Do you want to invest in a mutual fund which has near zero-risk, offers returns in range of 6-9% with high liquidity and at the same time, they are tax efficient? Welcome to the world of “Arbitrage Mutual Funds”.

Arbitrage mutual funds are a category of mutual funds which are comparable to liquid funds or a pure debt fund whose returns are in range of 6-9% per annum, but from taxation perspective they are treated like equity mutual funds. These arbitrage funds have suddenly become very famous with investors after this tax budget, because the taxation on debt funds changed and became unattractive compared to past.

How does an Arbitrage mutual fund work ?

You should first understand the word “arbitrage”. In short arbitrage means – “simultaneous purchase and sale of an asset in order to profit from a difference in the price”.

Let me give you an example

Imagine that a person wants to buy a second hand phone and is ready to pay Rs 2,000 for it. You go to OLX and see that the same phone is selling at Rs 1,200 there. You then buy the phone at 1200 and sell it at 2000 and make the profit of Rs 800 . This is one example of arbitrage

Another example is gold. Gold prices are different in various cities. So there is a possibility that gold can be cheaper in bangalore compared to chennai and a gold dealer buys it from Bangalore and sells it in Chennai. This is another example of arbitrage

In the examples above, the problem is that the buy and selling happens at two different times, and hence there is small risk.

But what will happen if you are able to buy and sell at the same time? In that case, there is no risk, because instantly you are locking the profits (the difference price)

This is exactly what happens in Arbitrage mutual funds

In case of arbitrage mutual funds, the funds explore the arbitrage opportunities where the same stock is quoting at two different prices at BSE and NSE at the same time and they buy and sell in different markets and make the profits.

The other thing which an arbitrage fund does is use cash and derivative markets. For example, a stock might be available at Rs 100 on stock market, but it might be selling at Rs 104 in future’s market (if you dont understand derivative markets, thats ok , dont worry) and they make the difference as profits.

Lets not go to much into detail of how they work, as of now just understand that arbitrage funds use the arbitrage technique to earn the profits from the gaps in markets and its almost risk free.

Arbitrage funds returns are tax free after a year

So lets come to the biggest plus point of an arbitrage fund.

The biggest advantage of arbitrage funds is that they are treated as equity mutual funds, when it comes to taxation. Hence any return you earn after holding it for 12 months is tax free, and incase you hold it for less than 12 montsh and make any profits, the taxation is 15% (short term capital gains tax).

So, return wise arbitrage funds can be compared to a liquid fund and the returns potential are in range of 6-9% depending on the time frame and the yield of the instruments they have invested into.

Now think about this scenario

If you want to park a big sum of money for some months or approx one year, but you dont want to take a lot of risk on the capital and at the same time want a highly tax optimized solution, what are your options?

FD is not that great option, because if you are in 30% tax bracket, you will be paying tax at the rate of 30% and if you break your FD in between before maturity, you will also pay penalty. In that case, these arbitrage funds can be a very good alternative, because they can give decent returns, high liquidity and lower tax (no tax if held for more than a yr)

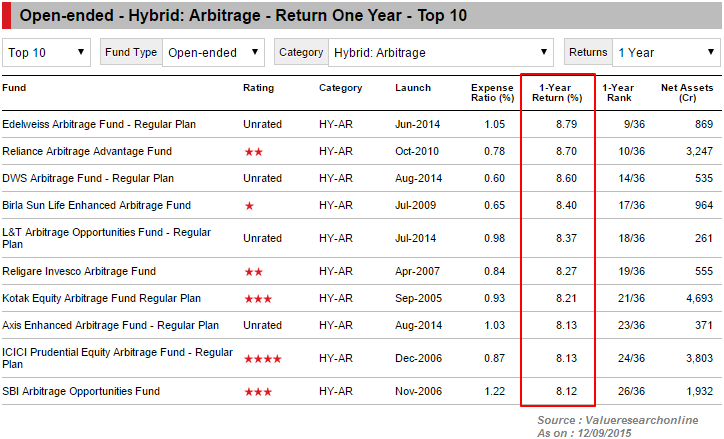

Below you can see some of arbitrage mutual funds and their performance over the last 1 yr (as on sep, 2015)

You will see that the returns from these funds have been in the range on 8%, which is quite good and comparable to Fixed deposits and liquid funds.

Are there any risk in Arbitrage Funds?

Yes, But more then risk, I would say these are some points which every investor should be aware about before they invest in arbitrage funds.

You should understand that arbitrage opportunities must exist if arbitrage funds have to perform better, means if the markets are uncertain, then good opportunities will exist for arbitrage funds and they will give decent profits, but if markets are not volatile enough, it might happen that the returns from arbitrage funds are unattractive.

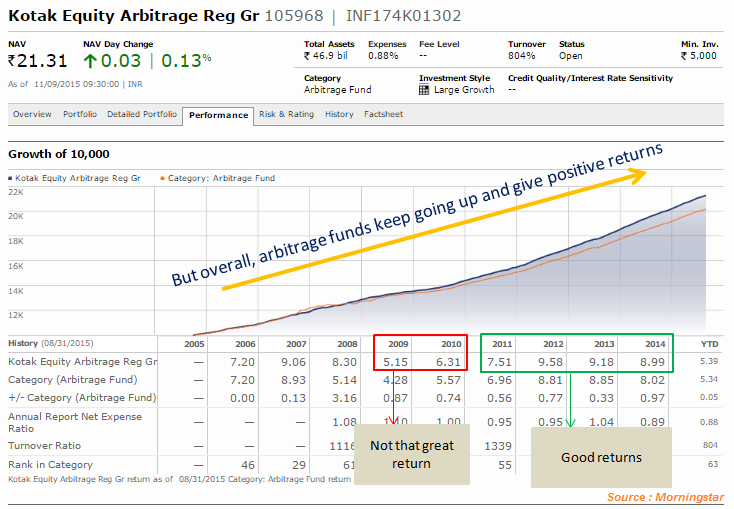

If you look at past 3 yrs returns, you will find that the returns have been very good, but if you go a bit in history you will see that they have not give the same kind of return always. See the chart below for Kotak Equity Arbitrage fund, a very good fund in that category

You will see that in the year 2009 and 2010, the fund has not performed well like it did in earliar years or after 2011. So be very clear that you cant expect them to return in the range of 8-9% always. There will be times when they will return 4% or 5%, but that happens rarely.

How liquid are Arbitrage funds ?

Lets talk about liquidity factor now.

You will often hear that arbitrage funds can be compared to liquid funds as they are highly liquid and risk free. So some extent this is very true, but if you go deeper, there are few differences.

Arbitrage funds redemption can take 3-4 days : An arbitrage fund redemption can take 3-4 days compared to just 1 day in case of liquid fund, so if your requirement is that the money should come back to you the next day if you want to redeem, then arbitrage funds are not the right choice.

Arbitrage funds have exit load for 90 days – Most of the arbitrage funds have a small exit load anywhere from 0.25% to 0.5% if you take out the money before 90 days. If compared to liquid funds, there does not exist any exit load and you can take out the money even in a week without any loads. For example, incase of ICICI Prudential Equity arbitrage fund, its exit load is 0.25% if redemption before 30 days

The above two points conclude, that one should ideally choose arbitrage funds if one is looking to park funds anywhere from 3 months to 2 yrs. Also someone who is falling under a lower tax slab, will not benefit too much from investing in arbitrage fund because anyways their tax slab is less.

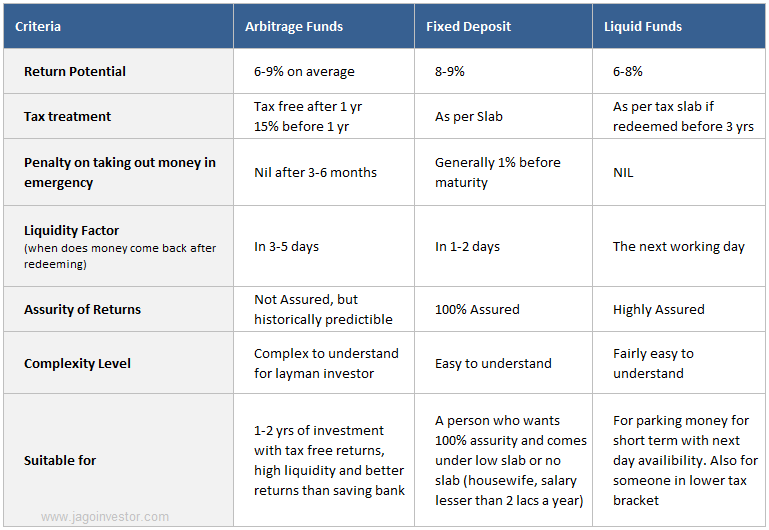

Comparing Arbitrage fund with Fixed deposit and Liquid fund

Finally, let me give a rough comparision of arbitrage fund with bank FD and liquid funds, which will make you more clear. The comparision chart below shows various criteria and how these products compare.

So shall you invest in arbitrage funds?

I think based on the above information, you can now take the call if you want to invest in arbitrage funds or not. Let me know what you are going to do and what comes to your mind about this category of mutual funds.

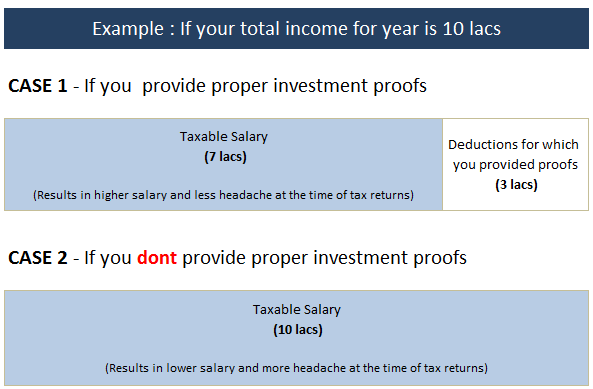

Do you know everything regarding investment proofs which you provide to your employer at the time of tax-saving season? If your answer is NO, then this article will help you understand a lot of things which you don’t know or partially know about.

So, I will talk about some of the common things you should take care while giving your investment proofs to your employer for tax saving purpose.

1. Investment declaration helps employer to deduct appropriate tax

The first and most basic thing, that you as an employee should know is that your employer is supposed to deduct your income tax on monthly basis and deposit it with govt on 7th of the following month.

For this, the employer should calculate your taxable salary and it can only happen if you before hand give him an idea about how you are planning to save tax, and apart from that how much of HRA, LTA, Medical reimbursements you are entitled for.

