How do you want your 2012 to end? We always have to much of pending tasks in financial life. We know that the time required to complete most of the tasks is pretty small one and if we just dedicated 1 full day, most of those tasks will be completed within no time, but we keep delaying it.

Action month is back !

yearl We are conducting an Action month called “How do you want to end your 2012” for our wealth club members. We wanted to do this action month for our wealth club and then realized that why not include everyone, as its such a big event after a long time, hence we thought of sharing it with everyone. Last time we had a hugely successful action month and hundreds of readers completed so many tasks in their financial life within few days time. Go to the main Action Month page on Jagoinvestor Wealth Club. Listen to the Action Month Audio to understand what it is all about This time its your turn to complete those pending things and also do a yearly review. The theme of this action month is “How do you want to end your 2012” . We want to make sure that when 2012 ends, you complete most important pending tasks which you have been delaying from long and also have a clear view about where you stand in your financial life.

How to be part of this Action Month ?

Step 1 – Register for Action Month Action Month is CLOSED now Step 2 – Review your 2012 and complete pending things The next step is to review your 2012 and see if you are on track or not and then list down the pending items you want to complete before 2012 ends. When you register, you get a support excel sheet also. Wealth Club members already have access to yearly review checklist sheet. Step 3 – Action Month ends and share your success story Once you complete your action month, you can then share your actions and what all you did, It would be a great thing to let others know of your success and how you ended your 2012 and have planned your 2013. Go to the main Action Month page on Jagoinvestor Wealth Club.

For all the Participants

The registrations are open for only next 4 days and this action month will run for only till 31st Dec 2012. Note that all the updates about what you are doing in action month has to be done on the main Action month page on Jagoinvestor Wealth Club. Also the best sharing at the end of the Action Month will get a surprise gift from us.

Everything in life has basic ground rules, which we should never forget. You can consider these ground rules as the pillars of your decision making activity. Even our financial lives have some ground rules to follow in order to have a great and enriching life. Over the last 5 years of writing this blog and having interacted with thousands of people, I can clearly conclude that more than making right decisions in financial life, you should focus on avoiding bad decisions. I have seen so many people who have been careful, not messed up things and their financial life quality is really awesome. They have not lost wealth due to foolish mistakes and live a clean financial life overall and while they feel lag behind others, I can say they are ahead of others in many ways. Yes – They have not taken awesome decisions, but the best part is they have not made terrible mistakes either. Lets explore more on this today

6 pillers of great financial life

Now I am going to talk about 6 areas of financial life which are like pillers. If you are clear about these ground rules and start some serious work on all of them, your overall quality of financial life should go up. But having said that, its a long term activity !

1. Rule of Earning

“Do not depend on a single income. Invest and create a second/ third source of income”

So many people just never focus on this. A person in a job has just taken it as his fate, that his only source of income will be his Salary. For him alternate source of income other than his salary is like a distant dream which he can only see, but could not achieve. The same happens with a businessman at times. He depends solely on his business income. Why? Why not also have some other passive income from other non-core business area.

Atleast start thinking in that direction ? Lets Explore some extra income source. I dont say, it need to be some grand income, but lets make some start atleast, if not in action taking, atleast in thinking about it, I personally tasted some passive income from my first book royalty, while it was not a big one (opposite to what people think) , it atleast gave me some good feeling. Other than our business income, I had some source of income from other stream. Thats important ! . It can be a small income, not a grand one . Thats okay ! . Whatever is your specialization, you must be god gifted into some or the other thing in life, start sharing about it with world by writing about it, you never know when you start making fans for yourself and it might bring some opportunity to you in life. Nandish has written a nice piece of “Giving your Gifts to the world” on our Jagoinvestor Wealth Club, check it out . If you are damn good about something , why not offer consulting or accept freelance projects in your own capacity.

Forget all that, at minimum, If you are a person who comes home early, why not take some tutions to make few extra bucks. Its not about earning a little more, its about the habit of creating an extra income. You never know when, in the future when you might have to look at it seriously! . So the point is, go ahead and put a small seed in your head about “Creating Alternate income” .

2. Rule of Spending

“If you buy things that you do not need, you may soon have to sell things you need”

People are over spending. There is no doubt about this. Just look at your own expenses & write them down. Question each of your expenses, do you really need them? Is it out of necessity or just a desire which you can avoided altogether or atleast minimized? The answer will be in front of you. If you have not yet tracked where your money is going and if you are our special member at Wealth Club, you might want to download this Budget Template.

One of our Bangalore clients told us last year that he has seen a lot of his friends, who buy a car on the first day of getting the job! and mostly they dont need it. Its either to show off, or just that short term desire of own it, without thinking about long term aspects of it. Its just unplanned!. Then there are people buying 25 shirts, when they only need only 12. There are people, who don’t have the `haisiyat` of driving an Alto Car, but they have bought a Honda City just to show off !

It just violates the rule of spending!.

Slowly but surely, this will take them towards disaster. It will come as surprise (to them) one day. Spending is a core activity of your life. You earn so that you can spend it, nothing wrong with it, but there is a difference between spending and over-spending. Understand it today to make your future more robust.

3. Rule of Savings

“Do not invest what is left after spending, instead spend after you save/invest”

This is directly related to rule 2 above. If you do not control your spending, you can never be able to save much and then you will never be able to give your best for your wealth creation. Fix this clearly & prominently in your head. For most people the formula is

Saving = Income – Expenses

If you rely on the natural flow of life, you can never save. Life will give you all the reasons why you can only save amount X . At times Nandish tells me – “Manish , you know what, if you do not define the purpose for your money, money will find its own purpose” . This is very strong point , for a moment, just slow down and think about it. you will realise what it means. You need to control the flow of money and you have to create that flow yourself.

I just ask to most of the people to do this 1 min experiment. I tell them – “Imagine your employer says that from next month, you will get a salary cut of 10% and all you will get is just 90% in your income. For most of the people, will they not be able to live the same life as they lived till now ? If the answer is YES , then why are they waiting for ? Why not give that small salary cut to yourself as your gift to your financial life. You will enjoy this salary cut in coming years. trust me.

So your next task today is tell your family, yourself and your relatives that from now on you will be living on just 90% of your salary – PERIOD! . Start doing it and slowly you will see that magically – you will be able to manage things – Try it! It works! .Your assets , your net worth , and every bit of wealth comes from those tiny savings you consistently do for years. That’s the most important ingredient part of your wealth creation. If you do not focus on optimizing it, nothing else will work out!

4. Rule of taking Risk

“Never test the depth of the river with both your feet”

There is a very thin line between risk and calculated-risk. Calculated risk is the risk which is taken after due thought, and by accepting the future consequences and a thought full evaluation of how the odds are stacked.

If you invest a big sum of money in stocks, just because markets are going up and you do not want to miss the train, and just because that guy on CNBC said you should , then you are taking a risk. You will not be able to sleep at night for sure.

