Do you want to know how to update aadhaar card details online? Yes – It’s possible. You can easily update your details online without any offline documentation and then download your new aadhaar card online and start using it.

Recently, I wanted to change my address details in my aadhaar card and I completed the whole process online by visiting the website of UIDAI. It was just a few minutes task and very easy. I have also created an online video tutorial with all the steps. Below is the video if you want to refer to it.

8 step process to update your aadhaar card details online

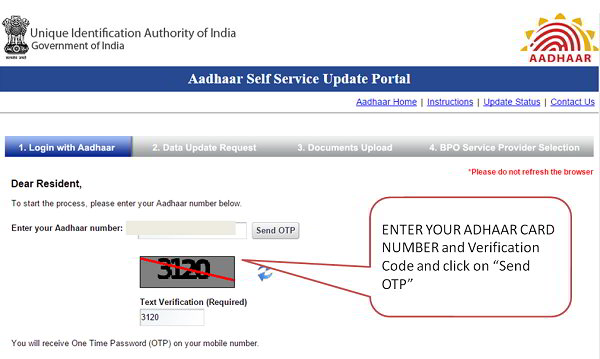

Enter your aadhaar card number and text verification code to generate the OTP

Enter your OTP and then on the next screen choose the details you want to change

Enter the details which you want to change and then proceed to upload the documents

Choose the supporting document which you want to upload. Make sure the document is self attested and signed by you and scanned back.

Note down the UTR number which can be used later to check the status

How to Check the status of your Aadhaar change ?

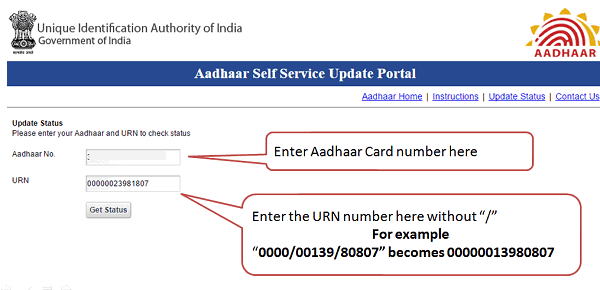

Once you have submitted the change request, you will get a UTR (Unique request number), which can be used later to check the status of the change. Here is how you check the status later

Enter your Aadhaar card number and the UTR number (without slashes)

You will get the status. It might be awaiting approval or might have approved already in which case you can then download your new aadhaar cared online and start using it

How to download your new aadhaar card after the update is complete?

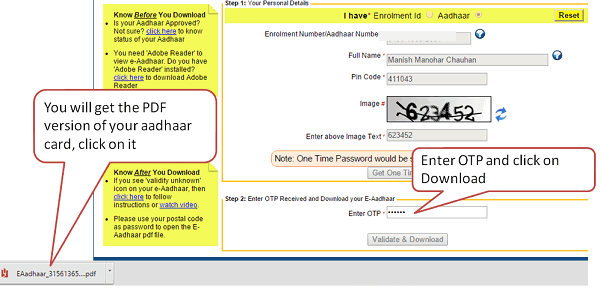

Choose the option to enter your aadhaar card and enter all details

Generate the OTP and enter that to proceed

A PDF will get downloaded which can be opened by entered your pin code as the passport

You can now start using this new aadhaar card by taking a color Xerox

Cases where you might want to change the aadhaar details

Your address might have changed after your aadhaar card was made

Incase of name change after marriage in case of female

Your mobile number or email id is changed

You have changed your name or your name was wrongly captured at the time when you applied for aadhaar card

By mistake your gender or date of birth was wrongly captured

I hope this tutorial was clear and easy for you to follow. The process to update aadhaar card details just takes 5 min of your time. Try it and let me know if it worked for you or not. Also do not forget to share this article with your friends circle; it would be very useful for them.

Recently, I came across one interesting short story on quora, which I found interesting and worth sharing with all the readers. This story will help you understand why you are not able to save enough money by the end of the month. You will get to know why your hard-earned money is spent into useless things and you don’t have enough control over it.

Lady: Do you smoke?

Guy: Yes I do.

Lady: How many packs a day?

Guy: 3 packs.

Lady: How much per pack?

Guy: $10.00 per pack.

Lady: And how long have you been smoking?

Guy: 15 years

Lady: So 1 pack is $10.00 and you have been smoking 3 packs a day which puts your spending per month at $900. In 1 year, it would have been $10,800. Correct?

Guy: Correct.

Lady: If 1 year you spend $10,800, not accounting for inflation, the past 15 years puts your spending total at $162,000. Correct?

Guy: Correct.

Lady: Do you know if you hadn’t smoke, that money could have been put in a step-up interest savings account and after accounting for compound interest for the past 15 years, you could have by now bought a Ferrari?

Guy: Oh. Do you smoke?

Lady: No.

Guy: Then where’s your fucking Ferrari?

The story above sounds funny. The lady did not smoke, so that money must have got accumulated and she should have owned a Ferrari as per the logic. But that did not happen in reality.

Why?

The answer is – “Ferrari was never on her mind”

Her money was not put on the purpose of buying the Ferrari someday. She did not spend the money on a cigarette but then that same money kept getting consumed on some other things which came in small chunks.

Life kept throwing small and tempting desires and she fell for it without realizing it. And finally at the end, did neither have the money, nor the Ferrari.

You are the biggest enemy of your financial life

If you leave your money in the saving bank account without giving it a strong purpose. Then the lifestyle today is such that no amount of money is enough to meet your short term desires.

Life will throw all kinds of requirements and if your money is available right in front of you, you will keep trying to handle those requirements without much analysis.

Justifying the expenses becomes very easy when you have the money sitting in front of you, waiting to spend. Investors are generally over-confident about their saving abilities and there are tons of research to prove that.

Take out the manual mode of investing from your life

Here is the rule – “Lesser the money available in front of your eyes, higher the chances that you will restrict your useless spending.”.

You need to take out the manual mode of saving money out of your life and take the help of automation. There has to be some way, where some part of your salary leaves your bank account and gets invested on its own. Because the more you leave the decision making to yourself, it’s not going to happen on a consistent basis. Humans are designed to take the path of least resistance. Machines don’t make mistakes.

Let some automated way to save your money, and it will happen consistently, without fail. No one will

The best example of this is your EPF

Your employer deducts a part of your salary and that gets accumulated over months and years. That small deduction becomes a very big amount, if you leave it just like that and don’t disturb it. EPF does not earn very high interest, but still, it accumulates a decent amount.

Now just imagine this, Your employer tells you that they will not deduct that amount and you have to save money each month. It’s fully in your control now.

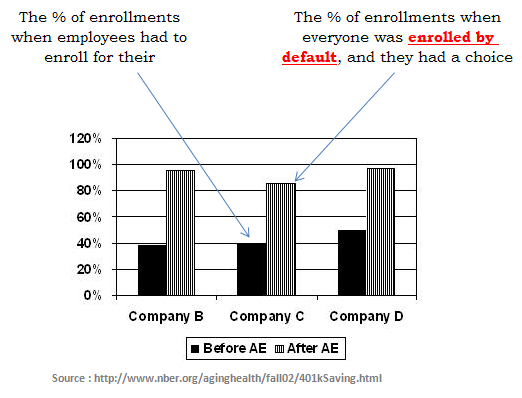

You should feel great that you have EPF and some form of automatic saving. If you were given the freedom to choose the EPF, it would be a bad thing. Because most investors won’t have chosen it. Here is a similar study from the US, where employees were asked to enroll for the 401K program (similar to EPF in India). However, the catch was that they had a choice to not opt.

When the enrollment was made a compulsory thing as a default choice, with an option to opt-out if one wants, the enrollments more than doubled. Why did it happen? Because enrollment happened automatic!

So coming back to EPF example, Will you save money equal to your EPF each month if it were not taken out of your salary automatically?

Are you really confident that you have the determination and commitment and control over yourself to save that money month after month, year after year without fail?

Are you understanding what I am trying to tell you here? The point is, YOU are your own enemy when it comes to saving. Take your manual judgment and your decision making out of saving each month. Let it happen on its own, automatic.

My personal Experience

Around 6 months back, my wife wanted to start a recurring deposit.

She started a recurring deposit of Rs 15,000 per month for 1 yr period. After 8 months, when she checked the bank accounts, she could see the 1.2 lacs in the deposit account. Suddenly she felt – “How this money did came there?”.

The point is – it was automatic saving. It all happened in the background and didn’t give her any scope of judging the decision again and again. She always saw her salary minus 15k in her bank account.

All her expenses, shoppings, indulges, bills had to happen out of the money which she saw in her account and it happened. The expenses fit themselves in the amount available. It’s the nature of money, and I will share more about it in some time.

Don’t trust yourself for saving money

Don’t trust yourself, when it comes to systematic saving. Your intelligence can be your big enemy. If you decided that each month you will carefully set aside some part of your money yourself, after all the expenses are done, then it’s going to be a tough time for you.

Do this simple exercise

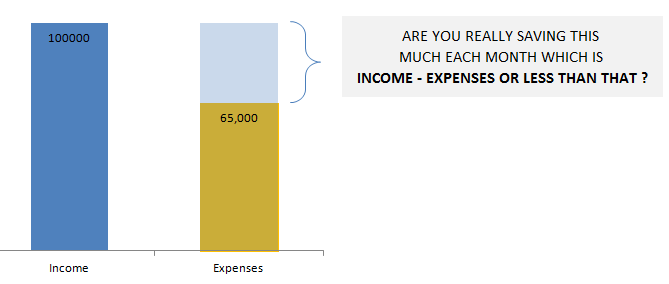

Take a sheet of paper (or open an excel sheet). One the left side write down your income each month and one the right side, write down all the expenses per month.

Now subtract your expenses out of your income, and you get your monthly surplus. So each month after all your expenses are made, you should be saving that surplus amount. Correct?