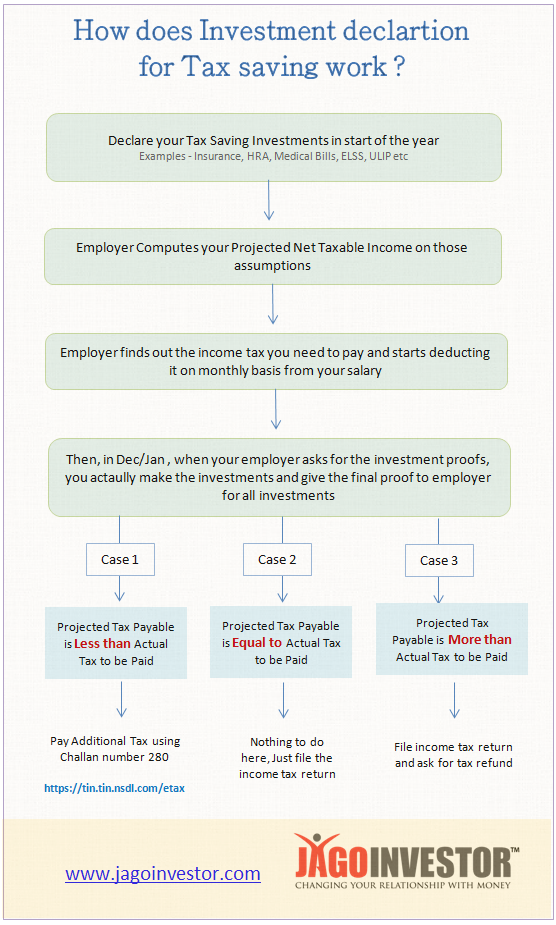

For this purpose, your employer asks you to declare your various investments in the start of the year itself, so that they can compute your net taxable salary and then pay your salaries accordingly, after deducting TDS from your salaries.

And then, finally around Dec/Jan, they start asking you to provide them the actual proofs of your investments and receipts so that they can match things with their initial calculations and if there are any difference they have 2-3 months in hand to handle the discrepancies. Below is a small example of it

What If you failed to submit investment proofs?

If you failed to submit your investments proofs (you declared them, but didn’t invest in reality), in that case you are liable to pay higher income tax, but employer has not deducted it and hence they get a 2-3 months of extra time to adjust it from your salary.

Following things are required by employer as investment proofs.

To claim LTA, you need to provide Travel receipts (flight boarding pass, train tickets)

ELSS investments proofs or any other 80C investments

Life insurance and health insurance premium receipts

Various donations receipts

Rent receipts to claim HRA

2. You can also share your saving bank interest, FD interest with employer

A lot of people do not know this, but you can share your saving bank interest, FD/RD interest earned during year, any capital gains from shares or mutual fund, rental income and other kind of incomes with your employer, so that they get a complete picture of your taxable salary and deduct your income tax which will be more accurate.

If you do not disclose these additional incomes to your employer, in that case – you will have to separately pay additional income tax yourself and then take these things into account while filing your income tax returns.

Note that another advantage of declaring these additional income with employer is that you will not have to pay any penalty which might arise due to not paying advance tax on time.

Also, you won’t have to take the burden of paying the additional tax at the end of the year, the tax will get distributed almost equally throughout the year.

3. Didn’t submit income tax proofs to employer? You can claim things later

A lot of investors have this myth, that if they didn’t do their investment proof submission to employer, they will never be able to claim the deductions and will have to pay higher income tax. This is not true.

Yes, it’s a good practice to give the investments proof to your employer on time, and that will save you a lot of headache later while filing the returns.

But for some reason, if you fail to provide the investment proofs (example, like you don’t have money in the month of Jan and you decided to buy a life insurance policy only in Mar), in that case – your employer will deduct the income tax, but then at the time of filing your tax returns you can claim the tax refund, if you finally managed to invest in tax saving products later.

Here is a chart which will give you a better idea

Here is another detailed example of how it happens

Ajay has the salary of 12 lacs a year, and he declares to his employer that he will invest Rs 1.5 lacs in 80C products

Employer based on Ajay declaration will calculate that Ajay taxable salary is 10.5 lacs and will be based on that suppose the total income tax for the year is 60k (just for example) . So Ajay final salary will be 10.5 lacs – 60k = 9.9 lacs. This 9.9 lacs divided by 12 will be 82500 which he will get on monthly basis and the employer will deposit Rs 5,000 as his tax to govt on monthly basis

Now in Jan, when the employer asks Ajay to give them the investment proof, suppose Ajay realizes that he forgot to make the investments and does not have money to invest 1.5 lacs in 80C products. But he will do it in Mar himself. And he fails to provide the income tax proofs to his employer.

Now his employer will come to know that Ajay real taxable salary is 12 lacs and not 10.5 lacs as declared by him and lets say on this his income tax is 1 lac, so additional 40k is to be recovered from Ajay, which will be adjusted from Ajay’s salary in Feb/Mar

Ajay then invests 1.5 lacs in Mar and finally his taxable income should be just 60k , as per the planning (because his taxable income is 10.5 lacs as declared in the start). However his employer has deducted 1 lac in total from his salary and paid to govt.

Now Ajay can declare in his tax returns that he has invested in 80C products and he is liable to get refund of Rs 40,000 which he will get in next few months.

In the example above, you can see that not giving investment proofs on time has resulted in some inconvenience for Ajay, but that does not mean that he will lose out on his tax benefits. One can always invest around the end of the year and then claim back the tax refund later.

However, there is one exemption here

Few exemptions are made only at employer level, like LTA and medical reimbursements. So if you fail to provide LTA and Medical reimbursements proof to your employer on time, then you lose the benefit. You can’t claim it back at the time of filing returns.

4. You DONT need to submit any proofs while filing your tax returns

Another important point you should remember is that while filing income tax returns, you just have to furnish the information about your investments, and not attach any investment proof.

Please do not attach xerox copies at all. It’s not required.

Its required by the employer because they are deducting the TDS and as a third party they need the documents for verification purpose.

But if you are claiming at all the benefits yourself at the end of the year, you just need to declare things. However note that you should keep the receipts and all the required documents with you for some years, because if their is any scrutiny later, you need to be prepared to answer income tax authorities along with documentary evidence.

Which means that you should never lie about your investments which you have not done in reality. Always provide true information.

5. You need to give “proposed investment” proofs for the month of Feb and March

A lot of people are confused on how will they provide the investment proofs for the month of Feb and Mar in Jan itself, when the employer asks for investment proofs. It might happen that your life insurance premium is due in Mar or if you are doing SIP in ELSS funds, you still don’t have the statements showing the investments.

In those cases, you have to provide a declaration that you are going to make the investments for Feb/Mar and based on that declaration, your employer will process the TDS.

All the employers provide you with the declaration form. You just need to write there that you promise to do the investments for tax saving in next 2 months and your exemptions should be given to you based on your declaration.

Let me know if you have any questions or if you want to share some important information on this topic

I recently inquired about one of the plot schemes near Pune and finally visited their project. They sent a car to pick me up. When I reached the site, the staff there sounded very professional compared to some other experiences I have had in past.

While I had a good experience interacting with the sales person on the last project I visited, I realized that often that does not happen with many people. A lot of education needs to happen on this topic, because many investors who go to meet brokers for the first time or to do site visit are lured by some tricks and fooled a lot of times.

So I have created a list of points, which I want to share with all the prospective home/plot buyers. Some of these points are tricks played by agents, and some points are suggestions on what you should do when you meet a builder, broker, agent or sales executive who is showing you or explaining about a project.

Here are those points one by one. Detailed description of these tricks can be seen after this table.

[su_table responsive=”yes” alternate=”no”]

Trick #1

They create artificial scarcity and try to rush you

Trick #2

Don’t show the eagerness to buy

Trick #3

Don’t get mesmerized by Sample flat or Jazzy brochure’s

Trick #4

Ask for the legal documents and regarding the basic amenities

Trick #5

Say that you are seeing other nearby projects as well

Trick #6

Don’t be tempted with awesome deals and discounts, they are well designed

Trick #7

Ask which all banks have approved the project

Trick #8

Don’t get over obsessed with the “upcoming infrastructure”

[/su_table]

1. They create artificial scarcity and try to rush you

An year back, I got an email from one of the builders with the list of available flats, area, price per square feet and final price of the flat. Out of 600 flats in the project, Around 90% of them were marked as “SOLD” or “BOOKED” .

Just by looking at that, I got a “left out” feeling. It appeared as if everyone in this world is owning the plots and flats and its just me, who will be left behind. A voice from inside said – “Go, book that plot NOW, else you will regret all your life”

I had no way to verify if they were really sold or booked by someone. I just had to rely on what the excel sheet told me. This created a sense of emergency. The feeling I got was – “I need to hurry, else I will lose out on the opportunity”. Almost 80% of the time, this is artificially created by the sales executives.

See the table –

If a sales executive tells you that you have a week’s time, multiply it by 10. That’s the time you generally have in real life. Some of the things you will hear from sales executive will be as follows

Sir, All the 2 BHK are sold except 3 units. You will either have to book it in next 10 days or go for a 3 BHK (they know you don’t have the budget for 3 bhk)

Sir, 58 flats are booked already in the pre-launch. This price is only for this Diwali after, which it will go up by Rs 300 per sq

This price is only available for this exhibition because of pre-launch offer, once the “actual” launch happens, the rate would be at least Rs 100 more per sqft.

At times, you might really lose on some good opportunity in real life, but maximum number of times – its a sales trick. This is exactly the reason why they generally ask you to come along with cheque book, so that in order to not lose the opportunity, you will book the property right there and then by paying a token amount.

Note that this trick of creating emergency is a general sales trick and applies everywhere.

2. Don’t show the eagerness to buy

If you are seriously looking forward to buy the property and want to get a good deal, then do not show your eagerness to buy. Hide that over enthusiastic and needy person inside you.

Hide your temptation and do not show that you are dying to buy the property. The moment they sense, that you are already sold out in the game, it will be very hard for you to negotiate on pricing and other things, because they are very sure that you will not be stopped by minute points.

The agents/sales executives are paid commission on closing the deal and they will go to an extra mile to close the deal with you. Show them that you are not in hurry and your life does not depend on the property. Show them that you are a serious buyer who is not in hurry and if they have to win you, you will require a good incentive to invest money.

They will ask you for booking amount, token amount, they will give you “last date”. But don’t take a decision in hurry. Do all your investigation, scrutiny, and think on how you will arrange the money. Here is a nice comment from someone on the Indian real estate forum

Fully agree. Don't negotiate with fear in mind that this is your last chance, and so far nothing worked for you (frankly, if you have this fear, would suggest don't even bother to negotiate, and more so don't get into RE market). Be prepared to walk away right from the beginning. Don't buy builder claims that they are going to increase rates, all flats except one sold out, they have enough cash, etc.

Show them you are not emotionally attached and this is one of the many options. Also, don't close deal in first meeting (if you do, most probably that means you did not negotiate enough). Last but not least, you have all the negotiation power before handing over the money, once you pay them, your negotiation power is zero.