However if you look at the current market and tell yourself that – “Markets have not moved up from last 5 years, and this kind of situation in past have been proven to give great returns in next 5 years and you are economically ready to loose up to 30% of your money, and thats why you choose to invest in stocks, then its a calculated risk! . You have put some reasoning , thoughts and accepted the downside of that decision and hence you are taking that risk !

Taking risk is not a bad thing at all. It’s the only thing which can help you grow at exponential rate. Those who don’t take risks, just die a simple life most of the times. The best things in the life are on the other end of the Risk , its on the opposite side of it. So take risks, but always make sure they are calculated one ! . Over the long term, one an average, you will do great. Its proven already, I am just reminding you!.

5. Rule of Investing

“Do not put all your eggs in one basket”

Warren Buffet is not a very big fan of diversifying. All the money he has today, comes from stocks, but there is one simple rule he has followed – “Put all your eggs in one basket, if you know you are an expert of that basket and closely keep an eye on it”.

Most of us are not like Warren Buffet! . So lets not copy him. What if you have put most of your money in one single asset class or a property or a particular branch of a bank? or just a single stock. Things can go wrong, and when it goes wrong, you will cry out loud, but no will will be able to help. You will be helpless and will regret like anything.

As a best practice make sure that your wealth is not in a single place. Remember that portfolio diversification is mainly a tool of minimizing risk, not for maximizing returns, so don’t ask a stupid question like – “Will diversifying my money to different places increase my returns?” – The answer is “It might… or it might not!/. But properly done, it will surely minimize the risk of losing your wealth in future.” .

6. Rule of Expectation

“Control your expectations, and control your happiness – they are same thing”

One very dedicated reader of this blog – Pattu, who teaches at IIT Chennai, told me once that he does not expect equity to give him more than 8% of returns in long term and he always invests his money in equity, assuming that he will get 8% or better in long run. Anything more than that would be a bonus for him. I am sure that he must be happy all his life and will never be disappointed with equity returns.

In financial life, we expect agents to work in our favor, we expect financial products to give us amazing returns, we expect financial planners to charge less, but give an awesome experience (Like we give to our paid clients) , we expect life insurance companies to pay our family, even if we make some mistake while disclosing some important information, we expect our credit card to forget the penalty for in-case we don’t pay on time, we expect government to decrease the tax rates.

If you look, we are an “expecting” machine in our life. I can say from my tiny experience of life till date, happiness and expectations are just the two different words for the same thing. If you want to get in control of your happiness level, just control your expectations in life. Stop the expectations from others, better control yourself and your expectations, because thats all you can control. not others.

Practice these 6 rules in your financial life

If you can master these 6 rules in your financial life, your quality of life will improve. Each decision of yours should originate out of these 6 piller rules.

What do you say? Which rule did you like the most? Share it with us in comments section…

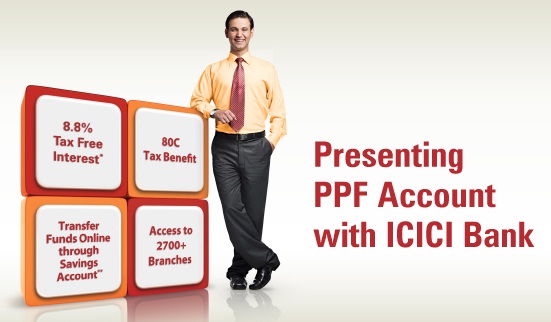

Do you want to open PPF account in ICICI Bank ? Yes It’s possible now. Few months back, ICICI started the facility of PPF account. The way it was advertised was “Online PPF” , but it mainly meant that you can deposit and maintain your account online. While you can also apply for the PPF account online, still you need to provide them the documents physically. In this article we will look at how to open Public Provident Fund account in ICICI Bank.

Can you open PPF account in any ICICI Branch ?

No , you can not open PPF account in any ICICI Branch . For each city, there are special designated branches for opening PPF account. You will have to open the PPF account there, here is the list of those designated braches . Note that you need to have a ICICI Bank account before you open the PPF account in ICICI, however the account can be in any branch of ICICI .

Documents required for opening the PPF account in ICICI Bank ?

Case 1 : For customers who have a relationship with ICICI Bank that is < 5 years.

Form A

Passport size photograph

Copy of PAN card

Case 2 : For customers who have a relationship with ICICI Bank that is > 5 years

Form A

Passport size photograph

Copy of PAN card

Residence proof – Passport/ Electricity Bill

In case 2 , the additional Residence Proof must be required mostly because if the customer is quite old, his address must have got changed. Note that if you do not have a ICICI Bank account already, you will have to first open an account , in which case you will fall into case 1

How to transfer your existing PPF account to ICICI Bank account ?

As per the PPF scheme of the Government, subscribers can transfer their PPF account from one authorised bank or Post office to another (Check detailed article on how to transfer a PPF account from Post Office to SBI bank) . In such a case, the PPF account will be considered as a continuing account. To enable customers to transfer their existing PPF accounts to ICICI Bank, the following process must be followed.

The customer approaches the bank or the Post office where his current PPF account is held and makes an application for transfer of PPF account to ICICI Bank’s branch.

Once the application is processed, the existing bank/Post office arrange to send the original documents such as a certified copy of the account, the account opening application, nomination form, specimen signature etc. to ICICI Bank branch address provided by the customer, along with a cheque/DD for the outstanding balance in the PPF account.

Once transfer in documents are received at ICICI Bank branch, customers are required to submit fresh PPF account opening form (Form A) and Nomination form (Form E/ Form F in case of change of nomination), along with their original passbook . Also customer is required to submit a fresh set of KYC documents.

You will not get PPF passbook in ICICI bank by default

This is something interesting I found which was getting discussed on our jagoinvestor forum . Looks like by default ICICI bank does not provide a PPF passbook when you open it. If you really need it, you will have to give a written request and only after its processed it will be given. Under its PPF terms and conditions its mentioned that

3.3. Passbook shall not be made available to the Customer/s for PPF Account/s which are applied for and operated through ICICI Bank Internet Banking Services. However, the Customer shall be able to view his/her transactions through his/her statement of accounts available online on the Website. In the event, i Customer wishes to have a passbook for the PPF Account applied for through ICICI Bank Internet Banking Services, he/she shall be required to put in a written request for the same at the designated base branch where PPF Account is/has been opened as per ICICI Bank’s policy / process/Primary Terms.

However, if you mostly do all the transactions online, the Passbook point is not that big thing to reject the idea of opening PPF account in ICICI bank.

Conclusion

PPF account was always opened at SBI bank or Post Office by maximum people and ICICI bank is the new player in this field. Only time will tell about their services and how they handle this PPF service. However overall for netsavvy investors who already have a ICICI bank account, seems like its a good option and which can be acted upon faster. Now you need to take your decision. Let us know if you will open a PPF account in ICICI bank or not ?