Is that happening? Did I hear NO

Why does it happen? Why are you not able to save the money equivalent to your surplus each month?

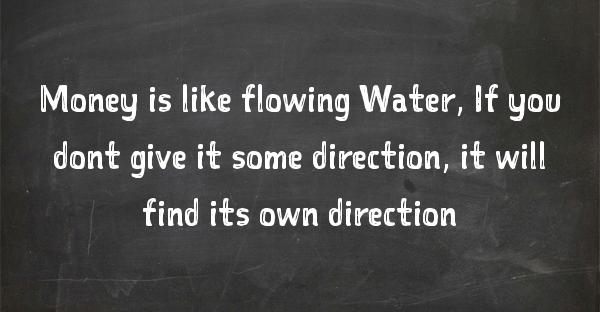

MONEY is like flowing WATER

Have you ever wondered why you are not able to save enough money, even though your salary has kept increasing in the last many years? Your expenses keep on matching with your expenses.

Even if you are saving some money, are you reaching your full potential? I guess NO

Why?

It’s because money is like flowing water. If you do not give it some direction, then it will find out its own direction.

When you do not automate saving money, then all the money will get consumed into “something”. Life will keep throwing various kind of expenses, desires and requirements, and if money is easily available in your bank account, then trust me, you will always come up with strong reasons why you can’t avoid those expenses.

Some of our clients get shocked when they fill up the datasheet we send them. The most common complain is – “I am not saving anywhere close to what my income – expenses is showing up”, where is it all going?

The answer is – “Its getting consumed into things which looks important and urgent in short term, but in reality, they are not”

My friend real life case

Few months back, I was talking to one of my close friends. He told me how he is not able to save anything by the end of the month. He was very confident that it’s very tough for him to save anything. After all, if he had any surplus, why it’s not there at the end of the month?

I asked him a simple question – “If his income increases by Rs 1,000 per month. Will it remain in the bank account after all his expenses?”

This one single question was a game changer.

He told me that he is very sure that even if his income increases by Rs 1,000 per month. His life would be same, it will surely get consumed somewhere.

I told him – “In that case, if your income drops by Rs 1,000, your situation will be same”

So why not set aside that Rs 1,000 in the starting of the month itself, and see fewer months in the bank account. Trust me, your financial life will figure out something, it will adjust. It will surely try to fit it.

And that’s exactly what happened. I helped him in starting his first SIP of Rs 5,000 per month.

Just a few days back, the first auto debit happened. I can almost guarantee that by the end of the year, these Rs 60,000 which was getting consumed somewhere, will “automatically” get saved in mutual funds.

So what is the worst case?

Ok fine, your financial life is really in bad shape & you can’t save even a penny. Let’s say, you show some courage and start a recurring deposit of Rs 1,000 per month, even though you know you will need that 1k later.

What is the worst case?

You would need that money back in some time again? Right?

Solution – It that happens, then break the Recurring deposit and use the money …

Or you could start a SIP of Rs 1,000 and incase you needed it, you can always redeem it and take back your money.

But you know what, you will not take it back. You will not redeem it. Because like most of the investors, you are lazy when it comes to money. It’s easier to adjust rather than take that pain to go to the bank and sign that paper for redemption.

We humans take the path of least resistance. You don’t know how amazing human laziness can be for your financial life. Ask those who bought IT stocks and never cared to think about what to do with it. Its only their laziness, which has made them millionaires, because they still hold the stocks

Most of the people are living with this myth that they will not be able to save even a penny by the end of the month. It’s not true. For 95% of investors, it’s a self-created illusion.

They have just not tried enough in the right manner. Let me share with you this in detail

Income – Expenses = Saving

For most of the investors, the default equation each month is “Income – Expenses = Saving” . This equation looks very natural and logical. First, you take care of expenses because they need to be handled NOW, and then if something if left, you will save it. This is how any normal person will think like. But that’s the root of the problem.

If you are not able to save enough money each month, I am ready to bet that this is the equation that is destroying your financial life. Let me guess how it looks like.

Each month, you must be earning some money, then you take care of various expenses, some fixed and some random surprises and if you get lucky, you must be having some surplus money in a bank account each month.

But wait, The money is still in your bank account. It’s still “easily available”. You decide that you will do something about it very soon. You decide that once it becomes a big amount, you will create an FD out of it.

Next month, again you have some surplus and more money got accumulated in your saving bank account. Suddenly in the third month, your spouse tells you that she wants to upgrade the washing machine. After all, anyways its Diwali time and she deserves it.

And why not? After all, you have the money available in your bank account. What’s the problem then?

Your timing is also perfect, the thought of upgrading the washing machine has come up just when Flipkart sale is round the corner. I am sure it’s a coincidence.

No , it’s no coincidence.

The point is – the money found its own direction and that’s because you didn’t gave it any direction beforehand.

For a moment, think what would have happened if the additional surplus was not available easily. It was there in a recurring account or was into SIP in some mutual fund or ELSS (locked for 3 yrs). It’s hard to imagine that you would have said – “Let’s stop our RD or SIP in mutual funds and upgrade the Washing Machine”.

Can you see how everything changed in both the situation?

Or imagine you would have created an FD out of that money before hand for paying the school fees for your kid at the of the year. Would you break your kid’s related FD to upgrade the washing machine? Generally not.

I am not against the expenses

Trust me, In no way, I am judging the urgency of your needs or desires. They might be genuine and very much reasonable. Please go and upgrade your washing machine, if it’s really needed. I am not even against taking a loan for that, but just assure that your requirement is genuine and not a made up one.

Just 1 yr back, I bought a sports cycle out of impulse and you should have met me just before I purchased it. I would have convinced you that I need the cycle more than I need oxygen. Plus, I had the money with me at that time. Today I am not using it enough to justify my buying decision.

I can tell you – this false belief of “I need it so much” and the availability of money in your bank account is such a deadly combination.

So what do you do ?

Change the equation to “Income – Saving = Expenses”

Few changes in life give a new direction to life. Everything changes.

Trust me, this is one such change if you really understand it well. If you decide to change your saving equation to “Income – Saving = Expenses”, it can drastically impact your financial life in positive way.

Here is now you implement it.

Find out what is the minimum amount you think can save each month. Is it 10%, 20% or 30%. Take a lower amount at the start, else it won’t be sustainable in the long run.

If your salary arrives in your saving bank account on date X, then, setup a recurring deposit or a SIP in mutual funds on date X+2 or X+3

Trust automation, it will do wonders for you

And in the worst case, if you really need the money, you can redeem it back and use it or stop the RD or SIP.

If you can take this first step, then you have already won the big part of the battle. Other things like great returns, advice, controlling risk, finding the best financial product and all that will be taken care of later. But the first step it this – changing the equation

If you can spare 20 min, you should watch this amazing video by Shlomo Benartzi, on the topic of Saving for tomorrow, tomorrow. You will understand the impact of automatic saving in a better way in this video

And you don’t have to compromise

Don’t confuse automatic saving with compromising on your expenses and fun. We are not asking to stop eating out or cut on your entertainment in life. A lot of investors live in this myth that financial planning is all about compromising your desires and spendings. No, it’s not.

It’s all about giving a meaningful structure to your financial life and exploring various possibilities to make your financial life awesome. That all.

I would love to hear what you think about this idea of changing the equation. Do you think that this single thing is really a very important parameter to live a good financial life? Please share your own saving habit in the comments section

Are you an existing mutual fund investor? If YES, then you must have got an email from the fund houses where you have invested to provide some additional information about yourself and about your tax residency related questions in the name of FATCA declaration.

In this article I will quickly guide you about what is this FATCA Compliance and how you can update this information with AMC online in 5 min.

What is FATCA Compliance?

Foreign Account Tax Compliance Act or FATCA was passed in US in the year 2010 to make sure that the financial institutions across the world share some basic information of their US based clients.

A lot of investors from US (US citizen and NRI’s residing in US) were supposed to disclose their investments outside the US, but it didn’t happen the way US govt was expecting.

So finally, US govt passed this FATCA law and signed treaties with various countries across the world. India is one of them. So now various financial institutions based in India are asking all their customers to give a declaration about their tax residency, place of birth and if they are paying taxes in any other countries. I am not going into too much of detail here, because you can read it in detail in this moneylife article here .

The main purpose of this article is just to help you understand, how you can update these FATCA details quickly in 2 min online.

All mutual funds investors are supposed to update their information with AMC’s by the end of Dec 2015.

If an investor fails to update their FATCA declaration, then their additional investments will not be processed in future and any SIP which is currently running will also get stopped. So it’s suggested that you complete the declaration as soon as possible. Note that your existing investments will remain intact and there is no impact on that.

