Are gold saving schemes by jewellers really a great investment option? There are huge number of people who become part of gold saving schemes offered by jewellers, assuming that they are amazing deals which they should not miss! There are few advantages and disadvantages about these gold saving schemes. It’s important to understand them before you invest in those.

Ankur asked this simple question on our jagoinvestor forum which triggered this article

Lately there are ads coming on TV abt this Golden harvest scheme (GHS) from Tanishq, where you pay for 11 months and the company will bear the installment for 12 month to buy Gold. Any reviews abt the scheme?

1. Most of the schemes are plain money saving schemes

The way a lot of gold saving schemes project their plan is as if you are buying real gold each month, but majority of them are just plain money saving scheme where you deposit a fixed amount each month for X months and in the last month the jeweler deposits the “bonus” installment and then finally you use the money to buy the gold jewelery at the price prevailing at that time! Not at the gold price the time of joining the scheme! So in practice the whole scheme becomes like a recurring deposit where you deposit some money each month. The bonus installment deposited by jeweler makes sure you get a return around 8-10% on the overall installment.

2. You cant redeem Money

Unlike recurring deposits, you can’t use the money accumulated in gold saving schemes for any purpose. The gold saving schemes make it mandatory that you have to buy gold jewellery and only gold jewellery, not even gold bars or coins. So in case you need money for some other purpose, you can’t use it. But you will say that it’s fine, because at times you also are offered “Zero Making Charges” under these schemes, but you miss reading the terms and conditions which says that it’s only on selected designs and models. What if you do not want to buy those designs? In that case you have to pay the making charges which are applicable and what happens if the design and model which you like have much higher price than you have accumulated? In that case you have to shell out more money. The making charges which you will pay will cancel out the 8-10% returns which you make on the whole scheme.

3. Not as safe as Recurring Deposit

Now as you have understood that gold saving schemes deep down are just like a recurring deposit. However they are not as safe as a banks recurring deposit, for the simple reason that jewelers are not as strong financially as banks and some jewelers actually deposit the money they get in schemes in banks as fixed deposits only. Some jewelers might even be using the money for their operating expenses also.

4. Gold saving schemes are designed to guarantee future sales

If you look into the design of gold saving schemes, it’s clear that it’s a way to assure future sales. People join these schemes, start saving money with jewelers and after 1-2 yrs, they will buy some thing from them. So if X people join the program, all X people will buy something at the end.

R.K. Sharma, executive director from PC Jeweller confirms this – “This scheme is a business building programme. By getting customers involved in this scheme, we ensure future sales. A majority of the times, people purchase a jewellery for a higher price than the amount invested. It is a sure shot business opportunity through which we seal our future sales.” – source

Some of the gold schemes in market

Gold Harvest from Tanishq

Jewels for Less from PC Jewelers

Shagun from Gitanjali

Kalpvruksha from Tribhuvandas Bhimji Zaveri

Gold Tree from GRT Jewelers

Jos Alukkas Gold Saving Scheme

Kothari gold deposit scheme

Gold Schemes – Bhima Gold

When you should join these Gold Saving Schemes ?

So given these fine points, there are few advantages to these gold investing schemes and there are conditions when you might want to invest in those. The first thing is that, a lot of investors who do not understand what are other kind of options for investment in gold like Gold ETF, e-Gold etc which are popular ways to buy gold online these days. Because of not having full information, investors get inclined to these schemes and invest on the name of “Gold”. However good part of these schemes is that, because of these gold schemes, they atleast develop the habit of regularly investing some money, which they would not have done otherwise. So these schemes can be your monthly gold investing plan in a way. These investors will not invest in gold ETF and simple recurring deposits anyways, so its better that they atleast invest in these gold investments schemes by jewelers atleast. So these schemes are good from that point of view.

Another reason when you can look at these schemes is when you have a marriage or function due in next 1-2 yrs and you might want to systematically invest some fixed money for the purpose of buying gold jewellery. Even in that case it makes sense to get into these schemes.

Have you invested in these kind of gold saving schemes online without understanding how it works? What are your comments on these kind of schemes?

While I was working out in gym in morning, I has a strange feeling that I can connect every aspect of ‘staying healthy’ with ‘building wealth’. There are various things which can be used as an analogy to teach good things about ‘creating wealth’ , but the area of health is best as an analogy. I am sure a lot of you who take health seriously and exercise regularly will be able to connect well and appreciate this article, others who do not take care of their health might get the maximum value because they will appreciate both the things (health and wealth points) . Lets see those points .

1. Starting is Easy, Continuing is not

Its very easy to go for a jog/walk at 6:00 am for 2-3 days. A lot of people decide they will do it, and a lot actually achieve it . But what happens after a week/month ? We discontinue it and life is back at square one and we are just lost in our daily life exactly the same way we were earlier . You break your promise of “I will exercise in morning at 6:00 am” , and it all starts with a very small violation, which takes a big shape. Starting out something is damn easy, but the real question is how long you continue it ! and with what commitment. So don’t tell me you got up at 6:00 am . Tell me how long have you been doing it , that’s the real parameter.

In the same way, its too easy to start reading a new blog, starting your SIP , start writing your budget and even working on your financial life. A lot of people get some adrenaline rush, after I write some good article which makes them feel – “Its high time now. I should do something about my financial life” and they start doing something, but the real parameter to look at it is – “Are you consistently doing it ?” . Is your SIP running from many years, month after month without fail ? Are you writing the budget month after month and following it ? A Rs 5,000 SIP running for 10 yrs would always (well , in most the cases) beat a inconsistent SIP of Rs 12,000 . A consistent written and followed budget which was not that detailed, will be much better than a inconsistent budget which was very detailed. A simple strategy followed for years with consistency will just be better than a complex one which is not followed regularly.

2. Focus has to be on Long Term

Imagine you a trainer in gym and someone recently joined with 90kg weight, and complains to you that – “It has been 1 week, and my weight is still the same !” . What will be your reaction to that ?

You need to give sufficient time and patience to see results. You need to understand how things work in health and only when you understand the internal working , you will have faith in exercising , only then you will continue it. Over 6 months, you will see some results , over 1 yrs you will see good change, over 2-3 yrs , you will be a transformed person all together. Short term is just short term ,you can only build some artificial muscle in such a short time. But if you need some serious health, it can come in long term only.

In the same way, wealth can not be created in short term (I am talking about investments here) . Wealth multiples itself over long term and if you want to build 1 crore rupees in 3 yrs with your Rs 50,000 per month salary (god knows what is left at the end of the month) , you are probably from Venus , not Earth for sure. Just like long journey starts with a small step, you need to start your wealth journey with small steps and then built upon it . You need to understand some of the fundamental principles of personal finance (which I have shown in my book – “16 personal finance principles every investor should know“) . Unless you understand them, you will always doubt short term volatility in your portfolio, you will just get too much attached with security aspect of your money and will not allow your wealth to grow.

3. Diversification is Important

Imagine you are only and only working on your left hand when you exercise . Try to visualize it . You are concentrating only on your left hand and how to make it strong. What will happen in next 2-3 months ? I am sure you will not even last that long, but even if you do , your left hand will surely look artificial on your body and ache like anything because you just never cared about other parts of your body and other aspects of your health. A good health is function of good diet, good sleep , good exercise and your life style. Imagine you work out brilliantly , but then, all you eat is junk like Mc’D , KFC , Pizza’a , maggi etc etc .. Or imagine your diet is excellent , but you do not work out at all and sleep at 3 am and wake up at 11 am daily. This all is going to reflect in your health and you are not giving 100% to your health. You cant expect a lot !

In the same way, when it comes to wealth, you just cant be sitting on only and only Fixed Deposits or only and only ETF’s, or just 100% into real estate fully (unless you are a pro and understand what you are doing). You have to make sure you keep a balance and understand each component’s importance in your financial life. A good mix of real estate, equity, debt , cash , gold is desirable for most of the people (for a common man) . While Debt part will give you security and some peace of mind, real estate will make sure you do not feel left out in the race, the equity part makes sure, you are earning some real return at the end after tax and inflation, gold will keep you wife happy and cash will bring smile on your face and tears in your relationship managers face. The point is – don’t over-invest in one category without understanding its impact and accepting the outcome. Always keep balance and harmony among each other depending on your age and risk profile.