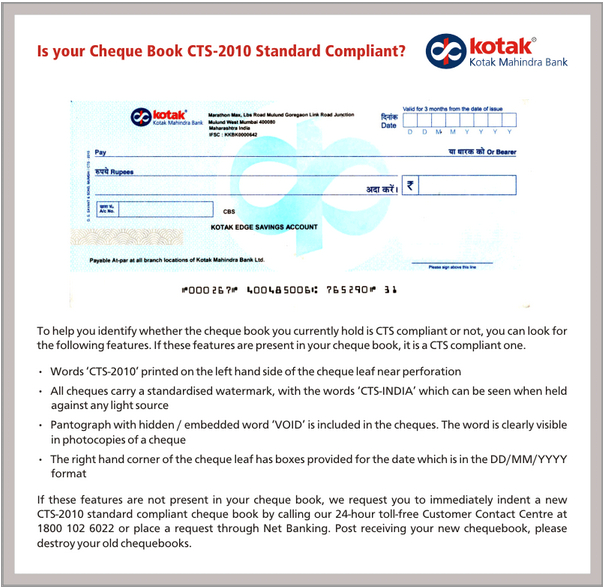

It might happen that your cheque’s start bouncing and do not get accepted from Jan 1, 2013 . There is a new standard in banking called as Cheque Truncation System or CTS 2010 , which all the banks have to follow now. RBI has issued a circular telling all banks that they should only process and accept those cheques which follow CTS guidelines.

What is Cheque Truncation System or CTS ?

Its just a new improved structure for chqeues and a set of guidelines which will change the way cheques are being processed and cleared. Right now, all the cheques are sent directly physical to the other bank for clearance, but with this new Cheque Truncation System guidelines, the banks will send the digital version of cheques (read scanned image) to the other bank and the clearance will happen almost same day or very fast. Some of the features of CTS cheques would be

It would have the wordings “please sign above this line” at right bottom

All CTS-2010 cheques will have a watermark with the words “CTS INDIA”, which can be seen against a light

A bank logo will be on cheque with a Ultra Violet Ink , which can be seen only under UV Scanners.

The Cheque Truncation System 2010 enabled cheques will not allow any alterations. If there is any mistakes, the cheque will be invalid

“payable at par at all branches of the bank in India” text will be at the bottom of all the cheques

There will be IFSC and MICR code on the cheque

You will have to sign the cheque will a darker ink, so that your signatures are valid for scanning.

If you look at these features, you can simply see that these are required for digital processing and once these Cheque Truncation System enabled cheques arrive , the whole banking system will start clearing the cheques in a must faster time. This will improve banking and save paper 🙂 . Below is a sample of cheque which fulfil CTS criteria’s.

SBI has already told all its customers to get new cheques because all the old cheques will become invalid , In the same way HDFC bank and ICICI bank have also told their customers to get new cheque books.

What you must do ?

1. Replace your Post Dated Cheques

If you have given any post dated cheques to someone like for your home loan payments or for some other kind of payment, then its the time to replace them with fresh cheques else it will just bounce and you might have to pay the bounce charges

Deposit any Old Cheque now

At times, we accumulate old cheques and deposit them for clearing only after many days or weeks. If you have any cheque which is to be cleared, better deposit it and encash !

A lot of banks have also asked its customers to give return back the old invalid cheques at their branch and collect new cheques, not sure why they need old cheques , why cant they issue the new cheques directly ? Also note that the cheques will be sent to the last updated address only. Learn more about CTS here .

You already have CTS-2010 compliant cheque books ?

Note that RBI has directed all banks to issue Cheque Truncation System 2010 enabled cheque books already from last many months. So it might happen that your cheque books are already complaint with those standards . So please check it once and dont rush to bank to issue you new cheque books . Like one of the reader found out that he already has the right cheque’s .

Banks like ICICI Bank and Axis Bank had already started issuing CTS-2010 compliant cheque books since last year. So please verify whether cheque book you have a already CTS-2010 before rushing to bank to get a new one. After I placed a request for new cheque book, I found that my existing cheque book issued to me in Mar-2012 was already a CTS-2010 one.

I hope you are clear about Cheque Truncation System (CTS) and how your cheques will become invalid from Jan 1,2013

Today we will talk about how a newcomer or a fresh investor start his investment journey. We will see 4 steps which a newcomer can follow to start his invstments. I see a lot of new people on the blog asking things like

Hey Manish

I am totally new to this world of investing, I just joined job 3 months back and it seems like I have no idea how to start. I can see my friends who have been in job already, but they have messed up so much in their financial life. I do not want to be that way and want to do best. Can you tell me where should I invest?

In today’s world of over communication and an environment where things look complex it’s no wonder, a new person is confused. While there cant be a one strategy that fits everyone, we can still propose a generic 4 step rule, which can help most of the fresh candidates and these 4 steps becomes more important these days because most of the people mess up hugely in the first 5 yrs of their financial life and they have no idea how important starting years are in financial life. So today, here’s a look at the 4 steps, I feel will be applicable for most of the people.

Step 1. Enjoy for the first year – Spend !

Almost everyone who starts a new job has this feeling for a long time – “Once I start earning, I will buy things for my parents! I will buy a bike! I will roam places! . I will buy that awesomely cool mobile which I could not afford when I was a student! . I will do this! . I will do that! I will go here! I will go there!” . Everyone goes through that feeling and when I started my first job, even I had those same kind of excitement.

You know what? This is totally acceptable and a 100% correct!

The moment we enter the world, we become the part of the rat race (remember 3 Idiots?) We get good grades, we get into best school, study hard to get into college, and then finally land at job, assuming its the end of the race. At this point, if someone tells you – “Start Investments Early!”, what would be your reaction ? I would say that as a statement, its a great thought, but to a young guy (or girl), who is yet to get comfortable with the environment, it’s a foolish statement, distant from reality and kinda crushing the emotional side for their ‘desire to spend’ .

The only thing which makes sense at this point is to let all those wishes come true! Let the guy spend!. Let him or her spend on those things which he or she ever wanted. Let them splurge! . Buy things which they dreamt about for years . Let them travel! . Buy gadgets! . Shop for clothes and phones and whatever they wish to! .

I’d say, go for it!. Let it happen for the full 1 year in the start. After a year, the person should have done most of what he or she wanted, in that time, he or she should be more settled in the first job. He/she would have got a taste of “earning money” . Now! This is the good time to talk to him about finances.

Step 2. Start a Recurring Deposit and Start learning

The next step is to get started, to get into the process… The biggest issue which I feel with newcomers is that they do not have this habit of “regular investing” . Lots of people, when they start their financial life, want amazing returns immediately! . They hear about SIP from media, they hear about stock markets and real estate markets and suddenly the only thing that plays in their mind is “high returns”.

First, they need to work on their “habit of investing.” They should first understand, what it means to save regularly, they should first get a feel of how money grows over time. A person is mostly raw in the beginning and needs some serious understanding of basic concepts and how everything works! The need of the hour is “habit” and “education”. For anyone new to investing and who has just started his career, should read my first book “Jagoinvestor” where I talk about few fundamental principles of personal finance. From most of the people who have read it, they told me that it was an eyeopenor for them. If you want to get a understanding of what it looks like download this sample 1st chapter of my book and read it . It also has tons of reviews from other people who have read it already.