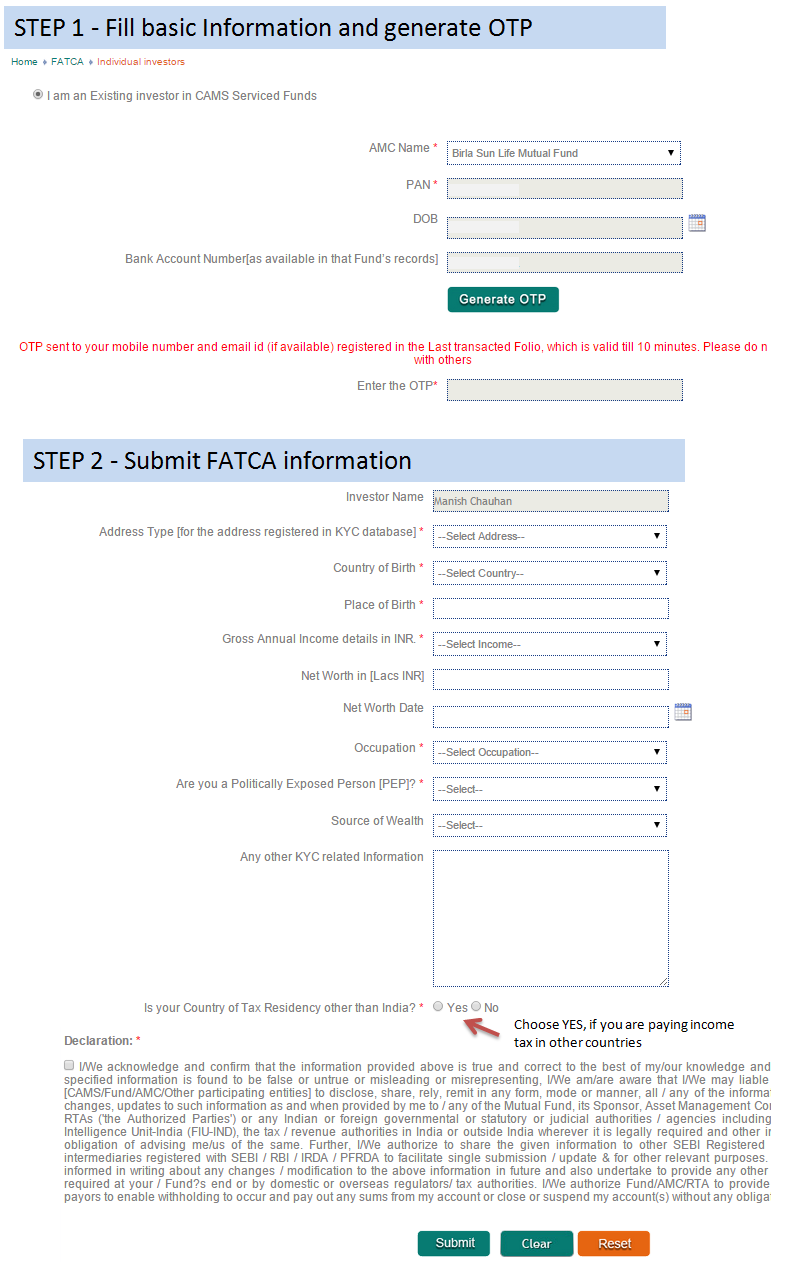

How to update your FATCA related information online?

It’s very simple. All you need to do is visit the following two links and update your information.

Note that a mutual funds is either serviced by CAMS or Karvy (all funds except franklin Templeton, go this link where you can update FATCA for franklin). So these agencies have come up with the links online where one can update all their information.

When you update your information online, an OTP will be generated which will be send to your email/phone which is registered in their records. If you are invested in mutual funds which are services by CAMS (like Birla, ICICI, HDFC etc) , you just need to update the first link (cams one). If you are invested in mutual funds which are serviced by Karvy like Reliance, UTI or Canara Robeco, then you will have to update the karvy link as well.

In the same manner, you can update the Karvy link with your FATCA information. The OTP will be generated in that case also and all the information is same. You need to update the karvy link, only if you have invested in any mutual fund serviced by them in past.

In anycase, my suggestion is to try to update both the links. There is no harm anyways

FATCA Impact on US & Canada NRI’s ?

So what is the impact of this FATCA declaration on those NRI’s who are based in US and Canada. Let me be very brief and to the point here. Only 3-4 AMC’s in India are going to except fresh investments from US & Canada based NRI’s. Few of them are UTI, L&T and Sundaram mutual funds. so if you are a NRI based in US and Canada, now you will not be able to invest in mutual funds from HDFC, ICICI, Birla, Reliance and many others.

However any existing investments can be continued (SIP wont be continued, but the current worth in those funds will be as it is) . One can redeem them whenever they wish to.

NRI’s based in other countries can invest in any fund house they want.

Incase you have any question on this FATCA declaration, feel free to ask your queries in comments section

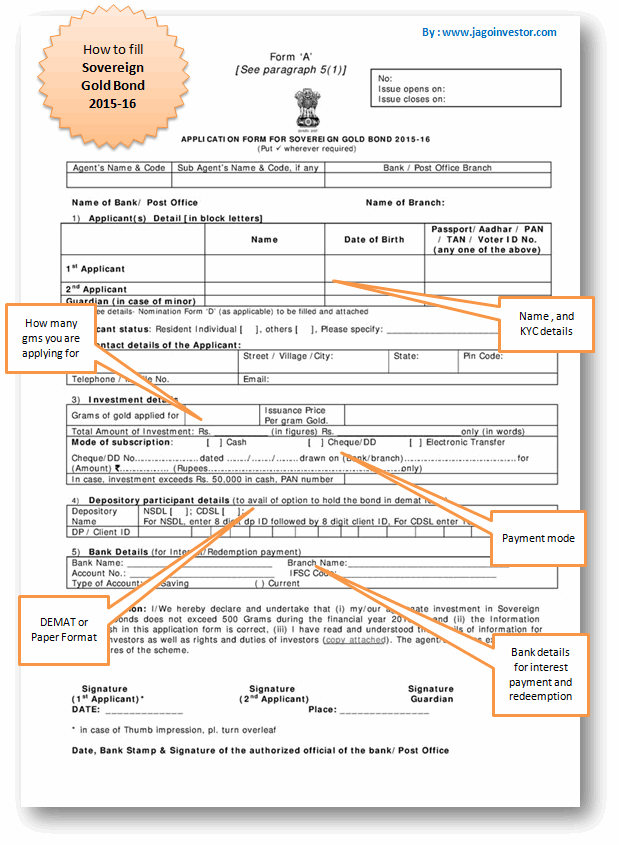

Today I want to share some quick facts regarding Sovereign Gold Bonds which was announced in budget session and recently mentioned by our Prime minister.

RBI is going to issue something called Sovereign Gold Bonds for investors who want to benefit from the movement from Gold prices. It’s an alternative way to invest in gold apart from buying physical gold or through gold ETF or gold Mutual fund.

These bonds issue is part of the market borrowing program of govt of India, where it tries to borrow money from the public for the long term. So to understand it in brief, govt wants to borrow money from those who want to invest in gold and they would return back the money after X number of years which will be linked to the price of gold apart from a small interest.

10 FACTS about Sovereign Gold Bond Scheme you should know

Now let’s understand quickly what Sovereign Gold Bond Scheme is all about and some high-level important points every investor would want to know.

1. Issued by RBI and hence it’s safe and secure

These bonds are issued by Reserve bank of India and hence it carries a sovereign guarantee by Govt of India.

So in a way its 100% safe and secure and there are no chances of fraud or any issues happening in the future.

However, you need to know that the bond value is linked with the gold prices and hence the value of the bond can increase and decrease in the future depending on the gold price movement.

However, whatever is the maturity value will be paid to you and the guarantee is only for that. There is no assurity for any minimum value payment or any promise of return. One can hold the bonds in a single name or joint name as per preference.

2. First Batch of bonds available from Nov 5-20

As per a report, out of Rs 15,000 crore of bonds, the first batch of Rs 1,000 crore bonds are available from Nov 5 and the last date for application is Nov 20. The bonds are available for only residents Indian and NRI’s cant buys it. The bonds will be available at selected banks and post offices designated under the scheme.

I was not able to find exact locations, but I think all the major PSU banks in every city and some big post offices will be the contact point if one wants to purchase these bonds.

The minimum one has to buy 2 gms worth of gold bonds and the maximum can be 500 gms. So every normal middle-class person who wants some exposure in gold can buy it. The initial issue price is fixed at Rs 2,684 per gram. Which means a minimum initial investment would be Rs 5,400-5,500 at least.

Note that price fixed is a simple average of the closing price of the 999 purity gold, published by India Bullion and Jewellers Association Ltd (IBJA).

The bonds will be issued with an 8 yr tenure, however, an exit option will be available after 5th year onwards. The bonds can also be traded on stock exchanges if you have it in Demat form. However, I think it’s not going to work for most of the investors because that will get too complicated.

Also, you will be able to trade the bonds on markets only if the volumes are very good, otherwise it will be locked away and you will be able to get back the money only after the 5/8 yrs of time. You can read detailed FAQ’s on this scheme here

Also note that these bonds can be provided as collateral incase, you need any loans.

4. You will get interest of 2.75%

You will get interest of 2.75% interest on the initial value of investment (not the market price) every 6 months. I have not gone in details, but I think the way it will work is that if you invest Rs 1,00,000 in these bonds, then every 6 months you will get 50% of 2.75% of Rs 1 lac as interest, which would be Rs 1,375

5. Taxation on returns and maturity

Note that the interest you earn every 6 months will be taxable in your hands. Also at the time of maturity, the long-term capital gains will be applicable, which means that after applying indexation, you will have to pay 20% tax on the returns. Note that because KYC is done properly, you cant escape this.

6. KYC requirement

You will be able to buy these gold bonds only after the KYC is done for you. In simple terms, at the time of application, you will have to provide your identity and provide your PAN or Aadhar card etc and the payment can be done electronically, with cheque/DD or even CASH.

However, you will not be able to hide your identity. This will surely discourage those investors who want to convert their unaccounted money (CASH) into white money.

7. Investment in Paper or Demat Form

You can purchase the bonds in paper format or Demat holding as per your preference. Means if you want the bond in paper format, you will get a receipt and a bond that you can keep in your locker or at home and at the time of maturity you can give it back. Or you can hold it in Demat form and not worry about keeping the bond safely.

Who should not invest in these gold bonds?

I think that 5-8 yrs tenure is a long tenure and you can earn much better returns in this long term. Equity mutual funds would deliver better returns compared to this scheme. Hence if you are a young person below age 40, and are looking at wealth creation as your main goal, then you can give a miss to this scheme.