4. To get best quality, you need to invest your time/money/energy

I recently invested a huge annual fees in a well known gym. We get best equipment’s, best environment, best facility, dietitian to look after what we are eating and a good tracking of where we are in our health chart, regular track of our weight, measures and it helps me and my wife move in the direction we want to reach. You need to invest money to get the best most of the times. Apart from the money, you need to put a lot of times and energy from your side. This brings good health over long term. While you can also just go to a park in morning or jog on a road, you still need to invest your time and energy. You need to invest in good shoes, a comfortable work out dress. The point I want to convey is – while you can always look out for free things in life, which works , at-times you need to invest your money, time and energy to get the best. Do not look for money when it comes to your health, you can earn 10x times more if you have a better health.

Just like that, I see a lot of investors destroying their financial life, because they just do not want to invest money, time or energy in their financial life. You can get best, if you are open to invest money, time and effort from your side. The good things do not come cheap always. Hire a good advisor/planner who you think will be able to deliver what you want out of him. Invest in good programs, good books , invest your time to learn things, go to that extra mile to understand concepts and how things work. We have around 550 articles at this moment on this blog and 6,000 questions answered on our Q&A forum, ask yourself how much energy and time have you dedicated to learn things and find out new ideas. We have written 3 books, which we feel can really transform your financial life, all it takes is Rs 1,000 to buy them. Go ahead and just read all of them and you will at a new level. I recently paid Rs 3000 to attend a TIE session in Pune, just to hear Naranyan Murthy (for 1 hour) and Devdutt Patnaik (for 30 min) . What I got back was tons of their experience and whole new ideas which made my Rs 3,000 a tiny thing. Good things always comes when you make an investment , you just have to focus on value.

5. It keeps you energetic

When you exercise in gym or at park near by or at home, there is a point where you feel – “I cant do more exercise, Its paining now” . At that point if you stop, you do not get the best results. The best results are always on the other side of your comfort zone – Always in every area of your life. When you feel exhausted, gave your 100% , when you are wet with sweat, your whole day goes amazing. The kind of energy and excitement you feel inside you is awesome. You are more happier, you smile more, you are more kind and you feel more energetic, ideas inside your head are better. Just one activity leads to a great day. And when you do it every day, then each week and each month is great.

Just like you feel energetic when everything in your health area is good, you feel really blessed and good when thing are right in your financial life. When you have completed all your pending tasks in financial life (Join our massive action revolution called 100moneyactions), when you have achieved a sufficient milestone in accumulating wealth, when you have some respectable bank balance, when you have good emergency fund in place, term plan and health insurance already taken and completed. The kind of energy and excitement you have in your financial life is different . You look at your financial life and feel better. You can concentrate on other areas of your life.

6. Structure and Environment increases your dedication and consistency

Good health comes when you are into a nice structure and environment, which fuels your appetite to exercise and improve your health. You will not feel like working out when you are inside your office space, you will not feel like exercising when you are into a movie theater. But when you are inside a gym or a park in morning, you suddenly ‘feel’ from inside that you want to exercise. Thats the power of Environment. Just see anyone who has amazing health, its because they are part of some great environment and structure, it can be as simple as getting at 6:00 am and going for a walk. That’s also an environment.

In the same way, a proper environment helps a lot when you want to improve your financial life. When we did a 1 day full workshop in Mumbai recently, It was all about creating an environment, where you 100% focus on your financial life and discussing ideas which can take your financial life to next level. This blog is an environment, our 100moneyactions is a dedicated environment for taking actions in your financial life . I want you to look at the following video which will help you understand more about power of environment and structure in your financial life.

7. Starting early helps

While its never too late, its always a good idea to start early in life. Imagine two cases, one where you have had a healthy life all your life, and then second case is when you are extremely unhealthy till now and now trying to have a health life at 45 yrs ! . Most of the people around 40-50-60 yrs old today are facing so much issue getting a health plan and also dealing with life overall. They have medical issues and its affecting everything in their life, even people who are connected with them.

Imagine if they had taken care of their health long back, it would be a different situation today. If you are not joining the gym right now, just because it costs money or you have less time, you get very clear that you will pay both of them later with huge interest. In Nandish Book – “11 principles to achieve financial freedom”, In one of the chapters, he has put a quote by Dalai Lama , when asked what surprised him most about humanity ..

“Man. Because he sacrifices his health in order to make money. Then he sacrifices money to recuperate his health. And then he is so anxious about the future that he does not enjoy the present; the result being that he does not live in the present or the future; he lives as if he is never going to die, and then dies having never really lived.”

The same applies to your wealth and financial life. The mistakes you make today, will come back to you later and hit you hard very much. I cant say more on this, but just say you this – A lot of people are not able to lead their financial life properly when they are earning right now. Imagine what they are going to do when they will not earn and still be living on this planet for 30-40 more years. I am talking about retirement. You work for 30 yrs and earn, and you struggle a lot. Imagine retirement of another 30-40 yrs, when you are not earning. Its a life sentence followed by death if you do not start earning and do something about your financial life. A good start will always give a great support to your financial life. Here is an article showing you the power of starting early

8. Neglected, because it does affect you in short term

This is my favorite. This I think this is one of the biggest reasons for a bad health life and a bad financial life. A single action if not taken does not affect our health or wealth at that moment, but collectively they destroy our health and wealth in long term.

Coming to Health, When you eat a sweet (I used to eat a lot of them, when I worked in Yahoo) , skip your meal, skip your gym/exercise , that single act is not going to affect you at all (it looks like that) . You cant see its impact on your health in a long run. Each Pizza you put down your stomach instantly gives you taste, but instantly it does not give you a shock. You only see it months and years later. When you put on weight, you suddenly one day realize – that you have put on weight, it does not appear in parts. Suddenly one day you feel , your are too weak or do not feel energy in your body. It all starts small.

In the same way, I see a lot of messed up financial life which all started with one small mistake and then just grews SLOWLY ! . Every time you swipe your credit card, you feel like you will deal with the debt somehow, how troubling can one credit card swipe (which was really not needed) be anyways ! and then you create history !

Each month, when you blow up your money and do not save a single rupee, it does NOT affect you at that very moment. Every time you stop you SIP for something which is URGENT, it does not mess your financial life at that very moment. But all these things combined are just destroying your financial life. Each time you postpone taking some action in your financial life, it just messed up your financial life even more. So nothing hurts in short term, because its not visible – and its true in all the area like health, wealth, relationships, career or whatever it is ! . Stop looking for instant gratification, and suddenly you will have the half battle won !

9. There are shortcuts offered

You must be seeing a lot of shortcuts offered in the area of Health on TV and Newspapers. Some magic belt which will eat off all the fat, some majestic coffee, which has divine properties and can reduce your fat, health clubs offering packages which promise you things like – “Reduce 20 kg’s in 2 weeks” .. etc. A lot of people take these shorts cuts and end up paying huge costs, Money is lost, time is lost, health takes a hit and your trust reduces on anyone who comes to offer you any advice in future.

The same thing happens in the area of wealth too. We often get a lot of paid clients, who had a bitter taste with some other financial advisor in past, who sold them junk or didn’t provide any thing valuable to them even when they charged them good amount of advisory fees.

There are too many people offering you free advice, some good and some bad, there are too many short cuts which are offered to you and even you as investors are keen on taking short routes to build wealth, but eventually end up paying huge cost. There is no alternative of doing your homework and really spending your time and effort in building your financial life.

10. You act on it when you feel a sense of Urgency

Its a strange thing, but most of the people start to take any action in the area of health, when they see there is some ‘problem’ . When its URGENT to do something, when its too late and now its a matter of Do or Die. Didn’t those people who are very obese, knew from many years that some thing needs to be done ? Are you not aware right now, that you need to improve your health ? Yes you are , but you will take action only when you have a sense of urgency in that area, then you will suddenly have time, money and that effort required, which you do not have at the moment (this is what you believe).