So coming to the point, what can this new investor do at this step once he is ready to take the plunge ?

I can think about 3 things here.

a) First, open a Recurring Deposit in your bank for a big amount which you can save. It can be 10,000 , 20,000 or even 50,000 depends on how much are you saving! . This will make sure that a part of your salary is now getting invested in a Recurring Deposit on a regular basis for next few months atleast. You can see some money regularly invested and get a feel of how money grows over some months. The money will also be safe.

b) This is also a serious time to start exploring and learning about the other kind of investment options. You can learn from all kind of websites, blogs and books written on personal finance and more. Ask questions if you have any doubts on our Q&A platform (we already have 4,000 questions and 20,000 answers on it). This phase will act like the preparation for rest of your life. The clearer the concepts and fundamentals to you, better it is. At this point, you should concentrate on learning things. Your money is getting accumulated anyway in the recurring deposit and is safe. So nothing to worry about there.

c) Apart from the above points, you can also start the background documentation & processes which will be required in the future. You can apply for your PAN Card incase you dont have, start a demat account, get your KYC done for mutual funds investing. If some document is missing, apply for it, & open more bank accounts if you think you would need them. It’s like, you’re getting all your weapons ready for the future.

For those newcomers who like to learn through Video’s – we have a 37 min course called Basic Concepts of Personal Finance on our Jagoinvestor Welath Club.

Step 3. Complete Most Important and Primary Tasks First

Now, you are ready & educated, have a good understanding of everything, gotten a taste of investing money and are ready for the next step. Now in any financial journey, there are few steps which you should take right at the beginning. These are like the “first things first” tasks. I see people on this blog, who have not completed these important early tasks even after 5-10 years of their first job. There are few things like

These are mostly one time tasks. Once you complete them, They are complete ! . You might have to pay a regular premium for few products, but the main task of taking actions in those areas are complete, which most of the people struggle with. Understand that, if you delay these most important tasks, they will just get pushed for “future” and it will take ages to complete those when you actually need them.

Remember, these one time activities complete a major part of your financial life. After this, you mainly have to just review these each year from time to time, and mostly concentrate on your “investments part”. After you have completed these tasks, your primary objective is wealth creation. A lot of people I see are still lost in these primary, first level tasks even after years and years , just because they didnt do it in start and now when its time for concentrating on their wealth creation, they are still stuck in these primary level tasks.

By this time, you will be more comfortable investing in new avenues like Equity mutual funds, Real estate, ETFs, Stocks, and other investments. To start with and to get a taste of mutual fund investing, start SIPs in a a balanced fund like HDFC Prudence or HDFC Balanced or if you are too risk averse, you can also start SIP in Montly income plans (MIP’s) or some debt mutual fund.

4. Design your financial life and explore more

In the end, after you’ve completed the 3 steps mentioned above, you can see, how easy it would be to extend your actions. I’d say the above 3 steps will take anywhere around 2-3 years depending on what kind of person you are and your circumstances. In those 2-3 years, you must have accomplished these things

You must have done a good amount of spending and fulfilled most of your wishes

You must be educated well about financial matters and have good clarity about your future.

You must have completed the primary level of basic tasks which any financial life needs

You must have saved a respectable amount through recurring deposits and other investments.

At this moment, you can plan the next 5-10 years of your financial life. Clearly define and prioritize your financial goals in life, and start investing aggressively for your wealth creation. Even if you feel like applying for a loan to buy home or car, you should be able to handle it in a much better way after the first 3 steps. Because you know about his future premiums outgo, & your aspirations more clearly. At this step, if you feel you need some kind of external help to get a better clarity, you can also hire a financial planner for yourself and work with him to get more clarity. A small investment for your financial life can prove to be worth.

You can see that with these 4 steps, the actions one will take will be more defined and realistic, rather than the random events, that push you & which gives an unwanted shape to your financial life.

Conclusion

You can see that these 4 steps are just about giving more meaning and a better shape to any financial life. It focuses on slowing down and then slowly moving forward in your financial life. Any new person is very excited about his life ahead and there are great chances to mess up. These 4 steps will help a person to move forward in his financial life. Good luck!

Do you know how to withdraw your EPF without Employer Signature ? Do you think if its possible at all ? Is your previous employer not signing your EPF Withdrawal documents? Have you left your company long back and now you can not take your past employer signatures ? Or is your EPF company stuck because your employer is not supporting you or helping you in withdrawal procedure ? Or it might happen that your employer relations with you mess up for some reason and now they are not ready to cooperate in the EPF withdrawal procedure and threatening you? Here are 2 real life examples of these kind of situation

Case 1 : Priyanka was also stuck with a company which was shut down and her PF was stuck

The last company i was working with has been shut down. Now I need to withdraw my EPF, however I am not getting any help from the company. I have tried to contact the GM – HR and the CA but no response. As the sum is huge, I am worried if I will be able to withdraw the amount without company’s approval or authorized signature. The full and final settlement has been closed and relieving letter has been issued by the company. Please advise how should i go about in this case.

One of my friend was in a similar situation few months back. I have pay slip but no relieving letter. When contacted with the finance dept, I was told that I cannot get the epf amount as I have not got the relieving letter. The amount will not be released by them even though an epf amount is mentioned in pay slip. He was asked to pay the amount for serving period of two months and then get relieving certificate and later only will they release the funds for epf account.

Now the question. Can one withdraw his EPF without the support of his past employer signatures or support ? Yes ! – There is a solution! .

Today we will discuss, how you can withdraw your Employee Provident Fund money without your past employer’s help. A lot of people feel that it’s not possible without employer involvement, but it’s not true! Let me start by sharing a bit about this.

Employer can not control EPF money

Each month employer takes the EPF part, out of your salary and along with their contribution, deposit it into your EPF account with the EPFO organisation. Once they deposit it with EPF office, then it’s just your money and no one else’s. Your employer can not control it. However note, that your employer’s signatures are required on the EPF withdrawal form, to certify that you are not employed with them anymore and now you can withdraw the EPF.

A lot of people leave their jobs without serving the notice period or because of some other issue and employers do not help them to claim their Provident Fund money. Here is one instance on our Jagoinvestor Forum

I worked in a company in 2009 for few months. I had some issues with them and resigned from that company. I did not get any relieving order. All I have is my salary slip which has PF account no. Is it possible to get back the PF amount without the permission/notice to the previous employer which I worked ?

3 steps to withdraw your EPF without Employer Signature

Here are 3 steps you need to do to successfully withdraw your EPF without previous employer signatures.

Step 1

First download and fill up Form 19 (for EPF withdrawal) and Form 10C (for EPS Withdrawal)

Step 2

Get it attested by any one of the following

Manager of a bank (PSU preferred)

By any gazetted officer.