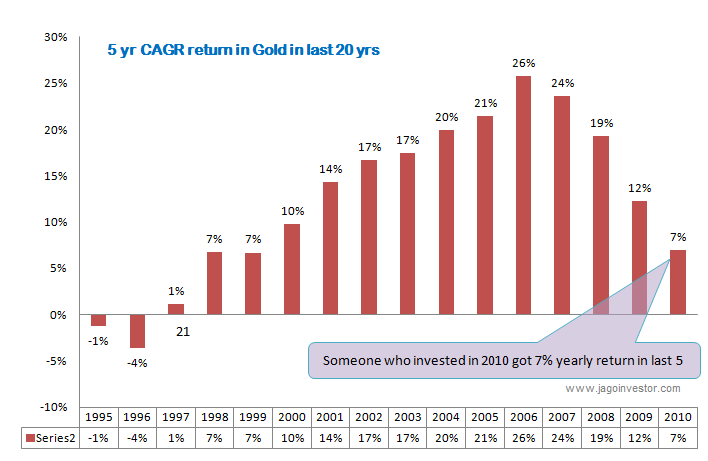

The return on the scheme (2.75%) is not to be considered and the gold returns historically have been around inflation only.

If you look at the below chart, you can see 5 yrs CAGR return of the gold investment. Note that for the tenure of 2000-2010 the returns have been very very good, but then if you look at someone who invested in the year 2010, they have just got a 7% CAGR return, which is very much in tune with long term gold returns.

So if we look at the optimal use of your investment to generate a decent return, I personally dont consider this as a great investment product. You can skip this.

Who can think of buying these bonds?

Now if we look at the other side, There are many investors who are very attached to gold and really want to invest in that. No logic will move them and no conversation of CAGR will make sense to them. So for those investors who were anyways going to buy physical gold or Gold ETF, can look at this scheme as a good alternative.

Anyways your investment value will move as per gold prices and on top of it, you will get 2.75% interest which you do not get in case of physical gold or gold ETF/funds. The best part of this scheme is that you don’t have to worry about the quality of the gold or where to store it as its all in paper format and no one is going to steal it from you.

The money will only come back to your bank account only which you have provided at the time of investment.

However, note that the investment in these bonds is going to be mainly illiquid in the very short term. If you buy physical gold, you get that liquidity in your hand and if you need money urgently you can sell off the gold. You will not get it here.

So overall, you are the right person to pick if this scheme is for you or not.

Please share what are your views on this scheme. Do you think it’s going to be a hit among investors?

I recently visited Mumbai for some work and it was 7:15 pm in the evening. When I came out of a building in Andheri East, Mumbai.

I had booked a cab from Pune to Mumbai and I was now ready to be back. I called up the cab driver and here is the conversation…

ME – “Bhaiya, kidhar hain aap?”

Driver – “Bas sir, Yahi hun 200-meter piche, 20 min me aa jaunga, aap gate ke pass hi rahiye”

ME – “Main aa jata hun paidal chal kar, Aap bataiye kidhar hai exactly”

Driver – “Arre nahi sir, aap wahin rukiye jidhar hai, itni bhid me Mujhe nahi khoj payenge”

Finally, after a long 20-30 min, I saw a car near me, honking like hell and flashing lights on me. It was my cab driver and he was indicating – “Get inside the car asap”…

Finally, I was inside the cab and we were going back to Pune. It took us another 20 min to just get out of the lane. It was really frustrating to just see yourself in the middle of traffic and move nowhere.

The first half of the total time took us to come out of Mumbai and the second half took us to reach Pune. Finally, I reached Pune at 11:30 in night.

Story of the Cab Driver and his Financial life

In this article, I just want to share with you a conversation between myself and a cab driver I met recently. I asked him some questions about his life, a bit about his financial life and his work schedule. I know, it’s not directly related to personal finance, but I think, it’s a good idea to share it with you all as it has some good things to know about.

(The photo above is not the real cab driver in question)

The moment we were out of the lane we were stuck in at Andheri, the driver looked really irritated by the sheer amount of traffic. I asked him – “Bhaiya, Mumbai ki life Kaisi Lagti hai aapko?”

And his answer stunned me – “70 saal jeene waala insaan 50 ke khatam ho jayega, yahi hai Mumbai ki life”

While I knew he was a bit tired and his frustration was making him speak these words, there was surely some element of truth in his words. The way of life, the speed, the running around for everything. It’s really mind-boggling in Mumbai.

Anyways, One my way back to Pune, I had conversations with Driver and here are few things I came to know.

1. He drives 400 km EVERYDAY

Did I ask him if travels to Mumbai often? He said every day. YES – Everyday .. 30 days in a month… May be once in a while there is no pick or drop but in general every day. He said that he does close to 10,000-12,000 KM every month. His legs and Back pains a lot and sometimes it’s so bad, he can’t explain it. We reached Pune around 11:30 pm at night and he had to get back at 4 am again to take someone to Mumbai airport.

2. No family life

I think we felt by good talking to me, and he kept on going.

“Family life nahi hai Kuch Bhi Sir .. Ghar Jata hun, khana khata hun aur sidhe so jata hun”. He told how his life is tough and there is no energy left once he is back home. He has no motivation to talk to his kids, spouse or enjoy with them.

Even when he has to drop or pick someone, he has nothing to do and he just sits inside the car and it’s really tough to do that, day after day, month after month and year after year … It’s the height of boredom”

He was a calm person, but he said that when he is stuck in jams atleast he feels he want to throw away the car like HULK. It was a calm frustration coming out of him.

3. He had Life + Health insurance

I realized that his job is very risky. He has to drive each day and he is prone to accidents. His legs are so important for his job and to earn the money. I thought I will explain to him why he should think of covering these risks and I asked him – “Do have Insurance?”

“Yes Sir, I have life insurance and health insurance both from ICICI Lombard”

I was happy and a bit shocked to hear that because I didn’t expect him to have that. He told me that one of his agent friends had explained to him about these products and how it might help him. I congratulated him on that point and said that it’s a great thing that at least he has something. Thank god he did wait to find the “best product”

4. He saved Rs 4,000 per month in Recurring deposit

Though his earnings were limited and he was on a tight budget, he told that he managed to save Rs 4,000 per month. He gave it to his wife every month which is invested in Recurring deposit. I thought it was a great thing and didn’t say anything like “why don’t you invest in equity?”. I think it would have confused him a lot and it was not the right time for all that Gyan. He was doing well.

What do you learn from this?

Let me know what you feel after reading the story of this cab driver? I think that the cab driver did a few things correctly which even many with a lot of privilege fail to do. Like if you see this cab driver, he has a habit of saving some part of his income even though he does not earn as we all do. He had life insurance and health insurance which is really commendable. I know he does not represent an average cab driver from that angle, but still.

Sometime around March of 2010, I was checking my inbox and saw an email from a person from CNBC. The message said that there was an opportunity of me authoring a book on personal finance.

For a moment, I could not believe it.

It was an ecstatic moment for me because I was just 27 yrs old, with 2 yrs of experience in IT industry and 2 yrs of experience running this blog. The world around me was all about python, Perl and servers and here was an email asking me to author a book on money which would be published by CNBC. I was going to be a mini-celebrity and I knew it would be counted as great achievement on my portfolio. This blog was around 2 yrs old at that time.

I replied back that I would surely be interested in this assignment and wanted to know how it works. It was a great coincidence that I had a very rough idea of a book already in place, when I used to fantasize the idea of book writing some day and here was the opportunity knocking my door.

I went to Mumbai, had a quick meet with concerned person and I was all set on the assignment of Book Writing.

Starting of the Book writing journey

The next few days were highly energetic.

I could not believe that I was really writing a book at this age. I had already done more than 300+ articles by that time and had interacted with thousands of investors by that time over comments section of this blog. I had a fair understanding of what kind of book will really help an investor.

I started jotting down all the important points and concepts which I should cover in the book. I thought that writing a book would be easy for me, as I had written so many articles on various concepts already. After all, I just needed to arrange them in a certain manner which looks like a book, change the language of the content to look powerful, add few examples and enough stories to make it interesting and engaging.

I created a Google doc folder and started creating various chapters’ pages. Here is a snapshot of how it looked like finally…

My initial way of planning and thinking about the book was like this…

I thought, if I wrote 10 pages daily, it would just take 25 days to write 250 pages. If I target the book in 30 days, I would still have 5 days left. I added 1 more month as a buffer period to refine my book and make any changes if required. I thought 2 months would be enough.

The book finally took me 500 days

I know what you are thinking right now. I know I so stupid.

As you must have guessed by now, I had done a very poor job in planning and estimating the time required to write a book. I think it’s not even “poor planning”, it was “pathetic planning”.

I over-estimated my capabilities to the highest level. I finally took 1.5 yrs (500 days) to complete the book and now I will give you insights on why it took so long.

Let me share with you that, I was very clear that I don’t want to do a “good book”. I wanted to write an extra-ordinary book, which is relevant for many years to come and truly helps an investor who is new to the world of personal finance.

I had seen some the other books which were written and they all focused mainly on the “knowledge” part of personal finance. Each of those books had information about various financial products, tax saving avenues etc. I think those kind of books have their own importance and are required. However, I didn’t want to write “just another book” on the shelf, which is giving the same information to investor like others.

What kind of book I wanted to write?

I wanted to do a book, which shakes the investor. A book which shows them the mirror and truly makes them understand some really important principles of personal finance. I wanted to do a book which is ACTION oriented, not just information oriented.

I wanted to write a book which wakes up an investor from their sleep and clears their way of looking at their financial life. A book which acts like a big brother guiding them on how to look at their money matters and builds a guideline for them to follow. And I think, I succeeded in what I wanted to do, the proof is 81 reviews on flipkart, with an average rating of 4.4 out of 5

I was like the director of the movie, who had to make sure he casts the right actor, good story, great scenes, and dialogues and at the end, had to connect all these elements and come up with a master piece. Before I move ahead, I would like to check out a review by “Saravanan A” on amazon. It captures the essence of the book beautifully

I started writing the book

When I finally started writing the book, I started building the book skeleton.