The area of money is same. You do not work on it, until there is no option left. Most of the people who come to us for financial life come at the last moment. We always tell them, if only they would have come lot earlier, we could have served them in a better way. You go to a paid workshops, only when you are very sure now you need an external help, you go finding a solution, not to learn and explore new ideas . You are too needy in your financial life then and remember one thing – “Needy people do not have power in life”

I would suggest that you get my latest book – “How to be your own Financial Planner in 10 steps” and start planning your financial life in a better way. So do things not when they are urgent, but when you should do it. Dont take health insurance when you have a illness, you will not get it. Take it when you are in the best of your health. Don’t start SIP in mutual funds, when you can see your goals has almost arrived, do it when its very far and you have good time left for your money to work hard.

Wish you best of luck !

I hope you got some realization today, do let me know which area of your life did you get realization on ? Wealth or Health ! .. or BOTH !

What do you do when you want to take a very high health insurance cover like 20 lacs? Is the only option a regular health insurance plan? In this case, you can use top up health insurance plans, which are one of the best ways to enhance your health cover after a certain threshold? In this article lets understand how top up and super top up health plans work and how they benefit you. So we will understand both “top up health insurance” and “Super top up health insurance” in this article, but let’s understand first what the meaning of “Top up” is, in general.

What is the meaning of “Top Up” Cover ?

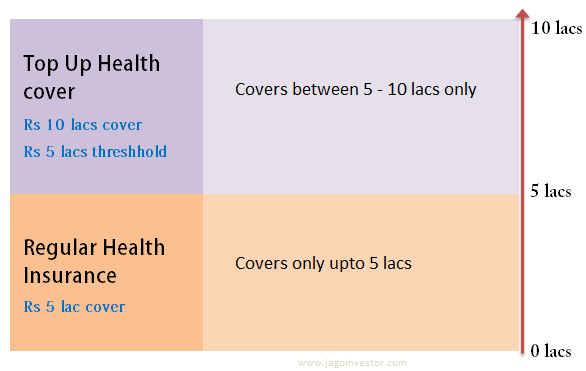

A top up cover actually covers you after a “threshold limit” is already exhausted or used. To give you an example lets say you have a top up health cover of Rs 10 lacs sum assured with the threshold limit of Rs 5 lacs, in which case the policy will only cover your expenses beyond Rs 5 lacs only. If your claim amount is Rs 8 lacs, then it will only pay you Rs 3 lacs (8 – 5), and NOT Rs 8 lacs total. That’s the main difference between a regular health cover policy and a top up cover.

So now if you already have a health insurance cover of Rs 5 lacs sum assured, then you can take a top up cover up to Rs 10 lacs with threshold limit of Rs 5 lacs, that way you will be covered up to 10 lacs. The first policy will cover you up to Rs 5 lacs, and the top up cover will cover you for the 5-10 lacs range. You can understand that more clearly with following image.

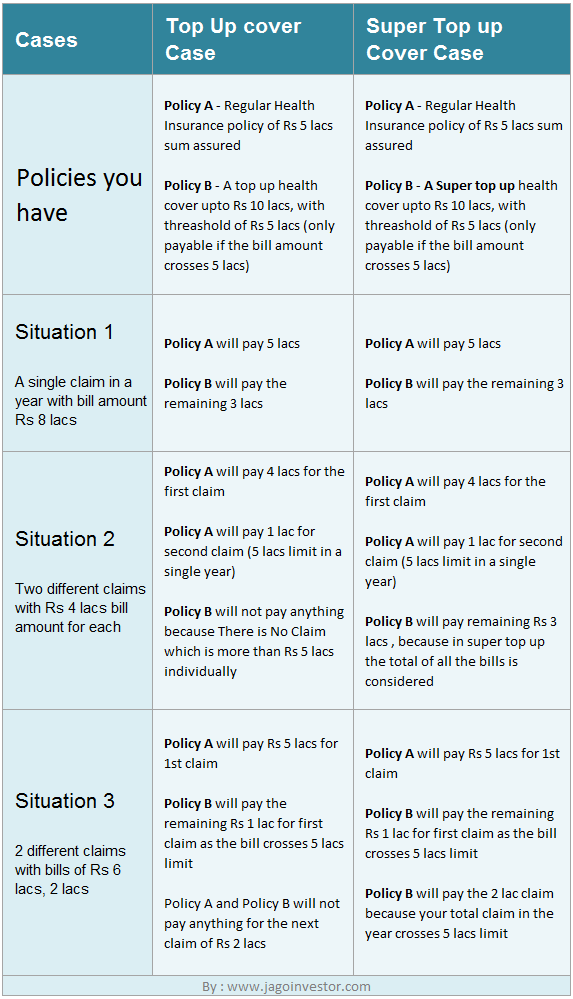

Suppose you have following 2 policies.

Policy A – Regular Health Insurance Plan with Rs 5 lacs sum assured.

Policy B – Top up cover of Rs 10 lacs with threshold limit of Rs 5 lacs.

Now let’s take this same example and try to understand how Policy A (Regular Health Insurance) and Policy B (Top up health insurance) will pay you in 3 different scenarios, just to make sure you fully understand how top up health insurance policies work.

Scenario 1 – Claim of Rs 3 lacs

In this case, the first policy will cover you for full Rs 3 lacs, as your policy itself is for up to Rs 5 lacs.

Scenario 2 – Claim of Rs 8 lacs

In this example, the first plan A, will cover you up to Rs 5 lacs, but if your hospitalization expenses go to say Rs 8 lacs, then the first policy will only pay Rs 5 lacs, but the second policy (B) will cover you for the rest of the Rs 3 lacs, which is above the threshold of Rs 5 lacs.

Scenario 3 – Claim of Rs 12 lacs

In this case, first policy A will pay you Rs 5 lacs, and the second policy B, will pay you next 5 lacs only, because you have taken a top up cover of up to Rs 10 lacs only. So the Rs 2 lacs extra, you will have to pay from your own pocket.

What is Super Top up Cover ?

Just like a top-up cover, there is something called as Super Top-Up cover, with a very small difference. A top-up cover will pay you only if your claim amount (bill for a single hospitalization) is above the threshold. Like, in our example above, the top up cover will help you only when your bill is above Rs 5 lacs each time, only then it will come into picture, like in the case of the Rs 8 lacs bill, then the top up cover will pay you an additional Rs 3 lacs. But if you have two bills of Rs 4 lacs each, then the normal Top up cover will not help because no single bill amount is above the threshold limit of Rs 5 lacs.

That’s where Super top up plans come into picture, which takes into consideration the TOTAL of the bills in a year and not just the single instance. So in case of two bills of Rs 4 lacs each, your total bill is Rs 8 lacs (above threshold limit of Rs 5 lacs), then Super top up cover will pay you, where a Top up cover will not.

Let me clear that with a more detailed example by using the chart below

Companies Offering Top up and Super top up plans in India

Companies offering Top up

Apollo Munich OptimaPlus

Bajaj Allianz Extra Care

Bharti Axa High Deductible Health Insurance

ICICI Lombard Healthcare Plus

Star Health Super Surplus

United India Top up Health Insurance

Companies offering Super Top up

United India

HDFC Ergo Health Suraksha (offering to bank and credit customers, currently)

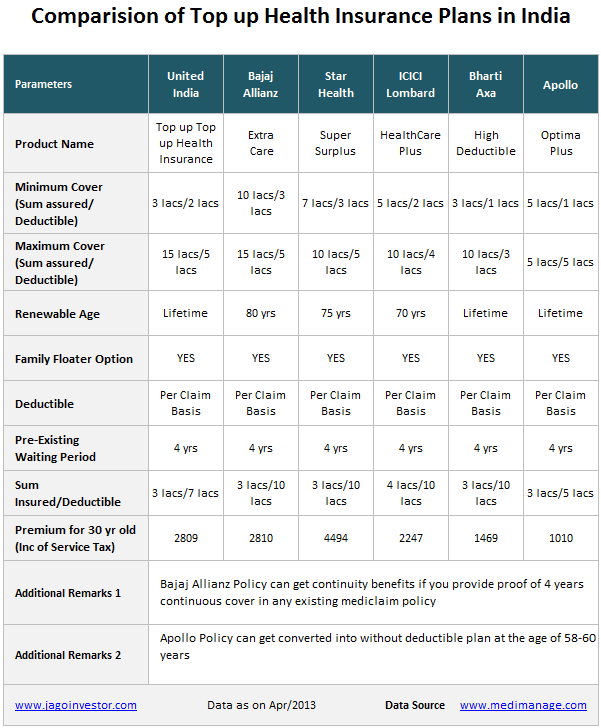

Let me give you a comparison chart of the current Top up health insurance plans in India at the moment. Not many Super top up plans, so they are not in the chart while comparing.