Magistrate / Post / Sub Post Master / Notary

Step 3

Write down a letter addressing the regional PF commissioner, stating the reason why you have to get it attested and how you are facing issues with your employer. In case you have any proof of unsupportive behaviour from your employer, better attach it. (This step is optional, and not mandatory)

Step 4

If you are unemployed, you will have to make an affidavit that proves that you are unemployed. Download this Affidavit Sample and get it printed on a Rs. 100 stamp paper with a notary or any gazetted officer signature on it (This Affidavit is part of our Jagoinvestor Wealth Club) . This is required because you need to be unemployed if you want to withdraw your EPF . If you are employed, you can transfer your EPF to your new employer.

Step 5

Send these forms to your regional EPF office and wait for next few months for some kind of action.

Step 6

Once your application is processed, the EPF withdrawal request will be honoured and you will be paid. If you still don’t see any action or response, then its time to File an RTI application to EPF Department for finding out the exact Status.

Legal Action against your past employer

Note that Employee provident fund money is totally yours and no matter what the situation, your past employer should be helping you in withdrawing it. It can be some issue your employer or you might have.., your employer can not say that they will not give signatures and create issues in your EPF Withdrawal.

If that’s the case, it might be time to teach them a lesson.

If you are 100% sure that you are correct and it’s a case of harassment, just collect all the documents which proves the harassment and then inform your regional Provided Fund officer about this. He will carry out an enquiry, contact the employer and if he finds them guilty, there can be legal action against the company and might even amount to imprisonment. It’s the Employer’s duty to keep records as per the law and also maintain the terms and conditions, failing which employer can get a notice under a section 7A, which lays the guidelines of strict actions against the employer. I got this from one of the RTI related websites

Normally, the EPFO which maintained your EPF account should have settled the claim based on the signature of the Bank Manager since you find it difficult to get the form attested by your previous employer. They should not have sent it back to you telling to get the signature of the previous employer. The fact appears to be that the employer is not willing to sign the form for some reason or the other. (I presume the establishment is not closed but is still working). It is the duty of the employer to sign the settlement form. If he fails to do so the Regional Provident Fund Commissioner (RPFC) concerned can take action against him. You can make a complaint to the RPFC pointing this out and urging him to either settle the claim as it is or to get the claim signed by the employer and in case the employer declines to sign to take appropriate action against him instead of harassing you by not settling the claim. Please send this complaint by registered post and keep copy. After about a month if no action is taken file an application under RTI and ask what action has been taken on your complaint,people responsible for not taking action etc. Your claim will automatically be settled.

Conclusion

It’s possible to withdraw your EPF money without the help of your past employer. You just need to know the right steps and should also have the energy and motivation to follow up on the matter. Let us know what did you learn out of this article. Do you think this is something useful for you? From this article, did you understand properly how you can withdraw your EPF without Employer Signature ?

Are you a real estate expert ! ? If yes, please help a fellow reader Yakgna Kumar, who has been suffering due to his mistake by investing in a real estate project in Chennai . He wants a right direction and hence he is asking everybody help to guide him. Below is his story from our questions and answers forum

Yakgna story of Builder Cheating him !

We booked IB Greens apartment in chennai Oct 2010, Initial booking was made with promises that are not being fulfilled by IB now. They dragged the agreement signing for 2 years quoting various reasons and until now they are not clear on number of floors, UDS. Now that, they have come up with new agreement – completely one sided and no clear indication of number of floor, UDS, SBA Increase, change in carpet area/floor plan, shared club house for different phases as against separate club house and many other issues. This is clearly a Cheating case !

We have now applied for cancellation of the booking and asking IB to refund the complete amount paid for booking the apartment, IB is not responding on the details of refund but when we call customer care, they are quoting that we need to pay penalty of 5% of total sale price ! – this is mentioned in the Booking Agreement, the booking agreement also says, that agreement should be made within 1 year of the booking, if the booking is not made within 1 year of the booking IB will have to pay 9% interest … in addition to this, they have added few clauses that cancellation should not be intitiated by buyers. Now IB is asking us to sign a cancellation process which makes us to agree for penalty as per booking agreement.

With our little knowledege on real estate, we understand

1. The booking agreement is not an agreement and and just provisional booking form.

2. its been more than 2 years old and when exceeds 6 months it will become null and void.

3. As per the CCI(competation commission of India) any terms and conditions which is one sided is not acceptable and considered as Void.

4. Our refund request is not our own and because of IB failure to deliver the project intime. Till date they are not clear it will be 7 floor or 19 floor. During booking they informed 7 floors and if 19 floor your UDS is almost nil which is deviation from the booking terms.

Questions

1) what should be our step to get the refund, have you seen customers approaching with this kind of problems and how they have handled it?. we have lost 2 years since then the real estate prices have gone up, IB can cancel our booking and sell with latest price and making profit. we have already went through too much stress because of IB attitude towards us and IB billing department asking to pay the first installment without even signing the agreement and also penalty of 18% for delay in payments . we had multiple meeting with IB staff without any change in IB stand on the agreement and so we are planning to cancel. I am attaching the booking agreement snip related to the cancellation/refund from booking agreement. We are a team of buyers, we got introduced yourself after forming a google group when we had to face the problems from IB. We are stuck now, we need correct plan of action and without any further delay and stress for us. Based on your expertise, i would request you to let us know the next steps for us.

2) Will we be able to get our monies back based on the booking agreement? .. is the booking agreement considered at all after 2 years ?

3) We also think, the IB Higher Management may not be aware of the staff and local management’s attitude to customers, if there a way to escalate our issues?

Appreciate your time on reading this long mail. thanks for your support.

Please share your thoughts and Help

What do you think about this case ? Can you share what do you think about this cheating case and how this guy should move ahead, what should be his next actions ?

We are giving away a Free audio on Slowing Down and Grow Rich which we created for our Jagoinvestor Wealth Club last week. The Audio is totally FREE for all our blog readers.

Slow Down & Grow Rich

For a moment look around and see you will find everyone is in RUSH (including you). You rush to reach office, you rush to meet your deadlines, and most people do the same when it comes to producing wealth. Everyone wants to make a lot of money as fast as they can. The truth is that Human beings are CRAZY for money. But tell me! . Will an artist who is in rush be able to create the best painting of his life? Will a chef, who is in rush be able to prepare the best dish of his life? Will a doctor who is in rush be able to perform his life’s most critical surgery?

The answer is NO.

Similarly, an investor who is in rush, is unable to produce desired wealth in his lifetime. Speed has become like an operating system that is installed in the machine called “Human Being”. ButWealth is not a function of speed it is a function of depth. It is about how deep you engage yourself with the process of wealth creation.

Today, we have an Audio GIFT to share with you which is exclusively made for our Jagoinvestor Wealth Club members. With the help of this audio we want you to learn the principle of slowing down and apply it to your financial life. (Every month you get such audio files as club member and more stuff!). Wealth club material is priceless, still we have priced it in a way that anyone can become a member. We want every investor who gets in touch with us to slow down and to have an awesome financial life.

We have also released a nice calculator, which is going to help you understand your income/expenses and assets/liabilities in a much better way. It does some number crunching and based on your current numbers, gives you some detailed insights on your current situation. This calculator tries to give you insights on different parameters of your financial life and marks them as red, yellow and green, which represents “Bad” , “Average” and “Good” . So instantly you can see how well you are doing on various parameters. Watch the Video below to learn more about the calculator. In past we have also released Financial Freedom Calculator for our members.

