Jagoinvestor

Jagoinvestor

July 11, 2016

July 11, 2016

Closing your PPF after 5 yrs is possible now [NEW RULES]

Recently the PPF closure rules got changed and now a PPF account can be closed prematurely after 5 yrs itself, but only in some conditions which we will see in this article.

Till now, as per the old rules, the PPF account had a lock-in period of 15 yrs, and in no case, it was possible to close the account other than the death of the subscriber itself.

So death was the only valid reason to close the PPF account before 15 yrs maturity period.

PPF premature closure rules

As per the recent rule change by the govt, PPF closure before 15 years is now possible. You can close a PPF account if it’s at least 5 yrs old, in following 3 cases

Case #1 – Death

If the PPF holder dies, then the account can be closed anytime (even before 5 yrs) and the nominee/legal heirs can claim the amount from Govt.

Case #2 – Life-Threatening illness

The PPF account can also be closed in case, the money is required for curing the serious ailment or life-threatening disease of the following people

- PPF subscriber himself/herself

- Spouse

- Dependent Children

- Dependent Parents

Note that one has to provide the documentary evidence from a competent medical authority. So you will need to share the proof that you need to undergo some big treatment/surgery etc and you will need money for that.

Case #3 – Higher Education

If money is required for the higher education for the PPF subscriber or the minor on whose name the account is opened, then one can pre-close the PPF account. However one has to produce the fee bills and the proof of admission or any other documentary evidence.

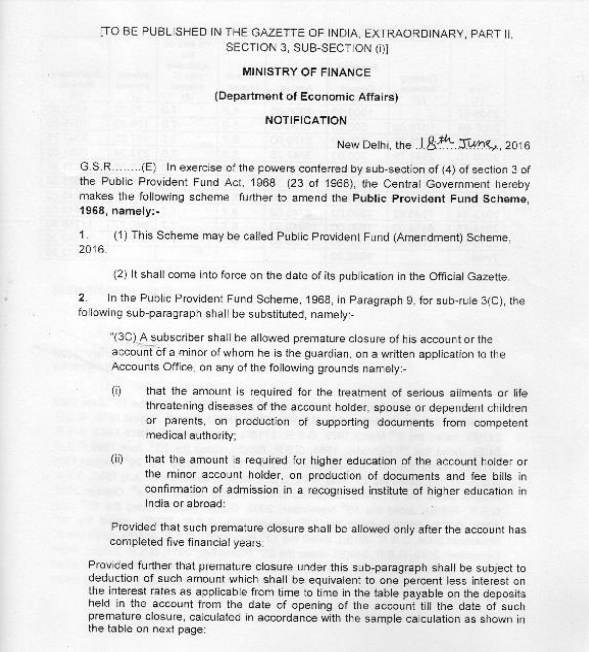

Here are the exact notification wordings

Penalty of 1% when you close PPF account before maturity

This pre-close feature comes with a penalty of 1% of interest for each year. What it means is that for all the years since your PPF account is opened, you will get 1% less interest for each year. So if you earned 8.7% for a particular year, your calculation will be done @7.7% and this way for each period 1% will be reduced.

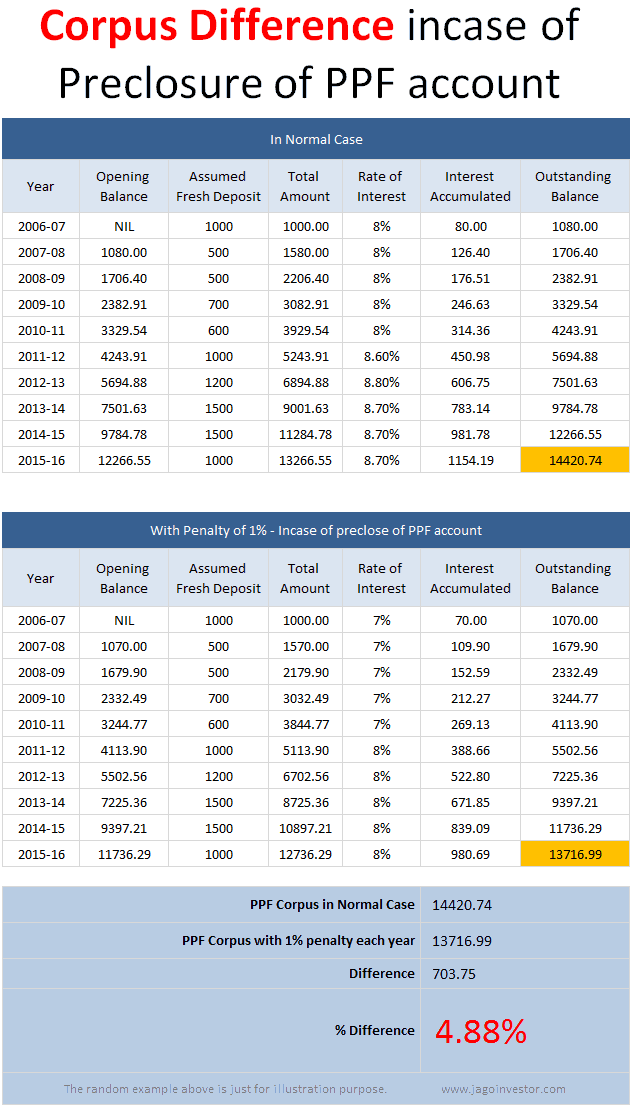

Govt has issued an example calculation for penalty of 1% . But the question now is does 1% penalty mean 1% less amount in final corpus after pre-closure?

