A lot of investors wonder how the real estate prices go up and down (do they?) over years. A very big role in the movement of real estate prices is played by something called “ready reckoner rates” . Ready reckoner rates for each area in the city are defined by the state govt. Let us understand this thing in detail.

what is ready reckoner rates

Ready Reckoner rates are the prices of land, residential properties, and commercial properties for any given area defined and published by govt each year. It’s revised from time to time whenever govt feels that there is a need for prices revision. Stamp duty and registration costs that are paid by a real estate buyer cant be below this ready reckoner price or the actual price of the property.

For example – Let’s say that ready reckoner rates for some location is set at Rs 4,000 per sq ft (as per state govt) and the cost of the property as per that comes at Rs 40 lacs. Now imagine that the builder is quoting the cost of the property to you at Rs 50 lacs. Now the stamp duty will be paid on Rs 50 lacs only because its higher than Rs 40 lacs. However – suppose you decide to pay Rs 20 lacs in black and only Rs 30 lacs in white money, still, your registration & stamp duty will be paid on Rs 40 lacs costs because that’s the minimum pricing set by govt itself.

Ready Reckoner rates are linked to Built-up Area

Note that the ready reckoner rates are linked to the Built-up area of the property, not carpet area or super built-up area. So if ready reckoner rate is Rs 4,000 sq/ft and builder tells you that he will also sell the property to you at Rs 4,000 sq/ft, don’t get fooled!, because builder tells you the pricing linked with super built up area and not built up area, which in most of the cases is higher, so eventually the rate charged by builder is always higher, if you convert it for the built-up area. Just for example if super built up area is 1,000 sq/ft and built up area is 800 sq/ft, then Rs 4,000 per sq/ft area quoted for super built-up area (Rs 40 lacs cost), is same as Rs 5,000 sq/ft quoted for built up area (same Rs 40 lacs) .

Just to make sure you understand the terminologies –

Carpet area – A Net usable area of the property (imagine you put carpet, what all part of flat, it will cover)

Built-up area – Carpet area + walls and doors area (imagine you remove the thick walls and all doors, then what you will be left with)

Super built-up area – Built-up area (which you get) + everything from the staircase, garden, gym, swimming pool and everything you use (your proportion)

How ready reckoner rates affect the prices of real estate

Now – It’s very clear, that ready reckoner price is the FAIR PRICE (which is fair value) set by govt itself. Now builders can charge the premium on that fair price depending on market condition, demand, quality and their goodwill and their exploitation power :). So the market price (the actual prices prevailing in the market), will definitely be always higher than ready reckoner prices (benchmark). Now if the benchmark itself is higher at any given point of time and also keeps increasing over years, the market price quoted by builders will also be high.

Example – Just to give you an example, in one of the areas called “Kondhwa” in Pune, the ready reckoner price set by govt is around Rs 3,700 per sq/ft, however, the builders are charging anywhere from Rs 4,500 to 6,500 per sq/ft at the moment. Imagine if this year govt increases it to 4,000, then automatically the rates will go up by that much margin because builders get a good reason to escalate the cost.

One of the largest revenue sources of any state govt is the stamp duty from property registrations and it’s always in state govt interest(from a revenue point of view) to keep the ready reckoner rates higher or increase it if there is any justification for it, live development done, roads constructed, etc…

Where to find the Ready reckoner rates for your area?

Now, you cant control the actual price you have to pay to a builder, but it’s a good idea to check out the ready reckoner rates of the area, where you are thinking of buying the property. Now there are few ways you can find out the ready reckoner rates of your area (or any area). Here are a few of them, some easy and some tough.

1. On the website of “Registration and Stamp Duty Department”

Each state govt has its own department of “Registration and Stamp Duty”. You can reach the website by searching the sentence “Registration and Stamp duty department” and adding state name along with it on google. Like if you want to find out the website for Maharashtra search for “Registration and Stamp Duty Maharashtra” (direct link) and the first link you get it “igrmaharashtra.gov.in/”. On the website, you need to search for a link – which says something like “market rates” or some equivalent in the local language of the state. If you are lucky, you might reach the final page which helps you find out the ready reckoner rates for all the cities in the state. It will help you find the rates as per city, taluka, location or survey number. I tried this trick and was able to find out the websites links for 3 states

Andhra Pradesh (for Hyderabad) – Direct Link

Note – The rates might be displayed in per sq yard, per sq meter etc, so better change them to per sq feet and also make sure you use IE or Firefox to access the websites because they still don’t know chrome exists!

2. Using RTI application

The second way to find out the rates is to use the RTI application against the same Registration and Stamp Duty department (many times called “revenue department” like in Delhi). All you need to do is file an RTI to the respective officer and to your jurisdiction asking for the rates in a particular city and area. You can take help of this article to understand the format and procedure

3. Office of Sub-registrar

One of the best ways would be to go to the sub-registrar office (where the properties are registered) and find out the rates from there itself. If you do not find the support of the staff there, don’t forget to mention words like RTI, CIC and “One of my friend works in Media” and they should accept doing some work for you.

4. From the newspapers

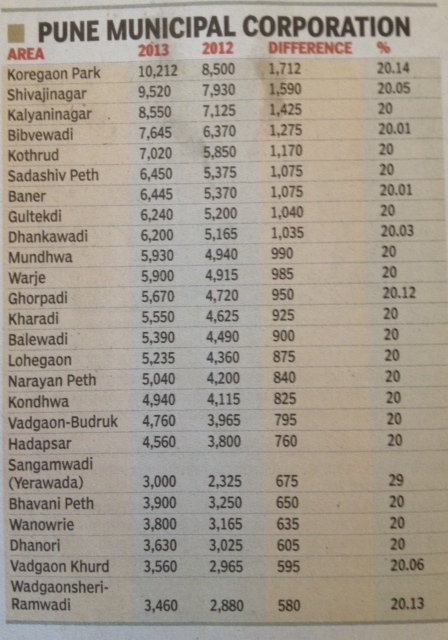

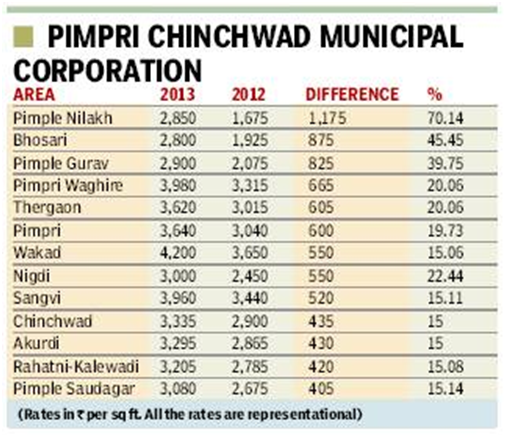

All the newspapers keep on publishing these rates from time to time. Just keep an eye on real estate section from time to time and you should be able to get some info. Below I am attaching some snapshots I got from the Internet for the revised rates in the year 2013 from 2012.

No Ready Reckoner rates for rentals

There are ready reckoner rates for buying the properties, but there are no ready reckoner rates for rentals. It would be amazing if govt comes up with that too, it would then help us to understand which area is doing better then others and how much premium home owners are asking for over govt defined rental rates.

Overall what do you think about ready reckoner rates and does it helps the overall industry or goes against it? Please put your comments!

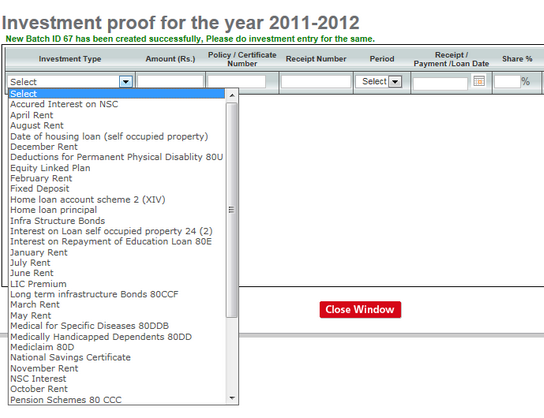

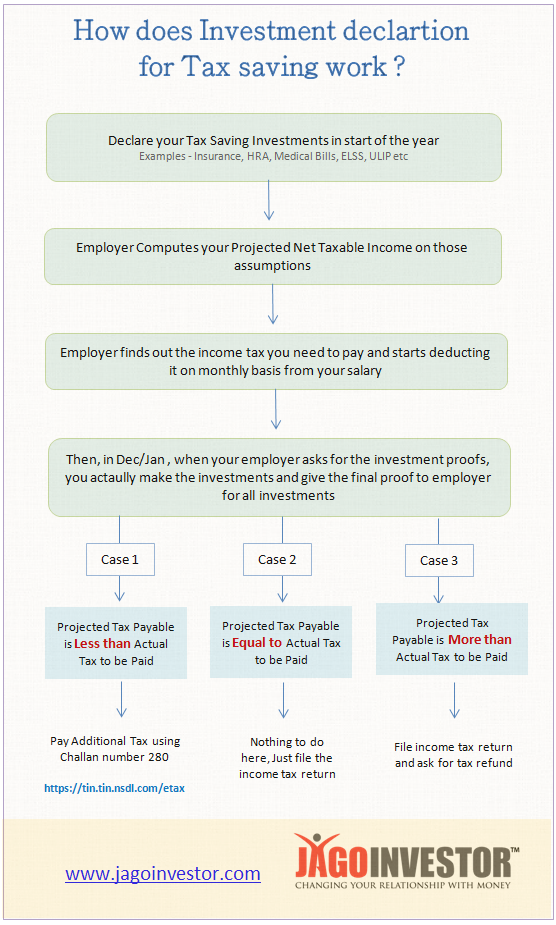

Every year, when the new financial year starts, employers ask their employees to declare their investments and give an idea about where will they invest to save the tax. There is a page on the companies’ websites, where each employee has to declare their investments. Come of the examples of the target options are life insurance premiums, ELSS investments, Rent, Ulips and home loan-related numbers.