Let us know if you listened to the audio and if you liked what you heard ? Are you also rushing in your financial life ? Do you think slowing down a bit and carefully moving ahead will help you to grow rich ?

Should you buy real estate properties from small builders ? While you keep hearing about big real estate projects, there are tons of buildings and buildings and apartments build by small builders also and they are quite high in number. Today I want to share 3 instances of dealing with small builders.

Case 1 : Real life case of Real Estate Fraud

One of the readers had invested in a property with a small size builder , but now he found out that the builder is arrested for fraud. He is now stuck with the investment and paying the EMI for the property whose future he is not sure about. Here is the full case

In Jan 2011 i have booked,Registered and stamp duty paid property located at Navi Mumbai(CIDCO property)and all the required documents are submitted to HDFC for under construction property.After verification and search report the Loan sanctioned. The payments are made according to Demands and Work completion by developer on time to time basis.Till the 70% of work completion all the payments are made(April 2012),but after that 19th July 2012 the developer has arrested by local police for cheating and fruad registration(Double registration) on his running projects.

In this issue he was arrested and the news spread across through all the media news papers that Customers are Cheated for Crores of rupees by Navi Mumbai Developer since May 2012.In this case on his arrest i have also made police complaint that, “The construction work has stopped since last two months and Developer has shut his office and mobile.According to media news i am also feeling that i was cheated and the home loan EMI are still there.”Now the developer and Police is also asking me to take back my complaint otherwise developer will sell that property to others and only give me the money which i have paid till the date. When i asked my bank about this to kinldy hold my EMI till the issue will solved.How do i pay EMI of the loan which i took for my Home and without getting home how do i proceed further for EMI?Bank said,”We have given a Loan to you not developer,even though all the documents are clear from Developer according to procedure.And my registration documents are Mortgage with the bank.So i have pay the EMI for the 70% Loan amount which i took from bank till the 70% work completion by developer.”Now i am paying EMI’s without getting Home. So guys pls think 100 of times before proceeding for Under-construction property.It doesnot matter whether it is a branded or Unbranded(Known/unknown Builder)

Case 2 : Unathorised Floor in the Project

One of the readers shared on our jagoinvestor forum that he has invested in a real estate project by a small builder, but the builder has violated rules and added another floor without approval. Now his money is stuck with the builder and he is not able to take any concrete decision

Recently I have booked a flat in bangalore with a small time builder. The catch is he has got approval (BBMP approval) for G+4 floors but he built an extra floor (My flat is on 4th floor). Does SBI approves the loan for apartment in such project? The builder is saying that there are 20+ loan approved from SBI (total 120 flats in project) and he will get my loan approved as well. He is also saying this is quite common practice now a days in Bangalore and he will keep this floor for renting purpose only.

Even if SBI approves my loan, should I buy this flat? What are the complications, I would face in future if selling off this flat (or will live in that flat). I have given 20% of the money as booking amount.

What are your suggestions in my case?

Case 3 : Builder not replying to many queries

I had a terrifying experience with a small builder, who projects himself as a Mid size builder(He completed one small project, of 20-30 flats and he himself given promotion as midsize builder and compares himself with some reputed mid size builders in Chennai).

I got all the documents from builder in a professional way(he gave all documents in set saying these are the documents required for legal verification) and gone for a lawyer verification(its my mistake not to wait for lawyer opinion) and he gave me enough evidences that he applied for a project approval form SBI( I told him, i will get HL only form SBI, after reading articles in Jagoinvester, Thanks to Jagoinvester for their precious articles) i believed him because he behaved very professionally(He is educated and worked for a consulting firm for more then a decade, making me believing he is professional) and i overshoot-ed the lawyers advice( i didn’t receive it for 15 working days) and made agreement and paid 20% of the property cost and then got a call form lawyer(actually lawyer couriered me the docs, but I didn’t receive them) saying courier was returned and he asked me to make a personal visit to his office.

The facts came into the picture with 10 queries( all of them are so simple like EC patta and couple of explanations) and i sent the same list to my builder and got promised, those silly queries will be answered in 5 days, and i waited for 15 days but no reply to lawyer from builder and after repeated follow-ups’(not with Mr. Professional, but with a staff in builders office) finally she went with answers and from my side i too gave the agreement copy for further evaluation and final advice from lawyer( as he is empanelled with SBI, it can be submitted for loan processing). The horrifying truths came out, he further raised additional queries and a builder cheating was projected. There are multiple problems in the land (it is total of 1.5 Acer).

1. Some part of the land was amortized with a PSU (not SBI) for 50L and he paid the amount in the month of July and obtained NOC (still the documents are under encumbrance) and attached the NOC with the documents and he is giving for customers for property verification. But when my lawyer made a background verification( as he has good networking with many bankers), it came to the limelight that he obtained loan again for 50L in the same bank after a month of time.

2. some part of this land is hereditary(legal heirs are 2 brothers and one sister) , sister didn’t sign the document and her brothers sold(here it is JV) the land to the developer, got her signature as witness.After some time she can go and fight legally for her rights on the property, and lawyer requested for a rectification deed and he objected and told he can provide a NOC(generally NOC is valid for 6 months of time, i really don’t know how NOC is valid in this contest)

3. DTCP approval is not obtained

4. There is difference in land available as per patta and land showing in project documents

5. Parent documents before 2004 are missing and told those can’t be retrieved

After presenting all the above(only critical are mentioned) queries, he tried to convince me and get my loan from some other financiers(of course i have a option to choose form PSU and NON-PSU), and offered some gifts (as he is planning to market his flats in Diwali offer such as free modular kitchen,( he increased the price of the flat by rs.200, but not for my booking, as I have done it earlier. Just to hold my booking he offered me this Diwali gifts)) and some other junk promises. I demanded for immediate cancellation of booking and refund all amount on the same day. However, I am in confusion state. If he clears all the above queries it is a great deal in that area and the price I paid was killer price.

I requested him to put all his words in a piece of paper (of course it is a judicial stamp paper of Rs.20, again Kudus to Jagoinvester for education me how to deal in such cases, especially with builders)Got a concrete promise to fix the queries in 15 working days else the entire amount will be refunded. 15 days passed and I have no communication from builder or from his office.On the final day I gave a call, asked him the status, and got a horrifying answer that he is still fixing the problems and when questioned deeply, got the terror answer that he did not start anything until date. Moreover, requesting me to wait for another 2 weeks.

I rejected his request and told him to arrange for cancellation deed and check, for the amount, and he rejected saying he will deduct rs.25 as per agreement. I initially rejected his check and told him I will collect the amount what ever after presenting the issue in front of consumers forum. Moreover, after short conversation he realized that I would make mess( i searched this property in internet and he also told me 70% of his customers are thru internet) if the total amount were not refunded. So guys please be aware and do a lot of background checking before investing your hard earned money.