No, the answer is 4.88 %!

Yes, You get 4.88% less corpus due to this pre-closure penalty of 1 %. But this is true for that example only which is given by govt in their notification. I went deeper and did the exact calculation and here are the results.

The reason why there is a good amount of difference is that there is the compounding of penalty in this example. If you check the balances in 3rd year, you will see there is difference of 2.1 %. And it keeps on increasing as the number of years increases.

Which means, Older the PPF account, the higher is the final penalty for you.

It does not make a lot of sense to close the PPF account before maturity once 10 yrs is passed, as the penalty will be higher than 4-5% if most of the cases.

PPF pre-closure rule will help investors

PPF is one of the widely popular financial products in India. Majority of families have at least one PPF account and given it’s a long term product, there is a good amount of money lying in it. Now with this new pre-closure rule, an investor gets the benefit of closing the PPF account if they want to do it.

But the only issue is that it’s not an emergency solution to the problem as the documentation requirement is there and being a govt product, you can expect a slow response while closing down the PPF account and using the money.

Please share what do you feel about this new change in PPF closure rules?

i have started my ppf account in 1996 april

then after i extended it for 5 years 3 times

now last 5 years period is april 2021 to april 2026.

now i want to close the account on march 2024.

i know the rules of 1% penalty on premature closer

Question is that 1% cut of from 1996 or 2021

cut from all 28 years or cut of from last 5 years interest?

I guess it will only for the years after your last extention.. So it will be 2021/22/23/24

Is the Premature withdrawl for the higher education is applicable only in respect of the account holder or his / her children also. This is not clear from the language of govt notification. Can any one elaborate.

For his/her children

Manish – i have opened two PPF accounts, one on my name and one for my son. I think i can only have one account either mine or for my son? Is that right? So can i close the PPF account on my name?

No , you can have your own + your son with you as guardian

Nothing wrong !

I want my EPF widraw

Hi balwinder

To withdraw the EPF, you can always fill up the form 19 and submit it to EPFO office. After few months try to follow up with RTI

Manish

Hi sir

I have started working from 2008 till now I have not changed my pf account, this is my 4th company.. can you advise me …

Way forward

This article is all about PPF , not EPF

Sir, Iam presently working for a public sector as an engineer. I started my carrier in July 2010. Planning to resign after Feb 2017. Will i able to get full PF amount(subscription+ contribution) after resignation?

YEs, you will get it

After lapse of 15 years, I extended my PPF account to 5 years 2 times. If I want to withdraw amount in the extended period after giving contributions for 2 years. How much will be the penalty period in this case. Is it for 22 years or will be the last 2 years which is the extended period or else.

Hi Sir,

I am an NRI citizen. I am holding resident savings account in India and not yet converted the account to NRO. The interest earned in this domestic fixed deposits are TDS at 10% . The total income earned in India is less than 1 lakh through bank fixed deposit interest. Also please note that this is the only income I earn in India.

Can I claim the refund while filing the tax returns? Please advise.

I guess yes

Hi Manish,

Just thought will ask another product of govt India recently launched that is sovereign gold bond scheme, could you please explain the details, what are the pros, cons, details how and where to take,?

Thanks ,

Jayatheertha N

What is better PPF or NPS?

and Is premature withdrawal possible in NPS?

And it is compulsory to buy annuity after withdrawals?

Withdrawals is not possible in NPS and you need to buy annuity , its compulsory !

PPF withdrawal by legal heir / nominee in case of account holder’s death was not attracting penalty earlier, does it attracts now .It appears so as per above details .

No it will not attract penalty even now

I have opened PPF account in My Son Name, it is Minor Account. My query here is, once he turn to 18 Years, can we convert that account to his name as a Major? Or we need to close that account and need to open new one?

Read this:

http://jagoinvestor.dev.diginnovators.site/2014/02/5-must-know-rules-before-opening-ppf-account-for-minor-kids.html#.V4ZGc0t97IU

You dont need to do anything once he turns 18. Once he turns 18, he will automatically be the owner of that PPF account and will be able to perform all tasks !

Is the preclosure penalty of 1 % also applicable to the nominees on the death of the PPF holder??

NO , this is not applicable in case of death !

The penalty is just too harsh. Even 5 years is not a short term by any means. Levying such a heavy penalty even after remaining invested for such a long time just isn’t justified. Looks like just another way the government has figured out to loot the common man. They know very well that many people will have to close PPF & withdraw money due to desperate and dire circumstances in life. So, let’s loot them even more in their time of dire need, that’s the motto of the BJP government.

