in Mumbai and Pune), then you will not be able to view both of them, In that case you will need to first transfer one EPF to another. However, you can view your EPF account details which are under different establishments like saying one in Karnataka, Maharastra and Delhi (suppose you had 3 jobs)

3. Total of 10 EPF accounts can be viewed

A total of 10 EPF account details can be viewed under different establishments. I think its very fair logic because, in all probabilities, a person will not have more than 10 EPF accounts in several establishments, if he has, no one can help him anyway 😉

4. Inoperative & Settled EPF account details not available

If someone’s EPF account is inoperative (it happens if you leave the job and for 3 yrs there is no activity in your EPF account, even the interest will not be credited to that account), or the account is settled (you withdrew the amount already) , then your details will not be available. Tip – You can file an RTI application for your EPF queries and get them answered.

5. Details on request if you left the job before Mar 2012

If you have left your job before Mar 2012, then your EPF account may not be seeing any credit in past few months, in that case he will not be able to see the Employee provident fund details immediately, but it can be requested on the website (you will see a link) and that will be uploaded in few days.

6. Available only if the employer has uploaded Electronic Challan Cum Return of May 2012 onwards

This facility is available only to those whose employers have uploaded the Electronic Challan cum return for May 2012 onwards, Electronic Challan is a way of submitting the employee’s contribution to EPFO online, which is recently introduced by EPF organisation.

7. No need to remember user id and password

There is no user id and password, all you need is your mobile number, document name and document number, which we all remember anyways. At the time of downloading your EPF Balance passbook, you will need to generate the PIN online which will be sent to your phone, this will reduce the chances of fraud

8. Private EPF trusts not eligible

Those employees who have their EPF with private PF trusts (or called as establishments exempted under the EPF Scheme) will not enjoy the benefit of this e-passbook facility, hence they will not be able to check their employee provident fund balance online using this.

9. Use multiple id’s to register

You can add several documents like Driving license, passport, ration card etc in the same account, this way you dont need to remember just one document id and its number, you can log in using any of those which you are carrying at that time.

10. Details and Entries in the EPF passbook

Month and date wise transactions made in member’s account will be displayed in the passbook from the year for which the annual accounts were updated for the establishment for the first time since computerisation of the concerned field office. For example, if the first annual accounts of member’s establishment were updated for the year 2008-09 by the concerned field office after its computerisation, the passbook will display the opening balance for the year 2008-09 and all transactions thereafter.

11. Error while Downloading the passbook

While downloading your EPF passbook, you might see an error saying “YOU HAVE ENTERED INVALID MEMBERS ID OR NAME”.

Please check whether you have entered the correct code & account number and/or name. In case yes, the name may not be matching as per the record in EPFO. In such a case, the member has to contact the concerned EPFO office. At times some entries from EPF passbook might be missing, in which case, the member should check first with the employer whether the returns for the month/year related to the missing entry has been submitted by him to the concerned EPFO office. In case yes then he/she can contact the concerned EPFO office regarding the missing details.

12. Not getting the PIN on your mobile?

Ideally, you should get the PIN on your mobile as soon as you click on “Get PIN”, but if you dont get it fast, it means the lines are busy and you should wait for more time and re-try!

Tip : Use Chrome instead of other browsers, Some components are running smoothly on Chrome, but not on other browsers .

Are you going to check your EPF Passbook?

Is this working for you? Did you try to find out your Employee Provident Fund Balance using this method? Once you are able to do your PF balance enquiry using this way and check your EPF passbook online or not? kindly let us know on the comments section.