Vultures are all around us in the form of builders, relaters and especially mediates or brokers or agents or what ever it is… (via)

Background Check of Builders before you purchase Property

It would not be fair to say that one should avoid small builders, but one has to be more cautious with the small builders compared to bigger ones. Here are the 5 things one should always check before they deal with a builder – small or big. This checklist will make sure that your pain is reduced later and the chances of getting in trouble will be minimised.

1. Enquire about their previously Completed Projects

You should always ask them directly about the previous projects they have completed. Better visit them too, and ask the locals and people living there about delays if any and the issues they faced. You should also search about those projects on internet and watch out for any grievances and complaints.

2. Check if they are part of some builders association

There are few associations and groups for builders community and there are codes of conduct defined for builders. Some of those associations are “Builders’ Association of India” (BAI) and “Confederation of Real Estate Developers Association of India” (CREDAI). Its always a good idea to watch out if the builder you are dealing with is a part of those associations or not. While you can’t say that not being a member is always a wrong thing, but you can always ask him why he is not a member. I would say a builder who is part of those association would be more serious and professional compared to other small time builder.

3. Check the rules incase of Delay or Cancellation of Project

You should always ask for the rules and terms and condition which will apply incase of delay or cancellation of the project. Ask them for an agreement copy even before paying the booking amount. Do not get too impulsive with the project and hurry. Watch “Compensation clause” which talks about the compensation paid to the buyer in case of any issues.

4. Search on internet for his review and past

Always do a thorough research about the builder and his quality of work on internet and different forums. While in general all the builders have some or the other bad reviews from someone, watch out that the internet should not be filled with bad reviews totally! In case you do not find any information or very little information about the builder, then you are mostly dealing with some new guy in town, who might be truly unprofessional. Avoid it.

Do you know someone who had dealt with small builder and was stuck with the situation or faced any issue? This can even happen with big builders. Share your experiences in comments section…

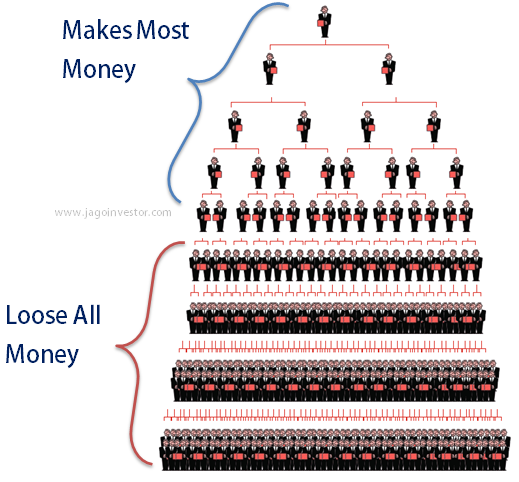

Today we are going to talk about MLM or Multi Level Marketing Schemes which have a pyramid kind of model. For years and decades, these kind of schemes are active and a lot of people get trapped in these Pyramid Schemes and lose their hard earned money. In this article, we will see the common mechanism they work on and their characteristics. We will also create a dummy Pyramid scheme to show you the traps & pitfalls. Before we move ahead, get this fact that we are talking about those pyramid schemes which also have different levels of people one on top of other and where one guy pays money which gets passed on as reward to another.

How Multi Level Marketing schemes work?

Multilevel marketing schemes are generally network based marketing schemes, in which a person has to add more people under him. The people obviously pay some money to “join” the business and then they add more people under them. In almost all the schemes, the person is incentivized for adding more people under them.

You all must have heard about the AMWAY business model, which is nothing, but a great example of Multi Level Marketing, while the business is legitimate and there is no fraud in it, still it also falls under a pyramid model. Even I have attended its meetings once when I was novice child :). The business model looked so easy, just pay Rs 5,000 to join the business and then keep adding more people to “business” and you get some percentage from the entire sales under your Tree. There are various ranks like Silver, Gold , Diamond etc., and the higher your rank, the more you make. Lot of people make money in it through legal way, and more you work harder , the money you can earn, but the point is , people who get in early make more money and the people at bottom struggle a lot.

Why most people lose money in Fraud Pyramid Schemes?

Guess what?! A lot of people make money in these Multi Level Marketing business models, and they become the ambassadors of the business. They flaunt the cheques and the money they make and believe me, some of them are real!. They really do make money and we will quickly see more on that, but the point is, that the majority of the people lose lot of money and struggle in these kind of get rich quick pyramid schemes. And that happens, because there is a limit to adding people. You can’t add more people in the tree after a certain point and when the tree becomes bigger, than it’s trouble point, it’s reaches a kind of saturation level when the biggest chunk of people who are at bottom lose all the money. Here is an example graph which will give you a good idea of what I am talking about.

Example of SpeakAsia

You must have heard about the latest craze called Speak Asia Online! I will really not be surprised if you tell me that you were part of it! I will not be even surprised if you tell me you made lot of money too! That might happen if you started earlier! Because then, the scam was still in the making! If you joined at the end, you were at the bottom of the tree you lost your money. This is how it worked!

A person can join SpeakAsia by paying Rs 11,000 and becomes a “panelist.” He then starts getting 2 surveys per week and getting Rs 500 for filling up each of them. That’s around Rs 4,000 per month and 48,000 per year and that was how Speakasia was promoted by its member to lure other members. This was at the start and though the amount of money coming IN was less than the amount of money which went OUT, and the whole model was unsustainable in long run, it was definitely sustainable in short term. Just think about it! Is it not easy to pay 10 smaller bakras if 100 bigger bakras join the next batch?

And after all that, it crashed! But still there are innocent people out there who claim that it was genuine and it worked for them. They are not wrong! It really worked for them and they made money, but that was part of the game. They wanted you to make lots of money so that you can bring more people in and then one fine day when they make a really big pile money that they can just vanish! Poof!

Breaking Relationships !

The biggest other bad thing about these pyramid schemes are how the relationships become sour and messed up when the person who is part of MLM tries to add all their friends and relatives into the MLM, suddenly they start looking at humans as “targets” , Here is one incident which happened with Shantanu

I know about this as I faced these offers couple of times from my very close friends and relatives. And I know how hard it was for me to tell them “I am not interested”. Those who is a very extrovert in nature and also convince people more, like insurance agents can get success. But most people are in the other side only. In fact one of relative faced very tough challenge later on when people found his scheme a scam. Anyway, I think after such articles also these schemes will come in future and again many will trap in them also.

In one other incident, one of the Fraud scheme called as “Japan Life” made someone lose his girlfriend

Long time back in 2000, my girlfriend got stuck up in a similar scheme called “Japan Life”. They used to take 80,000 Rs. and will give you a magnetic mattress. She tried to get me in as well and I was almost about to get trapped but sanity prevailed and I escaped, however since I did not join, I lost my girlfreind forever. I remember this fraud came up in Star News and I could see so many people getting cheated. This was around New Delhi and surrounding areas

Some other popular Multi Level Marketing and Pyramid businesses which were actually a scam were GoldQuest, StockGuru , UniPay2U etc etc (add more name in comments section if you are aware about them). Moneylife has also done this story on Multi Level Marketing companies in Forex trading, Have a look at it.