Super Top up Cover for Employees having group cover from Employer

A lot of salaried employees already have a group cover from their employer and they feel that they should not waste their money in a separate health insurance policy (which is not quite a right way of thinking, and you can read this article to know why I say that.) A top up cover is a very useful way for those employees to extend their cover beyond a point.

Lets say you already have a 5 lacs cover from your employer, but you feel that it’s insufficient and you wanted to have a cover up to Rs 10 lacs. Now, one way of doing it is to take a separate cover of Rs 10 lacs, but you can take a top up cover of up to Rs 10 lacs with threshold of Rs 5 lacs (as you are already covered from your employer up to 5 lacs). This way you will be covered up to 10 lacs. But understand that in that case you will have to claim your expenses multiple times.

Additional Health Insurance cover or Top up cover – Comparison

Just give me pointers, I will write about it, or just send me an example where we are comparing a 10 lac cover with A 5 Lac cover + top of 5 lacs

When does a top cover policy makes sense – Hear from experts

So is topup or super top up cover the best option to upgrade your health insurance coverage ? No !. Here is what Mahavir Chopra, a health insurance expert suggests –

Most Insurance advisers recommend a top-up plan to upgrade your coverage. In terms of convenience of purchase and claims, we would recommend upgrade of the same health insurance policy, as the best option. This is of-course, provided you are happy with the policy terms and services.

The second best option would be to compare available options of Super Top-up with option of Additional Mediclaim Policy. If the premium is more or less the same, we would recommend additional policy more than a Super Top-up.

After all the above options, look for the option of a simple top-up to increase your cover. Be sure you are aware of the fact, that this option is more useful in the very long term (6-10 years), since it will trigger only when your one claim goes above the threshold/deductible mentioned in the policy.

Features of Top up Health Insurance Plans

Let me tell some more points and features about the top up plans so that you are more clear about it and if its useful for you or not

1. Cheaper than regular health insurance plans – You have already seen that they are cheaper than the regular health insurance plans because they cover you only beyond a threshold, the probability of which happening is very less.

2. You can buy it from anywhere – You can buy a top-up cover from any company, there is no compulsion that you need to have another cover from same company. In-fact there is no requirement that you should have another health cover at all. You can just take a top up cover even if you do not have any other health insurance product.

3. Available with the option of individual and Family Floater Cover – A top up cover is available as individual cover and also as a family floater. So you can extend the cover for your entire family. Just that some policies might consider parents into family floater and others might not.

4. Concept of Pre-existing illnesses and Exclusions – Just like a normal health cover policy, even a top up cover can impose the restrictions on the pre-existing illnesses and exclude the diseases which they feel they do not want to cover. Also some top up covers might not cover pre and post hospitalization expenses. Some policies like Bajaj Allianz Extra Care provides continuity for already existing main policies. For instance, if you have a policy for 10 years with say New India Assurance, and you are buying a Top up from Bajaj Allianz, you will get continuity for the 10 years on the top-up and hence the waiting periods will not apply to you.

5. Tax benefits under Section 80D – You can get the tax benefit under sec 80D for the top up cover policies

6. Cashless facility would be difficult – I am not sure on this one, please guide! You need to follow the same cashless procedure, when your hospital bill exceeds the sum insured of main policy. If you are aware in advance about the high hospital bill, ensure you intimate at the time of admission itself.

Are you looking for extending your health insurance cover using a top up or a super topup cover ?

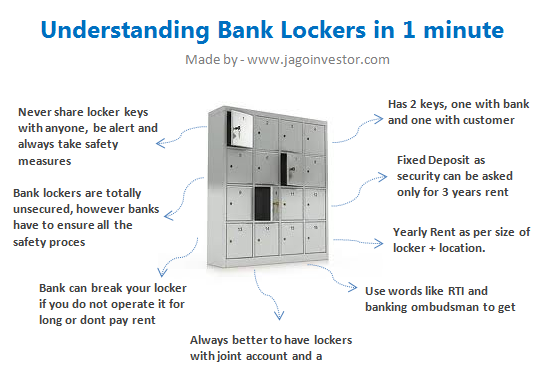

Today we are going to talk about “Bank Lockers” and how banks use unfair tactics by forcing customers to open a fixed deposit for a very large amount and that too for a long duration. It’s not uncommon to hear bank officials asking for fixed deposits of Rs 5-10 lacs in case you want to get a locker. That is just not allowed as per RBI and we will see what exactly the RBI guidelines say about it.

What is a Bank Locker and How does it work ?

Just like we have a saving bank account and fixed deposits to keep our money safely, we have “Safe Bank Lockers” to store our physical belongings like jewelry and various kind of important documents like WILL, Property Papers and other valuable items which you feel should not be kept at home.

There are always 2 keys for the locker, one key is with Bank and the other with the locker holder. The locker can only be opened when both the keys are used at the same time. Generally bank official applies the key and then leaves the locker room and only after he/she leaves, you should open the locker door and do what you wanted to do. The banks use very high quality, strong lockers (generally Godrej). So overall, this all makes sure that your locker is very safe.

Lockers are to be allotted on first come, first serve basis (as per rules) and in-case the lockers are exhausted, the bank is suppose to keep a waiting list of customers who have applied for the lockers and have to inform them when the lockers are free in the same order of application. If bank says that they do not have any lockers left at the moment, you can ask them for the “Waiting Register.”

Annual Rent for Bank Lockers and Security Fixed Deposit

Bank lockers come in different shape and sizes, which can be taken by customers depending on their requirement. For using the facility of lockers, you have to pay an annual rent which will vary depending on the size of the locker, the city (metro, urban, or rural). For most banks, the locker rent starts from Rs 750-1,000 per year and can go up to 5,000-10,000 for PSU banks and even 40,000-50,000 in case of Private banks (see the locker rates for bank for Baroda here) .

Is opening a Fixed Deposit mandatory for getting a Locker ?

Now lets discuss the biggest pain point of customers. Almost all of you might have faced this. When you go to open a bank locker, you are asked to open a Fixed Deposit for a large sum like 2-5 lacs for a long duration or asked to buy some policy (ULIP or Traditional Plan) saying that this is the rule for assigning the locker. However it’s just a plain lie and an unfair practice followed by Banks. A common man has no idea if the bank is correct or not and where to get the right information? So, I looked at RBI regulations on Banking and found out the exact rules.

And this is what I found – YES ! , Banks can ask for Fixed Deposits as security !

But, here is the catch ! .

As per RBI regulations, the bank can ask for a fixed deposit only to cover 3 yrs of locker rent and the breaking charges, not a rupee more than that and that too only from the new locker applicants, not old one’s already having a locker. Here is the RBI wordings from their notification

1.2 Fixed Deposit as Security for Lockers

Banks may face situations where the locker-hirer neither operates the locker nor pays rent. To ensure prompt payment of locker rent, banks may at the time of allotment, obtain a Fixed Deposit which would cover 3 years rent and the charges for breaking open the locker in case of an eventuality. However, banks should not insist on such Fixed Deposit from the existing locker-hirers.

To give you the proof one of the PSU banks – Bank of Baroda clearly mentions this fact on its website here

At the time of hiring the locker, bank will obtain a minimum-security deposit in the form of FDR from the lessee for the amount which would cover 3 years rent and the charges for breaking open the locker in case of such eventualities.