In general one who pays should be enjoying greater power, in reality we don't see that in RE market, more so in Pune RE. That was easy said than done, have tried it, and it works, key is patience.

As I said in the first point, most of the times the emergency is not real, its often the created one!. However, this does not mean that you delay things beyond limit, thinking they will come back to you all the times. If there are other leads who are ready to buy the property, you will not be contacted beyond the point. So keep a balance

3. Don’t get mesmerized by Sample flat or Jazzy brochure’s

Human visualize and fantasize about everything in life

This is the reason when you see jazzy brochure’s, the lush greenery, clean atmosphere and a world beyond reality, you visualize yourself living in the serene beautiful place which has no traffic, no tension and a all perfect life. I am yet to meet anyone with whom it has really happened 🙂

Please, do not do any booking only on the basis of the brochure, some presentation or looking at a sample flat.

Make sure you visit the actual project site and see the location, how well connected the area is city, how are the roads, what’s nearby the place and other important factors. A lot of people book properties in real estate expo and exhibition, which I don’t think is a good idea at all.

Real life example

I once met a sales representative who came to explain me about a project in WAI (near Panchgani, Maharashtra) and he sold a story which looked so amazing, that my inner self-was ready to book the property right then and there. I was so excited to take a look at the site.

However after a week, when I actually visited the site, all my excitement died because the reality was so different than what I had visualized. I must mention that it was not the sales executive fault here and he had not given any wrong information. In fact, he was a brilliant sales person and very professional.

The problem was me myself. I have over-estimated the greatness of the project and its location, because of the jazzy brochure.

In case of residential flats, remember that the jazzy brochure and the sample flats are created to exploit the human imagination and sell you dreams. What you actually get in reality will not be exactly like sample flats you see.

You won’t believe, but there are professionals who are hired by builders to give mesmerizing presentations to prospective buyers, especially NRI. Presentations are arranged in 5-star hotels and bills are paid in lacs of rupees. Here is one gentlemen explaining how it happens. Please see the video below

I am not saying that brochure’s are not important. They surely play a big role in marketing and you get a very good idea of what is the project all about, but go beyond that.

Judging a property by just looking at brochure is exactly like hiring an employee by just looking at resume.

4. Ask for the legal documents and regarding the basic amenities

You are probably doing one of the biggest investment of your life-time. Right?

If your buy something which is junk, you will regret it all your life. There are millions of people in India, who are dealing with legal issues today because the land they bought is disputed, the required sanctions were not taken and many other issues. So just don’t feel shy about asking legal documents. There is no hurry in doing the agreement.

Simply ask the sales representative to provide you all the legal documents, sample agreement copy and all approval related documents. For god sake, take the documents to a property lawyer and pay Rs 10-20k fees to consult him, before you buy that 75 lacs flat!.

The lawyer will check the documents and help you understand, if the project is totally fine or has some big trouble. Then you can take the decision of moving ahead or not.

It will save you a lot of money and energy in future. It’s not a very healthy sign if the sales person is constantly avoiding the conversation regarding legal documents or if he is hesitant in providing you a copy of the agreement.

Ask about surrounding area and the development coming up

Apart from the legalities of the project, you also need to inquire in detail about the surrounding area and what all development is coming up in future. Ask things like

Is some flyover planned?

Is some college coming up?

What kind of markets are nearby?

How far is bus stand?

How far is the main highway

From where will the water connection come?

What about electricity connection?

While you might not be able to verify a lot of things, but at least you can know about the basic amenities. Things like water is really a cause of concern

5. Say that you are seeing other nearby projects as well

Before you go to the project site, inquire about the other projects near by. At least, go to the websites of those projects and memorize the names, location etc. If possible inquire on phone about their rates.

Then, when you are talking to sales representative, share with him about all this. Let him know that you are an informed investor and if he has to win you as customer, you should be offered a good deal.

I can assure you, there is always a possibility of Rs 25-50 per square feet discount if you ask for it 3-4 times. Tell them that you had heard about the lower rate from one of your friends or tell them that someone else from their sales team had called them and shared about the lower rate few weeks back and that’s the reason you are inquiring. The sales person always has that much margin in his hands.

The big boss always tells them – “If you see that customer will go away, offer him up to Rs 25-75 discount per sqft, but only in worst case”. There is nothing wrong in asking, the worst case is that you will not get it.

6. Don’t be tempted with awesome deals and discounts, they are well designed

So the builder is giving you are modular kitchen included in the flat? WOW .. Who is paying for it? Definitely not you! . Come on! .

It’s all included in the price. Instead of 49.5 lacs, he is charging you 50 lacs and giving away the free modular kitchen worth Rs 50,000. What’s so great about it?

Some builders in premium segment also offer a car along with the house. Book a Villa and get a car. Sadly, that means “My project is not able to sell, here is my last trick on you by offering you a bait”

Trust me, If I were a builder who is selling a 4.5 crore villa, I can also come up with such offers. Increase the price and give the car along with it. At the end, its the customer who pays the price.

Understand that whatever you are getting is funded by your money only. No one in their right mind, will give any kind of discounts or offers because they have a big heart. It’s all money game. It’s just a way to emotionally exploit you and make sure you feel great about yourself. Just because its bundled offer, it looks very good.

7. Ask which all banks have approved the project

A good way to filter a good project from a bad project is to see if its approved by many lenders or not. If all major lenders have approved the project, its a sign that the basic level checks are done by lenders and you can now trust the project more. It does not mean that you should not do your homework further, but the primary level of investigation is done.

If a project is not approved by any lender or some not so famous lender has approved it (just a single one), there is a possibility that something is fishy.

Probably some approval is not taken care of, or may be the land is disputed. You should also ask them if they have a good crisil rating. Go and check the pdf on crisil website for that project.

I lot of small time builders offer their own EMI scheme like pay 20% now and rest in EMI for 5 yrs . This happens a lot in plots especially very far from city. I am not saying that they are bad always, but you should be a bit cautious with them on legality factor.

8. Don’t get over obsessed with the “upcoming infrastructure”

There will be lots of promises (real and fake) made to you. You will listen about the lots of development projects, the ring road passing from that area, the grand temple coming up, the new wide road which is planned and many such things. Some of them might happen in reality, but not always.

A lot of plots schemes are sold as “Proposed NA” status (which means soon it will be approved for residential purpose) and the agents will tell you that they have put an application to convert the land from agricultural to Residential which will take just 1-2 yrs.

But don’t believe them blindly. Converting a land status is a big task and in most of the cases, it might take 10-20 yrs time or it might never happen. A lot of investors are stuck with the plots paying huge money which they cant use. Don’t take decision in hurry.

Take your decision with caution

Real estate is a complicated investment and a lot of factors decide if you are making a right investment or a wrong one. As its one of your life biggest financial decisions, make sure you do not hurry and take your time. Everyone is there to make money out of you.

I would like to hear about your experience and what you have faced in life with different real estate agents and builders. Please share your unique learning which can help someone else. I would like to keep adding more and more experiences and tricks which you will share with me here in comments section.

Are you RICH or not? Do you have enough income or networth, so that others will consider you RICH in India? This is all this post is about.

I was day dreaming about get RICH few days back (I do it every week) and visualising how much should I earn so that I can call myself as RICH and how much net worth I should have, so that people would start considering me RICH? Is it 1 crore or 10 crore ? Is income of 5 lacs a year or 20 lacs will make me look RICH in others eyes?

So, I created a survey around this topic and 381 people took that survey. But before I share the survey results below, note that the group which took this survey does not represent the common man on street. This survey is mostly taken by net-savvy high-income earners, which only represents the higher income group. These people are on web, work in big companies and are considered to be doing very well in life by society.

How much Income makes you RICH ?

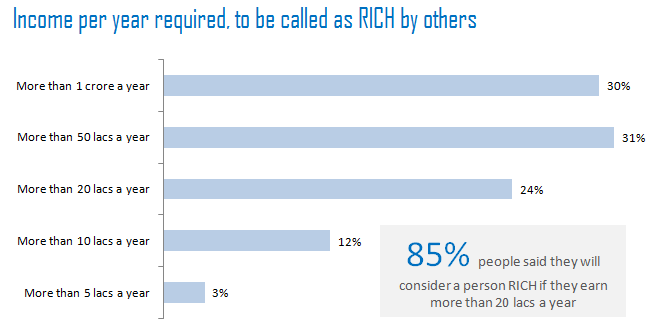

One of the questions asked in the survey was – “In India, How much yearly income one should earn, so that you will call him RICH ?” . Below are the results

As you can see above, only if you are earning more than 20 lacs a year, most of the people will consider you as RICH, otherwise you will be seen as middle class which is a very big range and not defined at all in our society. People earning 1 lac a year, 5 lac a year and 12 lac a year – they all call themselves as “Middle class”. Let me share some important stats with you on income.

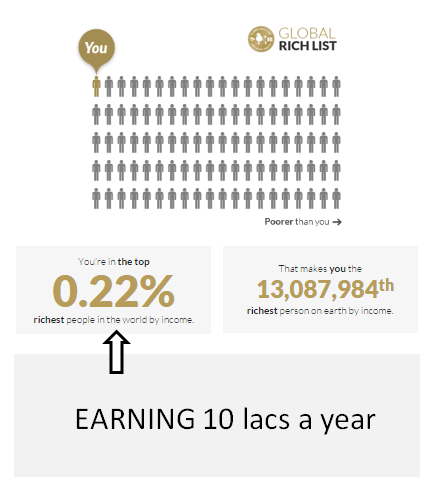

As per a website www.globalrichlist.com if you earn the income of 10 lacs a year, you would be in top 0.22% of the population globally. Can you believe that !

This means that if there are around 1000 people in the world, almost 997 people earn less than you if you earn Rs 10 lacs a year. Hence, you should be quite happy about this fact, but obviously we don’t think that way. We look at people above us and keep cursing how bad we are doing in life.

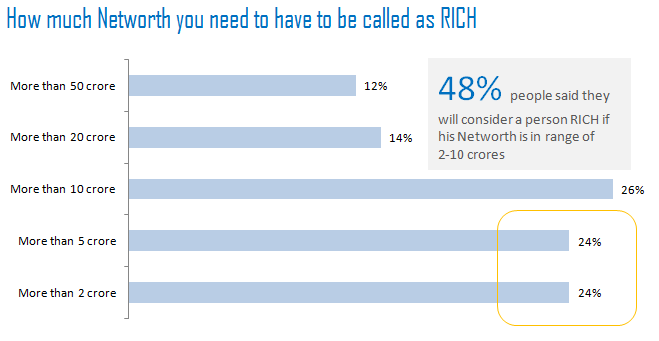

What networth makes you RICH in India in other’s eyes?