Why do employers ask for this investment declaration?

The employer asks for this information because they want to approximate how much will be your final taxable income (after deducting the tax saved through 80C investments, HRA, Home loan and medical bills. So that they can cut a constant amount of TDS each month.

A lot of employees get a bit tensed thinking, what exactly they should mention while declaring the investments. They feel that at the end of the year, they will have to invest exactly in the same order in which they declared. However, this is not correct. All you need to do is invest the same amount declared at the start of the year into any tax-saving investments option.

For example – If you had declared that you will invest Rs 50,000 in LIC policy and Rs 30,000 in Tax saving mutual funds (ELSS). The total is Rs 80,000. Now your employer will deduct Rs 80,000 from your projected income for the year and arrive at net taxable income and find out how much is the tax you need to pay at the end of the year (projected). Now he will just divide it by 12, and find out the monthly number and start cutting that much tax each month from your salary.

Now when the month of Dec/Jan arrives, your employer asks you for investments proof. Now when you actually give it to them, they recalculate things and see if things are matching with what you declared at the start of the year or not.

There can be 3 scenarios here.

Case 1 – Amount Actually Invested Less than Amount declared in the start

In-case you were not able to invest up to the amount you declared, or you were not able to submit the documents to your employer on time, it means your employer will assume that you will not be able to do so, and that means that they have over estimated your tax saving and the tax paid by employer is lesser (because you owe more tax, due to less tax-saving investments) . In which case, the employer will recalculate your tax liability and now will adjust it with the next 1-2 month salary (Feb/Mar). Which means you get less salary in the last 1-2 months.

But, If you are able to finally invest for tax saving, then at the time of tax filing you need to declare it and ask for a tax refund from the IT department. It’s always a good idea if you can avoid this situation because then it takes a lot of time to get back your refund.

If for some reason, your employer does not cut the tax from your last month’s salary, then you directly owe the tax to govt. This can also happen if you have any other income source, which is not accounted for by the employer, in that case, you need to pay the tax to govt directly. You can do it online using Challan 280 on the IT department website. Then at the end of the year, you can file the returns.

Case 2 – Amount Actually Invested = Amount declared in the start

If you invest the same amount as declared at the start of the financial year, it means that your taxable income would be almost same as computed by your employer and the amount of tax you paid was equal to what you owe to the income tax department. In this case, there is nothing much you need to do. just file the ITR at the end of the year and everything should be pretty smooth unless you have income from other sources.

Case 3 – Amount Actually Invested More than Amount declared

It might happen that you declared only Rs 50,000 investments, but finally invested Rs 1,00,000 into tax-saving instruments, which means you saved more tax. However, your employer has been deducting the tax assuming your declaration for Rs 50,000 only, which means the employer was paying more tax to govt on your behalf. Now, this means you are entitled to get a tax refund and you can ask for it when you file the returns. Generally, it’s a good idea to declare the maximum possible investments in the start, let your employer assume you will do maximum tax saving (so that less tax is paid), and then make sure you actually invest the promised amount. In the worst case, if you fail to do so, better pay the tax at the end of the year or get less salary (be prepared for it)

This article from Bemoneyaware talks about this topic in much detail. Did you get clarity about investment proofs for your employer? Do you have any questions?

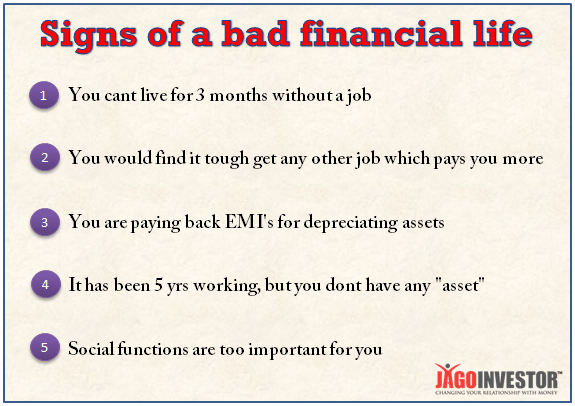

Is your financial life going well? Are you on the growth path or on the verge of disaster very soon? Your financial life might be in trouble, but maybe there is some more time left before you really take charge of your financial life and really do something about it, else it will crumble and you will be destroyed beyond recovery.

I see lots of people who are not in agreement with the fact that their financial life sucks and they really need to take giant leaps. Somewhere they are comfortable with the whole situation and keep expecting that “somehow” their financial life will improve. So, I am giving you 5 simple indicators, which you can look at and decide if you are headed towards financial disaster or not. The more these indicators are true for your financial life, the bigger is the problem and you need to get really serious about it. If none of these indicators are true for you, then congratulations! , you are mostly in a good situation.

Sign 1 – You cant live for 3 months without a job

The first and the biggest sign of disastrous financial life is that you cant live for a few months if you do not bring money on the table through your job or business. If you have been earning for a few years now, you should at least have a year’s worth of income saved with you, but that’s not the case with many people. Their monthly expenses make sure they are left with nothing at the end of the month. Worse, many people have the negative cash-flow and they are piling up debt each month to survive. These people are mostly dependent on credit cards and keep using them whenever they are in a “crisis” situation. The credit card should be held for benefits + reward points and not because of its a survival tool for you.

Ask yourself, how many months’ salary have you drawn to date in last so many years and how many worths of salary you have saved till now? If you cant survive for more than 3 months (or 4-6 months), you are in big trouble. I asked this same question on my facebook wall a few weeks back and I got responses like “6 months”, “3 months”, “10 yrs” and all kinds of numbers. So better look at your number of months. Do not focus on income alone, because income is not the same as wealth.

Sign 2 – You find it tough to get a higher paying job

Your job/business is the means to bring money to the table each month. Every year or in few years, ideally you should be able to move one ladder up and command a high salary because over the years you will gain experience, add new skills and would be wiser/knowledgeable. However, if you cant move upwards in your professional life, the amount of money you will bring back home will not increase and if that’s the case, you are in trouble.

Ask yourself– Do you see yourself earning 10X of your current salary someday in the future like the next 5-10-15 yrs or not? Are you dead scared of losing your job and never be able to find another? Do you feel that you have reached a level in your professional life, where if you lose your current job, you will find it tough to get the same salary job somewhere else?

If that sounds your case, you are in trouble financially because your biggest asset is your earning capability and not your this year’s pay package only? If it sounds your story, its time to find out how you can increase your skills and take better jobs in coming times, don’t wait for the last moment, it takes few years to hone your skills!.

Sign 3 – You are paying back EMI’s for depreciating assets

There is two kind of debt – good debt and bad debt. Any debt which helps you build assets and grows in value over time is better (I am not saying, go for it, but it’s just better than the bad debt). The bad debt is mainly the debt which is used for CONSUMPTION purpose. You use it and its gone. Examples are personal loans, consumer durable loans, credit card debt or even a car loan(especially the car, which you really don’t need, you can do with a two-wheeler, I am not talking about the car which is really required and can’t live without), then you are paying an outsider on a regular basis, without building any assets for yourself.

It’s like – you are doing the job to help others squeeze money out of you. If you are doing this, better stop it now and see how you can change your direction, you still might have the time to come back on track.

Sign 4 – It has been 5 yrs working, but you have nothing worth called “ASSETS”

You have worked for 5 yrs in the job, now even if you had saved 2 months’ worth of salary each year, you must have had 10 months’ worth of salary with you saved today? Is it there? You must be having some investments in Fixed Deposits, or some gold, or some mutual funds or at-least a small part of your future house down-payments which you are fantasizing about? Is it with you or you have blown up? In my 1st book – “16 personal finance principles every investor should know”, I have explained in the first chapter how the early start of your financial life can break or make the rest of your financial life. Grab it and read it.

Ask yourself, how much you can show off for the last 5 yrs of earning? Just add up all the salary you have drawn in last 5 yrs (let’s say at 4 lacs per year, its 20 lacs in total 5 yrs), how much you currently have in assets? Even if you have saved 3-5 lacs, I would say its fine. But if you are still trying to locate where has all that gone, it’s not a good sign. Remember, how do you start your financial life can be an indicator of your whole financial life. Dont neglect the first 5 yrs of your financial life because it matters a lot.