I prepared the chapter names and just wrote down what each chapter will talk about. Trust me it sounds very simple, but it took me over a month to just do that part in proper manner. Write one article was easy, but how do I write a book which is 100X times an article? At the same time it had to be interesting, outstanding, full of examples, insightful and had to have a strong flow at the same time. The book was suppose to make sure it hooks the reader till end.

It was not an easy job

I first created the list of chapters, and the number went upto 22 in numbers. There was so much to write in each chapter. I started with first chapter, then 2nd and then 3rd …

Gggrrrr…….

I realized, that I have done everything wrong. After I did 50-60 pages, everything I did looked so damn bad to me. I was not happy with it.

I hit the delete button and all 3 chapters were gone. I realized, I needed to relook at my strategy.

I now started defining the chapter names, sub-topics under each page. I wrote down the headings part of each chapter and what all will go into it. It was like mini-index of the whole book.

This way, it became more easy for me, because now I was actually creating a proper flow and was actually giving the shape to the book. Once I had completed that, I just have to expand each point with 200-300 words and my 800-900 point skeleton book would expand to 100X size and would be a 90,000 words book.

This was a top to bottom approach.

Trust me, it looks the obvious way to write the book NOW. But that time, it didn’t click me. I made a lot of mistakes and lost a good amount of time to just figure out, how to give a good start.

Anyways!

Finally, I ended up with 8 chapters. Some chapters were long, some were very short.

The First Chapter – My best work !

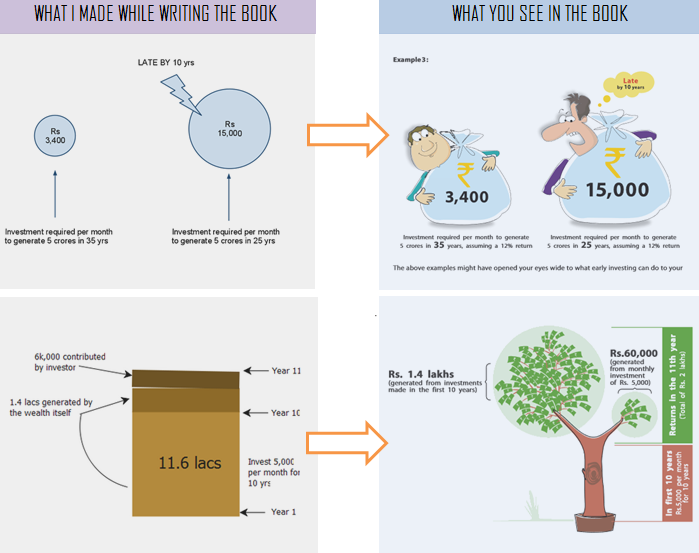

The first chapter I wanted to do was on the topic of early investing.

I was first wondering does this topic deserve a full chapter? After all how long can I write on the point of early investing?

In one line, if you summarize it, it looks like “If you invest early, you can start small , but if you are late, you will have to put more money later to build the same amount of wealth”.

But then were are so many dimensions to this single topic and I was so fascinated with it that I wanted a detailed chapter on this single topic, which is outstanding and goes beyond the simple conversation.

I wanted to give examples, real life analogies and enough data as the backup to prove my point. I found out that though the starting the chapter was very tough, it was not that tough later. Once I was in the flow, I started enjoying the book. I could visualize how a reader will feeling while reading it. What kind of questions they will have and what kind of examples will help them to understand the concept in a better way.

Working in Excel

I did a lot of work on excel, created charts, came up with examples and did a lot of number crunching.

I came up with lots of interesting conversations which would make investors understand the point. I wrote 40+ pages for the first chapter. I read the whole chapter once I completed and I found I can do better, then I went through the chapter, edited it back, and pruned the content, added some more ..

I created the rough sketch of examples and images and the designers at CNBC did an excellent job at recreating nice illustrative pictures which conveyed the same in the book. The eye-catching graphics which they created, increased the richness of the book. Here is a snapshot of what I created and what you see in the book.

I was happy on my achievement

Finally, I was satisfied and happy with my 1st chapter and I was proud of it. I could see the power and impact of the first chapter book on an investors mind.

My goal was simple – “If someone reads my first chapter, he will not delay his investments after that”.

It was as simple as that. Some book readers told me, that they started their SIP just after completing the first chapter, they didn’t even wait for completing the book.

I had done the first chapter in 15 days time and it was the biggest chapter of the book. I recalculated the time I would take to complete the book told CNBC, that I will not be able to complete the book before 6 months. They were happy listening to that 😉 (maybe they knew the reality)

Once I completed the first chapter, I thought of taking the break before I start my 2nd chapter. The short break lasted for 2 months. After working so extensively on the 1st chapter, I was a bit exhausted and was flying high with confidence and every time I thought of returning to the book writing, something or the other came up and made sure I could not concentrate on the book.

My 6 months deadline was about to complete and I was done with just 2-3 chapters only. It was just 40% of the book. For the first time, I was understanding how tough it was to keep your deadlines promises. Whenever someone defined the deadlines for the projects in our projects meetings, I had a dangerous smile on my face.

Finally, I completed the book

Now, let’s cut things short and come to the main point. I finally wrote other chapters on risk and return, insurance, simplicity requirement in next few months.

I also added a chapter called, “Relationship with Money” which touched the point of how our emotions are connected with money and how we see money in our life. It was a very different kind of concept which was introduced by Nandish Desai, my business partner.

So I requested him to write that full chapter because I knew that I will not be able to justify that chapter because of my limited understanding of that subject and I think he did a brilliant job in that. It added a whole new dimension in the overall book and it was aligned with the book mission.

It helped investors to connect with their emotional side of money. Thanks to Nandish to author that chapter (we will soon come up with his 1st book story)

Editing of the Book

Finally, I managed to complete the book in a year. By the time, I completed the 80% part of the book. The editing had started.

I was sending each chapter to CNBC which was now edited by a professional. They checked the whole book for the English language and the sentence duplication. If 3 lines conveyed the same thing, It was merged into one and the sentence was pruned. When the edited version of the chapters came back to me, I was horrified to see how pathetic my English was (I knew it was bad, but SO BAD ?)

With heavy heart when I asked the editor is that was normal? They said – “YES – It was totally normal and it happens with every writer”. I was a happy writer again 🙂

The Polishing of the book content

I saw, how the editor had polished the book language and made it look more professional. They had also suggested some changes (very minor) and I incorporated them. To my surprise, this whole thing again took few months and finally I got one final version of the book to check for one last time before the first print happens.

I started reading the edited version of the book. This was the first time when I was reading my complete book as a reader. That cute little thing as attachment, on my email was one of the most beautiful thing I had seen. I felt like I was a mother who just delivered a baby after 9 months of labor (1.5 yrs in my case).

I started the first sentence, then first page, first chapter … and finally the whole book.

Happy and Proud Moment

I was extremely happy and proud. I could see that the book was able to make an impact. I had taken a lot of time to do the book, but I had not compromised with the content quality. I didn’t write it with rush.

We originally gave the name of the book as “Jagoinvestor”, because the book focus was to wake up an investor and that name looked appropriate, however after an year, we changed the name to “16 personal finance principles every investor should know”, because it was a more clear name and conveyed what the book was all about.

Today when I look back, I am happy that I was successful in writing the book I visualized. As a first time writer, I did a very good job.

The book has been so powerful, that a lot of investors who read my first book suddenly start acting on their financial lives and some even contact us to do their financial planning. Our best clients came to us by reading our books. A lot of investors who are DIY investors, even they get a lot of value from the book.

What I learned by writing the 1st book (and you should know that)?

A book is a creation, which comes into life after a lot of hard work. There are many dimensions which comes together and then a book takes the shape. Writing a book might be easy, but writing a “good book” is not.

When you read any book, if you get one insight or one learning which can impact your life, I think the author has done his job and you have got your value. A book can have some mistakes, some part of the book might not sound great to you, but be thankful for the good part, ignore the average part.

Now when I read a book, I ask myself if I learned any ONE THING from the book or not? If the answer is YES, I consider the book as great. I have stopped criticizing any author (anyways, I never did) because I now know the other side too. I recently read a book called “Predictably Irrational” by Dan Ariely. My god – What a creation ! .. What a book it was .. If only I was 10% of that author, I would have done wonders!.

Share your comment

Let me know what do you think about my journey of writing the book? What did you learn from it? Also share if you have read my first book or not?

Do you want to know how you can take a high health insurance coverage at a cheaper premium, without compromising on the benefits and features? Today I am going to share how you can do that using top-up health insurance policies.

Gone are the day’s when Rs 2-3 lacs of health cover was considered a good cover, its not even average cover these days. With rising health care cost, a health cover below 5 lacs is just not sufficient for most of the people. I am confident on that, because in last 6 months, we have helped more than 1000+ people to take their health insurance and majority of them ended up with a coverage in range of 5-20 lacs.

I know, a lot of investors understand the importance of high health insurance cover, but they are unable to afford a high premium. So what is the alternative?

Use Super Topup Policies to increase your health cover at lower premiums

The solution is Super topup policies.

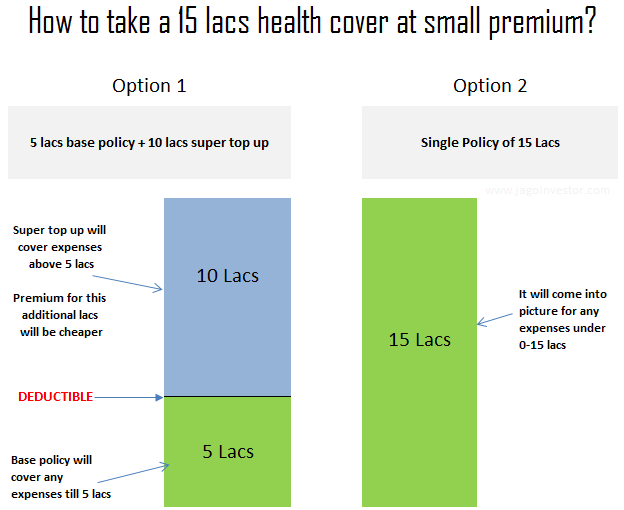

You can use Super Top-up health insurance policies to upgrade your health cover by paying a lower premium. Super Topup plans are the health insurance plans which pays only when a certain threshold is crossed.