The next question I asked was – “In India, How much networth a person should have, so that you can call him RICH ?”. Below were the results

If you look at the chart above, only 1 out of 4 people will call you RICH if you have 2 crores of networth in today’s value. 48% people who took the survey feel that anything above 2-10 crores is a good networth to be called RICH. Some even said 50 crores and 100 crores.

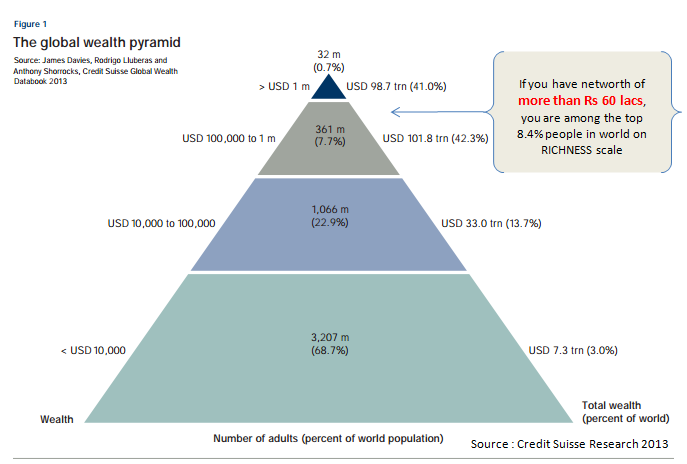

Forget crores! . What if you have a net worth of 100,000 Dollars or just approx Rs 60 lacs in wealth ? How rich are you?

As per a research published in 2013 by Credit Suisse, if your net worth is above Rs 60 lacs, you are among the richest 8% in the world and richest 0.4% in India. Think once again !

Out of every 1000 people in country, 995 people are below you in terms of net worth. I know some will say, that there is black money and many are there who do not disclose their income. Yes – that’s true, but we can’t find out how many are there like that. Even if you consider that, still you would be doing very very well. Below is the snapshot from the report.

Note that – we are not talking about ASSETS here, but Networth, which is ASSETS – LIABILITIES. A lot of people hold real-estate whose value they consider, but they forget to account for the home loan and other liabilities. So a lot of people who feel they have high net worth actually don’t have it.

Along with most countries in the developing world, personal wealth in India is heavily skewed towards property and other real assets, which make up 86% of household assets.

- Credit Suisse Report 2013

But feeling RICH is a state of mind

I know a lot of people will say that “feeling rich” is a state of mind and we should not just evaluate it with money. Agree to that. I am of the same opinion that it’s not others who will decide if you are RICH or not, but only YOU.

But thats not this article is all about. We are purely look at how others perceive your RICHNESS by income and your wealth.

Most of the people are not happy with their current status

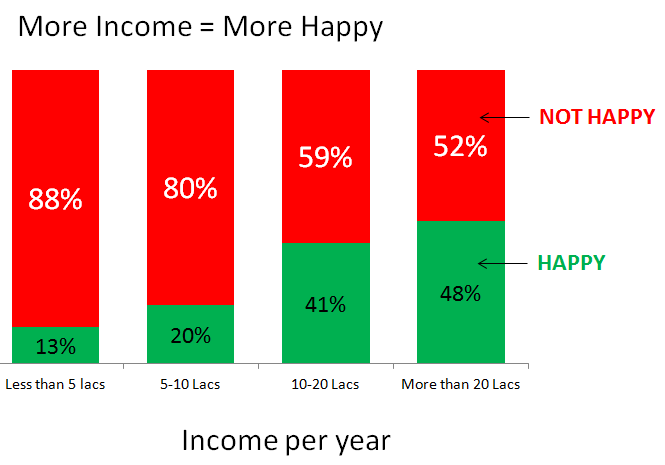

Let me give us some interesting information. If you have low income or networth and you are not happy about it. You should know that majority are like you only, even though they are on high income.

I asked another question in the survey – “Are you happy with your current Salary and Networth ?”

Guess what was the result?

On an average, most of the people are not happy if they are earning less than 10 lacs a year. I can understand that 10 lacs a year is not a very high income these days, especially in big cities. And if you consider the expenses, home loan EMI, education costs and lifestyle expenses, a lot of people are literally struggling to keep pace with rising expenses.

What looks a great salary to people in small cities, is not that amazing in big cities these days. Here is the result of survey, showing you how many people are happy or unhappy about their current income and net worth.

If you see people in higher income bracket which is more than 10 lacs a year, almost half of the people said that they are happy and another half said they are not. But one thing is very visible that in the higher range of income, most people said they are happy (I am not sure if they are really happy or not, but they said they are) compared to the people in lower range of income. To some level, we all can relate to it.

You are doing well at absolute level

After I did this article, I got a feeling how much our lives have got messed up due to money. We are literally lost in this world with the sole objective of earning money. You should be more happy about what you have achieved and not be unhappy about what you have not earned.

I am not saying that you should not be aspirational. Surely, you should have a higher target each year, but dont feel unhappy about what you have created till date. Let’s slow down a bit.

Wealth is important, very important, but also cherish and be proud of how you have done well till date compared to millions of others who are struggling in life due to money issues

You are way ahead of majority. Congratulations for that.

Let us know what you think about this whole article. What are your thoughts on who is RICH? What’s you definition of RICH in your own terms?

I am sure you must have shopped online very recently. In last 5 yrs, the whole dynamics of shopping has changed, We have more online for most of the things ranging from electronics, clothes, groceries and even movies ticket booking :).

We are fascinated with the discounts and offers we get online. However I am sure even if you know a lot of tips of saving money online, still you might not be exploring its full potential.

Hence, I am going to list down various points and how you can save more money. Detailed description of these points is after this table.

[su_table responsive=”yes” alternate=”no”]

Tip #1

Install Buyhatke extension

Tip #2

Go a bit extra mile in search for Coupons

Tip #3

Get cashback with specific credit cards and debit cards

Tip #4

Wait for the special days like Diwali and New year

Tip #5

Use Comparison Websites to find the best offer

Tip #6

Set Price Alerts

Tip #7

Leave items in your cart and wait for few days

Tip #8

Use wallet payment methods like paytm, mobikwik and payumoney

Tip #9

Use different emails for Shopping

Tip #10

Get extra cashback using Cashkaro.com

Tip #11

Industries like airlines and hotels give huge discount to there old customers

Tip #12

For used products you can get huge discounts on OLX, Quikr websites

Tip #13

Check prices on website pricebaba.com to know which brand is selling at discounted price or on MRP

Tip #14

To get the best deals keep checking the offer section of all website before you shop

Tip #15

Register on websites where users post great deals & discounts from here and there

Tip #16

Don’t get into the trap

[/su_table]

1. Install Buyhatke extension

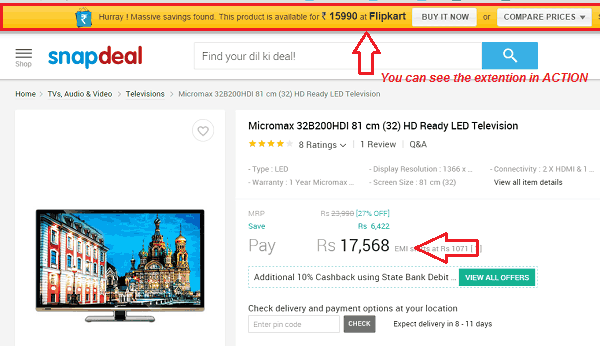

There is this website called Buyhatke.com which offers a chrome extension, which shows you the other website where you can get the best deal while you are looking at some product.

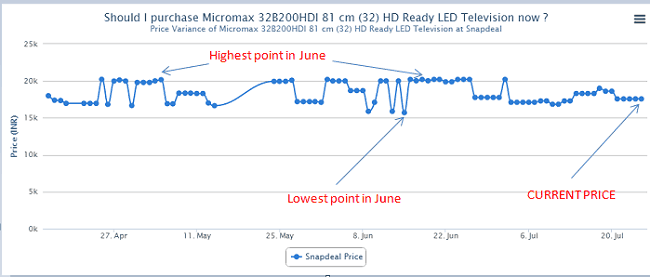

Below you can clearly see, when I went to Snapdeal to find the price of its one of the LED tv, the price it showed me was Rs 17,568. However, the buyhatke extension at the top showed me that the same product is available for Rs 15,990 on Flipkart.

I didn’t had to go anywhere to compare the price. The extension automatically searches the best deal and show it to me. You can also compare the prices of the product by clicking on “Compare Prices” tab on the top right.

However note that the extension does not take into consideration all the coupons and cash back. So take the decision after factoring in all those points.

Another amazing feature of this extension is the historical PRICE changes which you can see on the same page a bit below the product description (automatically it comes when you use the extension). You will be able to see how the price has changed over previous few months. You can see the maximum and minimum and judge if the current price might fall further in coming days or it can do up.

2. Go a bit extra mile in search for Coupons

This is the most basic thing you need to do when you are buying online. Sellers know that coupons are a great way to excite customers and make a faster sale by making buyers feel that this is the best moment to buy. Given the huge competition in the e-commerce space, every other company wants to give you a great deal somehow. Either the web site from where you are buying something may show you the coupon or you can find it on coupon sites.

On an average, I have always found some of the other kind of coupon which reduces the price by at least 5-10% . Some websites can have a variety of coupons depending on various categories (20 category = 20 different type of coupons). Something like “Buy above Rs 1,999 and get 20% discount” applicable on furniture.

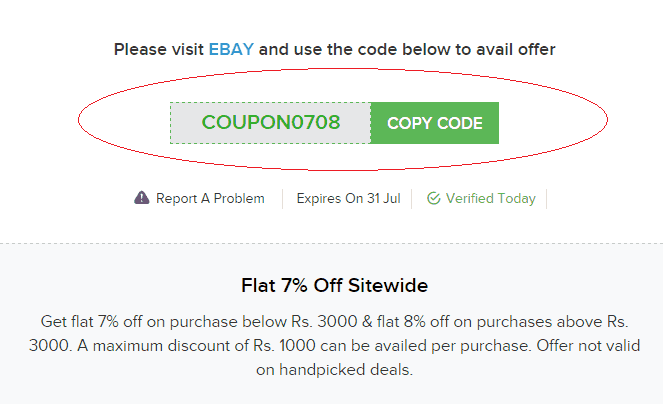

Then there are websites like Ebay, which have generic coupons like “Buy above 750 and get 7.5% discount”, These coupons are easily available on the majority of the coupon websites.

I know most of the people who buy online do search for coupons, but I don’t think a lot of them go an extra mile to search for the best coupon and settle with the first one which they get. If you are buying an item with a high price, it’s worth the effort to spend extra 5 min to search for the best coupon available. You can keep applying 3-4 coupons and see which is giving you the best deal.