Jagoinvestor MLM Scheme – Lets create a SCAM Plan right now

Let me know you how simple it is to create a pyramid scheme and it will look so attractive . You all know I have written a Personal Finance Book called “Jagoinvestor – Change your Relationship with Money.”

Now here is a scheme

Pay Rs 1,000 and become a member of the scheme

You get the book FREE on signup

Make a person join the pyramid scheme and get Rs 250 for each person

You can add any number of people to this scheme

You realize that if you add 4 people to the group, you will get a 1,000 bucks and a Free Book! So it’s extremely easy for you if you join the scheme early.

Let’s say 10 people join under me.

Level 1 – Add 10 people

So 10 people will pay 1,000 each and I will make Rs 10,000 total , and I will send back a FREE book to all the 10 people. I incur Rs 5,000 expenses and make a cool profit of Rs 5,000.

Level 2 – Add 100 people

Now let’s see… Each of these 10 people persuade 10 more people under them, and 100 more people join the scheme. They will pay Rs 1,000 each to me;, that means Rs 1,00,000. I will spend Rs 50,000 for the 100 books , and I will be left with Rs 50,000. But out of this 50,000, I need to give a share to each member at level 1, for 1 person the incentive is Rs 250 , so for 10 people, the incentive is Rs 2,500 for each person at level 1, and because there are 10 people at level 1, I will have to pay Rs 2,500 to each at level 1, and I will have to share 50% out of 50,000, that’s Rs 25,000. But I still keep Rs 25,000 with me.

So now you can see, I made a total 5,000 from 10 people at level 1 and Rs 25,000 from 100 people at level 2. And each of the 10 person at level 1 made cool 2,500 from 10 people they added under them, they not only recovered their 1,000 back, but also got extra Rs 1,500 and a FREE book! Wow! This business model is amazing!

Level 3 – Add 1000 people

So the business is expanding and the word is spreading and my book ambassadors are in the market advertising this scheme and showing the kind of money they are making and the free book they get! Dude! They also have a valid cheque with them! No fraud! . So the word has spread like wildfire now and everyone wants to join this business.

Now, lets say each person at level 2 adds 10 more people under them again, because the word is spreading about this awesome business. There will be 1,000 people at level 3, paying 10 lacs to me and I will incur 5,00,000 expenses. I will pay 2,500 to each person at level 3, that means 2.5 lacs in total, but I will still keep 2.5 lacs with me.

Level 4 + 5 + 6

Can you see, how it’s growing? And how people are making money? From 1 person to 10 people, and from 10 to 100 and them from 100 to 1,000? But what next? Level 4? Level 5? Level?

When this reaches level 6 , there will be 10 lakh people under this scheme and they will be paying 100 crores to me! . You guys are going to hate me at that level! . Because you will never see me again! . Neither will I send any more books to anyone!, Nor will I send any share to anyone. I will just run away and you wont be able to trace me! . Any person who would have joined in at the start would find it easy to grow and spread the business. But people at bottom will just not be able to do anything, they are the last batch of fools!

During my College days there were 2 such schemes ( 7000/- & 1200/- each) introduced to me by my friends & asked me to join them. I explained them that they are highly unsustainable by using simple exponential formula (2^e). But still they thought i am a fool & not making money out of this wonderful Golden “Pyramid”. Thanks to God for that!!!. I just want to say that “User Pure Maths” before entering or dealing with any thing with your hard earned money. Be on your foot not on air.

In 2007, one of my good friend called me when i was out of station. “Sam, i have something great to share with you, when are u coming back? i cant wait to meet you etc etc”. I was kinda surprised and was very curious what he is gonna talk about. He took me to this office where many others showed cheques explained business model, asked me to buy some product and become a member. People were so promising that they will help me , let me grow & earn lots of money and all.. It was ‘Gold Quest International’. That day i made the biggest mistake of my financial life. They made me buy some Gold & Silver coin for Rs.38000 rupees using my credit card. After i joined i tried to reach out to some people in my circle and most of them are already part of it & others are not interested. To pay this credit card bill, i had to take a small personal loan. It was the initial days when i got into job and all these incidents made my financial position worst.

I lost 20 K in this MLM bullshit … it was with the name Cossets in Delhi . They arranged a huge pomp show in Siri Fort to show off the happiness of the people who had made money and became millionaires. There were multiple stores in Delhi where u cud purchase if u were a member Then some Ex army also got fooled joined in and invested smthng like 4-5 Lakhs his life savings got duped and then he made a case on the company . Phew Cossets was like GAYAB.

My brother was a victim of it late in 2002 in scheme(scam) called netkhazana.He lost around 17k at that time.And from that time I have got recommendations from freinds(?) and relatives(?) in to hell lot of schemes but never got into any because of the first bitter expereince. I suppose this schemes are gr8 if you have selfless people involved but that does not happen as the corpus grows to crores of rupees and people at top tempt to cut the goose.

Other Models of Scam

There are many other multi level marketing scams, which are not in a pyramid model, but they ask for money for some awesome investment based on some logic and then they really give back awesome returns to handful of investors, who spread the word about the scheme and them more and more people join the investment scheme and once it becomes very big, the person who started that scheme vanishes. The Govt is going to take some tough measures on these kind of fraudulent schemes. Here is a nice video which explains more about this.

Beware of these Get Quick Rich models

There are a hell of a lot of schemes and businesses running which show promises of making awesome returns from gold, stock market, real estate and many other kind of investments. They mostly will look really attractive and credible, but always remember that if someone is offering you anything better than bank fixed deposits, there is no doubt that there is some of the other risk involved. The bigger the potential return, bigger the risk.

Disclaimer : Note that we have just discussed how Network Marketing works and the basic mechanism. There might be various businesses and models which are making money, and might be good. This article just wants to bring awareness among people on the concept of pyramid schemes and they fool and loot majority of people in our country .

If you come across any Business like this, first make sure you check that its a member of India Direct Selling Association, which kind of gives a legitimate name and also they follow certain code of ethics. If its not part of this, I would say better stay away from it. Amway is part of it. So, not all Multi level marketing models are fraud, a lot of them are genuine also. Here is what Sunil shares about this

A Multi Level Marketing is different from Direct selling. Any company selling directly to the customer, removing all the supply chain management commissions behind, will be governed by Indian direct selling association, http://www.idsa.co.in (within India) and world federation for direct selling association, http://www.wfdsa.org . There are many companies like Avon Cosmetics, Amway, Oriflame, Herbalife, Tupperware etc.. registered under these federations. These companies work under the ethics defined by the IDSA or WFDSA and are very harsh on the people who dont adhere to these ethics. Many people reading this article will agree that the quality of the products they produce are amongst the best in the world. Many people are under the impression that these companies are similar to the other ponzi schemes.

Let us know what do you think about the concept of Multi Level Marketing and associated businesses. What is the biggest reason you think people fall for them and get trapped?