Sign 5 – You like to spend a lot of social functions!

Most of the people with the worst financial life in India are too social in nature (not vice versa). They keep spending on all the useless social functions either due to social pressure or by choice. Examples like – “How can I not celebrate my child’s 10th Birthday with a grand party, all relatives are looking forward to it” or “I have to gift something worth to this friend/relative because of reasons reasons reasons.

Social functions in India are one the largest wealth-destroying activities, which are not comparable to anything. Dont get me wrong, I know you need to celebrate marriage, birthday, anniversaries and that’s an important part of life, but when it stops being celebration and becomes showoff and obscene display of imaginary status (which others know very well that you are faking), it’s utter nonsense and destroys your financial life. Please stop it

I know the current young generation does not believe too much into showoff and useless social functions, but due to parents’ pressure and mindset, even children have to kneel down at times and cant avoid this social spending’s even if they hate it from the core of their heart. Ask those children, who are struggling to buy a house because they do not have money and their parents blew up 30 lacs on their wedding to invite 800 people (500 of them you meet the first time in your life and they eat maximum ice-cream at food counters). What a joke !. A small bold decision would have made so many lives easy.

It would be a good idea for you to write down how much % of your income to date, have you spent on social functions (which you could have avoided) in the last 5 yrs. If its more than 2 %, I am sorry for you.

I must mention that all the views are my personal based on my ideologies, If you don’t agree with some point, You are equally right and much like anyone else. The points are general in nature and might not be 100% true for every person’s case.

Take some bold step

I can tell you from my experiences – Most people have bad financial life and they do not do anything about it, because it’s not affecting them in the short term. Every additional bad decision does not hurt their next day, the food will still be on the table, the next movie will still be watched and the small Sunday outing will still happen, but how long if you continue having these 5 signs in your financial life? In our 3rd book – “11 principles to achieve financial freedom” written by Nandish, the coach helps a guy in changing his mindset about his financial life and helping him think like a pro in his financial life, Its an amazing book I would say which no investor should miss.

You need to take some massive action, some really bold step, it has to be 20 times stronger than what you have in mind, you have to really upset few people in your life and have to embrace discomfort for few years. Just a tiny “try” will not help. Imagine you get a deadline from your employer that you can only work for the next 5 yrs and then you will not get any job in the whole world for the next 3 yrs, how will you prepare for this situation? That’s your game plan now!

It has been 5 yrs when the first draft of the Real Estate Regulatory Bill came and then there were many amendments in it over the years. However on 4th June 2013, it was passed by cabinet and now the next step is to table it in parliament this monsoon season and if our country people are really lucky, it will finally become an ACT of law.

Real Estate Sector is hugely unorganized and against buyers

We all know that the real estate sector is so much unregulated and unorganized. There are no proper guidelines on any thing and builders use this to make maximum out of the situation and take buyers for the ride at every level. Builders and Politician nexus are very known and from last 10-15 yrs, the real estate prices have crossed the level that a common middle-class family would never afford their own house.

In this scenario, the real estate regulations are not just a requirement, but a big need of the industry if our economy and society need to some stability over the long term. In this article, we will discuss all the major points in real estate regulations. There are many good points in the regulation and it will help the industry, however like any other law, this bill also has many loopholes and many rules can be exploited by the builders. This bill whenever becomes the final act, will only be applicable to new real estate projects, not the ongoing and completed projects.

From the last few days, there has been a great number of discussions over various news portals and discussion forums on how these regulations will be a great thing and how it is just another failure. So let’s see major highlights of the regulations

1. Mandatory to acquire all clearances before the launch

As per the bill, it would be mandatory to acquire all the required clearances from relevant authorities and govt bodies before formally launching the project. Right now builders launch the project when there is nothing more than plain land on the site and have no permissions for anything. They give rosy pictures to investors, start taking the money from the public and then start the overall process of acquiring the land, getting approvals, and coming up with the structure. This means there will be obvious delays and lots of confusion and frustration for investors.

With this, the concept of “pre-launch” offers will vanish and you can expect the prices of the property to be high on launch. A lot of people are saying that because of this, there might be a slowdown on the supply side because right now a builder keeps launching new projects. Another requirements is that these permissions taken are to be displayed on the website of the developer.

2. Use of Photograph of actual site for advertisements

As per the bill, the builders will have to use the actual sire pictures or the actual construction work pictures for advertisements for the project. Right now builders do not use the actual pictures for promotional purpose.

It’s easy to create an illusion by using graphics and shiny pictures and that is what happens most of the time. Builders use the classic graphics image of the project site which is full of greenery and nature around it and the feeling it gives you is that its an opportunity one cant miss. However, in reality, the project site is quite different. It might happen that there are buildings around it and no trees or any natural habitat. The roads around might be bad and the elevation of the project site might be high or low than the normal.

If a builder is found to be putting up misleading or wrong advertisements, then there can be a jail term of up to three years, if it’s done repeatedly.

3. Sale of property as per prices linked with Carpet Area

The bill says that any sale proceedings should be using the prices which are linked with carpet area and not super built-up area. Generally, builders use “super built-up area” as the parameter and define the per sq ft price as per that. Carpet area is the net usable area which can be used for living purpose (imagine you lay down carpet, then how much area it will cover), however super built-up area (or salable area as called by many builders) is combination of net usable area, area covered by walls, doors, parking area, staircases, temple in side the project, gym, garden and everything you can imagine which is part of your package (divided per buyer). So super built-up area becomes high and the per sq ft price looks small, however, if you divide the whole cost by the carpet area, then you will realize how much you are paying.

You should also know that even in agreement, only the carpet area is mentioned. However, builders quote the pricing only on super built-up area.

4. State Level Regulators and central appellate tribunal to be set up

The bills also say that a central appellate tribunal should be set up as a central body and each individual states should also have state regulators. This means that there would be some central guidelines for the real estate sector and builder and each state will focus on regulating their states real estate builders. There might be few rules different from states to states. I personally feel that there might be some confusion due to this.

5. Real Agents/Dealers need to register themselves

Right now, real estate agents and dealers are not at all registered with any central/state body and hence due to highly unregulated environments, they do not have any code of conduct or service standards defined. Now they will have to register themselves and will have clear responsibilities and functions. Consumers will be able to demand their rights from agents and dealers for the amount of commissions paid to them.

6. Separate bank accounts for every project

As per the bill, A builder will have to maintain separate bank account for each and every project and up to 70% of the funds for that project has to be there in that same bank account. In the previous drafts, this number was 100% (means no money for Project A can be used in Project B) , but looks like the builders and politicians lobby has been successful in diluting the quality of the bill wordings and in new draft now the number is 70% or less. It does not serve the protection of buyers because builders will still be able to divert 30% of the funds from one project to another.

Right now, the way it works is that a builder when faces a severe cash crunch launches a new project and uses the money collected in another project to complete the old project and this cycle goes on. This creates a lot of issues for home buyers because there are huge delays at times. Firstpost did an excellent article on this topic and concluded that real estate is a kind of Ponzi scheme

7. Builders cant take more than 10% advance without a written Agreement

A builder will not be able to take more than 10% advance money from buyers without a written agreement. Right now a lot of dealings happens by paying huge advances and the agreement part is delayed by many. In many cases, agreements happen after many months or years, as lots of transactions happen on a trust basis. This might help in curtailing some part of black money transactions. However only you guys can tell some real-life cases which this clause might not help and fail.

8. Full refund with interest, if property not handed over time

As per the bill, the builder has to refund your money along with the interest, if he fails to deliver the project on time. At this moment, this point gets added in the agreement and almost all the times, builders make sure that this point is omitted in the agreement and if it’s not there, you have to file a consumer court and after a long time, you are rewarded your right. However, the bill will make it a standard rule or clause.

The Bill rules apply to project over 4,000 sq meters in size

The biggest worry about this bill is that it’s applicable only to projects which are of 4,000 sq meters and above size overall and if a project is bigger than 4,000 sq meters, the bills allow to break the whole project into different phases and see each phase as different project. Now this clause itself destroys the protection layer for consumers. Because a builder can always break the whole project into different phases and show them as a separate project. Many builders anyways run various projects under different companies’ names to save on tax. So running two or more sub projects on different names (which are actually just one project side by side).

The old draft of the bill had this number at 1,000 sq meter, but this current recent bill has it at 4,000 sq meter, so again someone has been able to influence the bill.

No Single Window Clearance for Approvals

One of the major challenges and problems builders face is about the govt clearances and various approvals. This takes a lot of time and opens up the gate for bribes and bureaucracy, the bill does not address this problem at all. It would be great if there would be a separate govt department which would have a single-window clearance. This would help in defining the project completion time with more accuracy.

Will all this reduce the property prices or not?

This is the million-dollar question which is in every body-mind, that with this bill, will the prices of real estate come down or not, which is the biggest issue common man is facing right now, compared to any other issue. Delays and consumer exploitation is all fine if prices are normal and affordable, but if prices itself are so high that its out of reach of common man, then every other problem is secondary.