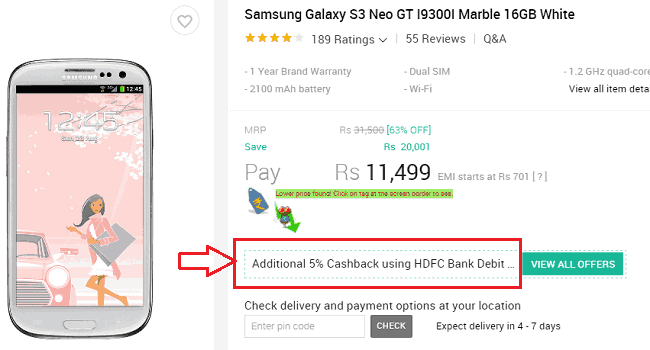

3. Get cashback with specific credit cards and debit cards

At times, you can get a good cashback or discount on paying from a specific bank credit or debit card. Banks tie up with the website, so that maximum payments go through their channel. This can be for marketing purpose or just to increase the sales of a particular credit or debit card.

Like Amazon may be giving a 10% cashback when you purchase by an SBI debit card or Snapdeal providing an additional 5% cashback on HDFC debit card

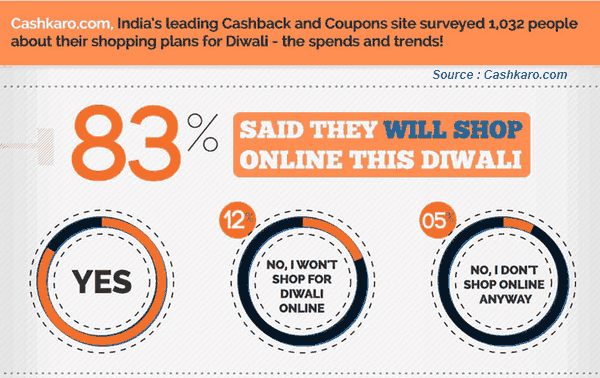

4. Wait for the special days like Diwali and New year

There are extra discounts and offers during Diwali, New year and many other Indian festivals. If you can wait and postpone your shopping, its always recommended to wait for these days, especially Diwali. Its a known fact that people in India buy high ticket items because of the auspicious festival. You might get a much better deal and cash back offers given the cut-throat competition between e-commerce companies in India.

Also, there are events like GOSF (great Indian shopping festival) where you can get good deals (not always). Last year, I made the same mistake. I upgraded my TV in the month of Aug and didn’t wait for Diwali and saw the same TV selling at 15-20% extra discount. If you can wait a bit, it’s always better to plan your purchases, especially high ticket purchases.

Another great benefit of waiting for some weeks or month is that you may realize that you actually don’t really need the product and it was a decision in haste to buy the product.

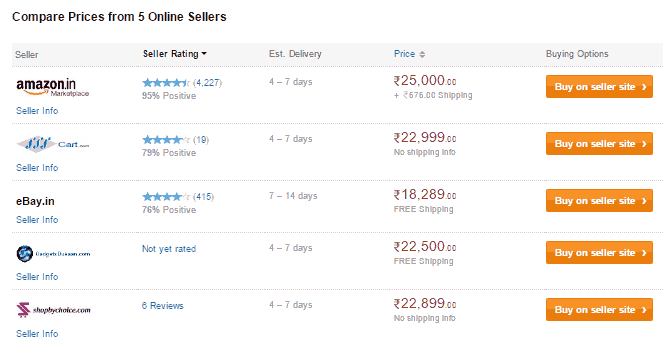

5. Use Comparison Websites to find the best offer

There are various websites like Junglee.com, mysmartprice.com and shopmania.in (and many others) where you can compare the prices of a product on various websites at one single place. You can see their shipping cost, estimated delivery time and also the rating of the seller.

It’s one window from where you can choose the website you want to buy from. At times, there is some mismatch in the main price on the website and the one shown on the comparison website. Below is how it looks like..

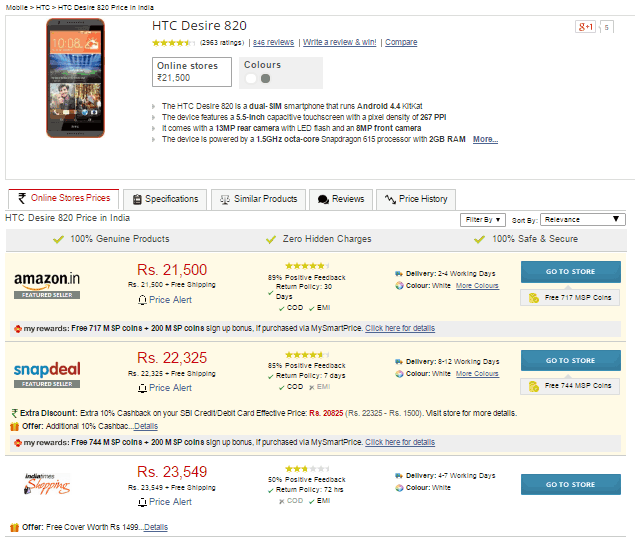

Mysmartprice gives a comprehensive comparison with various details and also the facility to set the price alert at the website level. It also gives section for price history, specification etc in a single page. Here is the snapshot

Scandid and pricebaba are some other good comparison websites you might want to try.

6. Set Price Alerts

At times, you are not in a hurry to buy some product, but you never know when the price of a product was reduced to a level where you become highly interested in purchasing the product. So in that case, you can set a price alert for a particular product and when it touches that price limit, you will be informed about it over an email

For example, if you want to buy a product which costs Rs 5,000 at the moment, but you are very sure that its price will come down to Rs 4700 and that time you would buy it, then you can set the alert and you will be informed about it.

How to set up the price alert?

You can use cheapass.in to set the alert. Just paste the url or the product and your email and your price alert will be set up

You can find the product you want to track on Junglee.com. You will see a “Set price Alert” link just near the product name.

7. Leave items in your cart and wait for few days

This trick might be working only with few websites and not all, but it’s still worth the try. You can first add all your items in the cart and then don’t check out. Just leave the items there in the cart. This is a big issue for e-commerce websites where the customers add the products to the cart, but at the final stage do not make payment and leave.

In technical term, this is called “shopping cart abandonment” and for most of the websites, its one of the biggest pain point, because a huge amount of sales is stuck there in the abandoned cart. As per the business insider report, globally out of every Rs 100 worth of products which is added to cart 71% is abandoned, means more than 2/3rd sales which can potentially happen, do not happen.

So, various companies in order to close that pending sale, will remind you about your cart and ask you to complete the sale. And some of them will often try to lure you with some extra discount with coupons etc. In the best case, you will be able to save a bit more and in the worst case, you won’t save anything extra.

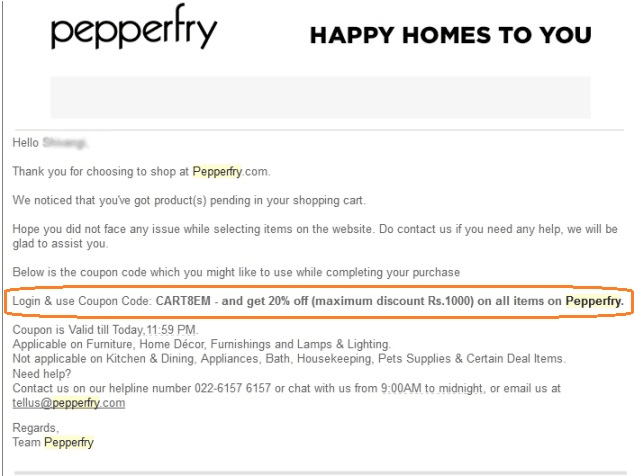

Below is a sample email from pepperfry which was sent to some customer who didn’t complete the sale.

Note that this trick will mostly work for new customers who have recently created their account, because companies are in the race to acquire new customers to show it to their VC on how they are growing. So do not expect this will well know and big websites where you are already buying from many months or years.

8. Use wallet payment methods like paytm, mobikwik and payumoney

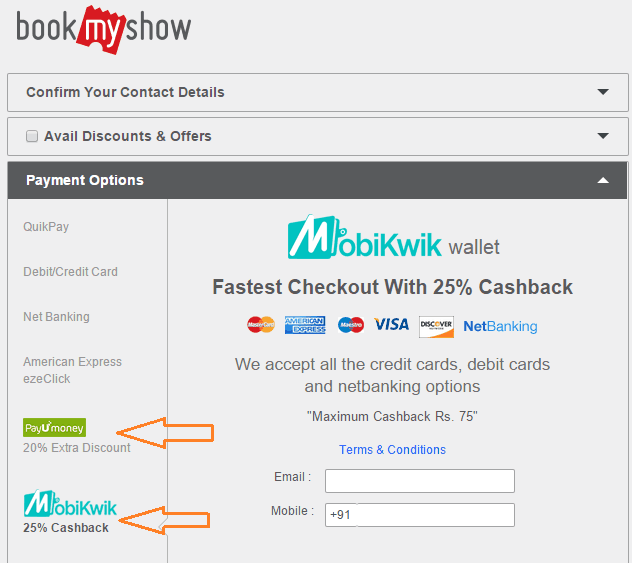

On top of your regular discounts which comes from coupons, you can also get additional discounts if you use the e-wallets these days. If not discount, you will surely get some kind of cash back. The best example, I can provide is from bookmyshow website where you get the extra discount when you use movie tickets.

Pro TIP for Bookmyshow: If you want to book X tickets and each ticket cost is as high as Rs 200-250, book 1 ticket X times, that way you get maximum cashback :). Just that you need to make sure you be fast enough to book all tickets you need.

9. Use different emails for Shopping

Almost all the companies offer some kind of discounts to new users. A lot of them offer coupons codes on email when you register for the first time. You can see this clearly on Foodpanda or Ola Cabs, where you get huge discount being a new user or get a FREE benefit for the first time.

A lot of companies are now offering the bigger discount if you order things using their mobile app, but you can’t use multiple phone number’s unlike emails, so that’s not easy enough. But if you have many people at home with smartphone’s, you can take this benefit too, for some limited time.

10. Get extra cashback using Cashkaro.com

On top of all the discounts you get, you can also get some cashback if you buy things from cashkaro.com links. Its a website where you have to create an account and then use their links to visit the actual website where you want to buy things.

This way, cashkaro website gets the commission from the seller and they share a part with you and it accumulates there. You can take the money in your bank account via NEFT once it crosses a limit. Below is a simple video which shows you how it works.

There are some industries like airlines and hotels which shows dynamic pricing to their old customers based on their history and location using your cookies. So if you use Incognito mode in the browser, they will not come to know that you are an old user and treat as a new customer.