So, suppose you want to get a locker whose yearly rent is Rs 1,200 and the breaking charges for locker is say, Rs 100, then they can only insist on a Fixed deposit of Rs 3,700 (3 years rent + breaking charges); nothing more than that. Ergo, 3 years locker rent is going to be a very small amount, which almost anyone can afford, but banks lie to you and trick you by telling you to invest in a really large Fixed Deposit .You oblige for your own reasons. Banks do it to make sure they reach their monthly and yearly targets of acquiring new fixed deposits and selling useless policies like ULIPs and traditional plans (Note that banks are one of the channels for many companies to sell their products)

So next time you go to the bank for enquiring about lockers and bank officials don’t give you proper information, you can tell them about the rules and the notification from RBI. That should give some shock to the employees there and they might treat you a bit fairly. If still they do not budge, use the threat of RTI and banking ombudsman (and then actually use it)

Use RTI to resolve the Issue and Find Information

RTI is a powerful tool for a common man. We will see now, how you can use RTI against PSU banks. Next time when you go to a bank (I am referring to PSU banks here), tell them you want to have a locker (assuming you are having a saving bank account there already) .

When the bank staff tells you that they do not have any lockers available at the moment or try to impose some rules, you can tell them that you will find out things by filing an RTI application to the branch manager and also would quote his name in the RTI (stare on his name plate at the desk , he/she might be in horror). If they do not budge, then really go file a RTI after the incident. I would say better file a RTI before and once you get the reply from RTI, reach the bank with RTI reply letter itself.

When you file RTI letter, ask following things

How many lockers are installed in the branch ?

What is the size and volume of lockers and how many types ?

Rental amount per year for the Lockers ?

How many lockers are Unoccupied and available for allotment

How many people have requested for it and are on “waiting list” ?

What is your serial number in that waiting list (in-case you have applied for it) ?

Is there any requirement to make a Fixed Deposit for getting the Locker (YES/NO) ?

What is the amount of fixed deposit to be opened and what are the rules for it ?

In how many days a bank locker is allotted ?

Who is responsible to allot the bank locker in bank ? What is the name of the officer or designation ?

A weak person is always exploited in society, that’s the nature of life . When you appear as uninformed and too needy, anyone can take advantage of you, but when you appear as informed investor, who will not allow anyone to take advantage of his/her and who appears to be committed to be treated fairly, its tough for the other side to exploit then. Here is an instance on how Nikhil got the Locker facility with any FD at ING Vyasa Bank

I experienced a similar forced selling sometime back at ING bank. I wanted a locker and the Relationship manager said I need to make an FD of Rs. 100000/-. when I said NO. they said its a rule. I said there is no Rule book which mentions this. Rules are same for all banks and branches. the Relationship Manager stubbornly said ‘This is the rule of this branch’.

I just went to their website, found the no. of Chief compliance officer and spoke to the officer who helped me on this. After 2 hrs, I got a call from the same Branch of ING and they requested me to come to the branch and gave me a locker without any kind of FD!

Locker with Joint Accounts and Nomination

Just like saving bank accounts and fixed deposits, you can open a locker as joint account and with nomination facility, so that in case the demise or unavailability of the main locker holder, the joint holder can access the locker and operate it. Also in case the locker holders die (both joint holders), at-least there would be a nominee, who can get access to the locker by producing death certificate and filing up claim form.

There are tons of cases where locker was just owned by a single holder and when he died ,the family had to move mountains to finally get access to the locker. Worst, many families are not even aware about the existence of the locker and banks don’t take much interest in tracing down the locker family for many years (provided they have got the rent or have the fixed deposit linked to it).

Can bank open the Locker without your permission ?

In the worst case YES ! You need to operate your locker from time to time (at least 6 months to an year ideally.) Recently there have been cases when explosives and illegal things were found in lockers, which shows how lockers can be misused. When you are allotted a locker, there is proper KYC done by bank to make sure they know everything about you. They would place you in particular risk category like low, medium or high. If you are a high risk category person, you need to operate your locker at least once a year to make sure everything is fine. If you fail to operate your account for very long (depending on your risk profile), the bank will first remind you about the locker and will ask you reasons for not operating your locker. If you still do not take actions, the bank has all the rights to break your locker and give it to some one else, even if you are paying the yearly rent on time.

In case there is a genuine reason for not operating your locker for a very long time, you need to give it in writing to the bank mentioning the reason (like if you are now an NRI or if you are out of the city for a long time.) Also, if you fail to pay the yearly rent, they can break off the locker and re-allot it to someone else. Fair enough 🙂

Are bank lockers really safe ? Who is responsible if something goes wrong ?

Now this can be news to many, and a shocker, but in truth, Banks are not responsible for your bank lockers for any unforeseen events which is beyond the control of banks, provided they have done every due diligence from their side to protect it. You have to understand what exactly a locker facility is. The bank just gives out the space they have, on rent and make sure that its safe and secured professionally. They are suppose to make sure they have all the safety and security measures in place, to ensure that the lockers are safe and secure. So its more of a proprietor and a tenant relationship. In case there is a robbery (not in control of bank), Earthquake, Tsunami, Fire (which is not in control of bank) then bank is NOT responsible, or liable to compensate you.

Let me give you an example – If there is a robbery in the bank and your locker is one of the unlucky ones to get robbed, you lose it completely and the bank is not liable to compensate you for the reason that it wasn’t in their control to stop it, especially when they have all the security measures in place like a security guard, powerful lockers, CCTV cameras installed, and emergency alarms in place. The act of robbery is more of a unlucky event for them and you. (However there are some policies in market which insures the jewelery in your bank locker like this policy from Axis Bank). If you think that robberies in bank (with locker looted) do not happen in reality, I must tell you that it happens and has happened in past. Here is one such example.

Robbers recently broke into the strong room of a Punjab and Sind Bank branch in Jalandhar and emptied out 36 lockers in an incident that stands out as a grim reminder of the abysmally poor security infrastructure at financial facilities in the country. The incident is a reminder of a burglary at the Chirgaon branch of the Central Bank of India in Jhansi, Uttar Pradesh. As many as 45 lockers had been robbed in the November 2010 episode. (Link)

When you put your valuables in bank locker, the bank does not know what did you put in there, there is no record of it in writing with bank. That’s one reason, they can’t compensate you in case something happens to it (It could happen that you never had anything in locker and you can suddenly say that jewellery worth 10 lacs is missing! What’s the proof ?) However it does not entirely mean that banks are not liable to pay back or compensate the locker holders in every case!

Bank has to make sure they have done their side of safety measures and security

Bank is not responsible for your lockers only in case of those events which are totally not in control of bank and unavoidable, but only when they have done their share of work and security like I explained above. If banks fail to do their duty and then a robbery or some unforeseen event occurs, which results in your loss, then a customer can always claim that the bank is liable to compensate, because then the incident might have not happened or could have been avoided if banks did their part.

In another case, of Bank of India vs Kanak Choudhary, the customer had kept currency notes in locker which was eaten up by termites. Here the bank didn’t do their job of ensuring that the place is clean and safe. The customer was awarded the compensation.

Bank of India vs Kanak Choudhary

Here, the customer filed a case stating that termites had destroyed currency notes and important papers kept in her locker. The commission said that the bank “was bound to ensure that the respondents’ locker remained safe in all respects”, and awarded compensation to the customer.

Even in the robbery case shown above, the bank was found to be irresponsible and didn’t not do a lot of security measures, and definitively there was a chance of the robbery being unsuccessful if only bank had done their share of work, which means the locker holders would get compensation from bank, but then issue now is, how much compensation bank has to give and why when ? The matter would have gone to court and delays and frustration must have happened in that case.

But how much you can claim back from Bank ?

Not 100%, because you can never define how much you lost with 100% certainty. Banks themselves insure the lockers to deal with the loss in an extreme eventuality, so bank themselves get some compensation from wherever they have insured the lockers. So you can get some compensation from bank out the amount they themselves get, but to get back the compensation, you will have to show the receipts of the things which you claim was kept in the locker. Even in that case, you will not get 100% back, it will be some percentage, which can’t be defined. Also you can’t get back any compensation for the documents kept (as you cant define it’s value) and the currency notes if any. You can look at the youtube video above to see these points on claims you can get back.