Here is a copy of the Real Estate Bill which I got from Moneylife article

There are many implications of this bill and tons of factors and variables which can affect real estate prices. Some are saying that prices might go up and some are saying pricing might come down. But It would only be clear when the bill becomes a reality.

However, we would like to hear what you think about this real estate bill and how it might impact the real estate prices?

Few weeks back, I posted an interesting question on our Facebook Page asking – “Given limited money – which is more important product to buy from security point of view – Term Insurance or Health Insurance ?” .

Lets say there is a guy – who wants both a term plan and a health insurance for his family and he only has Rs 10,000 per annum left with him, now he can either buy a 1 crore term plan for his family or buy a 5 lacs cover for his family. But he will be able to get only one of them from this Rs 10,000 left with him, then which out of term plan and health insurance is makes sense for family and is more useful? Lets see some points, raised by our facebook fans, which will help us to think about it.

1. Death is less probable compared to hospitalization

One of the argument is that, there are far greater chances of getting hospitalized because of some reason then dying. So if you look at this problem from probability point of view, you can be almost sure that in next 5-10 yrs, you or one of your family member will be hospitalized for some or the other reason – big or small. But meeting death is very less likely in comparison. So a lot of people argued that Health insurance is much more important than term plan, if you have limited money.

2. Premiums are increasing fast in Health Insurance and its can be claim every year

Another argument in favor of health insurance over a term plan was that, its a product where you can claim every year and protects your financial life from regular attacks of money sucking illnesses and accidents and anyways premiums are increasing very fast for health insurance (or would increase in future) because of the health care inflation. However for term plan the premiums are coming down over the years (now we might be close to saturation) .

3. Hospitalization Costs can be arranged in worst case

Now some people said that term plan is more important than health insurance and the biggest reason for it was that health insurance expenses are somehow manageable in worst case. You can take a loan, swipe a credit card, ask your friends and relatives or in worst case, sell some of your home stuff.

Life will again be on track somehow. But if you ignore term plan, its a very big risk for your family future, because the amount required by your family cant be arranged by asking it from someone (just imagine you die and now your family would need their monthly expenses for lifetime , your children expenses for current and future, their whole life is at stake now). It would generally run into several lacs or few crores.

High Probability – Low Impact

So its very clear that term plan has a very high impact on your financial life, but less probability of its occurrence , however health insurance has low impact on your financial life (compared to term plan) , but is high on probability and its has potential to occur multiple times in your lifetime.

Balancing both Health and Life Insurance Costs

Another workable option is to divide the money into premiums for both term plan and health insurance, but in this case you will compromise with the cover amount of both the things however small it is. This way you will have both the things in your financial life, even if its small . Do you think its a workable solution ?

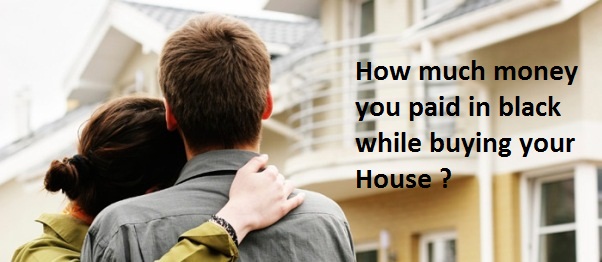

Naresh recently visited a new residential project in Pune which was ready for possession. The property cost was in his budget and he was about to finalize the deal. The total cost of property was around Rs 40 lacs. Stamp duty and Registration cost was to be paid separately which would take total cost to around 43 lacs. This was a bit heavy on Naresh pocket, so out of his regular habit, he inquired if there is any trick by which he can save some money on the deal ?

The builder was quick to give him a great saving advice – “Sir , You have to pay 6% stamp duty and 1% registration cost on the agreement price. Which comes to 7% of 40 lacs, thats 2.8 lacs additional, thats the reason the total cost comes around 43 lacs . Now if you want to save money, what you can do is pay some part of the deal in cash to us (means pay in black) and we will reduce the agreement cost by that much, that way – we will also save our tax on the black money part and you will save 7% on that cash amount. Like if you pay us Rs 10 lacs in Cash, then we will make the agreement for Rs 30 lacs only and you will have to pay stamp duty and registration cost on only 30 lacs which will be 2.1 lacs, and it will save you Rs 70,000 without doing anything extra ! . Cool na ! .”

The offer was tempting and Naresh fell for it, how cool is saving Rs 70,000 , all you need to do is pay some part in cash and lower the agreement amount in records. But do you understand, what is your loss in long term because of this kind of deal ? Let me break some hearts today, who have already done this mistake while buying their properties.

Stamp duty and Registration Costs

First understand that stamp duty and registration costs vary from one state to other state. For example – In Maharashtra, its 6% + 1% = 7% in total , so whatever is your total agreement cost , you will have to bear additional 7% on that amount as stamp duty + registration costs. Given the huge amount involved and the financial crunch every buyer faces at the last moment of the deal and hunger of builders to save every bit of tax, makes sure that buyers fall for this trick of paying huge amount in CASH (black money) and register the property at lower price just for few thousands (actually sizable if you look at it). This looks like win-win situation to buyers and they are pretty happy about it, however truly speaking, this is a loosing deal for the buyers in a very long run (if you are going to sell the property later) and only benefits the builders and let me now explain you why is it so ?

At the time of selling – The cost of house matters

I hope you are very clear that when you sell your property in future , you pay the tax on the profits made. And the profit is decided by your COST of the house and the sell price. So lower the cost of your house, the higher the profits on paper for you in future. You might be aware of the fact that indexation is applied in case of real estate transactions and 20% tax is paid on the profit.

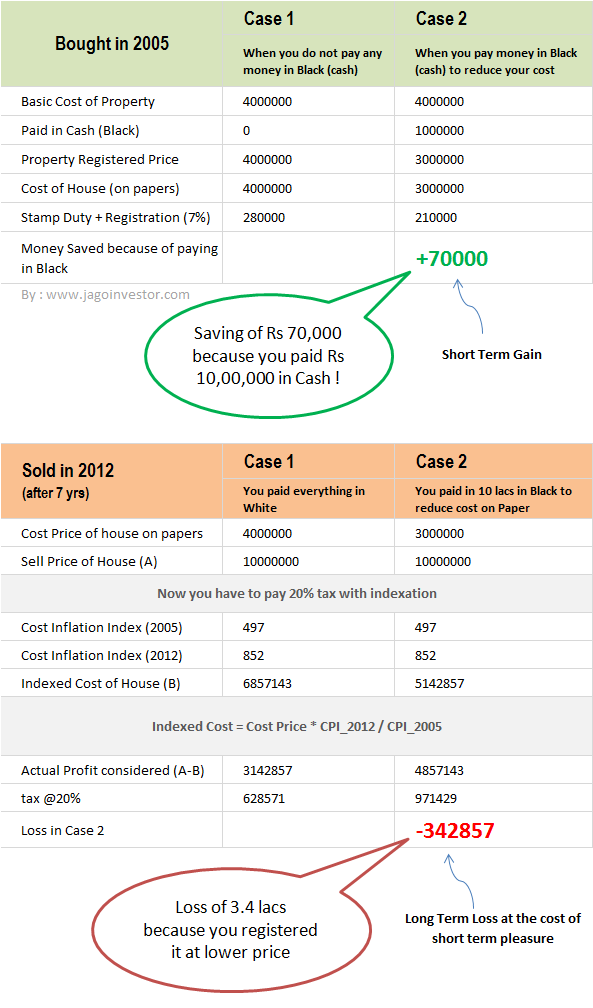

Now lets take this same example we are discussing and see how much you save at the time of purchase and how much you loose at the time of selling , which can be in distant future. See the working below and try to understand the whole situation

In the example above you can clearly see that by paying Rs 10 lacs in cash, a person is able to save Rs 70,000 instantly. However they are not able to look beyond the obvious and visualize the kind of loss they will incur in future when they decide to sell the property. The same person will pay 3.4 lacs of additional tax in future because he/she paid Rs 10 lacs in cash years back.

Now there are few points which can be debated here like there can be changes in laws in future, or one can save the tax by investing in another real estate properties (which again depends on future laws) , but the point here is to educate you on the long term implications of this. Now if you fully understand the message of this post, you can take your decisions with full responsibility.

I don’t want to shock you, but there are tons of cases where employer happily deducts your EPF amount from your salary, but they do not deposit it with EPFO. This goes on for years and one day you come to know that you are stuck ! , because there is no EPF money for you. Your employer has severe cash crunch or is about to shut down and now you have to run pillar to post to claim your money. The whole situation gets ugly and you feel cheated, because your company never deposited the Employee Provident Fund amount. Now you go to Police and file a case against employer. But this all can be avoided if you are careful a bit, from starting itself.

How about making sure your employer is depositing your provided fund money into your EPF account ? Before I tell you, how you can do that, let me first share with you some REAL LIFE cases where employer failed to deposit EPF money and employees are suffering ! . These are some of the examples shared by readers of this same blog over comments section in various of EPF related articles.