At times, you might want to check websites like Olx and quikr because you can get the same product at a very heavy discount, but for a used product. In some cases, it might fit your requirement and you will save a good amount

You might want to try out websites like pricebaba.com which can find out a better deal for you from an offline store. so you can compare prices online and then inquire for prices offline. This would work out for those products, where you are not getting any kind of discount online and its selling near its MRP.

Almost all the websites have their own offers and deals pages, you can keep a watch on those pages too. An example if a offer page from flipkart or the deals page on ebay

You can register on the website called Desidime.com, where real users post great deals and discounts they find here and there. You can also interact, ask questions to other users.

Last and more important tip – Don’t get into the trap (16th)

Now the last and the final point. All the tips which are mentioned above would be helpful and in your interest if you don’t lose control over yourself and be a responsible buying. Only buy things which you really need. These discounts and coupons are just extra benefits.

Don’t let these coupons and discounts become the carrot for you to buy things which you just don’t need. The sad reality is that, even though you feel that coupons are benefitting you, it’s actually helping sellers more.

These coupons and discounts are often funded and sourced by the sellers only to make sure they increase their revenue’s. Yes, in some cases, it will surely benefit the customer’s, but at a higher level these are mainly the marketing tricks of the seller and nothing more than that.

Let me take an example of Foodpanda, If you had to order food from outside, then foodpanda coupons are the added discount you get. But a lot of people are now using foodpanda on those days, when they didn’t had to order from outside, but just used it because there was a discount. Can you see how these deals manipulate your behavior and your way of spending?

Don’t browse for fun

Doing time pass on e-commerce websites is not good for your wallet :). The basic principle of economics is that “Supply creates its own demand” and with the mobile apps retailers are trying to create an ecosystem where you can purchase on just one click. With discounts, they are creating an environment of instant gratification and by giving money back guarantee and replacement guarantee, they are removing the fear for online shopping.

But the at end due to all these factors, people are buying things which they just don’t need at all and creating the big pile of junk at their home. So just make sure you do not browse for fun, because you will surely come up with some reason on why you need that product you just saw.

Let me know what do you think about this article? Also share some more tips which you personally use and you think can be shared with others as well 🙂

We see most of the investors having a complex and bad financial life mainly because they have done a lot of mistakes when they started their financial life, which I think should be minimized by learning from other investors mistakes.

So we are listing down 4 common mistakes which most of the new investors make when they start their financial life.

Mistake #1 – Buying products only for “saving tax”

I have experienced the power of “tax-saving” season in an investor’s financial life. When I was into my first job, the cafeteria and the reception area was filled with my employee’s sitting with some agent or advisor with various kind of forms all over the table.

The tax season was on and all the people were busy “arranging for the investment proof” and not investing their money. Especially the new employee’s who had no idea about anything and they followed the herd to save tax.

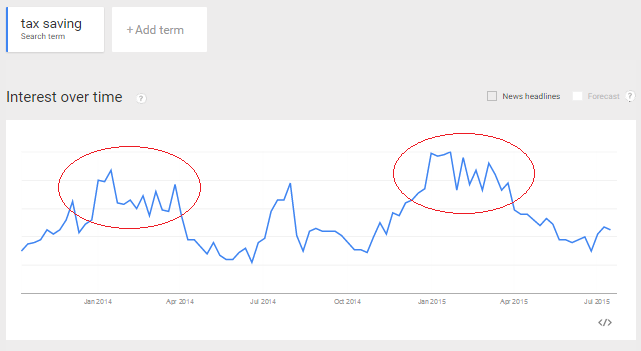

Below is the google trend showing you, how most the people starting thinking about the “tax saving” only in the month of Jan/Feb/Mar when they got emails from their employers. The search trend clearly shows that.

Only after many years, people realize that they have not done great justice to their money and invested mainly for instant gratification of saving tax. If you are a new investor, I suggest do not get carried away and only think about saving tax.

I know tax saving is important and one has to do it, but do it meaningfully.

Explore what all options you have and which one them will align well with your long-term goals and then invest in those products.

Mistake #2 – Waiting for the “right time” to invest

When we work with our clients, we observe that one of the biggest regrets, they have is that they didn’t start their investments early in life and lost the valuable time. A person in India spends close to 20 yrs in school/college and most of the students have seen a lot of struggle around money, because of which all their early life, they suppress their desires. They never freely spend money on anything and keep waiting for that D-day when they will have no restrictions around money. The first salary is nothing less than a big jackpot.

The first few months when they see a lot of money in their account, is the time of celebration and fulfilling all their wishes they had from years. There is nothing wrong about splurging, spending and enjoying it all. But some people extend it over many years and over-do it. When it comes to investing their money, they say that they dont save enough after their expenses and once their salary increase, they will invest then.

In short, they keep waiting for the “right time” and it never arrives. Because the nature of money is such that, the more you earn, the more you will spend and your lifestyle will keep changing its shape to fit in your salary.

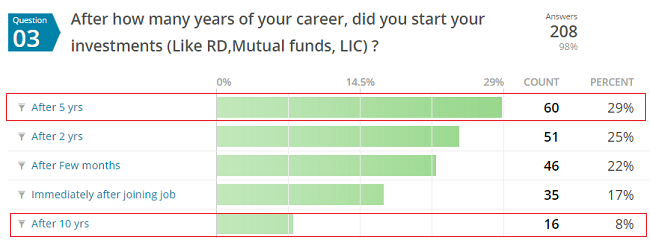

1 out of 3 investors wait for 5 yrs before making first investments

I ran a survey on this topic, which was taken by 208 investors and as much as 37% of investors said that they made their first investments after 5 yrs of their career. Think about this , around 1/3rd investors wait for 5 yrs before they make their first investment. Thats quite high. If you see the same survey results below, almost 8% investors didn’t invest anything for first 10 yrs of their earning life.

This makes them loose valuable time, and for many years they do not accumulate any wealth and get into the mode of living on paycheck to paycheck. Even if they had started a recurring deposit of Rs 2,000 per month, even that would be a great thing, because they are atleast getting into that habit of saving some money regularly and later its just about increasing it.

So if you have just joined your first job, I would suggest start a recurring deposit RIGHT NOW, not for a big amount, but just Rs 500 atleast.

Mistake #3 – Getting high on debt, early in life

Debt is not a problem in itself, if you handle it carefully and responsibly. I do not come from a class of people, who suggest that one should not take loans or avoid debt 100%, because thats not possible for a majority of people and its not practical in today’s times.

However, rore and more people are embracing the EMI culture and we are turning into an EMI nation. Everything is available on EMI ranging from gym memberships to Mobile Phones, from vacations to jeans to even flight tickets. Because of EMI, one can afford anything and everything.

So most and more people are buying not so important things TODAY, for which they have to pay in FUTURE.

Are you getting my point?

This is a perfect recipe to get into the never ending debt cycle. There are many investors for whom EMI payments is going on for years and years. For many years, they have never consumed 100% of their monthly salary themselves.

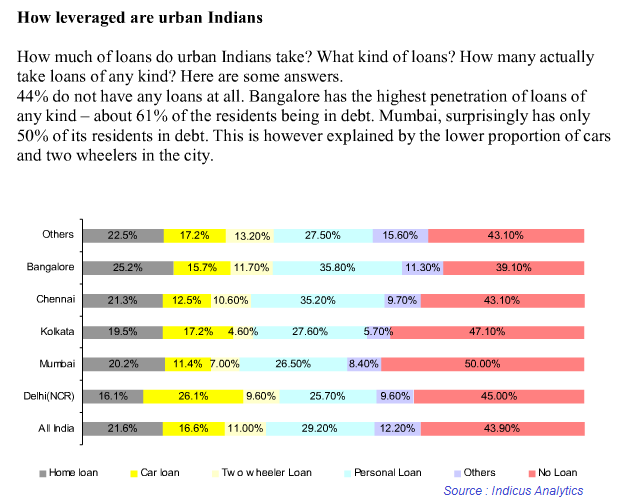

Below is a bit old study by Indicus Analytics on how leveraged are urban Indians, and you will be surprised to know that around 61% of residents in Bangalore have some or the other kind of debt. For Mumbai its 50% . Below is a snapshot of their finding’s.

So if you are young, try to see that you control your desires beyond a point else you will get into huge trouble later in life. Use the credit card and personal loans only and only if you really need it and you have no other options of borrowing and even then pay back the money as soon as possible.

Mistake #4 – Over relying on relatives, friends and parents for your financial decisions

Parents, friends and relatives can bring in a lot of experience and life lessons for us. But a lot of youngsters instead of learning about money, prefer to hand over their overall financial life to their parents. Parents have seen more life then their kids, but then times have changed a lot compared to last 1-2 decades and the many rules don’t apply today.

Also their way of thinking about risk, opportunities, returns etc might differ from you. Hence its not always a good idea to over-rely on parents advice. Mr Anand shares his view about this point in one of my old article

The times have changed so we have to change with the times. In most of the families, it is the ego of the parents which is finally ending with the suffering for the children. Parents feel that the children are incapable of handling money or they may get spoilt if the money is in their name. Also in some families it has become a question of pride saying – My children are so obedient that they are handling over their income to us.

The so called elderly, experienced people do not want to learn the new things and change and their beliefs are passed on to their children also. If we look around many Government employees, we can easily make out this. They are afraid to tell the children about the investments.

Relatives and friends role in your financial life

Also a lot of investors are influenced by their relatives and friends advice. A lot of them turn out to be life insurance agents who want to take advantage of the relation to meet their business targets. Out of 100 people I have come across, 95 people surely have an LIC policy sold by their relative, relative friend, friends relative, parents friend, or someone close.

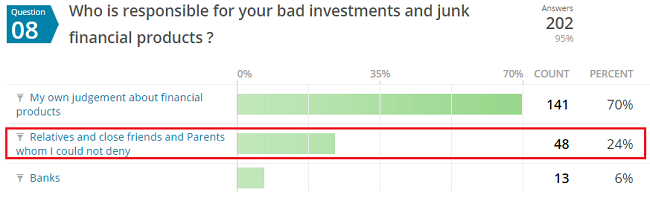

As per our survey, 1 out of every 4 investors financial life is messed up because of their relatives and friends who sold them some financial product or advice on something and they could not deny them.

We recently found that one of our client who recently joined job is paying close to 40% of his yearly salary in 6 life insurance policies. When we enquired more, we found that it were taken by his father for him 3 yrs back, and now as he has started earning, his father has passed the premium paying responsibility to him. The policies were sold by his father’s sister son’ who was behind his yearly targets

I would suggest learning things in the start of your career and not over relying on advice of your friends/ relatives and even parents. You could do many things like read personal finance books, attend workshops on money (we have next workshop in Bangalore on 2nd Aug, 2015) or just surf internet and ready various things.

How should an investor start his financial life at the start of his/her career ?