For example, consider a super top-up plan for Rs 20 lacs with deductible of Rs 5 lacs.

In this case, the policy will pay only when the initial Rs 5 lacs is paid off and they will pay the additional amount above Rs 5 lacs. So if the claim amount is Rs 12 lacs. The policy will only pay Rs 7 lacs (over and above 5 lacs deductible. If you are new to this concept, we have already explained the topic of super top up in detail here, please read it first.

So how can you use super top up to take a higher cover?

Instead of taking a full cover of X+Y amount, you can take a base cover for Rs X and take a Super topup plan for Y amount with X as deductible. This way you will be covered upto X amount by the base policy and for any claim above Rs X, the super top-up policy will get triggered and come to your rescue.

The main benefit here is that the Super Top-up policies come very cheap and overall your premium will be small.

Example of 3 member family (2 adults below 35 yrs + 1 kid)

Suppose you want to take a high cover like 20 lacs for your family (3 member family). Here you have two choices

Choice 1 : You can take a stand-alone policy of Rs 20 lacs here. If we take an example of Optima Restore Family Floater, the yearly premium would be Rs 23,527.

Choice 2 : As 2nd choice, suppose you the same take the same Optima Restore Family Floater for Rs 5 lacs, which will cost you Rs 12,513 and on top of it, you take a 20 lacs super topup from L&T Medisure Super Top Up with 5 lacs deductible, for which the premium would be Rs 4,389. So the total premium in this choice will be 16,902.

That’s a saving of 28% in premium.

However, note that both the choices will differ with each other, because from features point of view there are a lot of differences in both the choices.

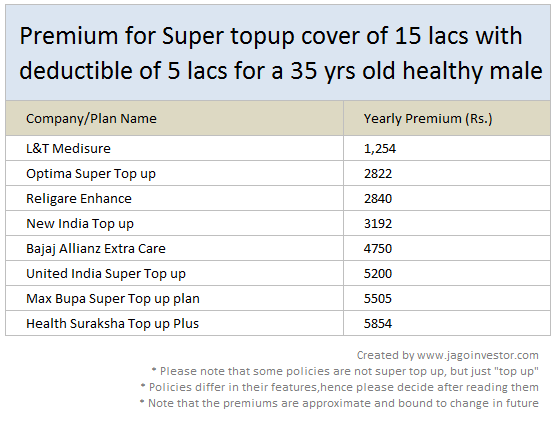

So for those who already have a 5 lacs cover already and wanting to increase their cover to 15 lacs total, below I have listed down some companies top up cover plans and the extra premiums they will have to pay.

Below is an example of how you can increase your health cover from 5 lacs to 15 lacs (or take 15 lacs cover).

Do you have a small health cover right now?

So, ask this question to yourself? Do you have a small health cover of 2 lacs, 3 lacs or max 5 lacs and you want to upgrade it to a big number like 15 lacs or 20 lacs?

For the sake of explanation, let me take an example of 5 lacs existing cover and lets see how you can increase it to 15 lacs for a small premium increase. So all you need to do is take a super top-up cover of 15 lacs with 5 lacs deductible. Below are some plans with the premium amount for a single individual of age 35 yrs.

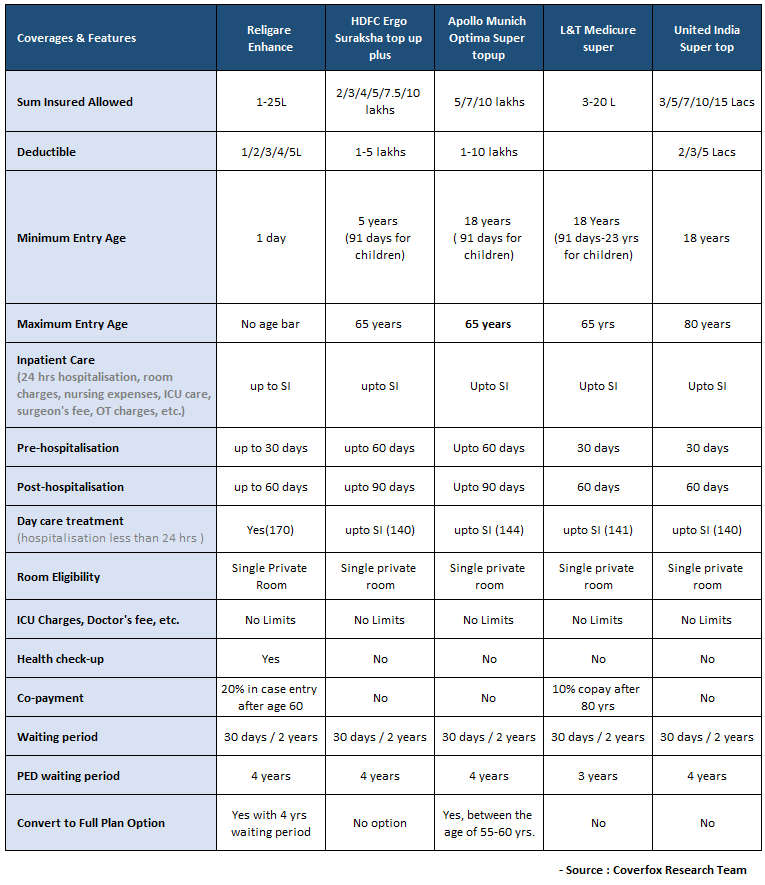

Comparison of Super Top-up Plans in Market?

Below I am sharing the comparison of various super top up plans in the market and how they differ from each other on various parameters.

Why Super top up premium is less?

I am sure many investors will have this question in mind that “Why is the premium for a super top up plan so less?“. The answer is that the probability of a super top up getting triggerred is statistically very less and hence the risk for the insurer is not that high.

Think about it this way. If you have a large cover of 15 lacs right now, what would be the hospital bill on an average? Most of the times, it would be in range of 50,000 to 1 lacs if you get hospitalized for a minor case and few lacs if there is some accident or some major issue.

Only in a very very fatal case or if you are highly unlucky, your bills will run over in the range of 10-15 lacs and thats going to happen once or twice in your lifetime. So the chances for a company paying for a claim above a certain threshold is very less. That’s the reason the premium for a top up plan is less. Higher the deductible, lower the premium.

Is it advisable to buy the base plan and super top-up from the same company ?

The answer is YES. If your base plan and the super top up plans are from the same company, it would surely help because you have to deal with the same company for both the claims. The documentation process is more simple and the communication is smooth. The company will not find any issues because it has all the records with them.

However note that even if you have it from different companies, it’s ok. You ultimately have to look at the features and what combination works best for you and if the total premium is affordable to you or not.

What are Convertible Top-up plans ?

Lately, a new kind of top up called as convertible topup plans are coming up in market.

“Some companies offer Super Topup plans with an additional feature that allows the plan to be converted into a base plan. This is done by buying out the Deductible in the plan.

For instance, if you have your company health insurance for Rs. 3 Lakhs you could buy a Topup of Rs. 15 Lakhs with a deductible of Rs. 3 Lakhs. In case you leave this employer, and/or are without cover, you can apply for buying out the deductible at the time of renewal by paying additional premium. There are certain conditions/triggers based on which this feature gets activated into the plan.

This is an excellent feature for people who feel that they would be working with employers who will provide health insurance cover all their working life, without any break.

For instance,

In case of Religare Enhance – The convertible feature gets activated after 4 continuous renewals. The plan has a waiting period of 1 year for Pre-existing diseases

In case of Apollo Optima Super – The option is available for customers who have bought the policy before crossing the age of 50 years. The option can be opted between the age of 55 and 60 years at the time of renewal by paying additional premium, if the policy has been renewed continuously without break. “

Who all should buy a super top up plan ?

Those who are having a small cover by themselves or a group cover through their employer and want to increase their cover (ideally you should have a base policy for a minimum amount)

Those who are right now having a small cover and want to upgrade it

Those who can take care of small medical bills themselves (like up to 2-3 lacs) and only want help in case of bills beyond that number by paying a small premium

Other Important Points related to Super top-up plan

A super top up policy can be taken stand alone – A super top up policy can be taken without a base policy. There is no compulsion that you should hold a base policy.

Premiums will rise as per age slab – You should be aware that just like a normal health insurance plan, a super top up plan premium will also rise as per age slab in coming years, so even if the premiums look very small right now, it’s bound to increase later

No Claim Benefit not present – Generally super top up plans do not offer No Claim Bonus (NCB) . This is the primary difference between taking a base cover of a high amount and combining a small cover with top up cover, because then you loose on the benefits of a No Claim Bonus over the years.

Not always a great option – Just because the premium is less, it does not mean that combining a small base cover with a super top up is always the best plan. Depending on situation, you need to find out if its a good option in your case or not. It might happen that you might loose out on some benefit and feature on the top up plans

I hope this article helped you to understand how you can increase your health cover at a small premium. Please ask your questions if any below in comments section

Do you know, which is the one thing – which is responsible for making financial lives complex these days?

The answer is – LACK OF CLARITY!

Most of the investors take wrong decisions in their financial lives and regret later about it. However, I want to assure you that by the time you complete reading this article, you will learn how to take better financial decisions and lead a simpler financial life.

Each financial decision you take has some pros and cos and some advantage or disadvantage. Some decisions will put pressure on your cash flow and some will make you rich in eyes of society, while some will create assets for you and some will destroy your net worth.

And finally, decisions will give you peace of mind and some make your life hell.

Some examples of decisions which investors have to make !

Should I prepay the home loan or invest it?

Should I buy that plot or not?

Should I take 2nd property or put the money in mutual funds?