Case 1 – How Abha’s company didnt deposit EPF money for 2 yrs

Dear Manish,

Thanks for such an informative post. At last i do see some hope. Here is my situation:

Worked for this company A for almost 4 years and left them in Nov 2011 as they were downsizing…yes it’s been more than a year and half of torture they have given me thus far. Company is kind of closed now as I don’t get any proper response from them, CEO is just not bothered. Company first asked us to wait for 2 months to file the claim as it is a rule, did that patiently. Later came the story of change of PF office from one (under which it was originally registered) to another and that went on for several months

They kept saying PF offices are not coordinating among themselves, the real reason was even shocking and more disappointing, PF guys were not updating because this company didn’t not deposit our PF amount for long time (2 yrs appx), they however kept deducting the same from our salaries (was surprised how come there was no annual audit by PF office and how this company could continue doing so for this long), anyways they cleared things in January this year and said we have applied again. When filed a grievance online, PF person says we haven’t received any claim whereas this X employer says they have already applied. Don’t know what the real truth is but on the basis on experiences I have… most certainly it is the X employer at fault.

Another strange thing is, when I checked by balance online in January this year it looked fine (updated up to 2012… I do have SMS proof) but from last 2 times it saying updated up to 2010, I am worried if this employer has dome some mischief here too, is it possible for a company to take back money from an employee’s PF account or it is the issue with PF website?

I don’t want to apply for my claim via options you suggested above unless I see the balance updated. Thank you so much for reading thru my query/concern. Appreciate your feedback.

Case 2 – Balaji Company asked him to Wait till they deposit the Employee Provident Fund money

Hi Manish,

I switched jobs in August this year. Before I quit the job, I had submitted form with my previous employer for withdrawing the amount in my PF account. I had not received the amount due till December. When I called my previous employer, they told that they have not yet deposited the money and I will have to wait till March 2013.

My question is, is what my employer did legal? How frequently should the employer deposit the PF money with the EPFO? I have been working with the organisation for little more than a year now.

Case 3 – Sarabjeet Kaur company not replying her because they did not deposit EPF amount

I worked in an organisation for 2 years. They have not deposited the PF amount which they used to deduct it from our account. Its been 1 year I am asking them to refund the PF. They have stopped replying to the emails and have stopped answering everybody’s call. Is there any ways I can withdraw the amount? The firm is based out in Mumbai and I used to work in Delhi Branch.

Employer can be Jailed if they do not deposit EPF money

An employer has no right to deduct the employee share from salary and not deposit it with EPF. There can be any excuse or justification for this, because its employee hard earned money. Once the employer deducts the Employee Provident Fund money from the employee salary, its their duty to deposit it with EPFO , and if they fail to do so for any reason, its a crime.

Whatever is the case, you can always complain about it with the EPFO department and the concerned officer has all the rights to proceed the legal complaint against the Employer and in the worst case, employer can also go to jail, because what they did is a criminal offence under section 405/406 of IPC .

1. Complain to CVO officer – You can also email your situation and case to the CVO (chief vigilence officer) at EPFO, who is appointed by Ministry of labour for EPFO to look after these kind of irregularities. You can email them at [email protected] . More at this link

2. File a Police Complaint – You can also file a criminal case, against the employer in police station which comes under the jurisdiction of your working office (not the registered one) . All you need to show them is the salary slip, which shows the EPF deducted, note that its always better to mail CVO about it anyways, so that the chances of local authorities influencing the matter will reduce.

3. Complain to Regional Provident Fund Commissioner (RPFC) – You should also complain about the matter to the RPFC officer if under the EPFO office, which will be investigated by him/her.

How Employers Deposit your EPF contribution to EPF account ?

How exactly your EPF money gets deposited in your EPF account ? Here is what I found on this website

Employees’ PF a/cs are maintained under these two different methods are –

1) All accounts are with O/o the RPFC

Every registered employer remits the Employee Provident Fund contribution by challans to the RPFC’s Bank a/cs. which in turn gets accounted in the respective A/c No.of every such employee. And the employer submits monthly returns to the RPFC showing the details, employee wise of contribution thus remitted.

Every such money is maintained by the RPFC who in turn disburses, thro’ the employer towards refundable loans, F & F settlements together with accrued interest to the respective employees. Once in a year a ledger sheet showing the transactions of any employee for one full year is issued to the concerned. Similarly from the PF contribution pension contribution is divided and remitted to the Pension a/c. of the employees thro’ a separate A/c. code. This method is the largest.

2) The other method is called “Exempted Establishments (PF Trust)”

An employer/company who employs more 100 employees on roll is eligible to apply to the RPFC for “exemption” from maintaining the EPF under the above said (1) method. RPFC grants the “exemption orders” under certain conditions after examining various aspects. After which the Employer sets up a EPF Trust to be run by Employer (employer’s nominees & Employees’ representative (Union nominees) which manages all the contributions of employees & employer (excepting Pension Fund which is never maintained by the Trust). A set of Bye laws, in the lines of EPF Act & Rules is prepared & duly approved by the RPFC for running the Trust.

This PF Trust money is invested in the Govt.approved securities for earning the assured interest from which accrued interest to the employees’ PF a/cs is credited. The Trust once in a year prints the Employees’ PF ledger a/cs and distribute to the concerned. The Trust accounts are audited by the CA and submitted to the RPFC. RPFC also periodically inspects the Trust a/cs and oversee. Monthly, annual returns in the Forms have to be submitted. The convenience under the Trust is quick disbursement of loans, withdrawals and F & F settlements to the employees. Surplus, if any never distributed but any shortfall is made good by the employer.

How to find out if your employer is depositing your EPF contribution or not ?

Let me share with you some steps you should follow, to find out if your company is depositing your EPF contribution properly or not.

1. First thing is the do not rely on hearsay’s here and there. It might happen that you come to know from some one that your company is not depositing your EPF money, but it might not always be true . Delays happens at times .

2. Every month on 25th , your employer is suppose to send few documents to EPFO department to intimate them on

Form – 2 (for new member during the month)

Form – 5 (detail of new joinees during the month)

Form – 10 (detail of left employees during the month)

Form – 12 – (Details of money deducted from employees salary)

3. The best thing is to first contact your employer and ask them for a copy of these forms for last 2-3 months, do double check if they deposited the money or not.

4. As per my opinion, the best way for a common man and most convenient option is to file a RTI against EPFO and ask them all these questions . Mention your EPF account number, your employer Code and simply ask if your employer has been depositing your contribution or not.

Conclusion

Mostly the big size employers might be depositing the Employee Provident Fund money properly on time, but some of the companies which are small sized or whose owners and management teams are unethical might be into these illegal activities of not depositing employees hard earned money. Its always a good idea to spend some time to be assured, in-case you feel your company is one of those who are not depositing EPF amount with EPFO 🙂

Do you know of any case like this ? Also Please share this article with more and more people

Do you have some doubt on Income Tax Return Filing Process or some question whose answer you are not getting anywhere? This post might be the end of your struggle.

Few weeks back, we ran a survey and asked investors to send us their queries and doubts on Income Tax Return Filing, whatever it may be. We then picked up some of the most asked and common doubts which investors face and thought of creating this comprehensive guide which will act like the bible to your ITR related queries.

Nobody in this world likes the annual exercise of filing Income Tax Return. Yet due to legal responsibility, everybody has to file his Income Tax Return. Now before understanding the Income Tax Return filing, let’s understand few common things first, which will help you to resolve your queries on ITR.

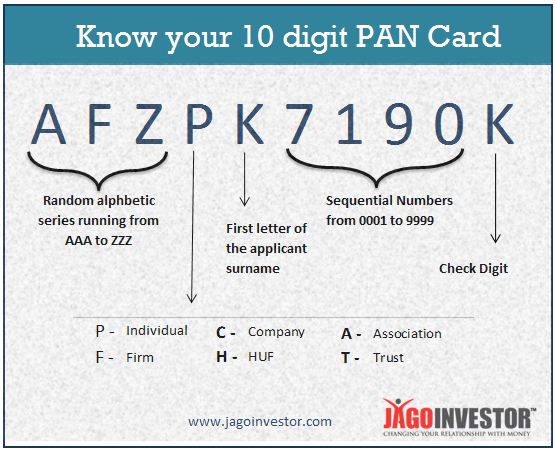

1. Permanent Account Number (PAN)

Permanent Account Number (PAN) is a ten-digit alphanumeric number, issued in the form of a laminated card, by the Income Tax Department, to any “person” who applies for it or to whom the department allots the number without an application. PAN enables the department to link all transactions of the “person” with the department.

These transactions include tax payments, TDS/TCS credits, returns of Income/wealth/gift/FBT, specified transactions, correspondence, and so on. PAN, thus, acts as an identifier for the “person” with the tax department.

A typical PAN is AFZPK7190K

First three characters i.e. “AFZ” in the above PAN are alphabetic series running from AAA to ZZZ

Fourth character of PAN i.e. “P” in the above PAN represents the status of the PAN holder.