Among the list of reasons, they should add Building a House as well. Isn’t it by far one of the biggest expenses of our lifetime and one that requires us to pool all the resources we have, from wherever possible? Closing PPF to buy a house if most definitely justified.

Earliar this option was not there at all. Now its added. If you feel that penalty is too hard, better not withdraw the money.

“Buying house” option is not there for preclosure, but anyways you can partially withdraw from EPF for that !

Penalty 1% for the whole period is not advisable for premature withdrawal from Public Provident Fund, which results to 4.88% of total investment. Penalty 1% should be from the withdrawing year only , if this new rule continues people will divert their their investments from Public Provident Fund .

Thanks for your comment Ashoke

The penalty is just too harsh. Even 5 years is not a short term by any means. Levying such a heavy penalty even after remaining invested for such a long time just isn’t justified. Looks like just another way the government has figured out to loot the common man. They know very well that many people will have to close PPF & withdraw money due to desperate and dire circumstances in life. So, let’s loot them even more in their time of dire need, that’s the motto of the BJP government.

Among the list of reasons, they should add Building a House as well. Isn’t it by far one of the biggest expenses of our lifetime and one that requires us to pool all the resources we have, from wherever possible? Closing PPF to buy a house if most definitely justified.

Basic concept of the PPF is to generate large sum of money by small savings over the long earning periods for the non-earning days of the retirement. If you do not want to invest in PPF you have other options like ELSS, which has a lock in period of 5 yrs. It’s a good that the government has given facility to withdraw the money for the needy people and not the greedy people. Governments give good interest rate with considering many conditions & one of the conditions is the maturity period, if anybody wants to differ with maturity period for withdrawal are liable to be penalized. You can relate this with housing loan ( fixed interest) where you pay penalty for the premature return. I do not see anything political in this. But greedy people like you will always try to find faults in the others & mislead others.

Greedy? Who is greedy? Trying to withdraw your own hard earned money is not called greed. I didn’t steal someone else’s money & asking for interest on that money. I’m asking for what is rightfully mine. Stop sucking up to the government all the time.

I understand the purpose of PPF but life is full of uncertainties & I may need the money beforehand.

You say the withdrawal option is only meant for the needy. So, you don’t mind the government looting the needy by levying such a high penalty at a time when the person needs the money the most?

Please do not advise youngsters to close prematurely their PPF account. I am 68 year old person who opened fresh second PPF account at the age of 48 years after my first PPF matured and I took the maturity amount. In last 19 years have accumulated about Rs. 28 Lakhs in it. Please note I avoided temptation to withdraw even when financial need. I contribute every year as much as possible. The greatest advantage in PPF is compounding effect and that interest is tax free and even withdrawal is tax free. You get 80 C benefits. I have also invested in stocks myself ( MF is not for me- why should I pay salaries and perks of others?) I am a retired person with modest interest income sufficient for me and my wife . We do not have very big medical insurances. Me and my wife have mediclaim of Rs.1 lakh each which is sufficient if you do not go for 5 star hospital treatment ( which is loot). In case of real need arises I can always withdraw 60% of my PPF balance which is my insurance. Old age mediclaim premiums are costly and waste of money. If hospitals know you have cashless mediclaim of large amount they charge exorbitant. So my advise to youngsters, as far as possibe do not touch your PF and PPF unless it is very very essential. May sound old fashioned

thanks for sharing your life experience – its a great advice. I will surely try to follow this – till now i am tryign to keep my funds diversified but yes a subtantial amount goes for mutual funds. I will now try to increase more into ppf.

Very well said, your experience is shared and is highly appreciated and I take this as an advice. Thanks a lot.

I strongly support your views & advice youth to open PPF account at the early years & continue even after 15 years are completed. I have continued it twice as of today.

You are absolutely right Ganesh. PPF is a long term investment tool and that’s why rules are getting tight for people who want to close the account earlier. I found many people around mixing every investment product together. They just don’t know why they are investing in FD or ULIP or PPF or NPS. Purpose is different for each tool.

PPF can be continued for every 5 years after completion of 15 years. I have already done that.

Why did you open 2nd account instead of continuing with the first ? Let me know if I am missing something here.

Sir, I am not advising them that. I am just reporting the news which came in 🙂

I have PPF Account from seven years. But now PPF is loosing its charm due recent cut in interest rates (8.7 to 8.1). Interest rate of PPF varies according to the inflation.

Thanks for your comment Gaurav

Buying ones own FIRST HOUSE should be added in the conditions to pre maturely close the PPF account…. PPF savings can be a sizeable upfront contribution, down payment to by ones own house…

Sure, let’s add my daughter’s wedding expenses, my son’s LKG donation as well.

Wedding is not a mandatory part of marriage, hence there is no reason to add it as a reason. But can you build a house without a sizable corpus? Taking loan is an option but why do so & pay crazy amount of interest every month when you got the funds in your PPF account?

But you anyways have the option to withdraw from EPF for house 🙂

My EPF is managed by Trust…my employer says EPF can only be withdrawn upon separation…