Should I buy the higher end model of the car or the lower one?

Should I change my job for higher salary or be in my comfort zone?

Should I give 1 lac to my friend as loan or make some excuse?

Should I buy the 2 bhk or 3 bhk?

Should I keep so much money in FD or invest in the 2nd house?

Did I make a mistake by spending so much on myself? Am I selfish?

I must acknowledge that its always going to be tough, to take a decision. But can we do something which can simplify the process of decision making and give us a framework using which we can quickly decide and take things to next level.

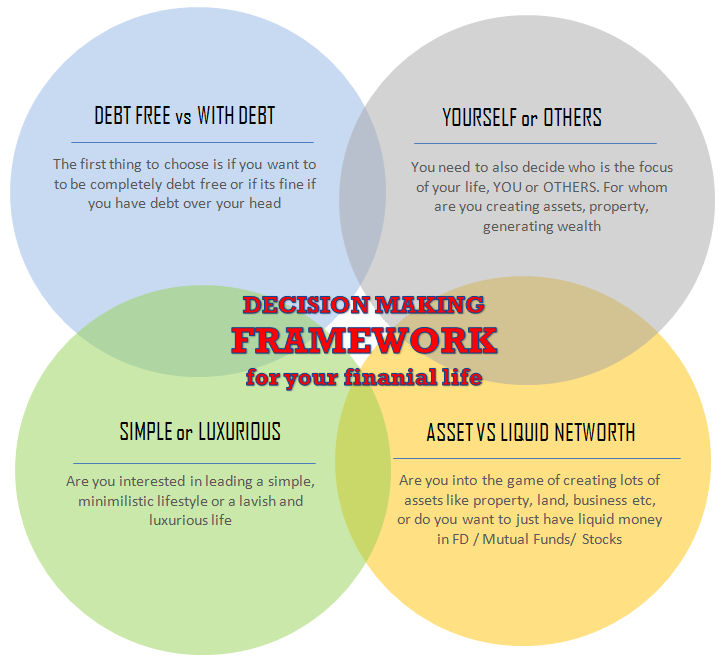

4 point Decision Making Framework

Let me introduce you to the concept of “decision-making framework”, which I recently invented and to test its effectiveness, I ran a survey which was taken by around 132+ people online. I will share the results with you below shortly.

Below are the 4 points which I have included in the decision-making framework.

What is decision-making framework?

Like you saw above, a decision-making framework is nothing but few choices which you make before hand. So whenever you need to take some major financial decision involving money, you can check if it’s aligned with your overall decision-making framework and vision for yourself. You can check if the decision will take you closer to your goals in life or take you farther!

So now, let’s dive deeper into each point and you decide for yourself which side you fall into.

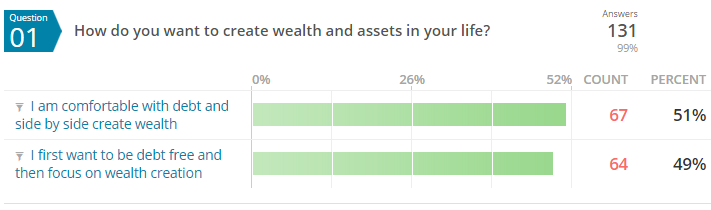

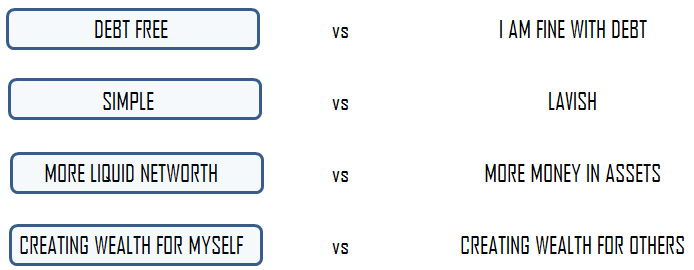

1. Debt Free or With Debt – What is your priority ?

The first point in your decision-making framework is if you want to lead a debt free life or if you are comfortable with debt and side by side you are creating your wealth.

This question is very important to answer because debt trap has destroyed many lives and made some really amazing people slaves in today’s world. So a person wanting to be debt free asap, keeps getting into debt because each opportunity looks so promising that they are attracted towards it and even though it does match with his vision in life, they still fall in.

Note that I am not taking about the first home loan you take in your life. No matter how much logic I put in, I think in today’s times, there is a very high chance that most of the people will end up with a home loan at least even if they want to be debt free. So for the sake of this 1st point in the framework, we will allow one home loan and nothing more than that.

So if you look at the other side, a lot of people after they have taken the first home loan, keep taking additional loans for 2nd house, 2nd car, plot loan, loan against property or topup loan and keep giving away their salary in EMI and keep making assets on the side.

While this is not an issue as such, but the problem happens when you realise that you wanted to debt free long back, but have spent all your life living in the pressure of EMI’s and never felt that independence of not having debt on your head.

Let’s see what most of the people choose out of the two choices.

As per the survey, it was a big tie between the two choices and almost 50% people said that they want to take the route of debt free life asap, but the other half were fine with the debt in their life while they create the wealth on the side. I am sure these are the investors who have a strong predictable income structures and safe job which gives them the confidence to say that. Below are the results

Real life example when it becomes tough to choose

Imagine you have taken a home loan which is 50% complete. You are regularly taking all the efforts to prepay your loan and because of your extreme focus, the loan will soon complete (in few years). You also have few lacs in your bank account accumulated from last few years which you wanted to keep as surplus funds and are now planning to repay the home loan further and that will almost make you debt free.

BANG!

Now suddenly you come across an amazing flat/plot which sounds like an amazing opportunity and you start visualizing how this can be an amazing addition to your portfolio. How after few years you will make 100% profit on it. You visit the site, the sales guy tells you about the amenities, location, the future prospects of the property and now you don’t want to miss the offer.

Your spouse is already happy and proud of you making further real estate investment.

You were closer to get debt free, but you again get into that debt trap, because this offer comes and now you are on the way to take another loan to fund the purchase of a new property. On one side, you are so happy, but on the back of your mind, you are worried if something happens to your job, will you be able to handle the EMI for another so many years? You are worried if the new property didn’t turn out to be that great, then what?

You are worried, if it really really makes sense to buy something which you will use after many years? What if it didn’t fetch you good rent?

Truly speaking, there is no right or wrong decision of the above problem, but your decision has to align with what you wanted in your life and hence you should before hand if leading a debt free life is bigger priority or not.

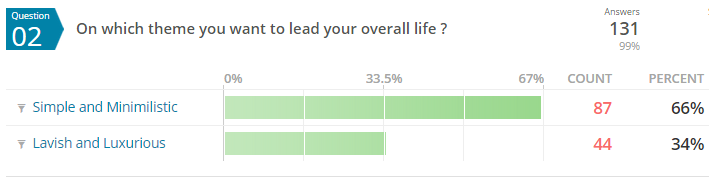

2. Simple or Luxurious – What will be theme of your lifestyle?

The next thing which I feel should be part of your decision-making framework is a clear choice between what kind of lifestyle do you want to lead? Will it be simple, plain, minimilistic or a lavish and luxurious one?

I know some people will say, they want a balanced life which has a mix of simplicity and luxury both? I get that !. But there is always one of these dominating one, which will be the major part, we are talking about that here. Its totally ok to choose to live a simple life, which occasionally has luxury in it or vice versa. But the theme has to be clearly defined for you and your family.

When I asked this same question in our survey, around 66% people said that their life theme has to be simple and minimalistic and 34% said they wanted it to be lavish and luxurious.

Let’s not judge people on this parameter. I am sure a lot of people who want to choose luxury theme deserve it and are working hard for it. It’s a choice of leading a life, after all it’s one life and when will you not live like a king if not right now at this moment.

On the other hand, there are people who are very uncomfortable with lavishness and want their life to be simple and plain. These people also spend a lot of money on few things they love and they become spendthrift at various points of their life. I am on of them.

Both the themes discussed above are RIGHT, and we never know why people choose the theme they are choosing. It all depends on how they have lived their lives till date, what is their outlook towards life, their past experience with money, the struggles they have seen in their life and what kind of people they associate with. There are too many dimensions to it

Why choosing your theme is important?

So that when a big purchase comes, you can see if it fits your theme or not?

So that you can choose which car to buy?

So that you can choose how much furnishing to do at your newly bought home?

So that you can decide if you want to buy a premium villa or a normal 2 bhk house.

So that you can decide where you want to give the kids birthday party.

I am associated with both type of people in my life. One of my friends bought 70 lacs home and did a 25 lacs of interior (his house is awesome), while the other friend bought a 35 lacs home and bought minimal furniture and setup, but he has bought a high-end camera which is very very expensive.

Its not about show-off

A lot of people might feel that those who want to lead a life of luxury want to impress others and show off, but let me make it clear that it’s not like that. It is how those people want to spend their life on this planet which is anyways limited and its very natural. Just because you are not like that, does not make the other person wrong.

So, if you have made the choice of lavish living as your theme, then “to hell” with those friends who keep saying why you should save for future. Spend yourself like a king, earn more and spend more on yourself, buy awesome clothes, go on exotic tours, travel like there is no tomorrow. But be clear that you wanted it 🙂 and the best part is that you will not be guilty about it. After all, you have chosen your life to be that way.

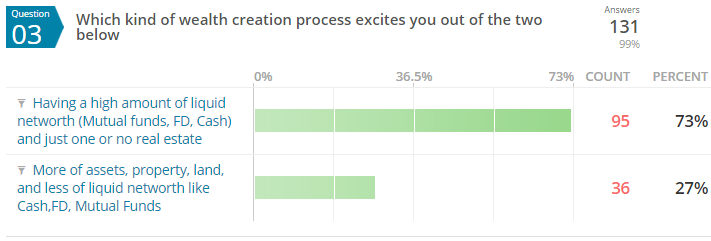

3. Blocked Assets vs Liquid Networth – What excites you?

For those who think a lot of money will solve their struggles, you will be amazed to hear that there are many investors with net worth of 2-3 crores depend on a personal loan if they suddenly need 8 lacs of money and if they suddenly loose their job, they will panic like anyone else, because they are not sure from where the next month EMI is coming up.