“P” stands for Individual,

“F” stands for Firm,

“C” stands for Company,

“H” stands for HUF,

“A” stands for AOP, “T” stands for TRUST etc.

Fifth character i.e. “K” in the above PAN represents first character of the PAN holder’s last name/surname.

Next four characters i.e. “7190” in the above PAN are sequential number running from 0001 to 9999.

Last character i.e. “K” in the above PAN is an alphabetic check digit. (More Details on PAN)

2. Tax Deduction Account Number (TAN)

TAN or Tax Deduction and Collection Account Number is a 10 digit alpha numeric number required to be obtained by all persons who are responsible for deducting or collecting tax. It is compulsory to quote TAN in TDS/TCS return (including any e-TDS/TCS return), any TDS/TCS payment challan and TDS/TCS certificates. (More Details on TAN)

3. Financial Year

In India, the Financial Year is defined as a period starting from 1st April of a Calendar Year & ending on 31st March of the next immediate Calendar year. All the income earned by a tax assessee has to be accounted for segregation on the basis of dates in different Financial Years.

4. Assessment Year

The applicable Assessment Year for a given Financial Year is the next +1 year. For example, if a FY is 2012-2013, the relevant AY ‘ll be 2013-2014. All the income earned by you in a FY and taxes paid by you in that FY ‘ll be assessed only in the relevant AY.

5. Form-16

It’s the statement of your yearly income provided by your employer to you after the end of FY. This includes your gross income, deductions claimed by you, net income, tax liability there on, Tax deducted by your employer, any tax liability or refund.

The most important thing to be remember in form 16 is the TAN of your employer should be written clearly & so do your own PAN.

6. Form-16A

Form 16 is issued by the Tax deducting authority where the TDS is applied on your investments (say FD in banks) or non salary cases. Say TDS applied by tenant against rent paid to landlord. Here again TAN & PAN quotation is must.

7. Types of Income

As per Income Tax Act 1961, the income can be classified only under the following heads.

1. Income From Salary or Pension

2. Income from House Property – Rental Income

3. Income from Business or Profession – Say Income to a Doctor or an Agent or Advocate or a Shopkeeper

4. Income from Capital Gains – Income arising out of sell of capital assets like Property, Gold, Art, Coins, Mutual Fund Units, Equity, Precious stones

5. Income from other sources – Any income which can not be classified in the previous 4 categories, comes under this head. Interest income, winning amount in Lottery or Quiz show (example KBC), Horse racing winning, Amount received as Gift from non relatives are some examples.

Now from the above list you can identify that you are having at least 2-3 income sources. Income Tax Deptt. has created different types of Income Tax Return Forms for the combination of different income sources.

Before Discussing Income Tax Return Forms, let’s discuss Income Tax Return itself.

8. What is the importance of Income Tax Return

If your income exceeds the zero tax limits, it’s mandatory for you to file an Income Tax return. During your income earning in the whole FY, there may be a situation that the tax deducted from you is more than the actual liability or there are some losses or deductions which you could not claim during the income earning phase or you paid less tax than the actual liability.

In all such case, you can only save yourself by filing an Income Tax Return. Actually your Income Tax Return form is the account statement of your income, tax liability there on & the tax paid by you. If there is excess tax payment, you ‘ll get refund. If the paid tax is less than your tax liability you w’d have to pay the difference amount.

Below is the official version for Income Tax Return filing essentially.

“The filing of income tax/wealth-tax return is a legal obligation of every person whose total income and wealth tax during the previous year exceeds the maximum amount which is not chargeable to income tax or wealth tax under the provisions of I.T.

Act, 1961 or Wealth Tax Act 1957, as the case may be. The return should be furnished in the prescribed form on or before the due date(s). Penalty of Rs. 5000 is imposable for non-filing of return within the assessment year.

Interest is also chargeable for non-filing or late filing.”

Watch this video to know why you should file income tax return:

9. Types of Income Tax Assessees

As there are multiple source & types of Income, so are types of Income Tax Assessees. Here are few examples –

Individual

Hindu Undivided Family

Firm

Limited Liability Partnership

Association of Persons

Company

Trust

Body of Individuals

Artificial Judicial Person

Local Authority

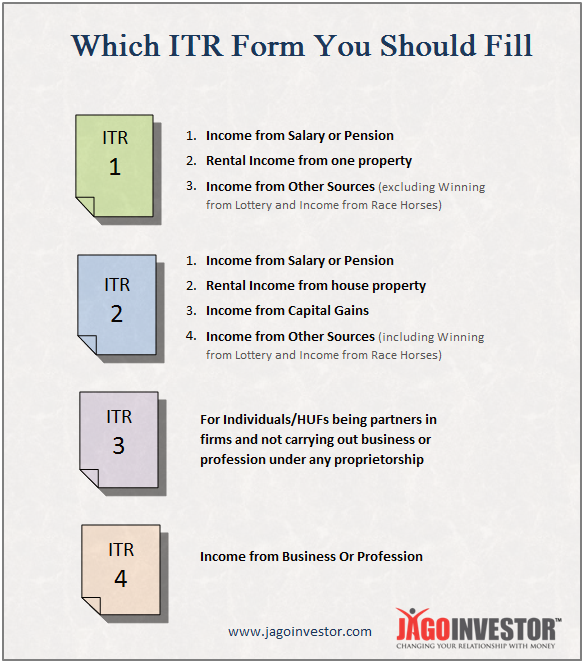

10. Types of Income Tax Return Forms

On the basis of the income combinations as well as Assessee types as discussed above, the Income Tax Deptt. has issued multiple Income Tax Return forms. these are numbered as ITR-1, ITR-2 ……. ITR-7.

Here is a table to understand the combinations of types Incomes for Individual Assesses & the applicable ITR form. Please do note, ITR-5, ITR-6 & ITR-7 are used by assesses other than Individuals & HUFs, hence not discussed here to keep this matter relevant for general public & common Individual assessee.

Majority of common individual tax payers fall in ITR-1 & ITR-2 category.

11. Online & Offline filing of Income Tax Return

The Income Tax Department is slowly transforming itself. Earlier all the returns were only offline mode. First non Individual & non HUF ITRs were made online filing compulsory. After that for Individuals & HUFs having income more than 10L Rs. were made online filing compulsory.

Now From AY 2013-2014, the income limit has been reduced to 5L Rs. for online filing. So we can safely assume that from next AY i.e. 2014-2015, the online return filing ‘ll be compulsory for each & every tax payer.

12. How to file online ITR

It’s quite easy. Now a days, a person can e-file either self by logging into the official site of e-filing. Apart from this, there are many other private online portals who are helping you to e-file your ITR. (Taxsmile, Taxspanner, Taxyogi, Cleartax are few examples)

Frequency asked doubts on Income Tax Return Filing

We hope that you are very clear about the basic information which every tax payer should be aware about. Now lets see some of the most commonly asked questions on Tax Filing. We collected these questions from one of our surveys and just categorized them into 13 questions. Here are they –

1. I forget (or could not produce in time) to claim HRA/Savings/Home Loan/LTC/Medical Bills etc from my employer. What to do?

Please relax. For all such cases, where either you could not claim on time or forget all together, your return filing is the time to tell the Income Tax department about the same & now you can claim the refund for the excess tax deducted from you. Note that the declaration given to employer is just to make sure that your TDS cut by employer is inline with your plans in a financial year. Incase something does not match, It can be finally done at the time of tax returns filing.

2. Where should I produce Bills/papers/receipts of the things related to Q. 1 above

Please do note that current ITR forms are ‘annexure less’ forms. Which means, that you need not produce any support documents to the Income Tax Department at the time of filing. Just keep the documents safely with you, so that you can produce the same if Income Tax people demand it from you in future. Documentation should be surely done by you, because incase there is a scrutiny case in future, you should have to documentary evidence.

3. I could not file my previous years income tax return on time or forget it .

It happens ! . There are penalty provisions if you do not file your due Income Tax Return on time. To correct the mistake, please file a delayed return now if you have not filed the previous years return. For ITRs related to previous years, please take help of a Tax professional to do the same. Filing late is better than not filing at all. Just contact a CA or tax filing portals, and they will be able to help you. Read this article on Late Tax Filing for clarity

4. I did not get the refund order/cheque . What to do ?

First check your refund status here. In case your refund status is available as cheque issued & the same is not received by you. Please contact at the E-mail or Phone nos. in the shared link. Also you read this article on how to Check your Income tax refund status online & Learn how to use RTI

5. I received the Refund cheque but I misplaced it/delivered at wrong address/wrong bank account number.

A lot of these issues happens because the address you provided at the time of filing returns years back is not the same where you are residing now, and the cheque goes back. For all such cases, you should contact your Jurisdictional Assessing Officer for offline filed ITR or CPC Bangalore for online filed ITRs. For online filed ITR, there is a link within your login window for Refund Reissue Request, use this for refund reissue.