While the risk is always there with bank lockers, note that this is an extreme eventuality. This information should be seen more of an awareness point, rather than a decision making criteria to choose or discard taking a bank locker. You don’t stop driving a car, just because there is a small chance of accident, right? In the same way, just because lockers are not 100% secured, does not mean you say that – “I will not go with bank lockers, because its not 100% safe.” Truly speaking it’s much safer than you bank almirah at least.

Some safety measures you should take for Bank Locker

You can never get rid of the complete risk, but you can ensure that you follow some best practices and common sense tips to make sure your bank locker is safe. Here are some good practice.

Always open your locker after the bank employee who accompanies you to the vault leaves the place.

Make sure your bank has all the necessary security measures, such as alarm system, iron-gated rooms, electronic surveillance via CCTV, etc.

Visit your locker frequently and ensure your valuables are safe. The RBI and banks expect frequent locker visits from customers.

Also, ensure the locker is properly locked before you leave the vault.

If possible, better have 2 lockers to diversify the risk (like one locker for valuables, and another for Documents)

If possible, always go with the bank where you have huge trust and comfort and its near your place, so that you can visit them often

Keep laminated documents in the locker, so that they are not damaged if you keep them for a very long tenure.

Always keep a record of what all you have in locker, so that in-case of eventuality, you can alteast find out what was lost and what was the worth

Demand a copy of the hire-purchase agreement for the locker so that the bank cannot ask for a higher rent in future

If a bank says the locker request is in the waiting list, ask for the waiting number

Demand a copy of the bank’s internal guidelines regarding lockers (their guidelines never mention fixed deposit as a mandatory condition)

I hope this articles has helped you understand almost everything about the bank lockers and how they work and different rules and regulations. Do you also have a bank locker ? Generally what all you keep their and how much do you trust your bank for the locker safety ?

Guys – It has been 5 years now spreading personal finance education through writing blog articles, writing books on personal finance, leading workshop in different cities. We started very small and have reached so far only because of your trust and partnership. Every day we (I and Nandish) wake-up with one thought in our mind “How can we help people to live an awesome financial life?”

It’s time to look at what is exactly happening in your financial life?

I’ve always been fascinated by Socrates’ bold statement that “The unexamined life is not worth living.” The statement holds a lot of value and meaning in it, it has acted like a wake-up call to me. I examine my financial life every year very closely and my personal finance actions.I want you also to examine your financial life and your actions. Look at what is going on in your financial life, How many articles you marked as important but you never found time to read them, How many personal finance actions you have been procrastinating, how many times you told yourself it’s high time I need to get serious as an investor. Get honest with yourself as that is the first requirement to be a part of personal finance action revolution.

You are committed but then why you are not able to take actions?

It is not that you are not committed but as life is dynamic you are always surrounded by multiple responsibilities in life. You play different roles in life and one of the role you play is of an investor. One of the thing we have found to be missing is a STRUCTURE. Yes, to move from point A to Point B you need a structure without that you will not be able to become effective. We have created a wonderful personal finance structure for you that will help you, motivate you and empower you to take actions in your financial life. It will not help you to complete 10, 20 or 50 actions but it will help you to complete 100 money actions in your financial life.

In our experience Personal finance is NOT about knowing things, it is about getting things done !

A lot of people think they need to have a lot of knowledge to take actions in their financial life. Because of this they start to expand their knowledge domain, they start subscribing on different websites and blogs, start to buy different books but eventually due to lack of structure they are not able to take required actions in their financial life. 100 money actions program is about getting things done, it is about expanding your action domain and it is about breaking your habit of procrastination.

What Existing Users are Saying about 100moneyactions.com

100MoneyActions is a real boon for people like me who are charged up and convinced to improve their financial life and take it to next level. Thanks to Jagoinvestor’s prolific pioneers Manish Chauhan and Nandish Desai for launching such a beautiful concept that is filled of actions. I have started recently with this program and I can sense the positivity that it has started to bring in, in my financial life. 100MoneyActions provides an excellent structure that is built on top of one critical thing “ACTION” and not just actions but “CORRECT POWERFUL ACTIONS”.

I believe that if I take all those 100 actions (believe me it is not as easy as you can read it ) my financial life will move from where it is now towards positivity. I believe that 100MoneyActions will bring in structure and actions that is missing in my financial life. And I wish that it will do the same to many more like me! Big thanks to this concept and all the best to the program/concept. I am sure it will be a great success.

Prasad Kulkarni

IT Professional

Pune

100 money actions is one of the best thing that has happened to me. This is one program which I am following very religiously over the last 2 weeks. After reading so much on Jagoinvestor blog I used to think that my all fandas related to investment instruments, finance management etc are in place but still I was not sure if I am doing everything right or I am taking enough actions to put the plan on track. This program is helping me in structuring my thoughts, making me aware about the smallest of gaps, consolidating literally everything.

Today I am using the sheets of this program extensively to track the progress of my actions which I am supposed to do within the defined timelines. While your blog and its articles are very informative and in plain English for a layman, this program is a next step to identify, structure and follow the actions which you always want to take. I am so thankful that I came in contact with you guys. Thanks Manish & Nandish. Cheers!

Anuj Gupta

IT Professional, Microsoft

Delhi & NCR

What you get on JOINING this ACTION REVOLUTION ?

PLEDGE Sheet (Your commitment with yourself)

100 Investigative Questionnaire (GAP Analysis)

Well designed ACTION document that helps you to complete 100 actions

Ready Reckoner List of Financial Products

Simple Structure to complete 100 money actions

Supporting Audio Files

Personal Finance Tools and templates where required

Useful Ebooks, Study material and resources for support

What it takes to be a part of this ACTION REVOLUTION ?

It takes commitment to be a part of this ACTION Revolution. You will have to trust the structure of this program. If you can make a commitment you will complete all 100 actions you can be a part of this revolution. Anything free has no value so it calls for a small financial commitment to be a part of this program.

Visit 100 money actions website and get more idea on how you can be a part of this personal finance action revolution. From the bottom of our heart we invite you to be a part of this ACTION REVOLUTION. Once you complete these 100 actions in your financial life, your financial life will not be the same and THAT IS OUR PROMISE TO YOU.

Now, anything free has no value so we decided to keep a small fee to be a part of this action revolution which is Rs. 1999/- only.( This fee is to generate commitment in you). Don’t let your concerns get in your way, don’t let the conversation of money get in your way as your Financial life is Priceless. Paying Rs 1,999 will not make you bankrupt but not taking actions will surely lead you to bankruptcy

Are you scared of using your credit card online on some website because you feel there might be fraud or a security threat? If that’s the case, then welcome to the world of Virtual credit cards, which I will explain in today’s article and also how it can be useful for you.

A virtual credit card (VCC) is an add-on credit card issued on your primary credit card; only it’s virtual and does not have any plastic existence. You can instantly create it, using your net-banking facility by providing your credit card or debit card details. All relevant details like the card number, the ‘VALID FROM’ date, the expiry date and the CVV number are visible online to you and this virtual credit card enables you to transact online with a credit limit of your choice. Also the virtual card does not have any fee associated with it and comes for FREE!

The key details of your VCC like the card number, expiry date etc. are used when you transact online, but your primary card details are never shared with the merchant online, so you never have to be worried about losing your card or having to carry it ‘safely’ in your wallet. There are tons of banks which offer these instant virtual cards these days. Some of them are

ICICI VCC

HDFC NetSafe

Kotak netc@rd

SBI-Virtual Card

Axis Bank e-wallet card

Validity of the virtual card ?

The virtual credit card is valid only for a single use and automatically expires within 24 hours if the virtual credit card is not used, which means that the chances of credit card fraud or misuse are significantly lower than a real credit card. Also understand the if you hold a VISA card, then the virtual card which you will get will be VISA one and if it’s Master Card, then it’s going to obviously be a Master card.

Is virtual Credit Card only for Online Use ?

Yes, as a virtual credit card is not a physical card, it can be used only for online transactions, for which all you need is credit card number, CVV number and Expiry number. Once used the card expires and can’t be used again. If you want to execute another transaction, you will have to generate another virtual card. The maximum limit of your virtual credit card can be as high as your actual limit on the real credit card. When you make the payment on some website using your virtual card, it will appear on your physical credit card statement itself.