Why is it so when their networth is 2-3 crores?

Because, its all blocked and locked in assets which is highly illiquid. If they want to take out the money, it will take many months and years to get the best deal. These investors choose to spread their money across various assets (especially real estate like plot and houses) and anytime they have some cash in their FD or mutual funds, they feel it should be diverted to something concrete which they can touch and feel (even gold is one asset class).

So they keep increasing their networth, but are always low on liquidity. The biggest problem which I feel with these investors is that if some great opportunity comes and knocks their doors, they are so low on liquid money that they cant take advantage of the opportunity and have to take help of loans.

The worst part is that a lot of these investors never wanted things to be like that. But because they never slowed down in their financial lives to think of how it should eventually look like, their financial life took the shape on their own based on circumstances.

Some investors like Liquid money !

Liquid money means the money which can be redeemed very soon, but with fair and decent returns. So A lot of money in mutual funds, fixed deposits and limited money in real estate is what I call as “liquid networth”. In our financial planning terms, Me and Nandish think that having 1 crore in liquid networth has to be one of the primary milestone of every investor.

You will find many investors who are having networth of a crore, but all of it will go away if you take out real estate out of the equation.

So the main question comes – “What excites you more?”

Do you want to create high networth comprising of liquid networth (stocks, mutual funds, FD,Cash + 1 real estate for living purpose) OR you want to be high on real estate, various properties, plots, businesses etc and lower on the liquid networth?

Whatever choice you make, it will help you to take further decision in life which you have to decide where should that Rs 5 lac go which you got as bonus!. I was surprised that 73% people in our survey said that they want high liquid networth (not sure if its because real estate is not doing so well from last 1-2 yrs). Below are the results.

It would be a good exercise to see if your current networth is aligned to your theme or not ?

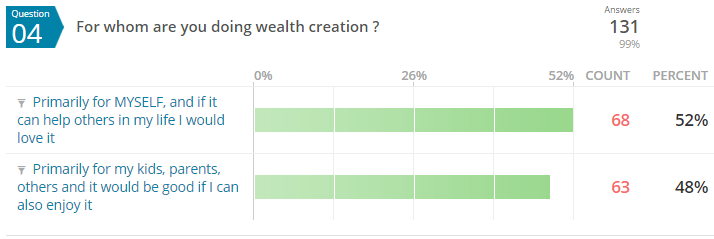

4. Yourself vs Others – For whom are you creating wealth for?

This point if the decision-making framework can be a bit uncomfortable for many investors, because now we are going to be a bit selfish in life here. And the tough question for you all is – “For whom are you earning this money?”

Mainly Yourself + a bit for others in your life (kids, parents, others in life)

OR Mainly Others + a bit for yourself

Our parents created wealth primarily for us – their kids. They earned all their live, but never enjoyed the fruits of their labour. They never gave priority to their desires in life. They never owned a car, so that we can have a bike. They never created their retirement fund, because they were busy funding our post-graduation. They never went for any lavish vacations despite having money because their daughter’s wedding had to be planned years before and the money was to be accumulated.

But this story is taking a new shape in last many years.

I am constantly seeing the shift in mindset. From last 10-15 yrs, the mindset has shifted on “them” to “Me”. from “their needs” to “my wants”. The aspirations have gone 10X high and we want to consume, spend, enjoy, live life in a very different way compared to our past generations.

We have seen many of our clients focusing more on their “Retirement goal” rather their “kids education” or “kids marriage” and to some level I think they are going right.

Kids Education and Retirement

In old days “Kids Education” means “Retirement goal”

You will find various parents today who have hit retirement, have nothing great in networth to talk about and don’t have a penny to feed themselves and there is no help coming from their kids as well for whom they spend all their wealth till date. A lot of parents secretly wonder, if they did the right thing to over think about their kids and others and never thought about their own retirement or aspirations.

But things are changing !

Today, you have to plan both the goals separately and for most of the people its not possible to reach both the goals easily. Kids today have many options like taking education loan (if they are highly smart and crack good institute) or first take a basic job go for higher education few years later using their own money. In fact, many parents are now taking the route of education loan (they help taking it), but finally ask the kids to repay it themselves.

Already a lot of kids are guilty these days that their parents have to spend on their weddings and they want to arrange it all themselves. I know this is a sensitive topic, but this always keeps hiding in every investors mind and no one talks about it.

Spending culture in increasing

These days more and more people are going on exotic vacations abroad and within India, spending more and more money on entertainment, eating out, having great experiences, and spending on possessions. But some people are not able to do that because they are not yet clear if its morally right to do it or not.

Here comes the biggest surprise. Almost half number of people who took the survey chose themselves over others and the other half choose others over themselves.

You have to complete your responsibilities in life

In no way, I mean to say that someone who is choosing themselves as the primary beneficiary of their wealth are running away from their responsibility. You still have to pay your kids school fees, clothes, your parents health expenses. Do all that!, but when you have to choice do a SIP for your retirement and another option is to pay EMI of a second house which you think will help you kids in future, you have to make a clear choice on who will get a bigger pie.

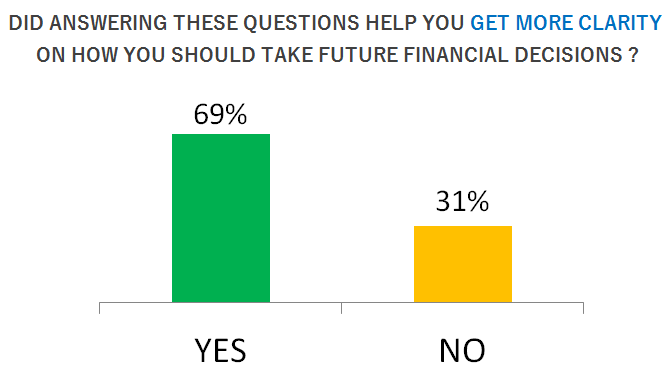

Will this decision-making framework help you ?

Truly speaking, YES and NO both are the answers. This whole exercise is nothing but bringing out your subconscious mindset on paper and make it clear to yourself on what you want your future to be like and how you would like to lead your financial life. You will not get robotic about your decisions, and obviously deviate from these points which you decide by yourself, but at least this will give you a structure to think and act.

At least 69% people who took the survey said that just by answering these 4 questions and choosing their answers helped them realise what really they wanted in life and how they should take their future decisions.

I also now realize, that why we should not think why others don’t act like us and why some are materialistic and others don’t, why some people spend too much on their comfort and some live frugally. Why some people buy too much of real estate and others don’t. Why some people are in rush to close their loans while you might be thinking that they are not taking right decisions.

SO what works for you might not be others priority and does not fit others life. Its important to understand this point and brings maturity in your thinking.

So what is my personal answers for my decision-making framework ?

I thought I will share with you all about my personal answers for these questions above and how I think about my own financial life. Below they are

Understand that the above points are my personal points based on my life experiences and my mindset, you should think that they are better than yours or anyone else. Because of my clarity on above 4 points, I will decide in following manner.

I would like to hear what do you think about this idea and does it make sense to you. Do you feel something like this simplifies the decision making or not? Also please share your personal decision-making framework. What are your answers on these 4 points?

Finally, we are doing our 1st investors workshop in Hyderabad on 1st Nov 2015 (SUNDAY). We started doing workshops few years back, till now we were doing programs in Pune, Mumbai and Bangalore and have trained around 500+ investors till date. It’s time we expand and include more cities, we are excited for our Hyderabad event.

Why you should spend 1 full day with us ?

We always love spending full day with participants, having some amazing conversations around money, how to plan their financial life and how to make things more simple and robust.This one day can bring a real turnaround in any person’s financial life and it can help you get started as an investor. It is our promise you will walk out of the room with a new level of energy and vision as an investor.

Note that no personal finance knowledge is required to be part of this workshop.

You can just skip this article and directlyregister for the workshop(early bird tickets available at discount)

Why we conduct these workshops ?

We do offline workshops so that we can connect with some of our readers at a deeper level, round the year we write articles, reply to thousands of comments and work with a few hundred investors one on one and in that process we learn, grow and expand as an individual.

Workshop gives us an opportunity to share outrageously all the knowledge and experiences that we acquire round the year. The program is an opportunity to get our readers more and more action oriented.

Why you should come for this workshop?

You will learn how to improve your financial life with your current set of resources and income.

You will learn how to plan for your financial life goals

You will interact and learn from other’s people’s financial life

You will dedicate one full day to get better with money management

You will learn to add new dimensions to your financial life

To understand that personal finance can also be fun

To give a whole new direction to your financial life

Below are some of the pictures from our Mumbai Workshop we did recently

It’s time at add Jagoinvestor workshop to your financial journey

It has been a few years now conducting “Design your financial life” workshop and the experience has been amazing. It is a wonderful space to be in, in which the group learns and starts to fall in love with the process of wealth creation. We do not teach tricks and tips to build wealth in fact we help you to discover your own personal process of creating wealth.

This time we want more and more couples to participate so that they can get on same page when it comes to personal finance. It is extremely important that husband and wife both take equal interest when it comes to money management. We are offering special discount to those who want to come with their partner. (You can even come with your parents, siblings or friends and can claim the discount)

The workshop we conduct are highly interactive, it has lots of activities and fun exercises which helps you to discover your relationship with money. The sessions are interactive and very easy to grasp for any kind of investor, beginner or advanced. In short there is something for everyone in this workshop.

Register for Hyderabad workshop on 1st Nov, 2015 (SUNDAY)

The hotel is 5 in walk from Lakdi Ka Pul Railway Station

Lunch and Breakfast is included in the program fees