6. How can I calculate my tax liability arising out of capital gains

Relax. You just need to punch in the required data in the excel sheet for ITR e-filing available at the e-filing portal. The sheet ‘ll calculate your tax liability on it’s own. Or you can refer to this article which will guide you on how to calculate capital gains.

7. How can I pay my due taxes as per calculation done by me or ITR excel sheet

Paying your due taxes is very easy. There are 2 ways to it. a) Use your net-banking account . b) Use the Official Portal . Please do note for self payment of Income tax, the applicable challan number is 280.

8. I fall in 20-30% tax slab. Bank deducted TDS @ 10%. Should I pay more Tax

The answer is yes. Bank has merely done it’s legal responsibility. Your Tax liability is more than the work done by bank. So please calculate your actual tax liability by adding the interest income into your gross income & pay your due taxes. Here is a full article on TDS related issues.

9. I forget to put in some data or wrong data was put in during my original return filing. How to rectify it ?

No problem, you can file a revised return to rectify these mistakes. The revised return can be filed before the assessment year is over for your original filed return. Here one important point is that the original return must be filed within due date. Just note this point, that if you have filed your returns and if there are any issues or errors, you can always file a revised return later.

10. I own a house in the same city & reside in a rented accommodation. Can I claim HRA & Home loan benefit simultaneously ?

The answer is YES. If you are actually residing on rent due to your Job or any other issues & the home loan house is also in the same city, you can claim both HRA as well as Home Loan benefits. Read this article for more on this

11. I was earning salary earlier. But now there is no income due to break or because I have become NRI with no Indian Income. Should I still file my ITR for zero income ?

The answer is no. if you do not have income or income is within the zero tax slab, you need not file your ITR. Yes in case, some TDS was there, you w’d have to file your ITR to claim the refund of this TDS amount..

12. My wife is a home maker & investing small money into direct Equity & earning some income. Which ITR should she use ?

First of all make sure her income is under zero tax slab or more than it. In case she is earning more than zero tax slab, she should file her ITR. Now the quantity of trades done by her to earn that income ‘ll decide the applicability of ITR. In normal situations, such earning ‘ll be Capital gains (Here it’s assume that gains are short term in nature due to holding less than 1Y) & she should use ITR-2.

For a very high quantity of trading activities, the applicable form ‘ll be ITR-3.

13. I worked with 2 employers in a FY. How to handle & file my ITR ?

First of all please collect form 16 from both of your employers. Now consolidate the income from both employers & check for an pending tax to be paid. Pay it now. Once all this is over, please file your ITR.

We hope all your queries about income tax return filing is solved in this article. If not, please post your doubts over comment section.

This article is contributed by Ashal Jauhari . A key member of Jagoinvestor community and a Tax expert . He writes on his blog here

In this article we are going to share SBI Maxgain Home Loan review with you. Now a days many home loan borrowers are opting a particular type of home loan from State Bank of India which is called Max Gain because it has many advantages compared to other kind of home loan scheme’s. In this SBI Max Gain home loan, an Overdraft (OD) account is assigned to the customer’s home loan & any amount parked by customer is treated as loan repayment for the purpose of interest calculation, for the days, the amount stays there in that OD account. As on date following banks are offering similar types of home loan to their customers. I would like to thank to Mr. VKS Nathan who gave the Idea of this article.

SBI, IDBI, CITI, HSBC & Standard Chartered. Punjab National Bank can also be added in this list but it’s offering a combo of normal loan + Overdraft. In this article, we are going to discuss only SBI Max Gain as in OD linked home loan, the maximum business is with SBI & the most discussed topic on Jagoinvestor Forum is also related to SBI Max Gain Scheme

What is an Overdraft account?

Before we discuss Max Gain, first understand, what is an Over Draft Account? All of us are well aware of functioning of an ordinary saving bank (SB) account. Here account operates between zero to positive & positive to zero. As we deposit our money, it’s used by bank & we get interest on our money from bank. In case of an OD account, bank first ask for a security & then assign a credit limit on the basis of the market value of that security. This security may be Fixed Deposits, Insurance Policies, National Saving Certificates, Shares, Mutual Fund units, house/commercial property etc. Now when we are using this assigned credit limit, the amount is going from zero to negative zone & when we are repaying, it’s coming from negative to zero. As we are using bank’s money in this case, the interest ‘ll be paid by us to bank. That’s how an OD account works.

So what is the correlation between Max Gain home loan & Over Draft account?

For Max Gain borrowers, State bank of India opens an Over Draft account where the Credit limit as discussed above is equal to the loan value assigned to the borrower. Here underlying security is the home you have purchased or constructed from that loan amount. Now as & when you are parking any surplus amount into this OD account, the parked amount is treated as payment towards loan (effectively you are bringing down your loan liability from negative towards zero position) and thus the interest ‘ll be charged only on the difference amount i.e. total loan amount – parked surplus amount.

What is the primary benefit of SBI Max Gain Scheme?

Well the primary benefit of MG is to keep your liquidity intact & still bringing down your interest outgo. To understand it better, please imagine a situation you are running a home loan of 30L Rs. & now you do have 2L Rs. with you to prepay. In normal home loan, your 2L Rs. ‘ll be accepted by bank & adjusted towards home loan & your amount is gone forever so no liquidity for you of that 2L Rs. amount. On the other hand, if you are MG customer, simply park those 2L Rs. in your MG account & your interest outgo ‘ll be lower from that month itself till those 2L Rs. or a part of it is there as surplus in MG account.

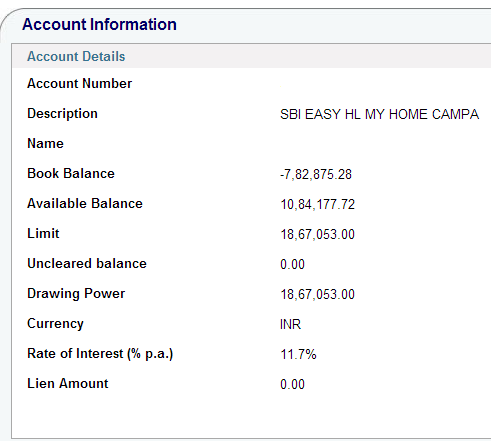

What is Drawing Power ?

Drawing Power is nothing but your as on date actual outstanding loan amount. Before final disbursal or start of loan repayment, it’s your sanctioned loan amount. Once your EMI starts, it’s your as on date actual outstanding loan amount. Please check Image below, Drawing Power here is 1867053 Rs. as on date. (Click here to understand it better)

What is Available balance?

Before final disbursal, it’s the sum of undisbursed amount + parked surplus & post final disbursal, it’s your parked surplus amount which is available to withdraw. Please check Image below, Available Balance here is 1084177.72 Rs. as on date. (Click here to understand it better)

What is book balance?

It’s the adjusted loan amount arrived after deducting the Available Balance amount from Drawing Power. In your account statements it’s shown with a negative sign. Please check Image below, Book Balance here is – 782875.28 Rs. as on date. (Click here to understand it better)

Is there any extra interest for Max Gain?

No, the interest for home loan is same in SBI be it for normal home loan or for Max Gain.

I’m an existing SBI home loan customer. Can I convert my old term loan to Max Gain?

Yes, you can. Please contact your loan serving branch or RACPC for the required paperwork to be done. This may be an outdated info so please do check with your loan serving branch for current day rules on conversion.

I have taken the Max Gain for an Under Construction Property. Can I park surplus amount to save on interest outgo?

The answer is yes & no both. Yes you can park your surplus during under construction phase but do remember SBI is disbursing partially at this juncture & in case due to any emergency you want to liquidate your surplus, SBI ‘l not allow the same. so park only that much surplus, you feel you ‘ll not need even in an extreme emergency.

If I’m parking some money on monthly basis or in lump sum, will my loan term come down or EMI go down?

No. Neither your EMI ‘ll come down nor your loan term. The only saving is in terms of interest outgo. To understand it better, Let’s assume a test case of loan amount 30L Rs. @ 10% Rate of Interest for 20Y term. The normal EMI for these nos. ‘ll be 28951 Rs. The break up of your EMI for first month ‘ll be 25000 Rs. interest & 3951 Rs. for principal repayment.

Now if you do have 2L Rs. surplus in the very first month & prepay the same as below –

Case – 1 Normal home loan

Your 2L Rs. is gone & outstanding loan amount ‘ll come to 2796049 & interest outgo ‘ll still be 25000 Rs. but the no. of months ‘ll come down from original 240 to 198 months.

Case – 2 Max Gain home loan

Your 2L Rs. are parked in that OD account & the interest for the very first month ‘ll be calculated on 28L Rs. & thus it ‘ll be 23334 & thus there‘ll be an interest saving of 1667 Rs. which‘ll remain available in your OD account as surplus along with your parked surplus 2L Rs. so for next month, the parked surplus amount ‘ll be 201667 Rs.

Please do note in case 2 above, Your loan term is still 240 months but the saving of interest ‘ll keep on increasing on mly basis from the parked surplus & of course the liquidity of those 2L Rs. is there.