Most of the banks issue a card which is valid internationally and you can use them on the websites outside India, however some banks like SBI bank still issue virtual credit cards which are not valid outside India. You will have to check with your bank if it is valid internationally or not.

Can you create Virtual Credit Cards using a Debit Card?

The answer is Yes for most banks. Even if you just have a debit card and not a real credit card (Check out the best credit card in India as per our survey), you can still use your debit card to create a virtual card. There are many people who want to transact online at times, but do not hold a credit card. Now they can create a VCC and use that to transact online. However I just checked my ICICI account and when I want to create a virtual credit card, it asks for my credit card number, so it seems like ICICI bank doesn’t allow VCC creation via a debit card. Anybody created one using debit card in ICICI bank? Let us know!

Real Life Situations when you can use Virtual Credit Card ?

When you are transacting on a website, where you do not feel very confident about security, but still you have to transact anyways due to some reason. Check out this fraud

When any friend of yours ask you for your credit card, where you want to “NO” , but still can’t say NO. You can now create a virtual credit card and give the details to him.

When you do not have a real credit card, but only have a net-banking facility, you can still create virtual credit cards and use them.

You can also use these virtual cards where you just want to try out the service , but by default the website starts charging the card on renewal basis. If you use virtual card, it will anyways get cancelled after one use and there will be no renewal charges later – Here is a real experience.

Do you feel virtual credit cards to be of any use in your life? Are you already using virtual credit card or planning to use them? Please share it with others!

A lot of investors still do not understand what is the meaning of TDS (Tax Deducted at source) is and how it’s related to their taxation.

While the concept is very easy overall, I have seen that tons of investors still get confused when TDS is cut on their Fixed Deposits at maturity and they feel that they don’t need to pay any tax now, or feel that they don’t have to pay any tax on their Fixed Deposit interest just because it was below 10,000 and TDS was not cut.

So in this article, let me make sure that you are 100% clear about Tax Deduction at Source and what it means.

What is Tax Deducted at Source?

TDS or Tax Deducted at Source is a tax collection mechanism by Government of India, where at the time of transaction itself, the tax is deducted by the paying party and directly deposited to the income tax department.

It’s assumed that the receiving party (one who gets the money) will have some tax liability. Now at the end of the year when you find out your tax liability, the TDS amount is the tax you have already paid and now you need only pay the balance amount.

So in a way, Tax Deduction at Source is a good thing for 2 reasons. You automatically pay a part of your tax liability and income tax department receives their tax collection. So TDS is always a mechanism, to reduce tax theft. Let me give you some very simple examples of TDS collections

Example 1 – Tax Deduction Source cut by Employer

When a company pays salary to employees, you must have seen that they pay the salaries after cutting the tax amount.

So at the start of the year itself, after the employee declares his 80C investments, HRA, LTA and other tax deductions which he will avail, the employer ‘estimates’ what will be the tax outgo of the employee and then each month they cut a certain amount as tax and pay directly to the income tax department.

And then at the end, the employee calculates his actual income tax liability to be paid. If the Tax Liability is more than TDS cut, he pays rest of the tax money and files the returns. If the Tax to be paid is less than the TDS amount, in that case he can claim for a refund in the tax returns.

Example 2 – TDS cut by Banks on Fixed Deposits

When you open a Fixed Deposit, you earn some interest in a year. Now the rule is that if the interest amount each year exceeds Rs 10,000 on your fixed deposits (across the different branches of the same bank also), the TDS has to be deducted by the bank.

Now a lot of people confuse this by paying the tax. The rule is that any amount you earn as interest is taxable. Even if the interest is Rs 100 or Rs 1000, you still need to pay the tax on that amount. Just that if the interest exceeds Rs 10,000, the bank will cut the tax directly and pay the tax to govt.

That will make sure that you pay your tax in advance itself (you know how difficult it is to pay tax when you have finished that money at the end). Note that TDS is also applicable in case of Sweep in Accounts and MODs (Multi option Deposit Scheme by SBI)

What about NRI Fixed Deposits?

In case of NRIs, the sad part for them is that there Tax Deducted at Source is cut @30% on any interest income earned on NRO fixed deposits (no limit of Rs 10,000 interest.)

Even if they earn Rs 1,000 as interest, they still pay TDS @30%. Note that the Fixed Deposits in NRE and FCNR accounts are totally tax-free in India, hence no Tax or TDS. A lot of NRIs send money back to India and invest in Fixed Deposits in their NRO account.

If they have to pay tax at the end, well and good, else they need to file the tax returns and claim it back. NRI’s should read this article on TDS applicability in economic times and also read this article to understand how NRI’s can claim exemption on TDS is applicable for you.

If you want to know more about the tax applicable on NRE, NRO and FCNR account then watch this video:

Make sure you quote your PAN

A lot of times, PAN card number is asked by banks or at other places before the payment is made to you. Do you know that there is a reason for it? If there are any TDS to be cut, they first check if PAN number of the receiving party is available or not.

If PAN number was given by the party, then the TDS is cut at a lower rate, but if PAN number is not quoted, then TDS cut is high.

For example, in the same Fixed Deposit amount, do you know that the TDS is cut @10% if PAN number is given, but if PAN is missing, then its 20% Tax Deducted at Source? These are the numbers of individuals (not companies, LLPs or corporate bodies.)

You should also know that in this budget Tax Deducted at Source @1% is to be cut for any real estate transaction above 50 lacs!

I want to invest where TDS is not applicable

A lot of investors try to invest in bonds, securities or at those places where TDS will not be cut. They do not understand that TDS is nothing but paying tax in a different way. I assume that they thought that if TDS is not cut, they don’t have to pay any tax, which is totally wrong.

All they are doing is taking the onus on themselves to pay the tax at the end. Or many might be finding ways to save the tax by various means suggested by their CAs.

A lot of investors also try to open a lot of small FDs and break it in the same bank but in different branches or in different banks too, but they do not know, that in this era of core banking, banks and tax officials can just punch your PAN numbers (yes, my CA told me this) and get all your tax-kundali and how much fixed deposits you have and how much interest you earned out of your investments.

So you need to pay your tax on those amounts anyway, whether TDS was cut or not. If TDS was cut, in a way it’s better because you pay the tax in advance itself and don’t have to arrange for tax amount at the end of the year. It really pinches at the year-end to arrange money and see it go into tax!

Make sure you ask for TDS certificates

Whoever cuts the TDS and pays it to income tax department has to issue you TDS certificates as the proof that you have paid the TDS. The document they give you is called the ‘TDS certificate.’ You would need this document if you want to show that the TDS amount is being adjusted in your tax payment.

Generally, as a rule, all the parties send the TDS certificates to you, but make sure you are proactive in asking’ it from them.

Myth: I don’t have to pay any tax if TDS is deducted

At a lot of times, it so happens that you don’t have to pay any tax at the end of the year and you already know it, but just because your deposits are earning more than Rs 10,000 of interest income, the bank cuts the TDS amount and then you have to claim it back by filing a return.

Case 1 – If Tax payable (TP) is more than TDS

In this case, if yearly TP is more than the TDS then the investor will have to pay the remaining amount left after deduction i.e TP – TDS = Remaining Tax Payable.

Case 2 – If Tax Payable (TP) is less than TDS

In this case, If yearly TP is less than the TDS then the investor will have to file for tax return because the tax which he was supposed to pay was less than the deducted tax.

Case 3 – If Tax Payable (TP) = TDS

In this case, if TP is equal to TDS then the investor will not have to pay any extra tax because the tax is already paid. However the investor will have to file for ITR toi show that he has paid the interest and is not liable to pay anymore tax.

All those people can simply submit Form 15G/15H to bank (each year) and then the bank will not cut the TDS (my father in law told me how Bank of Maharashtra guys in some particular branch still cut the TDS even if you deposit the Form 15G/H and how they are such a pain).

TDS tip – for salaried investors

Let me share with you a little tip which a lot of you might know already, but it will surely help new people. If you are a salaried employee, your employer must be deducting the tax each month already and you know that you don’t have to pay any tax at the end.