When a person joins a job, its a special moment in his life and a very crucial point. Taking good care at this point will be helpful for his whole life and many years worth of mistakes will not happen which happens with millions of people. Hence below is a very crisp checklist of what a new investor can start with.

See how much term plan you need and take it

See that you buy a good health insurance policy

See that you have started a recurring deposit or SIP in mutual funds for a minimum amount you are sure will not stop for next 5 yrs

Keep 2 months worth of expenses on the side in a saving account which you generally do not touch

Make sure you are meaningfully saving your taxes

Hire a good CA or Financial advisor if you feel you need handholding

Wish you best of luck for your financial life. Would like to hear your views on this topic

Today’s article is going to be very very basic. It’s one of the lessons which we should teach our kids when are growing up. The question is “Why Invest money at all?”

A lot of investors are not very serious when it comes to save enough money and invest it properly so that it grows well. A lot of investors are quite consumed in their life and don’t deal with this conversation fully. Only after years of working they realise that they have done a very bad job when it comes to investing their money.

I thank Mandar Rane to raise this question in Ashal Jauhari facebook group and shared what he faces with his siblings and many connected to him

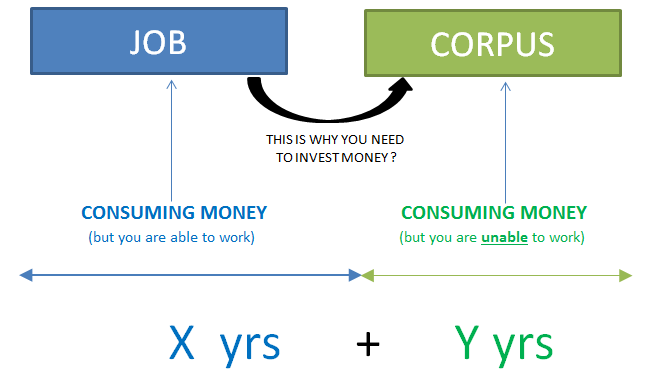

X+Y years theory – Why you should invest money at all ?

There is a simple conversation which I think everyone should go through once. I call it as X+Y theory. Its very simple.

Every person will be living for X+Y years in total.

X is the number of years when they will go to work and bring back money to pay their bills and acquire all they want to enjoy (movies, clothes, eating out, travel, food, fees). This is mostly ACTIVE income and money will come only when you work.

Y is the number of years, which we will spend without earning. We will still need food, clothes, travel, eating out and various other things, but the problem is we will not be working in those years, either by choice or mostly because we are unable to. Now where will the money come in that phase? The money has to come from somewhere?

Right?

So you mainly invest so that you create enough wealth which can last your Y years. I know I am making retirement planning very jazzy at this moment, But NO, this is just going one level deeper and answering the basic question of “Why should I invest at all?”

Note that when we are in X yrs phase, we are not too much concerned about the Y yrs, because the X yrs phase itself has many issues. Kids , House, job, health, parents, relationships and many issues which keeps us occupied enough and only when we approach the Y phase, we are bit scared and tensed, but then it gets too late.

3 basic level reasons you should invest your money?

Below I will talk of primary level issues why one should invest their money to grow in future. And when I say grow your money, I am not talking about saving it in bank account, I mean talking about really letting it grow beyond inflation.

1. Because of Inflation

The most basic reason to invest your money is to protect it from Inflation. Your money will decrease after many years in its purchasing power. A Rs 100 note will not be able to buy the same thing in future, what it can buy today. So you need to invest money properly so that you are able to at least buy the same quantity tomorrow or preferably a larger quantity.

2. Financial Independence

This is exactly what I was talking above. I am sure everyone want to work, but not becoming money slave’s. If you do not invest your money, you will never be able to create a corpus of money you can rely on, and will never be able to get free from your work. If you want to make sure your reason to go to job should be “because I love my job” and not “I need to pay my bills, I am helpless”, then start building that corpus as soon as possible.

And I am not talking about cutting down your desires and entertainment. Do all that, but also start creating that corpus. Keep a balance.

3. Reach your life goals

If you earn Rs 100 per month, and you need Rs 50 for some purpose suddenly you can surely handle is somehow. But what if you need Rs 5000, but you earn only Rs 100? In that case, you need to make sure you have accumulated that amount before hand, slowly and steadily.

We all know some of our financial responsibilities will be coming up in distant future and they would need a big amount. Things like house downpayment, children college education, marriage and many other things like that. If you do not invest, how will you fund those goals? It’s as simple as that.

You are sum of your experiences in life

A lot of youngsters have seen their parents struggle for money and their mindset is already set in a way that they understand the importance of saving properly and growing their money. However a big number of people have had a bad relationship with money. They live paycheck to paycheck, splurge beyond the limit and are careless enough when it comes to money.

A lot of people might say that they are just stupid to act like that and are highly careless and irresponsible. But I think its just a matter of lack of financial literacy or their way of looking at life is different. Everyone is raised differently in their lives and we all have difference experiences. We become what we experience at some level. If you save enough or do not save enough, at the end its just has an outcome which you need to be aware about. That’s all.

How to teach this lesson to your kids (and some adults)?

The simplest way to teach this lesson to small children is to tell them the Ant and Grasshopper story. It’s one of the most simple and powerful stories.

Here is the story for those who can’t see the video

In a field one summer’s day a Grasshopper was hopping about, chirping and singing to its heart’s content. An Ant passed by, bearing along with great toil an ear of corn he was taking to the nest.

“Why not come and chat with me,” said the Grasshopper, “instead of toiling and moiling in that way?”

“I am helping to lay up food for the winter,” said the Ant, “and recommend you to do the same.”

“Why bother about winter?” said the Grasshopper; we have got plenty of food at present.” But the Ant went on its way and continued its toil.

When the winter came the Grasshopper found itself dying of hunger, while it saw the ants distributing, every day, corn and grain from the stores they had collected in the summer.

Then the Grasshopper knew… It is best to prepare for the days of necessity.

Invest early and with discipline

To get the maximum benefit, make sure you start your investments as early as possible. Even if it’s small in the start, that’s ok. At least you will prepare yourself to invest bigger amount in future if you at least invest small amounts in the start. You will build some wealth (even though its small) and build your mindset to invest regularly.

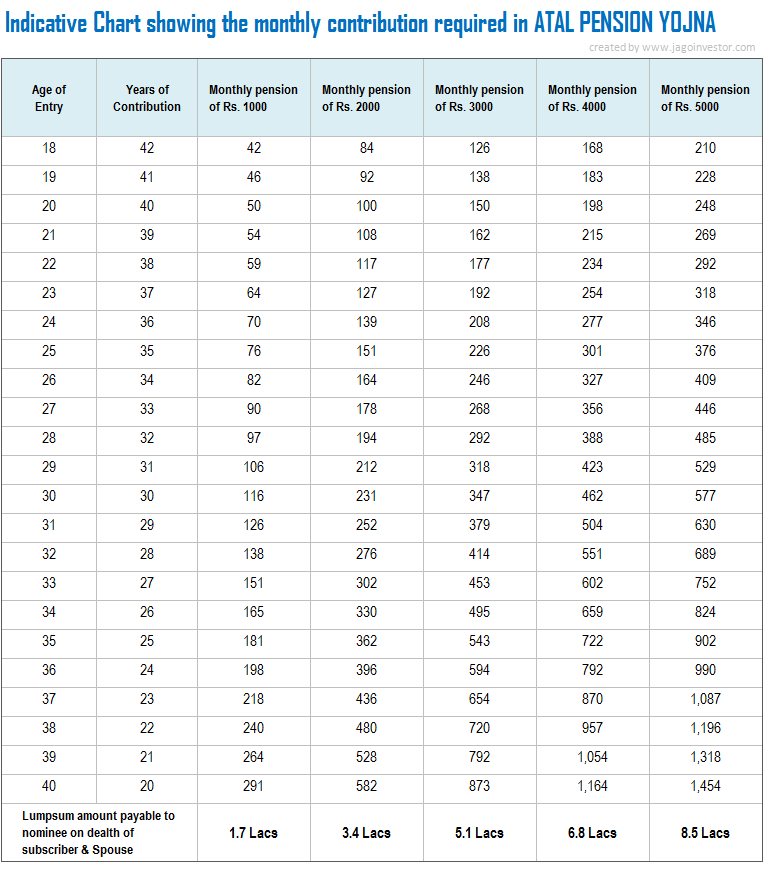

Recently the govt has announced the pension scheme called “Atal Pension Yojana”, which is targeted at workers from lower class who work in unorganized sector which constitutes around 88% of the workforce.

An account needs to be opened under this scheme and monthly contributions needs to be made till the time of retirement after which a pension amount ranging from Rs 1,000 to Rs 5,000 per month would be paid to the account holder and on death of subscriber and spouse, the nominee will get the lump sum accumulated by the end of the period.

Any person below 40 years of age can open an account.

The retirement age will be set to 60 years, hence one will get at least 20 years of contribution. Any person below 40 years can open an account. The retirement age will be set to 60 years, hence one will get at least 20 years of contribution.

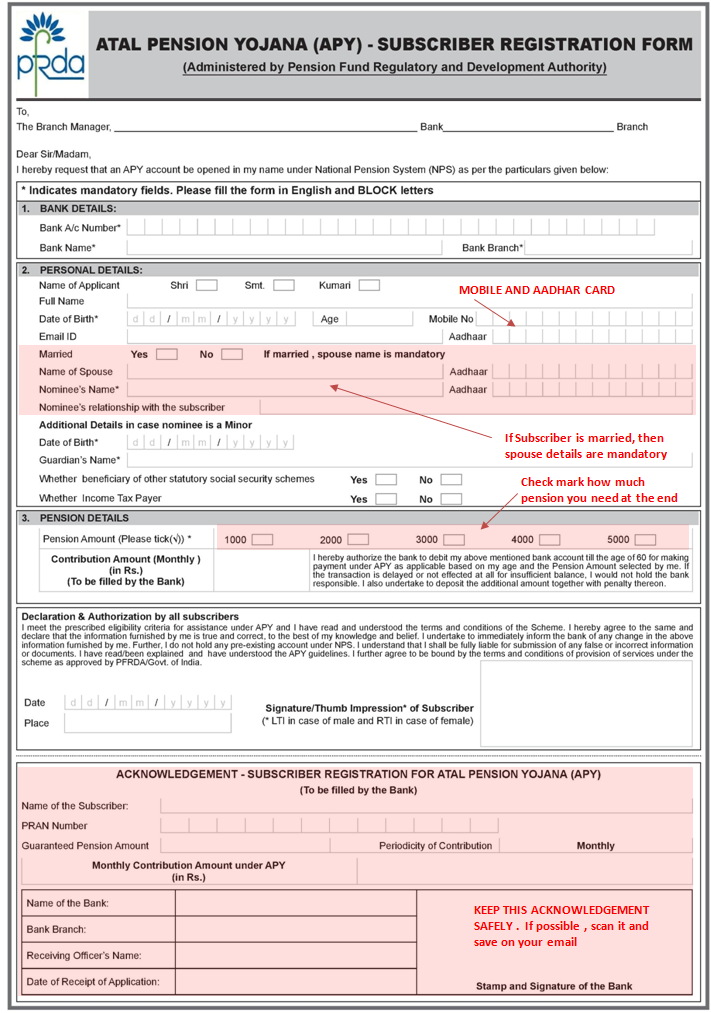

How to open Atal Pension Yojana Account?