How can I calculate my saving in Max Gain?

To know your actual saving, first of all please demand a loan amortization schedule from your loan serving branch & now for each month compare the scheduled interest outgo as per your loan amount. schedule & the actual interest outgo.

What should I do to maximize the savings in Max Gain?

If you are paying your EMIs from SBI’s SB account, you can maximize your benefits. How? here it goes. Say 15th is the EMi date on which EMi amount is debited from your SB acct. Now in a normal home loan, people ‘ll keep at least 2-3 months’ EMI amount as buffer in SB account. but in case of Max Gain, you do not need to keep buffer in SB account. Keep this buffer amount also in your MG account along with your routine surplus amount. now use the power of net-banking of SBI for your own good & create a schedule transaction of your EMI amount 28951 Rs. (in the above example) to be transferred on 13th of every month from MG account to SB account. At a time you can schedule for next 12 months by using standard instruction. So it’s technology that’s helping you.

I can transfer to MG account from my existing net-banking enabled SB account but reverse is not happening. why?

The answer lies in the fact that Net-banking transaction rights on your MG account is not enabled yet by your loan serving branch. if final disbursal is done, you can apply for transaction rights. if only partial disbursement has been done, sorry, you can’t apply for transaction rights till final disbursal.

Is it mandatory to purchase property insurance & life insurance along with Max Gain?

Having property insurance as well as sufficient life insurance is compulsory but purchasing the same from SBI’s sister cos. like SBI General ins. & SBI Life ins. is not at all mandatory. if you feel that policies are being cross sold to you to exploit your position (home loan seeker), please contact the AGM of your local RACPC where your loan application is under processing.

Is SBI charging higher processing fee for Max Gain?

No, as on date there is no differentiation in fee for term loan & Max Gain but SBi reserves the rights to charge different fee.

Can I claim section 80C principal repayment benefit for the surplus amount parked in Max Gain?

The answer is NO. Only the regular principal repaid by you from your EMI as part of your loan amortization schedule is available for tax benefit under section 80C. the parked surplus amount is liquid money & you can withdraw it any time, hence it’s not considered as actual repayment of loan & thus not eligible for tax benefit.

Can I avail cheque book & ATM card for my Max Gain account?

Yes, as & when you‘ll demand these, SBI ‘ll offer you the same. In case you are already holding an SBI SB acct. linked ATM card, you have the option to link your MG acct. also with this existing ATM card.

Can I enroll my MF SIPs in Max Gain?

Yes but do note, there should be a surplus balance i.e. available balance on the date of SIP, else your ECS or SI mandate ‘ll bounce.

Can i pay for my utility bills, credit card payments, online shopping from Max Gain?

Yes, you can do all this & more. In fact it’s in your best interest that you treat your MG account as your primary money parking account & route all your transactions through it so that money is lying there for maximum possible time & thus helping you to bring down your interest outgo.

I used my MG account ATM card to withdraw cash from other bank’s ATM & I was charged the money very first time in the month. Why?

The reason is, as per RBI’s circular 5 transactions on other banks’ ATM are free only for SB account & in this case, you forget the point that your MG account is not SB account. it’s an overdraft account.

For an imaginary situation, my loan amount is 30L Rs. & parked surplus amount is also 30L Rs. Does it mean, my loan is closed & I can claim my property papers from SBI?

No, your loan is not closed. Only interest outgo ‘ll become zero & EMi ‘ll remain continue as it is. Yes the interest part of your EMI ‘ll keep on accumulating in your MG account. If you want to close your loan at this point, you w’d have to inform SBI in written & now SBI ‘ll adjust your parked surplus amount towards the outstanding loan amount. you ‘ll lose the liquidity of your money but loan ‘ll be over & now you can get your property papers back.

How can I transfer my loan from other banks to SBI Max Gain?

For loan transfer, first of all contact your existing lender & ask for following things.

Loan Account statement from day one.

List of Documents, which were submitted by you at the time of availing original loan. In day to day language of bankers, it’s called LOD.

As on date outstanding loan balance with applicable interest, penalty & any other fee to close the loan.

Now contact, the nearest SBI Branch (if you do have an existing SB account with SBI, it’s advisable to contact there for ease of operation). Inform in that branch that you want to transfer your loan from existing bank to SBI Max Gain. fill the application form, submit the necessary papers & SBI’s RACPC ‘ll do the back ground job.

Once SBI is ready to accept the transfer, it ‘ll issue you a sanction letter of the loan amount & ‘ll ask you to go for loan related agreement documentation work with SBI. If you are not having property insurance, SBI may ask to purchase one. Same ‘ll be the case for your life insurance. Once legal documentation is over, the cheque of the loan balance ‘ll be issued directly into the name of the bank in question. After the amount is credited to your existing bank, within next 20-30 days, you ‘ll get the original documents submitted by you, from the existing bank. Now you w’d have to submit these documents to SBI. In some states like Gujarat, Maharashtra, Karnataka, SBI may ask to go for registration of mortgage deed on your property in the office where your property was originally registered in your name.

SBI Max Gain

Normal Home Loan

Liquidity of your part prepayments is there

No Liquidity. Money is gone for ever, once you prepay.

A bit complex to understand

Easy to understand

For people who can generate regular surplus amounts

For people who can only manage regular EMIs

Click here to know the real life example of Mr. Sudhir S for SBI Max Gain.

Do you feel, this article was able to answer your all queries related to SBI Max Gain? Was this article helpful for you to understand the overall concept of SBI Max Gain home loan? Please feel free to ask for more help

I have written almost every possible article on Life Insurance and even Health Insurance, but strangely I still find a lot of investors asking questions which clearly shows that somehow, somewhere they do not understand what is the underlying business model of insurance business and how are the products designed overall. Let me use simple stories and recreate some examples which will show you how things work in any insurance business. Lets move on ..

I see a lot of people saying something like – “How can these companies offer 1 crore term plan by charging just a small premium of Rs 10,000. Its surely a racket!”

Then a lot of people still feel that insurance companies are cheats and they will not pay out when a claim arises, just to make sure that they do not have to pay a big amount from their pocket. I am not advocating any insurance company here, nor am I saying that I have a solution to your doubts. All I can do is share what insurance is all about. This should surely help you understand the business model of insurance companies and how they make money. You can then choose to trust the system or reject it. Note that In our 100moneyactions program we have one of the tasks as completing your life insurance and health insurance with basic support system, So if you have still not registered for it, do it now.

Insurance Centuries Back – Lets go back in History

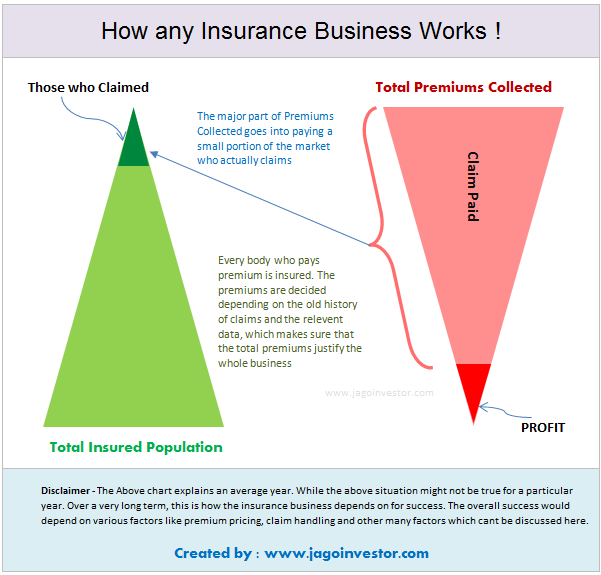

Insurance as a concept, is not a new thing in this world. It’s been in existence for centuries. Let me start with story which will give you some idea about insurance business and its evolution. Long back, there were businessmen all over the world, who traveled from one country to another for doing trade and business . They sent their stocks, inventories and material across globe on boats and ships. A lot of times when they used to send their ship from Point A to Point B, it so happened, that some ship drowned and everything on the ship got wiped out.

And this happened 10% of the time on an average. Out of every 10 ships which started from Point A, only 9 reached the destination and one businessmen almost surely went bankrupt. So you can see that the certainty was about the loss of 1 ship, but there was uncertainty about “whose” ship it will be (just like there is certainty that one an average 1-2 person will die in a city in accident for sure, but who will it be is not sure) .

So all the businessmen started to think over the issue and they found the solution. They started collecting 10% worth of the stocks from each of them, collected it in a bag. When each of 10 businessmen did this, the bag was full of money which would compensate any ship owner who was the unlucky one and lost his ship. If there was no accident and all the 10 ships arrived safely at their destination, there was no issue at all. But when there was a ship lost, the whole bag of money was given to the one who was affected, which meant that he didn’t suffer other than temporary shock and resentment.

So now if you see closely, you can relate this with insurance. These businessmen were doing nothing but mutually insuring their risk by pooling in the money (premium) and then compensating the unlucky business man in case of a disastrous eventuality (sum assured equal to 1 ship worth).