But now if suppose you already have made some fixed deposits or some investments, where the Tax was deducted, then you have already paid some part of tax liability.

Your employer is not aware that you have already paid some tax through TDS route. So in the Jan-Feb season when they finally ask for your investment proofs, you need to also give them form 192 and deposit the TDS certificates to your employer so that he can adjust the Tax paid and pay you back the extra amount. (March month salary is generally higher due to this money coming back and also because of HRA/LTA reimbursements).

Got a term plan for your family? Or may be you’re planning to take the term plan in a few days. If you are, good for you! . One of the biggest questions, every person considering term insurance has, is – “Should I take the cover for the maximum period?” . This is exactly what Chetan also asked on our questions and answers forum

Aegon provides coverage upto 75 years of age. or 20 25 30 35 40 years. I am confused which policy term is better to get maximum benefits?

Just like him, hundreds of investors have asked me this question over and over again, and I tell them, “Just take it only until you reach 60 years of age.”

And they happily ignore my suggestion; as if I am crazy, suggesting this to them. The “Insurance only till 60 years” looks kooky to them – kind of a “wrong deal” and they want to get “maximum benefit” out of the term plan. “The chances of my family receiving the claim amount is higher when I am covered for long” is the common thought process of every person who is in the mad rush of buying the highest possible tenure.

Trust me, that’s flawed thinking and I will explain why today. More than a sermon, think of this article as a discussion, where I put some points in front of you and you reflect and ask yourself – “Does it really make sense? or not?” and then make your own decision. So here are those 5 reasons on – why you should not take Insurance till the age of 75 years or more

1. You don’t need it beyond your working life

You really need to ask yourself the question – “Why am I taking Life Insurance?” and the answer is – “Because right now, I don’t have enough net worth, which will help my family if I am gone” or in other words – “Because my family is financially dependent on me.”

For a person who is not earning and does not bring money home, his death will cause family only emotional loss; not financial loss. Hence, logically you need to cover yourself through a life insurance product, only for the time you are working and others are financially dependent on you.

2. You will have “probably” have enough wealth by the time you retire anyway

Stretching the 1st point, if you are taking life insurance cover until you are 70-75 years, will you really need it at that time? Do you really feel that you will have any reason to have a cover of 1 crore that time (after 30-40 years?) . I am sure (more confident than you), that you would have completed all your financial goals by that time, you will have your own home by that time and you will have done everything in your life by that time. You focus area at that old age will be very different than what you focus on right now.

To understand this point, you have to stop for a moment and go into 2040-50; when you are retired and close to the heaven’s door. Are your children really financially dependent on your income – which does not exist? Is your spouse dependent on your income? You must have already accumulated enough wealth by that time and you must be getting some income out of that. Your death has nothing to do with family cash flows at the time.

3. The premium factors in your tenure already

Most of the people who feel that they are smart enough to take term plan till 75 years, forget that on the other side is a professional business running for decades now. They have hired people who are 10 times smarter, who design products (they are called Actuaries) that generate large profits for companies and not investors. Life Insurance is a “for-profit” business. They design things, so that they earn profit. If a company allows you to take a plan that lasts until you turn 75, why have they done that? Why did they allow that to happen? The premiums they charge already factor in everything. You pay premiums to get that term plan, it does not come free!

4. You will live longer – and they already know that.

Like I said in my last point, companies are “for-profit” businesses. They will not issue you a policy if your chances of living beyond 75 is not high. If you are a healthy person, already earning well, have access to good health care, what are the chances you will live beyond 75 years of age? Extremely high, that’s what!

Look around you – Are people dying early on average? No, you see people living beyond 80-85 already and here we are talking about your future which is 30-40 years away, when the average life expectancy of an average person in India would be closer to 73-76 years anyway (as per projections by govt studies.)

Now just imagine this … Compared to the 1.25 billion people in our country, are you in top 25% or lower?

Which means that you have much much better prospects to live beyond 80-85 years. Which brings me to another point, that you should seriously worry about about your retirement planning a lot more than the less important question of insurance beyond 70-75 years.

Even when we do financial planning for our clients, we make sure that we plan for their retirement beyond 85 years and have them covered only till 60 yrs or even lower if they feel they will retire earlier. The important point to understand here is that, a life insurance coverage is just a support for your family in your early life when you are making money, your financial replacement, if you will. So when a life insurance company issues you a term plan until 75 years, it’s not you who are smart, but the company! They know, with a really high degree of probability, you will keep paying the premiums till 75 years.

It’s all chance. Yes, there will be people who will die before they reach 75 years of age and yes, their family will get a lot of money, but it really is just the game of chances … Companies make profits because of those who will live beyond 75 years and not by those who die before that.

5. The value of your sum assured is peanuts later

I hear it most of the time – “I am taking the term plan till 75 years, so that even if I die, my family will get the money. So, the higher the tenure, higher the chances of making money.” But they forget that by doing so, they are actually helping the insurance guys make profit, but lets say you die at 70 years. Celebrations! Your family will get that 1 crore, which at this moment sounds good, but will not be worth a lot that time.

Let me show you the mirror that lets you look into the future 🙂

Let’s say you are a 30 year old guy, and your monthly expenses are 40k per month. You say to yourself, “Let me take that term plan worth 1 crore so that in case, I die my family can get 1 crore which will provide them some good monthly income.”

It would be very good number if you die early in your life! . With each passing year that 1 crore will be worth less. If you die the next year of taking the term plan, the worth of that 1 crore is pretty much same, 1 crore. But if you die after 10 yrs, that 1 crore will be worth 50 lacs in today’s world. So getting 1 crore after 10 yrs is same as getting 50 lacs right now. Are you getting my point? The money you get in term plan is a constant number, not linked to inflation!

So imagine you have taken the term plan till 75 years and you die at 70 (after 40 yrs of taking the term plan), what is the worth of that same 1 crore at that time? Hold your breath! It’ll not more than 6-7 lacs assuming a inflation of 7% and even if inflation for next 40 yrs is a small 5%, it would not be worth 15 lacs today! . So when your family gets that 1 crore after 40 yrs, it’s kind of worthless. No one would be depending on that money anyway; it’s just a bonus on your children’s inheritance money!

Act like a real informed and smart investor

I have been seeing this madness for many months now and was constantly wondering why people are focusing so much on this small thing called “long tenure” in the term plan. I see investors abandoning one insurance company for another just because the other company is offering a term plan till 75 years.

You are allowing yourself to fall into a trap if you do this. If you have already taken the term plan till 75 years, do not worry … do not cancel it, just let it run it’s course. Stop paying premiums when you feel that your family can be taken care of, by the wealth you have generated. If you are planning to take a term plan right now, take it for as long as it takes you to retire, probably till 55 to 60 years, but not beyond that.

Would be happy to hear your thoughts and your views on this topic! . You have taken the term plan for very high tenure ! .

Starting July 1, 2013 , EPF account holders will be able to withdraw or transfer their EPF accounts from one employer to another employer online. EPFO has said that they are working on setting up a central clearance house which will be operational from July 1, 2013 . One of the major problems faced by employees is to transfer their EPF accounts from one company to another when they change their jobs or to withdraw their EPF accounts after leaving their job, which takes years and months, without them having any transparency in the system and process. They are frustrated, lost and have no idea where to ask for their EPF status and to whom . Because of this delay, a lot of people just let things go and the matter drags for years and years

You can also Track the Status Online

The best part is that you will be able to track your request online and will be able to see which stage your EPF withdrawal or transfer is ! .

Permanent EPF account number for each person

EPFO has earlier said that they are working on the permanent EPF account number where a employee once allotted a EPF account number will be able to use the same Employee provident fund number when he/she moves to another employer. The new employer will deposit the provident fund money in the same permanent account number. This will solve a lot of issues, but this would be possible only after 1-2 yrs , the first focus is on introducing a online withdrawal or transfer service.

Verification of Details after the request is put ?

Once you apply for withdrawal or transfer, the verification of all the details from employer will be done by EPFO . All you would have to do is just initiate the transfer or withdrawal request online (Its not clear how it will happen or what you need to exactly do). After that EPFO department will take charge and do their part of work by contacting the employer. Here is how the transfer would work