Go to the bank where you have your saving bank account like SBI, ICICI, HDFC or any other bank..

Mobile number is compulsory, hence that needs to be filled

If you have Aadhar card, provide the number in the form (but its not compulsory)

You also need to provide spouse details if applicable and nominee details, which is compulsory

You will select the pension amount you need in future and based on that the bank official will write the monthly contribution required on the form

Below is a sample form

Note that the form itself contains a section which mentions that you are authorizing the bank to deduct the monthly contribution from your account till the age of 60 yrs. So once the Atal Pension Yojana account is opened, your bank account will then get auto debited in future every month.

If one does not have a bank account, then one can give their KYC documents along with account opening form with the Atal pension Yojna account form.

Eligibility Criteria for Opening an account

The age of the subscriber should be between 18 – 40 years.

One should have a saving bank account or should open a new saving bank account

One should be having a mobile number, which needs to be furnished at the time of filling up the form

Governments co-contribution for 5 years

If one joins this scheme between 1st June, 2015 to 31st December, 2015 , the govt will co-contribute 50% of the total contribution or Rs. 1,000/- per annum, whichever is lower for the 5 yrs period from 2015-16 to 2019-20, But this govt contribution will be available only for those who are not covered by any Statutory Social Security Schemes and are not income tax payers.

What that means if that if you are an EPF subscriber, then you will not be eligible for govt co-contribution part.

Below is the indicative monthly contribution required in this scheme at various age limits.

The subscriber can increase or decrease their contribution amount at some later stage if they want to do it

Will you get statements of transactions?

Yes, you will be getting regular intimations on your account information through SMS and even a physical statements each month. Note that you can move to any part of India without interrupting your contributions because the deductions will happen automatically from your bank account.

Can you exit or partially withdraw from the scheme ?

1. On attaining the age of 60 years – The first option is when you reach 60 yrs of age. At that time you will be able to use 100% of the money, but only in the pension form. You will only get the pension per month and not the lump-sum amount.

2. In case of death of the Subscriber (once they cross 60 yrs) – In case of death of subscriber, pension would be available to the spouse and on the death of both of them (subscriber and spouse), the pension corpus would be returned to his nominee.

3. Exit Before the age of 60 Years – The Exit before age 60 yrs, would be permitted only in exceptional circumstances, i.e., in the event of the death of beneficiary or terminal disease. As per Wikipedia, Terminal illness is a disease that cannot be cured or adequately treated and that is reasonably expected to result in the death of the patient within a short period of time. This term is more commonly used for progressive diseases such as cancer or advanced heart disease than for trauma.

What is your want to discontinue the payments or delay in payments ?

Non-maintenance of required balance in the savings bank account for contribution on the specified date will be considered as default. Banks are required to collect additional amount for delayed payments, such amount will vary from minimum Re 1 per month to Rs 10/- per month as shown below

i. Re. 1 per month for contribution upto Rs. 100 per month.

ii. Re. 2 per month for contribution upto Rs. 101 to 500/- per month.

iii. Re 5 per month for contribution between Rs 501/- to 1000/- per month.

iv. Rs 10 per month for contribution beyond Rs 1001/- per month.

Discontinuation of payments of contribution amount shall lead to following

After 6 months account will be frozen.

After 12 months account will be deactivated.

After 24 months account will be closed.

Subscriber should ensure that the Bank account to be funded enough for auto debit of contribution amount. The fixed amount of interest/penalty will remain as part of the pension corpus of the subscriber.

Are there any Tax benefits in Atal Pension Yojna scheme ?

No , there are no tax benefits available in this scheme. A lot of people might think that they will get any exemption under 80C or on maturity, but no benefits are available. The pension amount will be considered as the income for the person and will be added in the taxable amount.

What if someone is already a subscriber of Swavalamban Yojana under NPS ?

All the registered subscribers under Swavalamban Yojana aged between 18-40 yrs will be automatically migrated to APY with an option to opt out. However, the benefit of five years of Government Co-contribution under APY would be available only to the extent availed by the Swavalamban subscriber already.

This would imply that if, as a Swavalamban beneficiary, he has received the benefit of government Co-Contribution of 1 year, then the Government co-contribution under APY would be available only for 4 years and so on.

Existing Swavalamban beneficiaries opting out from the proposed APY will be given Government co-contribution till 2016-17, if eligible, and the NPS Swavalamban continued till such people attain the age of exit under that scheme.

Note that, the ultimately the money under this scheme will be managed through NPS only and thats the underlying thing. All the investments decision will happen as per the guidelines of PFRDA.

A good support system for Poor

As I mentioned, this scheme has the maximum pension of Rs 5,000 per month, that too when the person reaches 60 yrs of age, that too will happen only after a minimum of 20 yrs from now (only people below 40 yrs of age can open an account), so Rs 5,000 at that time would be a very miniscule amount.

However note that we are talking about the people in lower section’s who are really poor. At least this Rs 5,000 per month would be a great support in their old age when they won’t be working. A subscriber can open only one APY account.

With this scheme, people will be encouraged to save a small portion each month ranging from Rs 40 to Rs 210 per month. Below is the full chart showing how much money would be required to be deposited each month depending on the time of entry in the scheme and the pension amount chosen.

What is the returns of this scheme and should you invest?

So the question finally is, how good is this scheme and its returns if you consider the returns? I did a XIRR analysis of the scheme considering a 40 yrs old person is investing Rs 1,454 per month for 20 yrs , and then gets a pension of Rs 5,000 all this life (till age of 100 years). The returns I get is 7.74% through the excel sheet.

When I do the same thing for a 25 yrs old person invests Rs 376 per month for next 35 yrs (till age 60) and gets pension till he turns 100 yrs . The overall IIR is 7.9% . This includes the lump sum payment at the end to the nominee

So looking at the numbers, we can conclude that the returns from this scheme is in range of 7.5% to 8%. Considering that, Its a guaranteed return from govt of India, I will leave the judgement of its being good or bad to you only.

You should also read, Debasish Basu critical analysis of this scheme on this link to get more understanding about the issues of this scheme.

I would like to again reiterate the point that this scheme is more for the people of poor background who do not have access to any social security scheme already and will be somewhat beneficial for them, and not high-income earners because Rs 5,000 even after 20 yrs will be very very small amount.

If one wants to still open this account, one should find a good enough reason for themselves.

Are you investing in this scheme?

I would like to know what you think of this scheme and if you will be opening an account for yourself? You can also suggest this scheme to your maid, driver or any person who you think should get a minimum pension by the time they turn 60 .

At the end, I would like to share that we are doing our Bangalore workshop on 2nd Aug, please register asap for the event before its full

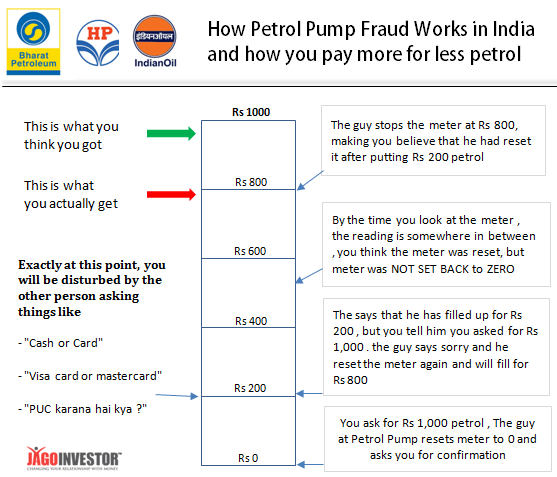

I got cheated at a Petrol Pump yesterday for ₹ 400.

Yesterday I went to a BPCL petrol pump to fill petrol in my car, where it all happened.

I asked the attendant for a “Full Tank”. I generally get out of my car and stand near the person filling it, but I was in a conversation with my friend and trusted the petrol pump as I have been there quite a number of times. However, this time I made a mistake.

The attendant asked me to see the ZERO on the meter and then started filling the petrol. Once the meter started and I thought that everything is fine, he stopped at ₹ 400 and started billing.

I knew this tactic where they say “Oh .. I thought you said ₹ 400”. So I told him to leave it at that point and bill it to me for ₹ 400 only. I paid the amount and went ahead.

However, my car indicator was still showing the same “51 km” which it was showing before I went to petrol pump and did not go past it. That’s when I realized that I was a victim of another Petrol Pump fraud, which I was unaware of. I already went too far from the petrol pump and had no proof of the incidence that happened. However, I was surely tricked.

I got back my Rs 400 and offer to terminate the employee

My immediate next was to lodge a complain on BPCL website with all details and I was quite surprised and happy to see that I got a call back from the petrol pump manager within 30 minutes.

He accepted the mistake and offered to pay back the fuel worth ₹ 400 and also terminate the employee if found guilty. I told the manager that I do not wish him to get terminated in this hard times. It will be enough if he can warn that person strictly and take measures to ensure this does not happen again.

Please listen to my 3 min audio recording with Petrol Pump Manager.

Update

Today I visited the petrol pump again as requested by the petrol pump main manager (he was not present that day when I got scammed). He was quite helpful and courteous in explaining all the things to me. He also got my car filled for Rs 400 petrol so that I am not in loss. Apart from that, he also showed me their automation system which records each and every entry with the time stamp.

I was able to see the entry of Rs 401.50 for the exact time and date. However as I said, the petrol did not reach my car at all. As I said I was not attentive enough that day. I guess the petrol was getting filled in some other vehicle or container (check Fraud #4 below) which I will leave the petrol pump to investigate using their CCTV. I was also offered by petrol pump to do 5 ltr fuel test incase I want to.

Please note that I am not holding BPCL or manager responsible for what happened. After I met the manager, and asked all the questions I had – I am convinced that it was purely employee mischief in this incident.

Also I want to acknowledge that BPCL was quite fast in resolving my case and the petrol pump manager was also quite prompt to investigate the case.

Is this a new kind of petrol pump scam which got invented?

This got me thinking about the quantum of these kinds of scams and frauds which happen almost every minute in our country in almost all the cities of India, where people get cheated of small amounts like ₹ 50, ₹ 20 or ₹ 500….